Propylene Market Size, Share & Industry Analysis, By Derivative (Polypropylene, Propylene Oxide, Acrylonitrile, Acrylic Acid, Cumene, and Others), By Application (Packaging, Automotive, Construction, Consumer Goods, Electrical & Electronics, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

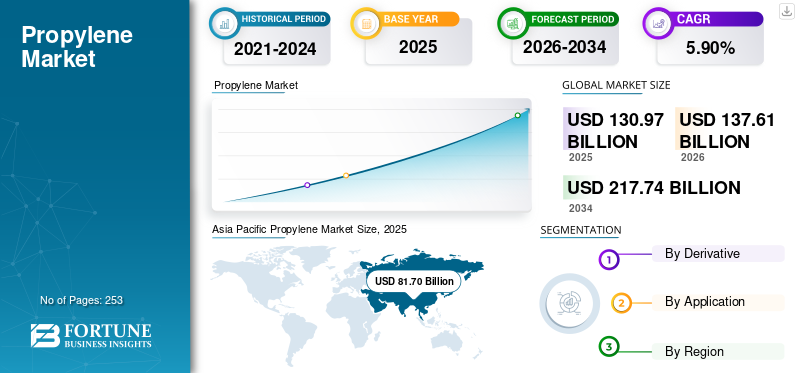

Propylene Market Size and Future Outlook

The global propylene market size was valued at USD 130.97 billion in 2025. The market is projected to grow from USD 137.61 billion in 2026 to USD 217.74 billion by 2034, exhibiting a CAGR of 5.90% during the forecast period. Asia Pacific dominated the propylene market with a market share of 62.38% in 2025.

Propylene, also known as propene, is a colorless, flammable gas produced through petroleum refining and natural gas processing. It is an important building element in the manufacturing of many chemical compounds, such as Polypropylene (PP) plastics, propylene oxide (used to make polyurethane plastics), acrylonitrile, and others. The product is widely used in industries such as automotive, construction, and packaging due to its adaptability and importance in the manufacturing of a wide range of commonly utilized goods.

Many key industry players, including China Petrochemical Corporation, SABIC, LyondellBasell Industries Holdings B.V., ExxonMobil, Reliance Industries, operating in the market, are focusing on developing innovative products to meet the increasing demand.

Download Free sample to learn more about this report.

PROPYLENE MARKET TRENDS

Shift Toward On-Purpose Propylene Production is the Latest Market Trend

A defining structural trend in the global market is the increasing shift toward on-purpose propylene production, particularly through Propane Dehydrogenation (PDH) technology. Traditionally, propylene was produced primarily as a co-product of steam cracking and refinery operations, meaning its supply was closely tied to ethylene demand and fuel production economics. This dependency often led to supply volatility, as product output fluctuated in response to unrelated downstream dynamics.

The expansion of PDH capacity represents a strategic move to decouple propene production from ethylene and refining cycles. PDH units convert propane directly into propylene, allowing producers to respond more specifically to product demand trends. This shift enhances supply predictability and enables greater operational flexibility, particularly in regions with access to competitively priced propane feedstock.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Need for Lightweight and Sustainable Packaging Solutions to Boost Market Growth

The global propylene market growth continues to gain strong momentum from the packaging industry’s structural shift toward lightweight, durable, and sustainability-aligned materials. Propylene-based derivatives, particularly polypropylene, are deeply embedded across food packaging, beverage containers, consumer goods wrapping, pharmaceutical packs, and personal care packaging due to their favorable balance of strength, flexibility, and chemical resistance. Packaging manufacturers increasingly prioritize materials that reduce overall product weight without compromising protection or shelf life, as lighter packaging directly lowers transportation costs, energy consumption, and carbon emissions across supply chains.

Compared with multi-layer or composite alternatives, propene-based packaging allows easier sorting, recycling, and reuse, making it attractive in markets facing heightened environmental scrutiny.

Additionally, brand owners across food, beverage, and consumer goods segments increasingly favor materials that support sustainability narratives without sacrificing cost efficiency or performance. As regulatory frameworks, retailer commitments, and consumer preferences converge around recyclable and resource-efficient packaging, product demand benefits indirectly but structurally, anchoring its long-term growth outlook within the global packaging ecosystem.

