Radar Link Market Size, Share & Industry Analysis, By Link Type (Electronic Link and Optical Link), By Component (Antenna, Diplexer, Transmitter, Phase-Lock Loop, Receiver, Processor, and Others), By Application (Airborne, Naval, Space, and Land), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

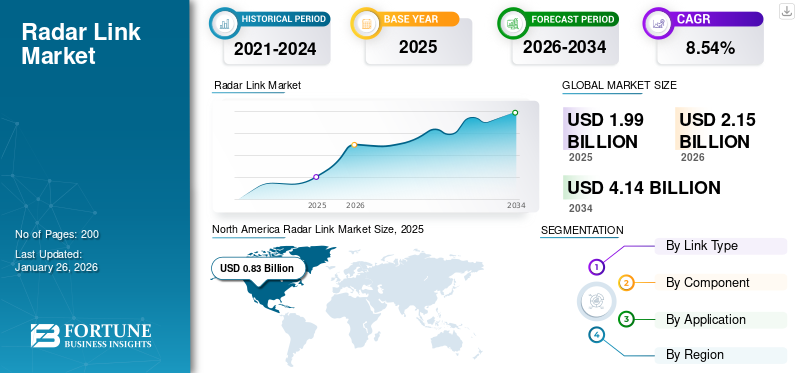

The global radar link market size was valued at USD 1.99 billion in 2025 and is projected to grow from USD 2.15 billion in 2026 to USD 4.14 billion by 2034, registering a CAGR of 8.54% over the forecast period. North America dominated the radar link market with a market share of 41.45% in 2025.

Radar is used in defense applications to detect air, land, and sea threats such as missiles, ships, aircraft, and spacecraft. Optical links can be categorized into two main types: electronic links and optical links. Electronic links are the traditional systems that use radio waves for communication, while optical links leverage fiber optics technology, offering advantages such as higher bandwidth, reduced weight, and improved efficiency. Applications of radar links are diverse, including military surveillance for detecting air, land, and sea threats, air traffic control in aviation, navigation in maritime operations, and advanced driver assistance systems in automotive technology. The integration of fiber optics into radar systems is expected to enhance performance and efficiency further. Additionally, the increasing focus on security and safety measures globally is likely to boost demand for radar links across various applications.

The key players in the market include AFL (U.S.), Amphenol Corporation (U.S.), Carlisle Companies Inc. (U.S.), Elbit Systems (Israel), II-VI Incorporated (U.S.), Ofs Fitel, LLC (U.S.) and among others. These players are focused in R&D activities to boost the market share and gain a competitive edge. The use of optical fibers in radar systems and radar sensors has gained popularity due to advantages such as reduction in weight, improved efficiency, higher bandwidth, and others. Fiber optics functions by means of the transmission of information and data by sending a pulse of light through optic fiber. The transmitted light forms an electromagnetic carrier wave to modulate data transfer. There are various advantages to using a fiber optic cable in radar links, as it has higher bandwidth and deploys cloud-based solutions.

Download Free sample to learn more about this report.

Global Radar Link Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.99 billion

- 2026 Market Size: USD 2.15 billion

- 2034 Forecast Market Size: USD 4.14 billion

- CAGR: 8.54% from 2026–2034

- North America dominated the radar link market with a 41.45% share in 2025.

- The electronic link segment is projected to account for a 62.02% market share in 2026.

- The airborne segment is projected to account for a 39.17% market share in 2026.

North America

The market was valued at USD 0.83 billion in 2025 and is projected to reach USD 0.90 billion in 2026.

Asia Pacific

The market was valued at USD 0.46 billion in 2025 and is expected to reach USD 0.49 billion in 2026.

Europe

The market was valued at USD 0.52 billion in 2025 and is projected to reach USD 0.56 billion in 2026.

U.S.

The market is projected to reach USD 0.57 billion by 2026.

Japan

The market is projected to reach USD 0.13 billion by 2026.

Read More

RADAR LINK MARKET TRENDS

Rising Technological Developments Fostered Adoption of Compact and Lightweight Hardware Components

In the traditional fiber optic approach, separate optic fibers are used for each point-to-point link. Such systems require three cable segments. The system is segmented into three sections, and a total of 8 fibers are used in each system. North America witnessed radar link market growth from USD 713.8 Million in 2023 to USD 766.4 Million in 2024.

Another approach in radar systems is the hybrid RF optical approach. In this system, one fiber carries all the RF signals, and another carries all RF signals in the opposite direction. In addition to fiber-optic transmitters and receivers, this approach also needs RF power combiners and RF demultiplexers.

The miniaturization and integration of radar systems are gaining traction, with advancements in semiconductor technology, materials science, and miniaturization enabling the development of these compact and lightweight systems. This trend opens up new applications and market segments, allowing radar technology to be incorporated into devices such as drones, autonomous vehicles, and wearable devices. Companies that invest in research and development to stay at the forefront of these technological advancements are distinguishing themselves in the competitive market.

