Protein Coffee Market Size, Share & Industry Analysis, By Product Type (RTD Protein Coffee, Protein Coffee Powder, and Protein Coffee Concentrates), By Source (Plant-based and Animal-based), By Coffee Type (Arabica and Robusta), By Packaging Type (PET Bottles, Cans, Sachets, and Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Stores, and Others), and Regional Forecast, 2026–2034

(Offer valid till 30th Jun 2026)

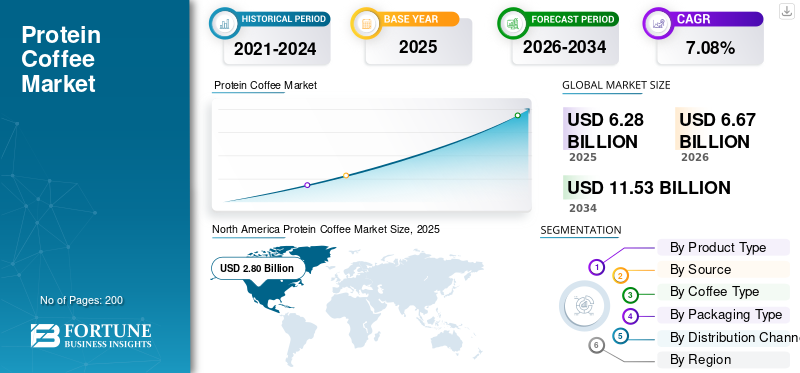

Protein Coffee Market Size and Future Outlook

The global protein coffee market size was valued at USD 6.28 billion in 2025. The market is projected to grow from USD 6.67 billion in 2026 to USD 11.53 billion by 2034, exhibiting a CAGR of 7.08% during the forecast period. North America dominated the protein coffee market with a market share of 44.59% in 2025.

Protein coffee is a functional beverage that combines coffee with added protein from sources such as whey, milk protein, soy, or pea protein. It is available in formats such as -to-drink ready bottles and cans, powdered blends, and fortified cold coffee beverages. These products are mainly used for energy, convenience, satiety, and nutritional support, making them relevant for health-conscious consumers and fitness enthusiasts. The global market is benefiting from rising coffee consumption, growing interest in protein-rich diets, a growing specialty coffee culture, wider use of functional beverages, and expansion through modern distribution channels such as supermarkets, convenience stores, and online retailers. The category also benefits from the familiar taste of coffee, which helps consumers adopt fortified products more easily than traditional supplements.

Companies such as Starbucks Corporation, Nestlé S.A., Laird Superfood, Premier Nutrition Company, LLC, and Slalte Milk are the major key players in the market. New product launches, functional reformulations, and broader retail expansion are among the key strategies supporting market growth.

Download Free sample to learn more about this report.

Protein Coffee Market Trends

Emerging On-the-Go and Ready-to-Drink Protein Beverages to Lead Newer Market Trends

One of the most important trends in the global market is the rise of on-the-go and ready-to-drink high-protein coffee products. Consumers increasingly prefer beverages that are easy to carry, quick to consume, and suitable for busy daily routines. This trend is especially strong among working professionals, students, commuters, and fitness enthusiasts who want both energy and convenience. Protein coffee is shifting from niche powder-based formats toward bottled and canned beverages that fit into breakfast, office, travel, and snack occasions. This trend also aligns with the broader evolution of coffee consumption, in which cold brew, iced coffee, and other premium ready formats are becoming more common. Consumers are showing greater willingness to buy beverages that combine function with convenience. That is why manufacturers are launching more chilled and ambient RTD products with protein, fiber, vitamins, and lower sugar content. These innovations are helping brands expand beyond sports nutrition and reach mainstream coffee drinkers. Wider availability through supermarkets, convenience stores, and online retailers is also helping the category gain visibility. Therefore, on-the-go usage and RTD innovation are reshaping the industrial landscape of the protein coffee market and enhancing its long-term commercial potential.

- According to the National Coffee Association, 36% of past-day coffee drinkers had coffee out of home in 2024. It shows consumer demand for ready-to-drink coffee and café trends in the global market, especially in developed economies.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Increasing Coffee Consumption and Specialty Coffee to Drive the Market Growth

Increasing coffee consumption is one of the key factors supporting the global protein coffee market growth. Protein coffee depends first on the strength of the underlying coffee category, and that base remains very large and resilient. The market is also benefiting from stronger participation in specialty coffee, especially in premium urban and younger consumer segments, where product experimentation is higher. As the taste of coffee remains familiar and widely accepted, brands can add protein and other nutrients without asking consumers to shift to an entirely new beverage category. The category is also benefiting from growing demand for specialty coffee, especially in North America, where premium and innovative coffee formats are now mainstream.

