Propylene Glycol Market Size, Share & Industry Analysis, By Source (Petroleum Based and Bio Based), By End Use (Polyester Resins, Industrial & Heat Transfer Fluids, Cosmetics & Personal Care, Pharmaceuticals, Food & Beverage, and Others), and Regional Forecast, 2026-2034

Propylene Glycol Market Size and Future Outlook

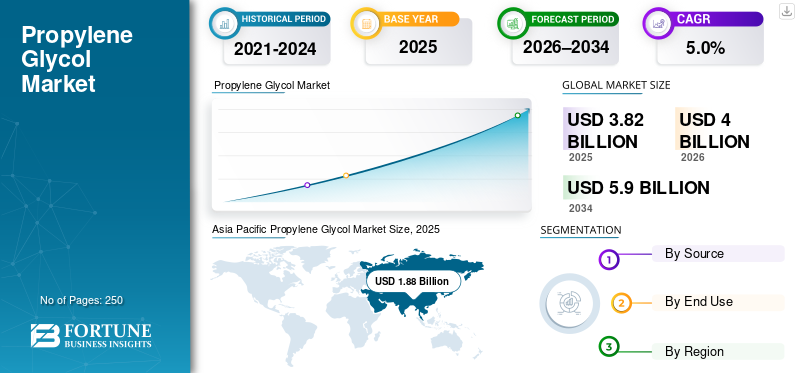

The global propylene glycol market size was valued at USD 3.82 billion in 2025. The market is projected to grow from USD 4.00 billion in 2026 to USD 5.90 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the propylene glycol market with a market share of 49.21% in 2025.

Propylene glycol (PG) is a versatile organic compound used as a solvent, humectant, antifreeze agent, heat-transfer medium, and chemical intermediate across a wide range of end-use industries. Its low toxicity, hygroscopic nature, and chemical stability make it suitable for regulated and human-contact applications such as food & beverage, pharmaceuticals, and personal care, while also supporting large-volume industrial uses, including polyester resins and functional fluids. Market growth is supported by rising consumption in personal care and pharmaceutical formulations, steady demand from polyester resin production, and gradual penetration of bio-based propylene glycol. However, overall expansion remains moderate due to maturity in bulk industrial applications.

Large, integrated chemical producers with strong access to propylene oxide feedstocks, global manufacturing footprints, and diversified end-use exposure dominate the market. Key producers such as Dow, LyondellBasell, BASF, SKC, Shell Chemicals, and AGC Inc. maintain strong positions through backward integration, scale efficiencies, and long-term supply relationships with downstream customers.

Download Free sample to learn more about this report.

Propylene Glycol Market Key Takeaways

- 2025 Market Size: USD 3.82 Billion

- 2026 Market Size: USD 4.00 Billion

- 2034 Forecast Market Size: USD 5.90 Billion

- CAGR: 5.0% from 2026–2034

- Asia Pacific dominated the propylene glycol market with a 49.21% share in 2025.

- The petroleum-based segment accounted for the largest market share in 2025.

- The cosmetics & personal care segment is projected to register the fastest growth during the forecast period.

Asia Pacific

Asia Pacific led the global market with a value of USD 1.88 billion in 2025.

North America

North America accounted for USD 0.68 billion in 2025.

Europe

Europe reached USD 0.90 billion in 2025 and is projected to expand at a 4.3% CAGR during the forecast period.

U.S.

The market is estimated at USD 0.63 billion in 2026, accounting for approximately 16% of global revenue.

Japan

Rising demand for high-quality personal care products and sustainable chemical solutions is driving propylene glycol market growth.

Read More

PROPYLENE GLYCOL MARKET TRENDS

Rising Adoption of Bio-Based and Low-Toxicity Glycols is a Key Market Trend

End-use industries are increasingly favoring propylene glycol over ethylene glycol due to its lower toxicity profile, particularly in applications involving ingestion, skin contact, or inhalation. This trend is most pronounced in food & beverage, pharmaceuticals, cosmetics, and personal care formulations. In parallel, bio-based products are gaining traction despite their smaller base, supported by sustainability commitments from brand owners and regulatory encouragement of renewable chemical inputs. Bio-based product is projected to grow faster than petroleum-based propylene glycol, reflecting increasing sustainability-driven adoption. Companies such as ADM, Corpus Naturals, and ORLEN have already integrated bio-based PG into their product portfolios to gain a long-term competitive advantage.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Broad Demand from Polyester and Unsaturated Polyester Resins to Drive Market Growth

The global market will be driven by broad-based demand for unsaturated polyester resins (UPR), which are widely used in construction, composites, and infrastructure projects. UPR is commonly used in the manufacture of fiber-reinforced plastics (FRPs), which are essential for pipes, tanks, and structural panels in construction and infrastructure. The steady growth in urbanization and increasing construction spending in developing economies, particularly in the Asia Pacific region, are major drivers. PG is a critical component in producing high-performance UPRs, particularly for molded products and coatings, and is often preferred for superior chemical resistance and structural strength. Hence, the high demand from the construction and composites sector will ensure that UPR remains a primary consumer of industrial-grade PG, supporting the global propylene glycol market growth.

