Racing Simulator Market Size, Share & Industry Analysis, By Component (Hardware and Software), By Simulator Type (Static Racing Simulators, Motion Racing Simulators, and Full-motion Professional Simulators), By Level of Immersion (Entry-Level Simulators, Mid-Range Simulators, and High-End Simulators), By End User (Individual Gamers/Enthusiasts, Professional Racing Teams, Automotive OEMs, Esports Organizations, and Others), and Regional Forecast, 2026-2034

Racing Simulator Market Size and Future Outlook

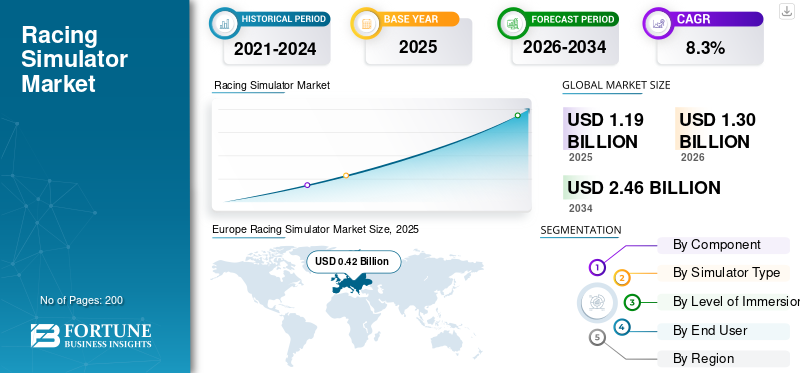

The global racing simulator market size was valued at USD 1.19 billion in 2025. The market is projected to grow from USD 1.30 billion in 2026 to USD 2.46 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period. Europe dominated the racing simulator market with a market share of 35.29% in 2025.

The global market refers to the industry focused on the development, production, and sale of hardware and software systems that replicate real-world motorsport driving experiences through simulation. It includes racing simulation rigs, steering wheels, pedals, motion platforms, VR integration, and specialized simulation software used for gaming, professional driver training, and esports. The market serves individual consumers, esports arenas, racing teams, and training centers seeking immersive and realistic racing experiences.

Key drivers of the market include the rising popularity of esports and sim racing competitions, increasing demand for immersive gaming experiences, advancements in virtual reality and motion simulation technologies, and growing use of simulators for professional racer driver training by motorsport teams and automotive manufacturers seeking cost-effective and safe performance testing environments.

Major players in the market include Playseat, Next Level Racing, SimXperience, Simucube, Fanatec (Endor AG), and Thrustmaster, competing through high-precision force feedback technology, advanced motion simulation systems, modular cockpit designs, VR compatibility, and realistic driving software integration to deliver highly immersive racing experiences for gamers, esports professionals, and driver training applications.

Download Free sample to learn more about this report.

RACING SIMULATOR MARKET TRENDS

Integration of Virtual Reality and Motion Simulation Technologies to Enhance User Immersion

A key trend shaping the market is the increasing integration of Virtual Reality (VR), motion platforms, and immersive display technologies. Modern simulators are moving beyond static cockpit setups to deliver highly realistic driving experiences through multi-axis motion systems that replicate vehicle acceleration, braking, and cornering forces. VR headsets and ultra-wide display systems further enhance immersion by providing realistic track environments and depth perception. Additionally, manufacturers are incorporating advanced haptic feedback, tactile vibration systems, and high-precision force-feedback steering to mimic real driving sensations. These innovations are making racing simulators more engaging for both professional drivers and gaming enthusiasts. As hardware capabilities improve and costs gradually decline, immersive technologies are expected to become a standard feature in next-generation racing simulation systems.

MARKET DYNAMICS

MARKET DRIVERS

Rising Popularity of Esports and Sim Racing Competitions to Accelerate Market Growth

The rapid expansion of esports and organized sim racing competitions is a major driver for the global racing simulator market growth. Professional leagues, online tournaments, and sim racing championships are attracting a large audience of gaming enthusiasts and motorsport fans. Many motorsport organizations, including Formula 1 and endurance racing leagues, have introduced official virtual competitions, encouraging gamers to participate using advanced simulators. These competitions require high-performance hardware such as force-feedback steering systems, motion platforms, and realistic cockpit setups. In addition, esports arenas and gaming lounges are increasingly investing in professional-grade simulators to host competitive events. The growing acceptance of sim racing as a legitimate competitive platform, combined with sponsorships and streaming opportunities, is significantly boosting increased demand for advanced racing simulation equipment worldwide.