The National Coffee Association reported that 66% of Americans had coffee in the past day in Spring 2025, while 46% of American adults had specialty coffee in the past day. This matters for demand for high-protein coffee because specialty coffee drinkers are generally more open to new formats such as cold brew, flavored lattes, and fortified coffees. As a result, protein coffee fits well into premium coffee routines where consumers want both functionality and the familiar taste of coffee.

At the same time, protein intake is becoming a stronger driver of purchase decisions across mainstream food and beverage categories. IFIC reported in 2025 that 70% of Americans are trying to consume protein, and that a high-protein diet was the most common diet followed in the past year. This directly benefits the high-protein coffee product by allowing consumers to combine caffeine, convenience, and nutrition in a single beverage.

- The International Coffee Organization reported that global coffee consumption reached a record 176.6 million 60-kg bags in 2021 and 2022 and is projected at 177.0 million bags in 2023 and 2024. This creates a large addressable base for protein coffee products, especially in markets where consumers already consume coffee daily and are open to functional upgrades.

Market Restraints

Rising Raw Material Price and Consumer Pricing to Hamper the Market Growth

Rising raw material prices are a major restraint on the global market. Protein coffee has a more complex cost structure than standard coffee because it relies on coffee, protein ingredients, sweeteners, stabilizers, and packaging. This makes the category more exposed to inflation across multiple components simultaneously. When coffee prices rise sharply, the cost pressure is directly transferred to premium protein coffee formulations. The problem becomes more serious when protein inputs remain expensive, as brands must protect both nutritional claims and coffee's taste. In addition, RTD formats require bottles or cans, filling, transport, and retailer margins, which further increase cost pressure. This is especially challenging for ready-to-drink high-protein coffee, where packaging and logistics account for a significant share of the total product cost.

As a result, brands may face tighter margins and reduced flexibility on consumer pricing. Higher raw material costs can also slow innovation, especially for smaller companies trying to compete with larger key players. In a competitive distribution channel environment, passing on all cost increases to consumers may not always be possible. Therefore, rising prices of coffee and protein-related raw materials remain a major challenge for the market.

- According to the International Coffee Organization, the average indicator coffee price increased from 229.34 US cents/lb in 2024 to 354.32 US cents/lb in February 2025.

Market Opportunities

Rising Popularity of Fortified Drinks to Create Strong Market Opportunities

The rising popularity of fortified drinks is creating a significant market opportunity. Consumers increasingly want beverages that deliver more than refreshment and caffeine. They are looking for products that provide protein, fiber, vitamins, minerals, and other nutritional benefits in a convenient format. This shift is helping protein coffee products move beyond a narrow protein supplement niche and become part of mainstream functional beverage consumption. The opportunity is particularly strong among health-conscious consumers who want beverages that fit active lifestyles and support better nutrition. Protein coffee also benefits from its potential as a light meal replacement or a satiety-supporting beverage during busy working hours. Since the category retains the familiar taste of coffee, it is easier for consumers to adopt than many traditional nutrition drinks.

Manufacturers are also strengthening the category by using different protein source systems and combining protein with fiber and micronutrients. This helps create premium multi-benefit beverages with stronger product differentiation. As fortified drinks gain greater shelf presence across retail and digital channels, demand for high-protein coffee is expected to grow further. Therefore, the rising popularity of fortified beverages remains an important opportunity for innovation, premiumization, and long-term growth in consumer demand worldwide.

- According to Starbucks, one of the key coffee chains, citing the 2025 IFIC Food & Health Survey, 8 in 10 Americans prioritize adding protein to their diet daily.

SEGMENTATION ANALYSIS

By Product Type

RTD Protein Coffee Led the Market Due to Better Convenience and Wider Consumer Acceptance

The market is segmented by product type into RTD protein coffee, protein coffee powder, and protein coffee concentrates.

