Preclinical Imaging Market Size, Share & Industry Analysis, By Type (Hardware [Instruments {Optical Imaging, Nuclear Imaging, Micro-MRI Systems, Micro-CT Systems, Ultrasound Imaging, and Others} and Consumables] and Software), By Application (Oncology, Cardiology, Neurology, Infectious Diseases, and Others), By End User (Pharmaceutical and Biotechnology Companies, Academic & Research Institutes, Contract Research Organization (CRO), and Others), and Regional Forecast, 2026-2034

Preclinical Imaging Market Size & Industry Overview

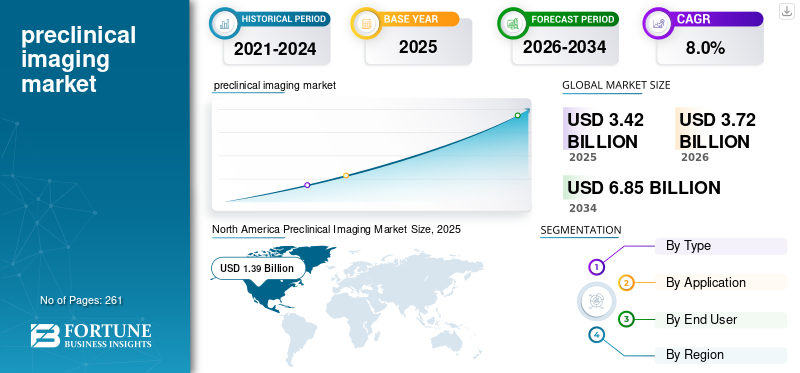

The global preclinical imaging market size was valued at USD 3.42 billion in 2025 and is projected to grow from USD 3.72 billion in 2026 to USD 6.85 billion by 2034, exhibiting a CAGR of 8.0% during the forecast period. North America dominated the preclinical imaging market with a market share of 40.64% in 2025.

Preclinical imaging is a non-invasive research and diagnostic technique that enables longitudinal monitoring of disease progression and therapeutic response, which is crucial for drug discovery and translational research. The rising prevalence of chronic diseases, including cancer, diabetes, and cardiovascular disorders, is further driving preclinical research and development and drug discovery activities, thereby boosting the adoption of preclinical imaging devices and software in the market. This, along with a growing number of clinical studies, is contributing significantly to the growth of the market.

- For instance, according to the 2025 data published by the International Diabetes Federation (IDF), approximately 590 million people were living with diabetes globally.

Furthermore, increasing technological advancements, including improved spatial resolution and broader multimodal capabilities, are driving the focus of key companies, including FUJIFILM Corporation and Bruker, and are expected to support market growth.

Download Free sample to learn more about this report.

Preclinical Imaging Market Key Takeaways

- 2025 Market Size: USD 3.42 billion

- 2026 Market Size: USD 3.72 billion

- 2034 Forecast Market Size: USD 6.85 billion

- CAGR: 8.0% from 2026–2034

- North America dominated the preclinical imaging market with a 40.64% share in 2025.

- The oncology segment held the largest share of 38.3% in 2025.

- The software segment is projected to grow at a CAGR of 8.5% during the forecast period.

North America

North America maintained its leading position, reaching USD 1.39 billion in 2025.

Europe

Europe is projected to grow at a CAGR of 7.1% and reach USD 0.99 billion by 2026.

Asia Pacific

Asia Pacific is expected to reach USD 0.89 billion by 2026, making it the third-largest regional market.

U.S.

The market is projected to reach USD 1.35 billion by 2026, accounting for approximately 36.4% of global sales.

Japan

The market is estimated to reach USD 0.16 billion by 2026, representing around 4.2% of global revenues.

Read More

Preclinical Imaging Market Trends

Expansion of Advanced Optical Imaging to Amplify Product Demand

Advanced optical imaging is emerging as a major trend in the market as researchers increasingly utilize fluorescence and bioluminescence imaging to study disease biology, monitor tumor growth, track cells, and evaluate therapeutic response in live small-animal models. The trend is primarily driven by the technology’s benefits in real-time imaging, non-invasive, high sensitivity, and compatibility with longitudinal study workflow.

