Portable Medical Devices Market Size, Share & Industry Analysis, By Product (Diagnostic & Monitoring Devices {Vital Signs Monitoring Devices, Cardiac Monitoring Devices, Blood Glucose Monitoring Devices, and Others}, Therapeutic Devices {Respiratory Therapy Devices, Wound Care Devices, and Others}, Assistive & Mobility Devices, and Others), By Application (Gynecology, Cardiology, Gastrointestinal, Urology, Orthopedics, and Others), By End-user (Hospitals and ASCs, Clinics & Physician Offices, Diagnostic Centers, Homecare Settings, and Others), and Regional Forecast, 2026-2034

Portable Medical Devices Market Size and Future Outlook

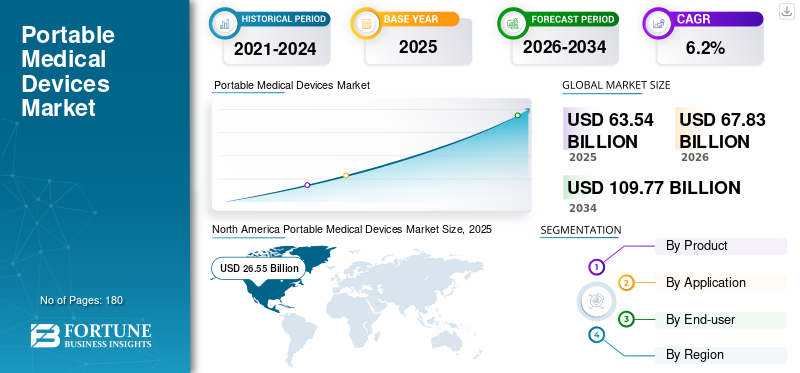

The global portable medical devices market size was valued at USD 63.54 billion in 2025. The market is projected to grow from USD 67.83 billion in 2026 to USD 109.77 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. North America dominated the portable medical devices market with a market share of 41.78% in 2025.

The global portable medical devices market comprises compact, mobile, handheld, wearable, and transportable medical equipment used for diagnosis, monitoring, treatment, rehabilitation, and patient support across hospitals, clinics, diagnostic centers, and homecare settings. These devices include portable monitors, glucose meters, cardiac monitors, portable ultrasound systems, oxygen concentrators, nebulizers, infusion pumps, wound therapy devices, and mobility assistance products.

The market is growing as healthcare delivery moves closer to the patient, especially for chronic disease management, elderly care, and post-acute monitoring. Rising cases of cardiovascular disease, diabetes, respiratory disorders, and mobility limitations are increasing demand for devices that allow faster diagnosis, continuous observation, and care outside traditional hospital settings. The shift toward home healthcare, remote patient monitoring, and outpatient treatment is also encouraging providers and patients to adopt easy-to-use portable solutions.

Medtronic plc, Abbott Laboratories, Koninklijke Philips N.V., GE HealthCare, and Siemens Healthineers AG held the highest market share in 2025, driven by strategic initiatives to expand markets and diversify their portfolios through product introductions.

Download Free sample to learn more about this report.

Portable Medical Devices Market Key Takeaways

- 2025 Market Size: USD 63.54 Billion

- 2026 Market Size: USD 67.83 Billion

- 2034 Forecast Market Size: USD 109.77 Billion

- CAGR: 6.2% from 2026–2034

- North America dominated the portable medical devices market with a 41.78% share in 2025.

- The Diagnostic & Monitoring Devices segment held the largest market share.

- The Hospitals & ASCs segment is projected to account for 33.9% of the market in 2026.

North America

North America led the market with a value of USD 26.55 billion and a 41.78% market share in 2025.

Europe

Europe is projected to reach USD 17.95 billion by 2026, supported by strong healthcare infrastructure and growing homecare adoption.

Asia Pacific

Asia Pacific is projected to reach USD 15.90 billion by 2026 and is expected to be the fastest-growing regional market.

U.S.