MARKET RESTRAINTS

Feedstock Price Volatility and Mature Industrial Demand May Limit Market Expansion

Despite its broad application base, the global market faces structural constraints stemming from volatility in raw materials and maturity across several industrial segments. Pricing and margins are closely tied to propylene oxide and upstream petrochemical markets, exposing producers to fluctuations in crude oil prices and refinery operating rates. This volatility can compress margins, particularly in price-sensitive industrial applications such as antifreeze and polyester resins. Additionally, demand growth in bulk industrial segments is relatively mature, limiting rapid volume expansion. In these applications, customers prioritize cost efficiency over performance differentiation, restricting opportunities for premium pricing. These factors collectively moderate overall market growth, even as regulated and specialty end uses continue to expand steadily.

MARKET OPPORTUNITIES

Growing Adoption of Bio Based and Pharma Grade Glycol to Create Lucrative Opportunities

Bio based propylene glycol represents a clear long-term growth opportunity as sustainability requirements intensify across the consumer, pharmaceutical, and food industries. Although the segment accounted for a smaller share of the total market value in 2025, it is projected to grow faster than petroleum-based grades. This growth is supported by renewable feedstock availability, carbon-reduction initiatives, and increasing customer willingness to adopt sustainable alternatives. Additionally, pharmaceutical and personal care applications continue to offer incremental upside due to an aging population, rising healthcare spending, and expanding demand for safe formulation ingredients. Suppliers that can deliver high-purity, bio-based, and compliant grades are well-positioned to capture this higher-value growth.

Segmentation Analysis

By Source

Petroleum Based Segment Dominated Due to Cost and Scale Advantages

Based on source, the market is segmented into petroleum based and bio based.

The petroleum based segment accounted for the largest global propylene glycol market share in 2025, supported by established production infrastructure, large-scale capacity, and cost competitiveness. These grades remain the preferred choice for high-volume applications such as polyester resins, antifreeze formulations, and industrial heat-transfer fluids. Its broad adoption across major PG application areas and its cost-effectiveness will maintain the segment’s dominance throughout the forecast period.

The bio based segment is anticipated to be the fastest-growing source category, with a CAGR of 8.0% in the coming years. Growth is driven by rising adoption in regulated and sustainability-driven applications despite its higher cost base. Over time, increased scale and feedstock optimization are expected to improve competitiveness. This renewable, low-toxicity alternative offers similar performance to its synthetic counterpart while significantly reducing carbon footprints by nearly 65%.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Polyester Resins Led Demand Due to Large-Volume Industrial Consumption

By end use, the market is segmented into polyester resins, industrial & heat-transfer fluids, cosmetics & personal care, pharmaceuticals, food & beverage, and others.

The polyester resins segment accounted for the largest share, reflecting the product’s critical role as an intermediate in unsaturated polyester resin production. Applications in construction materials, automotive components, marine composites, and corrosion-resistant industrial products drive demand. The segment’s growth remains moderate and is closely linked to broader construction and industrial activity. Despite maturity, polyester resins continue to anchor demand for baseline products due to their large-volume, formulation-critical nature.

Cosmetics & personal care, and pharmaceuticals represent higher-growth, regulated end-use segments. These segments benefit from the product’s low toxicity, solvent properties, and regulatory acceptance for skin-contact and ingestible applications. Cosmetics & personal care is the fastest-growing end-use segment and is expected to rise at a 5.5% CAGR, driven by rising demand for skincare, haircare, and hygiene products.

The pharmaceuticals segment is expected to rise at a CAGR of 5.3%, driven by growing use as excipients and carrier fluids.

Propylene Glycol Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Propylene Glycol Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching USD 1.88 billion, and is projected to grow to USD 1.98 billion in 2026. The region’s leadership is supported by large-scale polyester resin production, expanding industrial activity, and rising consumption of personal care and pharmaceutical products across China, India, and Southeast Asia. Asia Pacific also benefits from cost-competitive manufacturing and strong downstream integration with the construction and automotive industries. Aligning regulations with global safety standards further supports growth in regulated applications such as food, cosmetics, and pharmaceuticals.

China Propylene Glycol Market

Based on Asia Pacific’s strong contribution and China’s manufacturing strength, the China market is recorded at USD 0.96 billion in 2026, accounting for roughly 24% of global revenues.

India Propylene Glycol Market

The India market is expected to reach USD 0.37 billion in 2026. India’s market is driven by rising consumption in pharmaceuticals, personal care products, food processing, and industrial heat-transfer applications. Expanding healthcare infrastructure, increasing domestic manufacturing, and growing use of processed foods continue to support product demand.

North America

North America was valued at USD 0.68 billion in 2025 and remains a significant regional market. North America’s market is supported by strong demand from the pharmaceutical, food processing, and industrial fluids sectors. The region benefits from advanced chemical manufacturing infrastructure and stringent regulatory oversight, which favor the use of PG over higher-toxicity alternatives. North America is also a leading adopter of bio based propylene glycol, driven by sustainability initiatives and corporate decarbonization goals.