- For instance, in December 2025, motorsport authorities began recognizing sim racing participation as part of official driver licensing pathways, further validating simulators as professional racing tools and expanding their commercial demand globally.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

High Cost of Advanced Simulation Hardware to Limit Mass Consumer Adoption

One of the key restraints in the global market is the high cost associated with advanced simulation hardware and professional-grade setups. High-end racing simulators often include motion platforms, precision steering wheels with force feedback, hydraulic pedal systems, and integrated cockpit frames, which can significantly increase the overall cost. Professional simulator rigs used by Esports arenas and racing teams can cost several thousand dollars, making them inaccessible for many casual gamers. Additionally, the need for high-performance computers, large displays, or virtual reality headsets further increases the total investment required. This cost barrier restricts widespread adoption among price-sensitive consumers, particularly in emerging markets. As a result, many potential users opt for basic gaming controllers rather than investing in full simulator setups, slowing broader consumer-level market penetration.

MARKET OPPORTUNITIES

Increasing Use of Simulators for Professional Driver Training to Create New Opportunities

The growing use of racing simulators for professional driver training and vehicle testing presents a significant opportunity for the market. Automotive manufacturers, motorsport teams, and driver training academies are increasingly adopting simulation technologies to replicate real-world driving conditions in a controlled environment. High fidelity simulators allow drivers to practice track layouts, vehicle handling, and race strategies without the risks and costs associated with physical track testing. In addition, simulators enable engineers to analyze driver performance and vehicle behavior using advanced telemetry and data analytics. This technology is also gaining popularity in performance driving schools and motorsport development programs. As simulation accuracy continues to improve with better physics engines, motion systems, and immersive visuals, the demand for professional-grade simulators in training and research applications is expected to grow significantly.

MARKET CHALLENGES

Maintaining Realistic Physics and Hardware Compatibility Across Platforms to Pose Development Challenges

Ensuring accurate physics simulation and seamless hardware compatibility across various platforms remains a major challenge in the market. High quality racing simulators rely on complex physics engines that replicate vehicle dynamics, tire behavior, track surfaces, and weather conditions. Developing software that delivers consistent realism while remaining compatible with a wide range of hardware components such as steering wheels, pedals, motion rigs, and VR devices requires significant engineering effort. Additionally, different gaming platforms and simulation software ecosystems may use varying technical standards, making integration more complex. Manufacturers must continuously update firmware, drivers, and software to maintain compatibility with new hardware and operating systems. Balancing realism, system performance, and cross-platform functionality is therefore a persistent challenge for both hardware and simulation software developers.

Segmentation Analysis

By Component

Advanced Simulation Hardware and Immersive Cockpit Systems to Drive Hardware Segment Dominance

Based on component, the market is segmented into hardware and software.

The hardware segment dominates the market due to strong demand for physical simulation components such as steering wheels, pedal sets, motion platforms, and cockpit rigs. These systems are essential for delivering realistic driving experiences and are widely adopted by esports arenas, professional drivers, and gaming enthusiasts. Continuous upgrades in force-feedback technology, haptic systems, and modular cockpit designs further support steady demand, reinforcing hardware’s dominant share in simulator installations.

The software segment is projected to grow at a CAGR of 9.9% during the forecast period. Rising demand for advanced simulation engines, realistic physics modeling, and cloud-based racing platforms is accelerating software adoption. Continuous updates, track expansions, and integration with esports ecosystems further support segment growth.

By Simulator Type

Affordability and Wide Adoption in Gaming Setups to Drive Static Racing Simulators Segment Dominance

In terms of simulator type, the market is categorized into static racing simulators, motion racing simulators, and full-motion professional simulators.

The static racing simulators segment dominates the market due to their affordability, compact design, and wide adoption among gaming enthusiasts and esports centers. These simulators include fixed cockpit rigs with steering wheels and pedal systems, offering realistic driving experiences without expensive motion platforms. Their lower setup cost and compatibility with standard gaming hardware make them popular for home users, gaming lounges, and entry-level esports facilities, sustaining high installation volumes globally.

The motion racing simulators segment holds the second largest racing simulator market share. Also, it records the fastest growing CAGR of 9.2% during the study period as gaming arenas and professional users increasingly seek enhanced immersion through dynamic seat movement and force simulation. These systems provide more realistic driving sensations than static rigs while remaining relatively cost-effective for commercial entertainment centers.

To know how our report can help streamline your business, Speak to Analyst

By Level of Immersion

Affordability and Accessibility Among Casual Gamers to Drive Entry-Level Simulator Segment Dominance

Based on level of immersion, the market is segmented into entry-level simulators, mid-range simulators, and high-end simulators.