The U.S. portable medical devices market is projected to reach USD 25.91 billion in 2026, accounting for approximately 38.2% of global revenues.

Japan

The Japan portable medical devices market is projected to reach USD 2.71 billion in 2026, representing nearly 4.0% of global revenues.

Read More

PORTABLE MEDICAL DEVICES MARKET TRENDS

Shift toward Connected, Wearable, and Patient-Friendly Devices is a Key Market Trend

A major trend in the market is the shift from simple, standalone equipment to connected, wearable, and data-enabled devices. Patients and providers increasingly prefer devices that are easy to use, lightweight, wireless, and capable of transmitting data to clinicians or care platforms. This trend is especially strong in cardiac monitoring, diabetes care, respiratory monitoring, and general patient monitoring. Wearable ECG patches, continuous glucose monitors, smart pulse oximeters, portable multiparameter monitors, and app-connected respiratory devices are helping clinicians track patients more frequently and intervene earlier. Device design is also becoming more patient-centric.

Manufacturers are focusing on smaller form factors, longer battery life, intuitive interfaces, Bluetooth or cellular connectivity, and cloud-based reporting. For hospitals and clinics, connected devices support workflow efficiency and reduce manual documentation. For patients, they improve convenience and encourage adherence.

Another important trend is the blending of hardware, software, and services. Companies are selling devices and offering monitoring platforms, analytics dashboards, subscription services, and remote care support. This is changing the competitive landscape, as value increasingly depends on data quality, interoperability, cybersecurity, and integration with electronic health records. Over time, portable devices are expected to become less episodic and more continuous in their role within patient care.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Chronic Disease Burden is Fueling Market Growth

The growing burden of chronic diseases is driving the global portable medical devices market growth. Patients with cardiovascular diseases, diabetes, chronic respiratory disorders, neurological conditions, and orthopedic limitations often require frequent monitoring, long-term therapy, and repeated follow-ups. Portable devices reduce reliance on hospital visits by enabling timely monitoring and treatment in homes, clinics, ambulatory settings, and emergency settings. This is particularly important for diabetes management, where blood glucose meters, continuous glucose monitoring systems, and insulin pumps support day-to-day disease control.

Similarly, portable ECG devices, Holter monitors, and mobile cardiac telemetry systems are becoming important tools for detecting arrhythmias and monitoring cardiac patients outside hospital walls. Respiratory devices such as portable oxygen concentrators, nebulizers, spirometers, CPAP/BiPAP systems, and portable ventilators are also in increasing demand due to the growing prevalence of asthma, COPD, sleep apnea, and other respiratory disorders. According to the WHO, cardiovascular diseases, chronic respiratory diseases, and diabetes remain among the leading causes of noncommunicable disease mortality globally, reinforcing the need for continuous and accessible care solutions. As health systems aim to reduce admissions, shorten hospital stays, and improve patient outcomes, portable medical devices are becoming a practical and necessary part of modern chronic care delivery.

MARKET RESTRAINTS

High Device Costs and Reimbursement Gaps Limit Adoption

Despite strong demand, the market faces restraints from high device costs, uneven reimbursement, and affordability challenges, especially in price-sensitive regions. Advanced portable devices such as continuous glucose monitoring systems, mobile cardiac telemetry devices, portable ultrasound systems, portable ventilators, infusion pumps, and connected patient monitoring platforms often carry high upfront costs. In addition, many of these devices require recurring expenses for sensors, accessories, software subscriptions, maintenance, calibration, or replacement parts. For hospitals and diagnostic centers, procurement decisions are influenced by budget cycles, reimbursement coverage, and proof of clinical and economic value. In homecare settings, patients may delay or avoid purchasing devices when reimbursement is limited or out-of-pocket spending is high. This creates a clear gap between clinical need and actual adoption.

In emerging markets, the restraint is more visible as healthcare infrastructure, insurance penetration, and distribution networks remain uneven. Even in developed markets, payers increasingly assess whether remote monitoring or home-use devices reduce hospital admissions, improve adherence, or deliver measurable cost savings. If the value proposition is unclear, adoption can slow. Moreover, low-cost alternatives and refurbished devices create pricing pressure for manufacturers, particularly in mobility aids, basic monitoring devices, and respiratory therapy products. As a result, affordability and reimbursement remain critical barriers to broader market penetration.