U.S. Propylene Glycol Market

The U.S. market in 2026 is estimated at USD 0.63 billion, accounting for approximately 16% of global revenues.

Europe

Europe was valued at USD 0.90 billion in 2025 and is projected to grow at 4.3% over the coming years. The region represents a mature, technology-driven market characterized by strong demand from cosmetics, pharmaceuticals, and food applications. The region’s emphasis on chemical safety, consumer protection, and sustainability continues to favor the use of products over alternative glycols. Increasing interest in bio-based chemicals further strengthens long-term market fundamentals.

Germany Propylene Glycol Market

The Germany market is expected to reach USD 0.21 billion in 2026, equivalent to around 5% of global revenues. A strong chemical industry, an industrial manufacturing base, and the pharmaceutical and personal care sectors support the country’s demand. Polyester resin production and industrial heat-transfer applications also contribute to steady consumption, while sustainability initiatives support the gradual uptake of bio-based grades.

U.K. Propylene Glycol Market

The U.K. market in 2026 is expected to reach USD 0.14 billion, accounting for roughly 3% of global revenues. Growth is supported by demand from the pharmaceutical, food processing, personal care formulations, and industrial maintenance sectors. Regulatory alignment with EU chemical safety standards continues to favor market growth.

Latin America

Latin America reached an estimated market valuation of USD 0.21 billion in 2025. Polyester resin production, industrial fluids, and food processing applications support the regional demand. Growth remains moderate and is closely tied to construction, automotive, and industrial activity, with replacement-driven demand playing a significant role.

Brazil Propylene Glycol Market

The Brazil market in 2026 is expected to reach USD 0.12 billion, accounting for roughly 3% of global revenues. Brazil’s market growth is supported by industrial applications, food processing, and personal care products, supported by Brazil’s large consumer base and manufacturing sector.

Middle East & Africa

The Middle East & Africa’s estimated market valuation was worth USD 0.14 billion in 2025. Industrial fluids, petrochemical processing, and growing pharmaceutical and food applications lead the region’s demand. Infrastructure development and gradual expansion of regulated consumer markets continue to support long-term growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Feedstock Integration and Regulatory Compliance Define Competitive Strength

The propylene glycol market is characterized by large, integrated chemical producers with strong feedstock access, scale efficiencies, and global distribution networks. Competitive positioning is driven by production economics, supply reliability, and the ability to deliver multiple purity grades for industrial, food, pharmaceutical, and cosmetic applications. Key players include Dow, LyondellBasell, BASF, SKC, Shell Chemicals, and ADM. Petrochemical majors dominate petroleum based propylene glycol through backward integration into propylene oxide, while ADM maintains a differentiated position in bio based propylene glycol. Companies that combine regulatory compliance, cost competitiveness, and sustainability-aligned product portfolios continue to strengthen their market position.

LIST OF KEY PROPYLENE GLYCOL COMPANIES PROFILED

- ADM (U.S.)

- AGC Inc. (Japan)

- BASF SE (Germany)

- Dow (U.S.)

- LyondellBasell Industries (Netherlands)

- Manali Petrochemicals Limited (MPL) (India)

- ORLEN Południe (Poland)

- Shandong Runde Import & Export Co., Ltd. (China)

- Shell Chemicals (U.K.)

- SKC Co., Ltd. (South Korea)

KEY INDUSTRY DEVELOPMENTS

- December 2025: ADM expanded its bio based propylene glycol production capacity in North America to address rising demand from food, pharmaceutical, and personal care customers seeking renewable and low-carbon glycols. The expansion strengthens ADM’s position in regulated and sustainability-driven applications, particularly in markets with stringent environmental and safety standards.

- July 2025: Manali Petrochemicals Limited (MPL), part of AM International, Singapore, announced a major capacity expansion plan of propylene glycol by 50 kilotons, increasing its total production capacity to 72 kilotons after completion of the expansion project.

- November 2024: Clariant has announced plans to expand its storage capacity for recycled mono propylene glycol (MPG) in Scandinavia to support increased use in aircraft deicing fluids. The company has installed two additional storage tanks along with a dedicated truck unloading station at its Uddevalla facility in Sweden, enhancing storage capacity and improving product handling efficiency.

- May 2024: Dow planned a capacity expansion of its propylene glycol (PG) at its integrated manufacturing facility in Map Ta Phut, Rayong, Thailand. Under this expansion plant, the company will increase its production capacity by 80 kilotons/year, bringing its total output capacity to 220 kilotons/year.

REPORT COVERAGE

The global propylene glycol market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. This market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.0% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Source, End Use, and Region |

| By Source |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.82 billion in 2025 and is projected to reach USD 5.90 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 1.88 billion.

Recording a CAGR of 5.0%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The polyester resins end use segment led the market in 2025.

Strong demand for polyester and unsaturated polyester resins is expected to drive market growth.

Dow, LyondellBasell, BASF, SKC, Shell Chemicals, and AGC Inc. are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Rising adoption of bio-based and low-toxicity glycols to drive production adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us