Polyvinyl Chloride Packaging Film Market Size, Share & Industry Analysis, By Layer Type (Single Layer and Multi-Layer), By Packaging Type (Rigid and Flexible), By End-use Industry (Food & Beverages, Consumer Goods, Healthcare, Personal Care & Cosmetics, and Others), and Regional Forecast, 2026-2034

Polyvinyl Chloride Packaging Film Market Size and Future Outlook

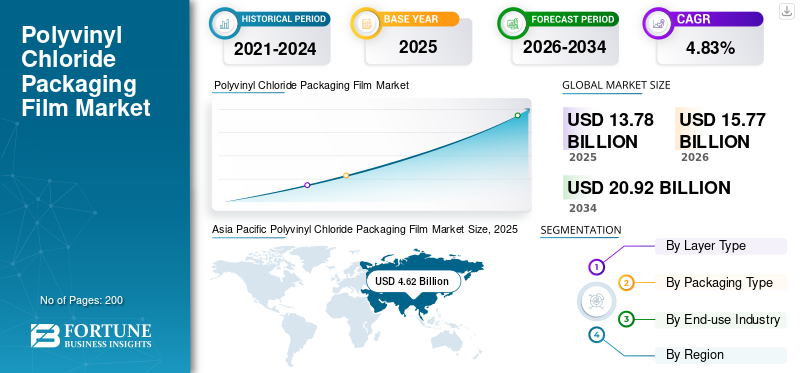

The polyvinyl chloride packaging film market size was valued at USD 13.78 billion in 2025. The market is projected to grow from USD 15.77 billion in 2026 to USD 20.92 billion by 2034, exhibiting a CAGR of 4.83% during the forecast period. Asia Pacific dominated the polyvinyl chloride packaging film market with a market share of 33.53% in 2025.

The market encompasses sectors engaged in the manufacturing, distribution, and application of flexible films made from PVC for packaging purposes. The growing need for affordable, clear, and resilient packaging in the food and consumer goods sectors is propelling the market growth. Additionally, a rise in retail consumption, demand for longer shelf-life, and the expansion of organized packaging and distribution networks on a global scale also boosts market expansion.

Furthermore, many key industry players, such as Amcor Plc, Nan Ya Plastics Corporation, and Klöckner Pentaplast, operating in the market, are focusing on developing innovative products and conducting R&D.

Download Free sample to learn more about this report.

POLYVINYL CHLORIDE PACKAGING FILM MARKET TRENDS

Shift Toward Sustainable and Recyclable PVC Alternatives is a Prominent Market Trend

A significant trend in the market is a slow shift toward more sustainable and recyclable formulations. Manufacturers are progressively investing in bio-based plasticizers, low-toxicity additives, and enhanced recycling technologies to tackle environmental impacts linked to traditional PVC. Regulatory pressures, especially in developed areas, are promoting the use of eco-friendly alternatives and closed-loop recycling systems. Furthermore, brand owners are emphasizing sustainable packaging to fulfill consumer demand, resulting in product innovations that strike a balance between performance, cost-effectiveness, and environmental compliance.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand from Food Packaging Industry is Driving Market Growth

The main factor driving polyvinyl chloride packaging film market growth is its increasing demand from food packaging industry. As modern retail formats expand, there is a rise in consumption of ready-to-eat meals and an increase in the packaging of fresh products, leading to a heightened need for dependable, economical, and sustainable packaging solutions. PVC films offer excellent barrier properties against moisture and contaminants, making them ideal for perishable items. This escalating dependence on packaged food products worldwide continues to maintain a steady demand for the product.

MARKET RESTRAINTS

Environmental and Health Concerns Hamper Market Growth

Concerns related to the environment and health associated with PVC materials serve as a major limitation to market expansion. The growing awareness of plastic waste and possible toxicity has resulted in more stringent regulations, particularly in areas including Europe. Numerous consumers and organizations are transitioning to alternative materials such as polyethylene and biodegradable films. These issues also affect brand image, enabling companies to rethink their use of PVC in packaging. Consequently, the costs associated with regulatory compliance and the threats of substitution are hindering wider acceptance of the product.

MARKET OPPORTUNITIES

Expansion in Emerging Economies Offers Potential Growth Opportunities

Emerging economies offer significant opportunities for the market, driven by swift urbanization, increasing disposable incomes, and development of retail infrastructure. The growth of supermarkets, e-commerce, and cold chain logistics is further amplifying the demand for effective packaging solutions. PVC films, known for their cost-effectiveness and versatility, are ideally suited to meet the needs of these expanding sectors. Moreover, enhancements in local manufacturing capabilities and investments in packaging technologies are anticipated to strengthen supply chain and open new growth opportunities for market players.