Expanding Demand from Automotive and Industrial Applications to Accelerate Market Growth

The aerospace industry continues to face increasing pressure to improve fuel efficiency, reduce operating costs, and meet stricter emission targets. Aircraft weight reduction remains one of the most effective levers to achieve these objectives, directly influencing fuel burn, payload capacity, and lifecycle emissions. Propylenes are central to this strategy, as they enable the manufacture of lightweight, high-strength structures with exceptional fatigue resistance and dimensional stability.

Modern commercial and military aircraft programs rely heavily on pre-impregnated carbon fiber for primary and secondary structural components, including fuselage sections, wings, control surfaces, and empennage structures. Unlike alternative composite formats, prepregs offer precise fiber–resin control, repeatable quality, and certification reliability, which are critical in safety-critical aerospace applications.

MARKET RESTRAINTS

Volatility in Feedstock Prices and Regulatory Hurdles to Hamper the Market Growth

Despite robust downstream demand, the market faces persistent constraints arising from feedstock price volatility and evolving regulatory pressures. Propene production economics remain closely tied to upstream hydrocarbon markets, where fluctuations in crude oil, naphtha, and natural gas liquids can rapidly alter production costs and profit margins. Such volatility creates uncertainty for producers, refiners, and downstream converters, complicating long-term supply planning and discouraging risk-intensive capital investments. When feedstock costs rise sharply or unpredictably, producers may reduce operating rates or delay capacity expansions, while converters face cost-pass-through challenges that can weaken downstream demand sensitivity.

MARKET OPPORTUNITIES

Shale Gas Bounty and Energy-Efficient Technologies to Unlock New Horizons for the Market

The evolving global energy landscape presents significant growth opportunities for the market, particularly through feedstock diversification and advancements in production technology. The increasing availability of shale-derived hydrocarbons, especially propane, has enabled a shift toward on-purpose propene production routes that are less dependent on traditional refining and steam-cracking operations. This transition enhances supply reliability and provides producers with greater flexibility in managing raw material sourcing, thereby reducing exposure to crude-oil-linked price fluctuations. Regions with access to abundant shale resources are emerging as competitive production hubs, strengthening their position in the global supply chain and encouraging capacity investments.

As producers integrate cleaner technologies and optimize feedstock utilization, propene is well positioned to expand into both traditional and emerging applications, creating new growth avenues while reinforcing its role as a critical building block for modern industrial and consumer markets.

MARKET CHALLENGES

Capital Intensity and Long Investment Cycles to Pose a Critical Challenge to Market Growth

Capital intensity represents one of the most critical structural challenges in the global market. The development of propene production facilities, whether through steam crackers, refinery integration, or on-purpose propane dehydrogenation (PDH) units, requires substantial upfront investment. These projects typically involve multi-billion-dollar capital expenditure commitments, long construction timelines, and complex regulatory approvals. As a result, investment decisions are made based on long-term demand forecasts rather than short-term market conditions.

Once commissioned, propene assets must operate at high utilization rates to recover capital costs and maintain economic viability. Fixed costs, including maintenance, energy consumption, and financing obligations, remain significant regardless of market conditions. This reduces operational flexibility during periods of weak demand or margin compression. Unlike smaller-scale chemical operations, propene production facilities cannot be easily scaled down or idled without affecting profitability and downstream integration.

Segmentation Analysis

By Derivative

Polypropylene Led the Market due to High Demand from Packaging, Construction, and Automotive Industries

Based on derivative, the market is segmented into polypropylene, propylene oxide, acrylonitrile, acrylic acid, cumene, and others.

The polypropylene segment accounted for the largest propylene market share in 2025, driven by strong demand from various end-use industries. Its lightweight nature, durability, and versatility make it ideal for applications in packaging, textiles, automotive parts, building and construction materials, and consumer goods. The rising demand from these industries is propelling the segment growth.

Propylene oxide is the fastest growing segment in the market. It is another major derivative used in the production of polyurethane foams, polyether, and various industrial chemicals. The growth in the construction and automotive sectors, which extensively use polyurethane foams, drives segment growth.

The acrylic acid segment is anticipated to grow at a CAGR of 6.24% over the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Packaging Segment Led the Market Due To Growing Demand for Flexible Packaging

Based on application, the market is segmented into packaging, automotive, construction, consumer goods, electrical & electronics, and others.