Key OEMs in the optical fiber market have been replaced by all-optical approaches where Wavelength-Division Multiplexing (WDM) technology is used to send more than one wavelength through a single optical fiber. Using WDM, it is possible to share a single optical fiber to carry two or more optical channels simultaneously at different optical wavelengths.

- In December 2023, Fujitsu Limited and KDDI Research successfully created a large-capacity multiband wavelength multiplexing transmission technology utilizing existing optical fibers. These two firms have formulated a technology that allows for the transmission of wavelength bands outside of the C band, which has not been utilized in medium- and long-distance commercial optical communications through a batch wavelength conversion and multiband amplification method. The optical fiber communications network implemented with this technology facilitates wavelength transmission at 5. 2 times the wavelength multiplicity of current commercial optical transmission technology.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising International Security Threats and Disputes Among Neighboring Countries May Drive Market Growth

Rising international security threats and disputes among neighboring countries are significantly influencing the radar link market growth. As geopolitical tensions escalate, nations are increasingly prioritizing the enhancement of their defense capabilities, leading to a surge in demand for advanced radar systems. Countries facing border disputes or threats from neighboring nations are compelled to invest in sophisticated surveillance and detection technologies to ensure national security. This trend is particularly evident in regions such as Eastern Europe, the Asia Pacific, and the Middle East, where military modernization efforts are underway.

Emerging economies such as China and India are increasing their defense expenditure to modernize the conventional radar communication system. These countries increase spending on the procurement of optical fibers for various advantages such as weight/space saving, high sensitivity, low cost, high data rate, and improved security.

- In June 2024, Raytheon, a subsidiary of RTX, was awarded a contract valued at USD 677 million to continue the production of AN/SPY-6(V) radars for the United States Navy. This contract aims to supply seven additional radars, increasing the total procurement under this contract to 38 units. The AN/SPY-6 is an advanced radar system designed for air and missile defense, showcasing the U.S. commitment to bolstering its naval capabilities amidst geopolitical tensions.

Moreover, the radar link market growth is attributed to the increasing need to improve the safety and security of military personnel and the development of automated radar control, navigation systems, and fire control systems. Thus, the advent of using fiber optics in radar systems due to greater bandwidth, faster speed, and better reliability drives the market growth of radar links.

Increase in IT and Telecom Sectors in Growing Economies May Boost Market Growth

The increase in the IT and telecom sectors in growing economies is poised to boost the radar link market significantly. As India, China, and Brazil experience rapid economic growth, the demand for advanced communication technologies is escalating. This growth is driven by the need for enhanced data transmission capabilities, which are essential for modern applications such as smart cities, autonomous vehicles, and comprehensive surveillance systems. The integration of radar technology with IT and telecom infrastructure is becoming increasingly vital to support these advancements.

Radar systems equipped with optical fibers can provide high-speed, reliable connections that are resistant to interference. This capability is particularly important for defense applications where secure and efficient data transmission is critical for operational success. As nations prioritize their defense capabilities in response to rising security threats, investments in radar systems that leverage advancements in the IT sector will likely increase.

As more businesses and governmental organizations invest in IT infrastructure to support high-speed internet and data services, the demand for radar systems that can efficiently utilize these advanced communication networks is expected to rise. This collaboration between radar technology and telecommunications will facilitate improved signal processing and data transfer capabilities, further driving market growth.

MARKET RESTRAINTS

Complex Installation and Maintenance of Fiber Optic in Radar System Hinders Market Growth

Optical fiber requires the use of specialized and competent professionals for testing and evaluation when assembling optical fibers and for optical fusion splicing. Additionally, fiber optics are difficult to splice, and fiber optic cables are prone to light loss within the fiber due to scattering. Fiber optic cables have limited physical cable arcs and are difficult to cut.

In addition, fiber optic cables are small and compact cables susceptible to cutting and damage during installation and construction. These cables can provide tremendous data transmission capabilities. Therefore, recovery, backup, and survivability must be considered when choosing fiber optic cable as the transmission medium. Also, fiber optics are expensive to install as they need to be installed by a professional. They are not as robust as the copper wire or other cables used. Special fiber testing equipment is used during installation, which increases the overall installation cost of the bend radius of the fiber optic cable. This is the amount of bending that can be allowed before the cable is damaged, has increased attenuation, or limits bandwidth performance. Excessive bending of a fiber optic cable can cause optical signals to refract within the cable and escape through the fiber jacket. Bending can also permanently damage the fiber by causing micro-cracks. This factor makes it difficult to install and maintain fiber optics in radar systems.