The RTD protein coffee segment dominated the market in 2025, valued at USD 3.73 billion. This segment holds the largest market share as it offers better convenience, immediate consumption, and stronger compatibility with modern on-the-go lifestyles. RTD protein coffee products are easy to carry, require no mixing or preparation, and fit well into breakfast, office, travel, and post-workout occasions. The segment also benefits from rising demand for functional beverages that combine energy and nutrition in a single pack. In addition, RTD products are gaining strong visibility across supermarkets, convenience stores, gyms, and online platforms. Premium cold coffee culture, higher acceptance of bottled and canned beverages, and growing product launches by major brands are also supporting segment growth. Therefore, RTD protein coffee remains the leading product type in the global market.

The protein coffee concentrates segment is projected to grow at the fastest CAGR of 6.98% during 2026–2034.

To know how our report can help streamline your business, Speak to Analyst

By Source

Stronger Protein Performance and Mainstream Acceptance to Drive the Animal-based Segment Growth

Based on source, the market is bifurcated into plant-based and animal-based.

The animal-based segment led the global protein coffee market share in 2025, reaching USD 4.64 billion. Whey and milk-based proteins are still more widely used in mainstream protein beverages. Animal-based protein offers stronger protein density, better amino acid profile, and greater familiarity among health-conscious consumers and fitness enthusiasts. It also performs better in many beverage formulations in terms of texture, creaminess, and nutritional positioning. As a result, many protein coffee products continue to rely on whey or milk protein as the main protein source. This keeps the animal-based segment ahead in value terms, especially in premium ready-to-drink and performance-led products.

The plant-based segment is expected to grow at the fastest CAGR of 8.59% during the forecast period. The growth is being supported by rising vegan and flexitarian diets, increasing lactose intolerance concerns, and stronger demand for dairy-free functional beverages. Plant-based protein coffee is gaining traction through pea, soy, oat, and blended protein systems, which are helping brands expand into broader lifestyle and wellness segments.

By Coffee Type

Arabica Segment Led the Market Due to Its Premium Quality and Smoother Flavor

On the basis of coffee type, the market is divided into Arabica and Robusta.

The Arabica segment held the largest share of the market in 2025, valued at USD 4.95 billion. It holds the largest market share because Arabica is more closely associated with premium quality, a smoother flavor, and a specialty coffee culture. Since protein coffee products are often positioned as premium functional beverages, brands prefer Arabica to maintain better taste, aroma, and value perception. Arabica also fits well with specialty coffee trends, café-style flavors, and premium RTD innovation. Therefore, Arabica remains the dominant coffee type in the global market.

The Robusta segment is projected to grow at the fastest CAGR of 8.38% during the forecast period. Its growth is being supported by stronger caffeine positioning, cost efficiency, and wider use in blends for value-driven and mass-market products.

By Packaging Type

PET Bottles Led the Market Owing to Being Widely Used in Mainstream RTD Beverage Distribution

On the basis of packaging type, the market is segmented into PET bottles, cans, sachets, and others.

The PET Bottle segment held the largest share of the market in 2025, valued at USD 3.06 billion. PET bottles are widely used in ready-to-drink protein coffee formats and are highly compatible with mainstream beverage distribution. They are easy to handle, lightweight, cost-effective, and suitable for single-serve functional beverages. Since RTD protein coffee is the largest product segment, PET bottles continue to benefit from broader commercial scale. Therefore, PET bottles remain the leading packaging format in the market.

The cans segment is projected to grow at the fastest CAGR of 8.97% during the forecast period. Growth is being supported by the premiumization of ready-to-drink high protein coffee and the increasing use of cans in modern cold coffee beverages.

By Distribution Channel

Supermarkets/Hypermarkets Led Market Due to Strong Shelf Visibility and Large Consumer Reach

On the basis of distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online stores, and others.

The supermarkets/hypermarkets segment held the largest share of the market in 2025, valued at USD 2.31 billion. Supermarkets and hypermarkets are important for both trial and repeat purchases, especially for RTD protein coffee products that rely on mass-retail visibility. This channel also supports multi-brand comparison, promotional activity, and wider placement of premium functional beverages. As protein coffee moves into mainstream beverage consumption, large-format retail continues to play the most important role in generating market value. Therefore, supermarkets and hypermarkets remain the leading distribution channels worldwide.

The online retail segment is projected to grow at the fastest CAGR of 8.55% during the forecast period.