The entry-level simulators segment dominates the market due to their affordability, easy installation, and strong adoption among casual gamers and beginner sim racing enthusiasts. These setups typically include basic racing wheels, pedal sets, and compact cockpit frames compatible with personal computers and gaming consoles. Their relatively low cost makes them widely accessible for home users and gaming cafés. Additionally, increasing interest in sim racing and esports is encouraging first-time users to invest in entry-level setups before upgrading to more advanced systems, sustaining consistent demand across consumer gaming markets.

The high-end simulators segment is projected to grow at a CAGR of 9.6% during the forecast period. Increasing adoption by professional racing teams, esports arenas, and advanced driver training facilities is driving demand for highly immersive systems featuring motion platforms, advanced telemetry integration, and ultra-realistic simulation environments.

By End User

Growing Popularity of Home Sim Racing and Gaming Culture to Drive Individual Gamers/Enthusiasts Segment Dominance

Based on end user, the market is segmented into individual gamers/enthusiasts, professional racing teams, automotive OEMs, esports organizations, and others.

The individual gamers/enthusiasts segment dominates the market due to the rising popularity of home-based sim racing and competitive gaming. Affordable simulator hardware, increasing availability of online racing platforms, and the growth of streaming and esports content have encouraged gamers to invest in personal simulator setups. Entry-level and mid-range simulators are widely adopted by hobbyists seeking immersive racing experiences from home. Additionally, the expansion of online racing leagues and multiplayer simulation platforms is further increasing engagement among gaming communities. As a result, consistent consumer demand for racing wheels, cockpit rigs, and simulation software continues to sustain the dominance of the individual gamers segment in the global market.

The professional racing teams segment is projected to grow at a CAGR of 10.8% during the forecast period. Motorsport teams are increasingly adopting high-fidelity simulators for driver training, track familiarization, and vehicle performance analysis. These systems enable teams to simulate race conditions, optimize strategies, and evaluate driver behavior without the cost and risk of physical track testing. The automotive OEMs segment also represents a significant share as manufacturers use advanced simulators for vehicle development and driver-in-the-loop testing. Additionally, esports organizations are investing in professional simulator rigs to host competitive sim racing events and training programs, further supporting market expansion across commercial and professional environments.

Racing Simulator Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Europe

Europe Racing Simulator Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe dominates the market due to its strong motorsport heritage, presence of leading simulator manufacturers, and widespread adoption of esports racing competitions. Countries such as the U.K., Germany, and Italy host major motorsport teams, racing academies, and technology developers that actively use advanced simulators for driver training and vehicle testing. In addition, the growing popularity of sim racing leagues and gaming cafés across Europe continues to drive demand for hardware and software. Continuous technological innovation and strong motorsport ecosystems further reinforce Europe’s leadership in the global market.

U.K. Racing Simulator Market

The U.K. market in 2026 is estimated at around USD 0.13 billion, accounting for a notable share of global revenues. Strong motorsport culture, expanding esports racing leagues, and rising adoption of advanced simulation systems in gaming centers and professional driver training, support market growth.

Germany Racing Simulator Market

The Germany market in 2026 is estimated at around USD 0.11 billion, accounting for a steady share of global revenues. Growth is supported by strong automotive engineering expertise, motorsport participation, and increasing use of simulators in automotive R&D and esports arenas.

North America

North America holds the second-largest share of the market and is projected to grow at a CAGR of 7.8% during the forecast period. The region benefits from a strong gaming industry, increasing investments in esports infrastructure, and the rising popularity of sim racing competitions. The U.S. and Canada are witnessing growing adoption of advanced simulators by gaming lounges, esports organizations, and professional training centers. Additionally, the presence of major gaming hardware manufacturers and technology developers supports product innovation. Increasing consumer spending on immersive gaming setups and streaming content is further driving simulator demand across the region.

U.S. Racing Simulator Market

The U.S. market in 2026 is estimated at around USD 0.32 billion, accounting for a significant share of global revenues. Expanding esports infrastructure, rising demand for immersive gaming setups, and growing adoption by motorsport teams drive strong market expansion.

Asia Pacific

Asia Pacific represents the third-largest market, driven by the rapid expansion of gaming communities and esports participation in countries such as China, Japan, South Korea, and India. The growing popularity of competitive gaming and racing simulation platforms is encouraging both individuals and gaming cafés to adopt advanced simulator setups. In addition, increasing internet penetration and rising disposable incomes are enabling consumers to invest in immersive gaming technologies. Several esports arenas and entertainment centers in the region are also installing such simulators to attract gaming enthusiasts, contributing to steady market growth across Asia Pacific.