MARKET OPPORTUNITIES

Home Healthcare and Remote Monitoring are Creating Lucrative Growth Opportunities

The biggest opportunity for portable medical device companies lies in expanding home healthcare, remote patient monitoring, and decentralized care. Healthcare systems are under pressure to manage aging populations, rising volumes of chronic disease, staff shortages, and rising hospital costs. Portable devices directly support this shift by allowing patients to be monitored or treated at home while remaining connected to clinicians. This opportunity is visible across multiple product categories. In diabetes care, continuous glucose monitoring and insulin delivery devices support daily self-management. In cardiology, portable ECG, Holter, and telemetry solutions help identify rhythm abnormalities without long inpatient stays. In respiratory care, oxygen concentrators, CPAP/BiPAP systems, nebulizers, and portable ventilators support patients with chronic respiratory conditions at home. In wound care, portable, single-use negative-pressure wound therapy devices enable treatment beyond inpatient settings.

Regulators have also recognized the importance of non-invasive remote monitoring devices, with the FDA issuing guidance intended to support continued availability and capability of such devices for patient monitoring. Companies that can combine reliable hardware with user-friendly software, patient engagement tools, cloud connectivity, and service support are well-positioned to capture this opportunity. The next phase of market growth is likely to come from integrated solutions rather than standalone devices, particularly in home-based chronic care.

MARKET CHALLENGES

Data Security, Accuracy, and Usability Remain Challenging for Market Expansion

One of the key challenges in the market is balancing convenience with clinical reliability, data security, and usability. Portable devices are often used outside controlled clinical environments, which increases the risk of incorrect usage, poor device placement, missed readings, connectivity failures, and inconsistent patient adherence. For a blood pressure monitor, glucose meter, portable ECG device, spirometer, or oxygen therapy device, small errors in use can affect the quality of clinical decisions. This makes training, device design, and patient support extremely important.

At the same time, connected devices generate sensitive health data that must be protected. As more devices transmit information through mobile apps, cloud platforms, and remote monitoring systems, manufacturers must address cybersecurity, privacy compliance, and data integrity. Interoperability is another challenge. Hospitals and clinicians often use multiple digital systems, and portable device data must fit into existing clinical workflows rather than create additional burden. There is also a growing need to prove clinical value. Providers and payers increasingly expect evidence that portable devices improve outcomes, reduce admissions, or lower total care costs. Companies that fail to demonstrate accuracy, safety, usability, and economic value may struggle to gain trust, reimbursement, and long-term adoption.

Segmentation Analysis

By Product

Diagnostic & Monitoring Devices Dominate as Chronic Diseases Demand Continuous Monitoring

Based on product, the market is segmented into diagnostic & monitoring devices, therapeutic devices, assistive & mobility devices, and others.

Diagnostic & monitoring devices hold the highest portable medical devices market share as they address the most frequent and recurring need in healthcare: measuring patient condition quickly and reliably. Blood glucose monitors, cardiac monitors, pulse oximeters, blood pressure monitors, respiratory monitoring devices, and portable imaging systems are used across hospitals, clinics, diagnostic centers, and homes. Their demand is strengthened by chronic disease management, preventive screening, remote patient monitoring, and post-discharge follow-up.

The therapeutic devices segment is projected to grow at a 6.7% CAGR during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Cardiology Led due to High Disease Burden and Strong Monitoring Needs

By application, the market is segmented into gynecology, cardiology, gastrointestinal, urology, neurology, respiratory, orthopedics, and others.