MARKET CHALLENGES

Competition from Alternative Packaging Materials Poses a Critical Challenge to Market Growth

One significant challenge confronting market is the rising competition from alternative materials including polyethylene (PE), polypropylene (PP), and biodegradable films. Recent advancements in material science have enhanced the performance attributes of these alternatives, rendering them as suitable substitutes for PVC in numerous applications. Additionally, brand owners and regulatory agencies are promoting the shift toward recyclable and compostable packaging options. This competitive pressure compels PVC manufacturers to engage in ongoing innovation and authenticate their value proposition within an evolving packaging environment.

Segmentation Analysis

By Layer Type

Cost Efficiency, Processing Simplicity, and High-Volume Applicability Drive Single Layer Segment Dominance

Based on the layer type, the market is divided into single layer and multi-layer.

The single layer segment is expected to account for the largest share of the market. The prevalence of the single-layer segment in the market is mainly attributed to its cost efficiency, simplicity in manufacturing, and suitability for high-volume applications. Its sufficient barrier properties and flexibility fulfill the demand for typical applications, including food wrapping, packaging of consumer goods, and industrial purposes. Moreover, increased production speed and compatibility with conventional packaging machinery improve operational efficiency.

The multi-layer segment is expected to grow at a CAGR of 4.28% over the forecast period.

By Packaging Type

Higher Strength, Shelf Appeal Drive Dominance of Rigid PVC Packaging Films

Based on packaging type, the market is segmented into rigid and flexible.

In 2025, the rigid segment dominated the global market. This is owing to its exceptional strength, structural integrity, and capacity to offer improved product protection. Its high clarity and glossy finish enhance product visibility and shelf appeal, which is vital in retail settings. Furthermore, rigid PVC effectively supports thermoforming processes, allowing for tailored packaging designs. These benefits render rigid PVC packaging a favored option for applications that demand durability, safety, and visual appeal.

The flexible segment is projected to grow at a CAGR of 4.01% over the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

High Consumption Volumes, Shelf-Life Requirements, and Retail Expansion to Drive Food & Beverages Segment Growth

Based on the end-use industry, the market is segmented into food & beverages, consumer goods, healthcare, personal care & cosmetics, and others.

The food & beverages segment is expected to hold a dominant polyvinyl chloride packaging film market share over the forecast period. This is due to its significant and ongoing need for safe, hygienic, and effective packaging solutions. PVC films are extensively utilized for wrapping fresh produce, meat, and ready-to-eat products due to their superior clarity, flexibility, and capacity to prolong shelf life by offering moisture and contamination protection. Furthermore, increasing urbanization and evolving consumer lifestyles have resulted in growing demand for food packages, further solidifying the segment’s dominant role in the overall market.

The consumer goods segment is projected to grow at a CAGR of 4.82% over the forecast period.

Polyvinyl Chloride Packaging Film Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

North America

Asia Pacific Polyvinyl Chloride Packaging Film Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the second-dominant share in 2024, valued at USD 3.50 billion, and maintained its leading position in 2025, with a value of USD 3.64 billion. In North America, the market is propelled by a robust demand for convenience food packaging alongside stringent regulatory requirements for food safety and materials. Manufacturers prioritize the production of high-quality, compliant product with enhanced formulations, while the evolving retail and e-commerce sectors persist in fostering steady consumption of packaged products.

U.S. Polyvinyl Chloride Packaging Film Market

Based on North America’s strong contribution the U.S. market was valued at USD 2.86 billion in 2025, accounting for roughly 20.73% of global sales. In the U.S., there is a significant demand for ready-to-eat and convenience foods, which propels the consumption of these products. The presence of advanced packaging technologies, stringent FDA regulations, and a robust retail ecosystem also fosters steady demand.

Europe

Europe is projected to grow at 4.46% over the coming years, the third-highest among regions. The market reached a valuation of USD 2.62 billion in 2025. The market in Europe is predominantly shaped by rigorous environmental regulations and objectives related to the circular economy. The initiative to minimize plastic waste is fostering advancements in recyclable and low-toxicity PVC films.

U.K. Polyvinyl Chloride Packaging Film Market

The U.K. market in 2025 was at USD 0.50 billion, representing approximately 3.61% of global revenues.

Germany Polyvinyl Chloride Packaging Film Market

Germany’s market was valued at USD 0.56 billion in 2025, equivalent to around 4.09% of global sales.

Asia Pacific

Asia Pacific region reached USD 4.62 billion in 2025 and secured the position of largest region in the market. The Asia Pacific region leads in growth driven by swift urbanization, increasing disposable incomes, and a heightened demand for packaged food and consumer products. The development of retail infrastructure and robust manufacturing capabilities in nations such as China and India is enhancing the large-scale production and consumption of affordable polyvinyl chloride packaging films.

Japan Polyvinyl Chloride Packaging Film Market

The Japanese market in 2025 was valued at USD 0.87 billion, accounting for roughly 6.31% of global revenues. In Japan, the demand is influenced by elevated expectations regarding packaging quality, hygiene, and visual appeal. The growing elderly population heightens the need for compact, user-friendly packaged food items, as manufacturers concentrate on precision, high-performance films, and eco-friendly packaging alternatives.