Protein Coffee Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Protein Coffee Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market accounted for USD 2.80 billion in 2025 and is projected to grow at a CAGR of 5.29% during 2026–2034. North America remains a major market for protein coffee, supported by its very strong coffee-drinking culture, high specialty coffee participation, and broad acceptance of protein-led beverages. The region benefits from a large base of daily coffee drinkers, strong premium coffee habits, and well-developed retail execution across grocery, convenience, club, and foodservice channels. Product expansion is being driven by RTD innovation, especially in cold coffee formats that suit breakfast, commute, and post-workout use. In addition, North America’s mature cold chain, large-scale beverage distribution, and broad digital reach support the faster rollout of both ready-to-drink and powdered formats. According to the International Coffee Organization, North America accounted for 17.5% of global coffee consumption in 2023, while the National Coffee Association reported that 66% of American adults drank coffee daily in 2025.

U.S. Protein Coffee Market

The U.S. market was valued at approximately USD 2.34 billion in 2025 and is expected to expand at a CAGR of 5.12% during the forecast period. The country has the largest coffee-consumption base in the world and also shows unusually high openness to specialty coffee, protein-enriched products, and premium convenience beverages. The market is further supported by a large population of protein-aware consumers, strong morning beverage routines, and rapid commercialization of RTD and customized café protein drinks. Product development in the U.S. is also broader than in most markets, ranging from bottled protein coffee to protein lattes, cold foam beverages, and hybrid coffee-plus-fiber products. According to the National Coffee Association, approximately 46% of American adults had specialty coffee in the past day in 2025. It supports the market growth.

Europe

The European market is valued at USD 1.79 billion in 2025 and is expected to expand at a CAGR of 6.68% during the forecast period. The growth is being shaped more by premium coffee culture, taste expectations, and gradual functional adoption than by mass RTD penetration alone. The region benefits from a large, well-established coffee base, high per-capita consumption across many markets, and a strong café and at-home premium coffee culture. Europe’s protein coffee opportunity is more closely linked to premium positioning, wellness-led innovation, and plant-based or dairy-alternative development. Consumer acceptance is supported by mature retail systems and growing interest in better-for-you beverages, but adoption remains more fragmented across countries.

Germany Protein Coffee Market

The German market accounted for approximately USD 0.44 billion in 2025. Germany is one of the strongest countries in terms of opportunities in Europe because it combines large coffee consumption, a broad retail scale, and a central role in Europe’s coffee supply chain. The market benefits from high levels of everyday coffee consumption, strong grocery and discount store reach, and a large installed base of packaged-coffee users.

Asia Pacific

Asia Pacific’s market reached USD 1.16 billion in 2025 and is the leading and fastest-growing region, with a 10.39% CAGR during the forecast period. Asia Pacific is the fastest-growing long-term opportunity for protein coffee because it combines the world’s largest regional coffee-consumption base with a rapidly expanding functional-beverage culture. The region benefits from rising urban coffee consumption, growing café penetration, stronger acceptance of premium cold beverages, and increasing interest in protein as a mainstream health claim. The emerging functional, fortified, and health-oriented coffee products are expected to drive the market growth in the region.

China Protein Coffee Market

China was valued at USD 0.29 billion in 2025. China is one of the most promising protein coffee industries in the Asia Pacific as it combines rapid coffee commercialization with strong consumer openness to modern beverage innovation. The country’s protein coffee opportunity is being driven by urban café culture, high digital engagement, delivery-led beverage habits, and strong acceptance of cold and customized drinks. Protein coffee can therefore benefit from both rising coffee adoption and broader demand for functional beverages. In addition, premium coffee operators continue to view China as a strategic expansion market, which supports brand building and category education. These conditions make China especially attractive for premium RTD protein coffee, café-style fortified drinks, and digitally driven product launches.

India Protein Coffee Market

India’s market reached USD 0.12 billion in 2025. India is an emerging market as it sits at the intersection of rising café culture, fast urbanization, and increasing protein awareness among younger consumers. The market is still smaller than China or Japan in coffee development, but it is moving quickly as branded café chains expand into more cities and premium coffee becomes more aspirational. That expanding premium coffee infrastructure should support the gradual uptake of protein coffee in metropolitan and upper-tier urban markets.

South America and the Middle East & Africa

South America accounted for USD 0.33 billion in 2025, growing at a CAGR of 8.38% during the forecast period. South America remains a relevant market for protein coffee because it combines deep familiarity with coffee with a growing premium coffee and wellness beverage opportunity. The region benefits from strong consumer familiarity with coffee, which reduces the barrier to education for coffee-based functional products. Rising café culture, premium packaged coffee, and gradual consumer migration toward convenient high-protein beverages are further contributing to the market growth.