Cardiology accounted for the highest market share in 2025 as cardiovascular conditions require frequent diagnosis, monitoring, and long-term follow-up. Portable ECG devices, Holter monitors, event monitors, mobile cardiac telemetry systems, blood pressure monitors, and multiparameter monitors are widely used to detect arrhythmias, monitor heart function, and manage high-risk patients. The burden of cardiovascular disease remains substantial worldwide, and it represents the largest share of noncommunicable disease deaths, according to the WHO. This creates steady demand across hospitals, clinics, diagnostic centers, and homecare settings. Moreover, the segment is estimated to hold a 20.0% share in 2026.

The neurology segment is anticipated to grow at a 7.7% CAGR over the forecast period.

By End-user

Hospitals & ASCs Dominated Market Due to High-acuity and Procedural Demand

On the basis of end-user, the market is segmented into hospitals and ASCs, clinics & physician offices, diagnostic centers, homecare settings, and others.

In 2025, hospitals and ASCs held the highest share as they are major purchasers and users of portable medical devices across emergency care, inpatient monitoring, surgery, diagnostics, rehabilitation, and post-operative care. Portable monitors, imaging systems, infusion pumps, respiratory therapy devices, wound care systems, and mobility assistance products are routinely used to support faster decision-making and flexible patient movement within facilities. Furthermore, the segment is set to hold 33.9% share in 2026.

The homecare settings segment is projected to grow at a 7.6% CAGR during the forecast period.

Portable Medical Devices Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Portable Medical Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 24.96 billion, and reached USD 26.55 billion in 2025. North America is expected to grow steadily, driven by its mature yet innovation-driven healthcare ecosystem. The region has high adoption of portable monitoring, diabetes care, cardiac monitoring, respiratory therapy, and home healthcare devices. The large chronic disease burden, robust reimbursement infrastructure, hospital-at-home programs, and broader adoption of remote patient monitoring support growth. The U.S. remains the main revenue contributor due to high healthcare spending, rapid adoption of connected devices, and a strong presence of major medical technology companies.

U.S. Portable Medical Devices Market

In 2026, the U.S. is anticipated to reach USD 25.91 billion, accounting for approximately 38.2% of global revenues.

Europe

Europe is projected to record a 5.5% growth rate during the forecast period, the second-highest globally, reaching USD 17.95 billion in 2026. Europe’s growth is driven by an aging population, established healthcare infrastructure, strong public healthcare access, and increasing preference for home-based and outpatient care. Countries such as Germany, France, the U.K., Italy, Spain, and Scandinavia have a broad adoption of portable diagnostic, monitoring, respiratory, mobility, and rehabilitation devices. The region also benefits from demand for cost-efficient care delivery, as healthcare systems try to reduce hospital stays and manage chronic disease patients outside inpatient settings.

U.K. Portable Medical Devices Market

The U.K. market is projected to reach USD 2.86 billion in 2026, representing approximately 4.2% of global revenues.

Germany Portable Medical Devices Market

Germany's market is expected to reach USD 3.93 billion in 2026, accounting for approximately 5.8% of global revenues.

Asia Pacific

In 2026, the Asia Pacific market is projected to reach approximately USD 15.90 billion, making it the third-largest market worldwide. Asia Pacific is expected to be the fastest-growing region, supported by a large patient population, rising healthcare expenditure, expanding access to private healthcare, and increasing diagnosis of chronic diseases. China, India, Japan, Australia, and Southeast Asia are all contributing to demand, though for different reasons. China and India offer large volume opportunities due to diabetes, cardiovascular disease, respiratory disease, and expanding hospital and homecare infrastructure.

Japan Portable Medical Devices Market

Japan is projected to generate approximately USD 2.71 billion in 2026, representing nearly 4.0% of global revenues.

China Portable Medical Devices Market

China’s market is anticipated to reach around USD 6.21 billion in 2026, accounting for nearly 9.2% of global revenues.

India Portable Medical Devices Market

India’s market is expected to reach approximately USD 2.13 billion in 2026, accounting for around 3.1% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to witness moderate growth, with the Latin America market estimated to reach approximately USD 3.09 billion in 2026. Latin America is expected to grow at a moderate pace, supported by rising chronic disease prevalence, gradual improvements in healthcare infrastructure, the expansion of private healthcare, and increasing demand for affordable, portable diagnostics and monitoring devices. Brazil and Mexico are the key markets due to their large populations, higher healthcare spending compared with many neighboring countries, and growing demand for diabetes care, cardiovascular monitoring, respiratory therapy, and mobility support devices.