Additionally, accessibility across different research settings, from large imaging setups to smaller biotech teams, makes optical imaging a practical molecular imaging tool for high-throughput preclinical studies. This, along with the growing focus of key companies on acquisitions and collaborations with other companies, is likely to fuel demand for the product.

- For instance, in February 2024, Bruker acquired Spectral Instruments Imaging LLC, a company in preclinical in-vivo optical imaging systems. This acquisition fills a gap in its technology and product portfolio within the Bruker BioSpin Preclinical Imaging (PCI) division, broadening its range of preclinical solutions for disease research.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Rising Preclinical R&D and Drug Discovery Activity to Fuel Market Growth

The rising number of preclinical biomedical research and drug discovery activities is a major contributing factor to the growth of the global market. Pharmaceutical and biotechnology companies, contract research organizations, and academic institutes are focusing on investments in early-stage research to identify potential drug targets, evaluate therapeutic efficacy, and generate improved translational evidence before entering clinical trials. Along with this, increasing demand for preclinical imaging systems such as optical imaging, PET, SPECT, micro-CT, micro-MRI, and ultrasound is also expected to contribute to market growth, as these platforms enable researchers to monitor disease progression, biodistribution, and other critical parameters.

- For instance, in January 2025, the National Institutes of Health (NIH) invested USD 48.0 billion in medical research aimed at enhancing health outcomes and reducing illness and disability.

Additionally, continued growth in biopharma funding initiatives and increasing new drug approvals are leading sponsors to sustain or expand upstream research capacity. Therefore, the factors mentioned above, along with the growing focus of key companies towards R&D activities to launch innovative products, are anticipated to boost the adoption rate, thereby contributing to the global preclinical imaging market growth.

Other Prominent Drivers

- Growing demand for non-invasive imaging technologies

- Expansion of drug discovery pipelines

Market Restraints

High Cost Associated with Technologically Advanced Systems and Software to Hamper Market Growth

There is a growing demand for these systems due to their advantages, including non-invasive operations and others. However, the high cost associated with technologically advanced equipment and software is anticipated to hamper the penetration rate for these systems, especially in developing countries, including Brazil, India, China, and others.

The high capital cost represents a huge expenditure, especially for mid-sized and small-sized healthcare facilities. Furthermore, additional costs associated with advanced imaging technologies, including periodic maintenance, software upgrades, or calibration of this equipment, further contribute to the financial burden.

- For instance, according to 2025 data published by Medilex LLC, it was reported that the price of optical coherence tomography (OCT) systems ranges from USD 35,000 to USD 100,000.

Moreover, limited healthcare infrastructure, software, and maintenance expenses, along with financial sustainability, are expected to hamper the adoption rate of this technology in the market.

Market Opportunities

Technological Advancements to Create Market Opportunities

There is a growing focus on the incorporation of technological advancements in this equipment across the market. Technological advancements, including the integration of multimodal systems, AI-assisted imaging analysis, and others, are expanding access and utilization volumes for the identification and evaluation of potential drug candidates.

These innovations are improving study quality, enabling longitudinal study designs, and strengthening translational relevance from preclinical models to clinical development. At the same time, advancements in AI-enabled image reconstruction, radiomics, and multimodal imaging analysis are enhancing the quantification of complex datasets, which increases the value of imaging in oncology, cardiology, neurology, and infectious disease research. Therefore, these advancements are opening opportunities for companies and software providers to position premium devices around sensitivity, throughput, automation, and integrated analytics.

- In April 2026, Exactice Medical, Inc. collaborated with ImSonic Medical, Inc. to complete advanced prototype development of its AIM device, the imaging and transseptal access solution, designed to make transseptal procedures faster, safer, and more cost-effective.

Market Challenges

Limited Diagnosis in Developing Nations to Hamper Market Growth

There is an increasing focus on initiatives among governmental organizations to contribute to rising research and development activities in the biopharmaceutical sector. However, there is a limited availability of advanced devices, limited professional expertise and awareness, reduced utilization rates, coupled with inadequate research funding, especially in emerging countries.