China Racing Simulator Market

The China market in 2026 is estimated at around USD 0.14 billion, accounting for a growing share of the global revenues. Rapid expansion of gaming cafés, esports tournaments, and increasing consumer spending on immersive gaming technologies is supporting simulator adoption.

Japan Racing Simulator Market

The Japan market in 2026 is estimated at around USD 0.08 billion, accounting for a moderate share of global revenues. Strong gaming culture, technology innovation, and the presence of major racing simulation developers continue to support steady market growth.

Rest of the World

The rest of the world region, including Latin America, and the Middle East & Africa, is gradually emerging in the market due to increasing interest in e-sports and immersive gaming entertainment. The expansion of gaming lounges, entertainment centers, and esports arenas in countries such as Brazil, the UAE, and South Africa is supporting simulator adoption. Rising internet accessibility and the growing influence of global gaming trends are encouraging younger consumers to explore competitive racing simulations. Additionally, tourism-focused entertainment venues are incorporating simulator experiences to attract visitors, contributing to steady demand for such simulator systems in developing markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Partnerships Intensifying Competition in Market

The global market is characterized by the presence of established gaming hardware manufacturers and specialized simulation technology providers competing through product innovation, realism, and ecosystem integration. Companies such as Fanatec (Endor AG), Thrustmaster, Simucube, Next Level Racing, and SimXperience focus on developing advanced force-feedback steering systems, high-precision pedal sets, and modular cockpit platforms to enhance simulation realism. Competitive strategies largely revolve around improving hardware performance, expanding compatibility with major simulation software platforms, and offering customizable simulator setups that cater to casual gamers, esports participants, and professional racing teams.

Market participants are also investing in technological advancements such as motion simulation platforms, virtual reality integration, and telemetry-based performance analytics to differentiate their offerings. Partnerships with esports organizations, gaming studios, and motorsport teams are becoming increasingly common as companies aim to strengthen brand visibility and product adoption. In addition, manufacturers are expanding their global distribution networks and launching product upgrades to attract a broader consumer base. The growing popularity of competitive sim racing and online racing leagues is further intensifying competition, encouraging companies to deliver highly immersive and scalable simulation solutions.

LIST OF KEY RACING SIMULATOR COMPANIES PROFILED

- Fanatec (Endor AG) (Germany)

- Thrustmaster (Guillemot Corporation) (France)

- Logitech G (Switzerland)

- Simucube (Granite Devices) (Finland)

- Next Level Racing (New Zealand)

- Playseat (Netherlands)

- SimXperience (U.S.)

- Asetek SimSports (Denmark)

- MOZA Racing (China)

- Simagic (China)

- Heusinkveld Engineering (Netherlands)

- Trak Racer (Australia)

- Sim-Lab (Netherlands)

- Cube Controls (Italy)

- Ascher Racing (Germany)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Thrustmaster released updated configuration guides and performance setups for iRacing systems, helping professional sim racers optimize hardware compatibility and driving realism across advanced simulator platforms.

- January 2026: Thrustmaster published new optimization guides for racing wheel setups in major simulation titles, highlighting growing adoption of high-precision force-feedback hardware among esports racers and simulator enthusiasts.

- December 2025: Gran Turismo 7 introduced support for Fanatec’s FullForce feedback system, enabling compatible wheelbases to deliver more detailed force feedback simulating tire grip, suspension behavior, and road textures for sim racers.

- October 2025: Thrustmaster showcased new sim racing hardware including the T598 servo base, T-GT wheel upgrades, and Raceline Pedals LTE at SimRacing Expo Dortmund, targeting both esports competitors and simulation enthusiasts.

- October 2025: Fanatec unveiled its next-generation Podium Series sim racing hardware at SimRacing Expo 2025, introducing upgraded direct-drive wheelbases and advanced pedal systems designed to enhance realism for professional and enthusiast racing simulators.

- September 2025: Logitech G announced the RS50 modular racing simulator system featuring a direct-drive wheel base, customizable pedals, and cross-platform compatibility, expanding options for mid-range sim racing setups.

- September 2025: Thrustmaster launched the T248R racing wheel priced at about USD 349, targeting budget-conscious sim racers seeking improved performance and accessibility in entry-level racing simulator setups.

REPORT COVERAGE

The global racing simulator market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Simulator Type, Level of Immersion, End User, and Region |

| By Component |

|

| By Simulator Type |

|

| By Level of Immersion |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.19 billion in 2025 and is projected to reach USD 2.46 billion by 2034.

In 2025, the market value stood at USD 0.42 billion.

The market is expected to exhibit a CAGR of 8.3% during the forecast period.

The static racing simulators segment led the market by simulator type.

The rising popularity of e-sports and sim racing competitions to accelerate market growth.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us