The Middle East and Africa region is expected to grow from a smaller base, supported by healthcare infrastructure investment, rising chronic disease burden, expanding private healthcare, and increasing demand for portable care in underserved areas. The GCC countries are the largest contributors in the region, driven by government healthcare modernization, medical tourism, expansion of mandatory insurance, digital health adoption, and strong hospital investment.

GCC Portable Medical Devices Market

In 2026, the GCC market is estimated to reach approximately USD 1.12 billion, representing around 1.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Initiatives by Key Players to Improve Their Market Positions

The global portable medical devices market is moderately fragmented, spanning several distinct product families, including portable monitoring, diabetes care, respiratory therapy, imaging, drug delivery, wound care, and mobility assistance devices. Key medtech companies such as Medtronic plc, Abbott Laboratories, Koninklijke Philips N.V., GE HealthCare, and Siemens Healthineers AG hold strong positions due to broad product portfolios, global distribution networks, regulatory expertise, and established hospital and homecare relationships.

At the same time, the market includes many other players, such as DexCom, Inc., ResMed Inc., OMRON Healthcare Co., Ltd., and F. Hoffmann-La Roche Ltd. These players often compete on price, local distribution strength, and product availability. Overall, the competitive landscape is shifting from standalone device sales toward connected, patient-centric, and homecare-enabled solutions, with larger companies likely to strengthen their positions through portfolio expansion, partnerships, and acquisitions.

LIST OF KEY PORTABLE MEDICAL DEVICE COMPANIES PROFILED

- Medtronic plc (Ireland)

- Abbott Laboratories (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- DexCom, Inc. (U.S.)

- ResMed Inc. (U.S.)

- OMRON Healthcare Co., Ltd. (Japan)

- Hoffmann-La Roche Ltd. (Switzerland)

- Baxter International Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Medtronic plc received FDA clearance for MiniMed 780G integration with Abbott’s Instinct sensor and approval for use in type 2 diabetes, broadening its automated insulin delivery ecosystem.

- April 2025: Dexcom, Inc. received FDA clearance for Dexcom G7 15-Day, extending wearable CGM duration for adults with diabetes.

- September 2024: Solventum launched V.A.C. Peel and Place Dressing, an all-in-one extended-wear dressing designed to simplify negative pressure wound therapy application.

- April 2024: GE HealthCare launched Caption AI on the Vscan Air SL wireless handheld ultrasound system to help clinicians capture diagnostic-quality cardiac images at the point of care.

- April 2024: Baxter International Inc. received U.S. FDA 510(k) clearance for the Novum IQ large volume infusion pump with Dose IQ safety software, expanding the Novum IQ connected infusion platform.

- February 2024: Butterfly Network launched Butterfly iQ3 in the U.S., introducing a smaller handheld ultrasound probe with enhanced imaging and 3D imaging capabilities.

REPORT COVERAGE

The portable medical devices market report provides a comprehensive analysis of all market segments, outlining key growth drivers and emerging trends. The report also provides opportunities, restraints, and challenges influencing the industry. In addition, it offers detailed insights into technological advancements, major industry developments, recent product launches, market share analysis, and in-depth profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product |

|

| By Application |

|

| By End-user |

|

|

By Region

|

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 63.54 billion in 2025 and is projected to reach USD 109.77 billion by 2034.

In 2025, the market value in North America stood at USD 26.55 billion.

The market is expected to exhibit a CAGR of 6.2% during the forecast period of 2026-2034.

The diagnostic & monitoring devices segment led the market by product.

The key factor driving the market is the rising chronic disease burden.

Medtronic plc, Abbott Laboratories, Koninklijke Philips N.V., GE HealthCare, and Siemens Healthineers AG are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us