The Middle East & Africa market was valued at USD 0.20 billion in 2025 and is expected to expand at a CAGR of 9.13% during the forecast period. The Middle East & Africa are still smaller markets, but they offer selective growth opportunities through premium coffee culture, imported functional beverages, and rising modern retail presence. Protein coffee is likely to gain traction first in markets where premium coffee habits, convenience-led consumption, and wellness spending already overlap, especially in the Gulf and select African cities. The opportunity is also supported by a growing branded café footprint and by the appeal of convenient, premium, better-for-you beverages among affluent urban consumers.

South Africa Protein Coffee Market

The South African market was valued at approximately USD 0.05 billion in 2025 and is projected to grow at a CAGR of 8.42% during the forecast period. Protein coffee is still niche, but South Africa has a better foundation than most African markets for introducing coffee-plus-function concepts through cafés, forecourts, corporate sites, and premium retail. It also benefits from an established coffee shop ecosystem that can support both trial and repeat purchases. Furthermore, a more developed branded café culture and a stronger packaged beverage infrastructure are needed to change the industry outlook.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Innovation, Portfolio Expansion, and Strategic Partnerships Lead to Stronger Market Positioning

The global protein coffee market is fragmented, characterized by a few dominant multinational corporations and numerous regional and local protein coffee producers. Leading companies such as Starbucks Corporation, Nestlé S.A., Laird Superfood, Premier Nutrition Company, LLC, and Slalte Milk hold a significant share of the global market. These players are focused on product expansion, geographic expansion, and innovation. It helps key players strengthen their global market share.

Key Players in the Protein Coffee Market

|

Rank |

Company Name |

|

1 |

Starbucks Corporation |

|

2 |

Nestlé S.A. |

|

3 |

Laird Superfood |

|

4 |

Premier Nutrition Company, LLC |

|

5 |

Slalte Milk |

List of Key Protein Coffee Companies Profiled

- Starbucks Corporation (U.S.)

- Laird Superfood (U.S.)

- Super Coffee (U.S.)

- Premier Nutrition Company, LLC (U.S.)

- Slate Milk (U.S.)

- OWYN (U.S.)

- The Protein Works (U.K.)

- Nestlé SA (Switzerland)

- Javy Coffee (U.S.)

- The Protein Factory (South Africa)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Starbucks Corporation, an American company, launched a new line-up of ready-to-drink (RTD) Starbucks Coffee & Protein beverages that blend premium Starbucks coffee with 22 grams of complete protein, 5 grams of prebiotic fiber, five vitamins and minerals, and just 2 grams of sugar.

- January 2026: Laird Superfood, Inc., a functional coffee, creamers, and superfood product manufacturer, launched Laird Superfood Protein Coffee with Lion's Mane Mushroom, made with whey protein from dairy.

- June 2025: Califia Farms, an American plant-based beverage brand, launched a new ready-to-drink coffee product, protein vanilla almond latte. The new product contains 10 grams of pea protein and 5 grams of sugar per serving.

- July 2024: Starbucks Corporation launched low-fat ready-to-drink coffee containing 20 grams of protein. The company partnered with Arla Foods, one of the global dairy companies, to develop and launch the new product in the U.K.

- March 2024: Jimmy’s Iced Coffee, a coffee brand, launched its new protein coffee in two flavors: Original and Caramel. The new product is developed in collaboration with Myprotein to meet the rising consumer demand for on-the-go protein beverages.

REPORT COVERAGE

The protein coffee market report provides in-depth analysis. It highlights key aspects, including global market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. In addition, the research report provides insights into the global market and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.08% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Source

|

|

|

By Coffee Type

|

|

|

By Packaging Type

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 6.28 billion in 2025 and is anticipated to reach USD 11.53 billion by 2034.

At a CAGR of 7.08%, the global market will grow steadily over the forecast period.

By product type, the RTD protein coffee segment led the market.

North America held the largest market share in 2025.

Increasing coffee consumption is expected to drive the market growth.

Starbucks Corporation, Nestlé S.A., Laird Superfood, Premier Nutrition Company, LLC, and Slalte Milk are the leading companies in the market.

Emerging on-the-go and ready-to-drink beverages to change the industrial outlook.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us