In many lower-resource countries, the healthcare infrastructure is still underdeveloped, which slows procurement and makes it challenging for academic institutions, CROs, and research centers to justify investment in high-end preclinical systems, thereby limiting market growth.

- For instance, according to 2024 data published by the Radiological Society of North America, it was reported that there is less than one CT scanner per million inhabitants in LMICs.

PRECLINICAL IMAGING MARKET SEGMENTATION ANALYSIS

By Type

Increasing Number of Preclinical Studies Fueled Hardware Segment Growth

Based on type, the market is classified into hardware and software. The hardware segment is further classified into instruments and consumables. Instruments are further subdivided into optical imaging, nuclear imaging, micro-MRI systems, micro-CT systems, ultrasound imaging, and others.

The hardware segment held the largest share in 2025. The growth is due to the increasing number of preclinical studies among researchers, resulting in a rising focus of key companies on launching novel systems.

- For instance, in September 2023, Revvity launched three systems, including the next-generation IVIS Spectrum 2 and the IVIS SpectrumCT 2 imaging systems, further elevating versatility and sensitivity standards in in vivo optical imaging.

To know how our report can help streamline your business, Speak to Analyst

The software segment is expected to grow at a CAGR of 8.5% over the forecast period.

By Application

Growing Prevalence of Chronic Conditions Boosted Oncology Segment Growth

Based on application, the market is segmented into oncology, cardiology, neurology, infectious diseases, and others.

The oncology segment held the dominant share of 38.3% in 2025 due to the rising prevalence of chronic conditions, including various forms of cancer. This results in a rising number of preclinical studies to study the potential candidate worldwide, thereby contributing to the adoption rate of these devices in the market.

- For instance, according to 2025 statistics published by the American Cancer Society, about 2.0 million new cancer cases occurred in the U.S.

The cardiology segment is set to flourish with a growth rate of 7.3% during the forecast period.

By End-user

Increasing Number of R&D Activities Encouraged the Pharmaceutical and Biotechnological Segment Growth

Based on end user, the market is fragmented into pharmaceutical and biotechnology companies, academic & research institutes, Contract Research Organization (CRO), and others.

The pharmaceutical and biotechnology companies segment dominated the market in 2025. The increasing number of R&D activities, rising adoption of preclinical imaging devices and software, and the growing number of pharmaceutical and biotechnological companies are some of the crucial factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold an 42.4% share by 2026.

- For instance, according to 2026 statistics published by Cross River Therapy, it was reported that there are about 5,000 pharmaceutical companies in the U.S.

The Contract Research Organization (CRO) segment is projected to grow at a CAGR of 8.8% during the forecast period.

Preclinical Imaging Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Preclinical Imaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 1.29 billion, and also maintained its leading share in 2025, with USD 1.39 billion. The increasing prevalence of chronic conditions, growing number of preclinical studies, advanced healthcare infrastructure, technological advancements in preclinical imaging devices, and strong pharmaceutical R&D investments are some of the factors supporting the growth of the market.

- For instance, according to 2024 data published by the Centers for Disease Control & Prevention (CDC), the prevalence of inflammatory bowel disease (IBD) ranged between 2.4 and 3.1 million among patients in the U.S.

U.S. Preclinical Imaging Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is expected to reach around USD 1.35 billion by 2026, accounting for roughly 36.4% of global sales.

Europe

Europe is projected to record a growth rate of 7.1% in the coming years, which is the second-highest among all regions. The region is likely to reach a valuation of USD 0.99 billion by 2026, supported by research institutions in the region.

U.K. Preclinical Imaging Market

The U.K. market is estimated at around USD 0.15 billion by 2026, representing roughly 4.1% of global revenues.