In terms of application, the packaging segment held the largest share of the global market. Its lightweight nature, strength, and cost-effectiveness make it ideal for producing flexible packaging solutions such as pouches, films, and bags. The rising demand for convenience foods and beverages, coupled with the growing emphasis on lightweight materials to improve transportation efficiency, is driving growth in the packaging segment.

Similarly, the automotive industry extensively employs derivatives in components such as bumpers and interior trim, benefiting from their lightweight properties and durability. The automotive segment is the fastest growing, expected to record a CAGR of 6.9% over the forecast timeframe.

Propylene Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Propylene Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 62.20% of the global market in 2025, generating USD 83.6 billion in revenue, and is projected to reach USD 88.3 billion in 2026. The region is projected to maintain its prominent position over the coming years. The growing middle class, rising disposable income, and increasing population in the region have all contributed to the product demand from the automotive, packaging, electronics, and construction industries. Additionally, significant investments in petrochemical infrastructure and capacity expansion have further bolstered the market’s growth trajectory in the region. China is the leading country in the Asia Pacific, owing to wide industrial activities and high demand for packaging in the country.

Japan Propylene Market

The Japanese market in 2026 is estimated at around USD 5.54 billion, accounting for roughly 4.1% of global revenues. Japan’s market is characterized by a highly integrated and mature petrochemical structure, with production largely derived from naphtha-based steam crackers and refinery operations. Competitive intensity is moderate, as capacity additions are limited and the market is primarily driven by replacement demand rather than large-scale expansion.

China Propylene Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 53.05 billion, representing roughly 38.5% of global sales. China represents the largest and fastest-growing market in the Asia Pacific, driven primarily by its dominant manufacturing sector.

To know how our report can help streamline your business, Speak to Analyst

India Propylene Market

The Indian market in 2026 is estimated at around USD 5.24 billion, accounting for roughly 3.8% of global revenues. The product demand in India is primarily anchored in PP manufacturing, which serves packaging, automotive components, consumer goods, and household applications. Rapid urbanization, rising disposable incomes, and expansion of organized retail continue to drive growth in packaged food, personal care products, and consumer durables. These structural trends provide a stable demand for propylene derivatives.

North America

North America contributed approximately USD 15.3 billion to the global market in 2025, accounting for 11.40% share, and is expected to reach USD 16 billion in 2026. The region is expected to be the third-leading in the market. North America is a cost-advantaged and structurally competitive region, underpinned by abundant shale-derived propane and a high concentration of PDH and refinery-integrated propene capacity.

U.S. Propylene Market

The U.S. market can be analytically approximated at around USD 1.35 billion in 2026, accounting for roughly 9.3% of global sales. The U.S. leads regional production and consumption, supported by strong downstream demand from packaging, automotive, and consumer goods sectors.

Europe

In 2025, the Europe market stood at USD 18 billion, representing 13.40% of global demand, and is projected to grow to USD 18.5 billion in 2026. The region represents a mature but strategically important market, characterized by high levels of downstream integration and regulatory oversight. Packaging, automotive lightweighting, construction materials, and specialty chemicals drive demand. European propylene prices typically trade at a premium due to higher energy costs, environmental compliance requirements, and constrained capacity additions.

U.K. Propylene Market

The U.K. market in 2026 is estimated at around USD 0.93 billion, representing roughly 0.7% of global revenues. The product demand in the U.K. is primarily anchored in packaging and consumer goods applications, driven by the food and beverage industry, personal care products, and household goods manufacturing. Polypropylene remains the dominant derivative, supported by strong retail and consumer consumption patterns.

Germany Propylene Market

Germany’s market is projected to reach approximately USD 3.40 billion in 2026, equivalent to around 2.5% of global sales. Propylene demand in Germany is primarily driven by PP production, which serves packaging, automotive components, industrial plastics, and consumer goods. The automotive sector remains a major consumption pillar, with propene-based materials used extensively in lightweight interior and exterior components to support fuel efficiency and electric vehicle development.

Latin America

Latin America recorded a market size of USD 6.8 billion in 2025, capturing 5.10% of the global market share, and is projected to reach USD 7.2 billion in 2026. Latin America is a consumption-led, structurally import-linked market, where demand growth is primarily driven by domestic consumption of propene derivatives rather than by large-scale upstream expansion. The region’s product supply is constrained by limited on-purpose capacity and uneven refinery integration, which increases exposure to global price cycles, freight dynamics, and currency movements. The Latin American market is set to reach a valuation of USD 6.19 billion in 2026.