China Polyvinyl Chloride Packaging Film Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 1.48 billion, representing roughly 10.73% of global sales.

India Polyvinyl Chloride Packaging Film Market

The Indian market in 2025 was at USD 1.24 billion, accounting for roughly 8.99% of global markets.

Latin America

The Latin America region is expected to witness moderate growth in this market space during the forecast period. The Latin America market reached a valuation of USD 1.82 billion in 2025. In Latin America, the growth of the market is propelled by the expansion of supermarket chains and a rising demand for cost-effective packaging solutions. PVC films are preferred due to their affordability and adaptability, particularly in food packaging, where economic factors significantly influence the choice of materials.

Middle East & Africa

In the Middle East & Africa, South Africa reached USD 0.28 billion in 2025. The growth of the Middle East & Africa region is bolstered by enhancements in food distribution networks and an increasing demand for packaged and imported products.

Saudi Arabia Polyvinyl Chloride Packaging Film Market

The Saudi Arabian market reached at USD 0.38 billion by 2025, accounting for roughly 2.78% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Launch and Acquisitions by Key Players to Propel Market Competition

The global market has a semi-consolidated structure, with prominent players including Amcor Plc, Nan Ya Plastics Corporation, and Klöckner Pentaplast. The significant market shares of these packaging companies are due to numerous strategic initiatives, including collaborations among operating entities to advance research. They companies are also investing in the research and development contributing to the market growth.

- For instance, in September 2024, Amcor Plc stated the introduction of a new generation of recyclable PVC based packaging films aimed at improving circularity in food packaging applications. This innovation emphasizes the reduction of material thickness while preserving barrier performance and clarity.

Other companies in the polyvinyl chloride packaging films industry include Intertape Polymer Group, TPC Packaging Solutions, and Pactiv Evergreen. These companies are expected to prioritize new product launches, strategic partnerships, and collaborations to increase their global market shares during the forecast period.

LIST OF KEY POLYVINYL CHLORIDE PACKAGING FILM COMPANIES PROFILED

- Amcor Plc (Switzerland)

- Nan Ya Plastics Corporation (Taiwan)

- Klöckner Pentaplast (U.K.)

- Intertape Polymer Group (U.S.)

- TPC Packaging Solutions (U.S.)

- Pactiv Evergreen (U.S.)

- POLIFILM Group (Germany)

- Winpak Ltd (Canada)

- Jindal Chemical (India)

- Avery Dennison Corporation (U.S.)

- AVI Global Plast (India)

- Riflex Film AB (Sweden)

- Hangzhou Haidelong Import and Export Co., Ltd. (China)

- Jagannath Polymers (India)

- Vansh Polyvinyl India Pvt. Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- July 2024: Nan Ya Plastics Corporation increased its production capacity for PVC films in Asia to satisfy the rising regional demand from the food and pharmaceutical industries. This expansion features state-of-the-art extrusion lines designed to enhance product consistency and minimize energy usage.

- May 2024: Klöckner Pentaplast launched a new series of rigid PVC films specifically designed for pharmaceutical blister packaging, which provide superior thermo-formability and enhanced barrier characteristics. This product introduction aims to meet the growing need for secure and tamper-evident packaging within the healthcare industry.

- March 2024: Intertape Polymer Group has finalized the acquisition of a provider specializing in packaging solutions to augment its flexible film portfolio, which includes applications based on PVC. This acquisition improves the company’s technological capabilities and expands its range of products in the food and industrial packaging sectors.

- January 2024: Pactiv Evergreen declared the expansion of its food packaging operations, emphasizing rigid PVC and alternative material trays. This investment encompasses the enhancement of manufacturing facilities to boost output and enhance efficiency. This initiative seeks to address the increasing demand for packaged food items in both retail and foodservice sectors, especially in North America, where the trend of convenience packaging is on the rise.

- November 2023: POLIFILM Group introduced a new series of high-clarity PVC stretch films specifically designed for packaging fresh food. These films provide enhanced cling properties and prolong shelf-life performance, making them ideal for applications involving meat, poultry, and produce. This development demonstrates the company’s commitment to innovation in food-safe packaging solutions, while also responding to customer needs for improved product visibility and minimized waste.

REPORT COVERAGE

The market analysis includes a comprehensive study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.83% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Layer Type, Packaging Type, End-use Industry, and Region |

| By Layer Type |

|

| By Packaging Type |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the market value stood at USD 13.78 billion in 2025 and is projected to reach USD 20.92 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 4.62 billion.

The market is expected to grow at a CAGR of 4.83% over the forecast period of 2026-2034.

By layer type, the single layer segment is expected to lead the market.

The growing demand from the food packaging industry is driving market growth.

Amcor Plc, Nan Ya Plastics Corporation, and Klöckner Pentaplast are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us