Germany Preclinical Imaging Market

Germany’s market is projected to reach approximately USD 0.22 billion by 2026, equivalent to around 5.8% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.89 billion by 2026 and secure the position of the third-largest region in the market. The fastest growth in preclinical studies, expanding healthcare capacity, and rising healthcare access are likely to support market growth. In the region, India is estimated to reach USD 0.10 billion by 2026.

Japan Preclinical Imaging Market

The Japanese market is estimated at around USD 0.16 billion by 2026, accounting for roughly 4.2% of global revenues. Japan has historically reported a relatively growing number of preclinical studies, with a strong focus on the expansion of R&D facilities globally.

China Preclinical Imaging Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.29 billion, representing roughly 7.9% of global sales.

India Preclinical Imaging Market

The Indian market is estimated at around USD 0.10 billion by 2026, accounting for roughly 2.7% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.18 billion by 2026, driven by a gradual increase in public healthcare investment across the region.

The Middle East & Africa region is also expected to grow with a considerable growth rate due to rising R&D activities among key companies in the market. In the Middle East & Africa, the GCC is set to reach a value of USD 0.14 billion by 2026.

South Africa Preclinical Imaging Market

The South African market is projected to reach around USD 0.03 billion by 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Key Players Focus on Launching New Devices to Boost Their Market Share

FUJIFILM Corporation and Bruker are the major companies in the market. A significant product portfolio, coupled with a strong focus on strategic initiatives worldwide, is one of the prominent factors supporting the dominance of these companies in the market. Moreover, the growing focus of key companies on the introduction of new devices is likely to boost their global preclinical imaging market share.

- For instance, in June 2025, FUJIFILM Corporation launched the multi-modal Vevo F2 LAZR-X20 Photoacoustic Imaging Platform. The system features high-powered, intelligent laser technology for advanced tissue characterization with high anatomical accuracy for preclinical animal models.

Other key players, including Revvity and others, are also growing in the market, primarily owing to their growing focus on acquisitions and collaborations among other players to strengthen their presence in the market.

List of Key Preclinical Imaging Companies Profiled

- FUJIFILM Corporation (Japan)

- Bruker (U.S.)

- Revvity (U.S.)

- Mediso Ltd. (Hungary)

- Siemens Healthineers (Germany)

- Miltenyi Biotec (Germany)

- MILabs B.V. (Netherlands)

- MR Solutions (U.K.)

- Trifoil Imaging LLC (U.S.)

- Aspect Imaging Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Mediso Ltd. announced that the nanoScan 7 Tesla (7T) PET/MRI preclinical imaging system was officially installed and operational in the U.S.

- September 2025: Revvity opened its new In Vivo Imaging Center of Excellence in Morrisville, North Carolina, the heart of the state’s Research Triangle.

- September 2025: Revvity launched its Living Image Synergy AI multimodal analysis software for in vivo imaging researchers.

- April 2025: Revvity launched the VivoJect Image-Guided Injection System as part of its distinguished cancer research and discovery portfolio at the AACR Annual Meeting 2025.

- September 2023: Revvity launched QuantumTM GX3 microCT structural imaging solution with increased resolution and speed for both in vivo and ex vivo imaging, designed to facilitate researchers studying disease biology or evaluating and fast-tracking therapeutic candidates.

- September 2022: PerkinElmer, Inc., launched the Cellaca PLX Image Cytometry System, a benchtop platform that enables researchers to assess multiple Critical Quality Attributes (CQAs) of cell samples in a single automated workflow, including cell identity, quality, and quantity.

REPORT COVERAGE

The report provides a detailed global preclinical imaging market analysis and focuses on key aspects such as leading companies and market segmentation, including type, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Application, End User, and Region |

| By Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.42 billion in 2025 and is projected to reach USD 6.85 billion by 2034.

In 2025, the North America regional market value stood at USD 1.39 billion.

Growing at a CAGR of 8.0%, the market will exhibit steady growth over the forecast period (2026-2034).

By type, the hardware segment led the market.

The introduction of novel devices is one of the major factors driving the market's growth.

FUJIFILM Corporation and Bruker are the major players in the global market.

North America dominated the market.

The growing number of preclinical studies is anticipated to drive the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us