Middle East & Africa

In 2025, Middle East & Africa generated USD 10.7 billion, contributing 7.90% to global market revenue, and is projected to grow to USD 11.2 billion in 2026. The market is shaped by Middle Eastern supply strength and African consumption expansion, with trade flows, infrastructure development, and downstream capability-building determining the pace and stability of regional growth.

Saudi Arabia Propylene Market

The Saudi Arabia market is projected to reach around USD 5.27 billion in 2026, representing roughly 3.8% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Capacity Expansions and Developing Bio-Based Alternatives are the Key Strategic Initiatives Adopted by Companies

The market is moderately consolidated, with a limited number of large-scale, vertically integrated petrochemical producers controlling a significant share of global capacity. High entry barriers, including capital-intensive steam cracking and on-purpose PDH production units, feedstock integration requirements, complex logistics infrastructure, environmental compliance norms, and strong downstream integration into polypropylene and other derivatives, restrict new entrants and reinforce the dominance of established players. Sinopec, ExxonMobil Corporation, LyondellBasell Industries, Reliance Industries Limited and SABIC are among the largest players in the market.

Other notable players in the global market include Shell plc, Braskem, PetroChina (CNPC), Formosa Plastics Corporation, Mitsubishi Chemical Group, LG Chem Ltd., and SK Geo Centric Co., Ltd.

LIST OF KEY PROPYLENE COMPANIES PROFILED

- SABIC (Saudi Arabia)

- China Petrochemical Corporation. (China)

- LyondellBasell Industries Holdings B.V. (U.S)

- Exxon Mobil Corporation (U.S.)

- Reliance Industries Limited. (India)

- Braskem (Brazil)

- PetroChina Company Limited (China)

- BASF SE (Germany)

- Mitsui Chemicals, Inc. (Japan)

- Shell plc (U.K.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: BASF announced progress on its new integrated Verbund site in Zhanjiang, China, including the development of large-scale steam cracking and downstream chemical units. The project is designed to strengthen BASF’s olefins production base, including propylene, and enhance integration with downstream chemical and materials manufacturing in the Asia Pacific region.

- March 2025: LyondellBasell announced an investment to expand propylene production capacity at its Channelview Complex in Texas. Construction is scheduled to begin in Q3 2025, with expected startup in late 2028. The new unit will have an annual propylene capacity of ~400 kt and convert ethylene into propylene for use in polypropylene and propylene oxide

- March 2024: Shell Chemicals started the supply of bio-circular and bio-attributed propylene feedstock to Braskem. The supply of such feedstock would enable Braskem to offer more sustainable solutions to cater to the increasing consumer demand from industries such as film, packaging, consumer goods, and automotive.

- January 2024: LyondellBasell announced a deal to acquire a 35% stake in Saudi Arabia’s National Petrochemical Industrial Company (NATPET) for over USD 500 million. The joint venture, facilitated by its Spheripol polypropylene technology, positioned LYB to grow and enhance its core PP business by providing access to advantageous feedstock and increasing product marketing capacity in a critical region.

- October 2022: Braskem formed a joint venture with Japanese supplier Sojitz to manufacture bioMPG (monopropylene glycol) for a range of applications and bioMEG (monoethylene glycol) for PET. This step indicates Braskem’s commitment to a low carbon circular economy.

REPORT COVERAGE

The global market analysis includes a comprehensive study of the market size and forecast across all market segments covered in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, and acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.90% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Million Ton) |

| Segmentation | By Derivative, Application, and Region |

| By Derivative |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 130.97 billion in 2025 and is projected to reach USD 217.74 billion by 2034.

In 2025, the market value in the Asia Pacific stood at USD 81.70 billion.

The market is expected to grow at a CAGR of 5.90% over the forecast period.

By derivative, the polypropylene segment led the market.

Growing need for lightweight and sustainable packaging solutions is the key factor driving the market.

Sinopec, ExxonMobil Corporation, LyondellBasell Industries, Reliance Industries Limited and SABIC are the major players in the global market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 253

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us