Moreover, maintaining fiber optic systems poses additional challenges. Factors such as temperature variations, aging of optical components, and environmental conditions can affect the performance and accuracy of fiber optic sensors over time. Regular calibration and maintenance routines are essential but can be resource-intensive, requiring skilled technicians who are well-versed in fiber optics technology. The need for ongoing maintenance can deter organizations from adopting these systems, particularly if they lack the necessary expertise or resources.

Market Opportunities

AI-Driven Radar Systems and Space-Based Radar Links Represent Significant Market Opportunities

AI-enhanced radar systems are revolutionizing object classification and detection capabilities. By integrating artificial intelligence and machine learning algorithms, radar systems can now process vast amounts of data in real-time, providing immediate and meaningful insights. This technology enables more accurate differentiation between objects, such as vehicles and pedestrians, which is crucial for autonomous driving and Advanced Driver-Assistance Systems (ADAS). AI-driven radar systems offer superior performance in poor weather conditions and low-light environments, making them invaluable for safety and security applications.

Space-based radar links are gaining importance due to increased interest in space exploration and satellite communications. These systems play a crucial role in climate research, environmental monitoring, and defense applications. Additionally, the development of radar technology for Unmanned Aerial Vehicles (UAVs) is creating opportunities in surveillance, search and rescue operations, and industrial inspections. As these technologies continue to evolve, they present significant growth potential for the radar link market across diverse sectors.

Market Challenges

Regulatory Challenges Pose Significant Impact on the Market

The radar sector is heavily regulated, particularly in defense applications where compliance with national security standards is critical. These regulatory hurdles can create delays in product development and deployment, limiting the ability of companies to respond swiftly to market demands. Additionally, issues related to cybersecurity and data privacy are increasingly becoming concerns for radar technologies. As systems become more interconnected, ensuring the security of data transmitted through radar links is essential to prevent unauthorized access or interference.

Companies must invest heavily in research, testing, and certification processes to meet compliance standards. This can increase operational costs and limit resources available for innovation. Additionally, cybersecurity and data privacy regulations are becoming more stringent as radar systems increasingly rely on data connectivity and analytics. Organizations must ensure robust security measures to avoid potential breaches, further adding to development costs and operational hurdles.

Impact of COVID-19

During the COVID-19 pandemic, the market witnessed a decline in its operations. Moreover, with an increase in digitization, the popularity of IoT, and increasing demand for fiber optics cables will see a rise in market growth.

SEGMENTATION ANALYSIS

By Link Type

Electronic Link Segment to Lead Supported by Growing Demand for Radar Systems in Defense Applications

The market is divided into electronic link and optical link based on link type.

Electronic link segment is projected to reach the market, accounting for 62.02% of the global market share in 2026 as the defense sector's need for effective threat detection systems has led to a surge in demand for radar systems. This is expected to drive the electronic link segment, which remains the largest due to its robust adoption across various applications such as aerospace, marine, and land.

The optical link segment is expected to be the fastest-growing segment in the radar link market. The integration of optical fibers in radar systems provides significant advantages such as reduced weight, improved efficiency, higher bandwidth, and enhanced data transmission capabilities. Optical links are becoming increasingly popular due to their ability to handle larger volumes of data with greater speed and security, making them ideal for modern surveillance and weather radar systems.

By Component

Antenna Segment to Lead Due to its Utilization in Commercial and Military Applications and in Aviation Industry

The market is divided into antenna, diplexer, transmitter, phase-lock loop, receiver, processor, and others based on component.

The antenna is estimated to hold the market share by 17% in 2025. The growing deployment of radar systems for both military and commercial purposes is a primary driver. Antenna diplexer transmitter phase lock loops are crucial for emitting radio waves and receiving echoes, making them essential in applications such as air traffic control, naval operations, and weather monitoring. The heightened focus on defense capabilities and modernization efforts in various countries is further increasing the demand for sophisticated radar systems that rely heavily on advanced antennas.

- In November 2024, Honeywell received a USD 16 million contract from the U. S. Navy for the complete construction, testing, and integration of 25 antenna array panels that will support the Surface Electronic Warfare Improvement Program (SEWIP) Block 2. This contract award follows Honeywell’s USD 1. 9 billion purchase of CAES Systems Holdings, LLC.

The receiver segment held a 19.77% market share in 2026. The growth of this segment is due to increasing demand for next-generation radar phase lock loop receiver processors for real-time information in military operations.

By Application

To know how our report can help streamline your business, Speak to Analyst

Airborne Segment to Dominate Market Owing to Expansion of Aircraft Fleets with Advanced Radar Systems

By application, the market is divided into airborne, naval, space, and land.

The airborne segment is dominated by platform type, capturing 39.17% of the market share in 2026. Governments worldwide are prioritizing the modernization of their military capabilities, particularly in airborne systems. This includes significant investments in advanced radar technologies to enhance surveillance, reconnaissance, and targeting capabilities. The airborne segment will witness significant growth during the forecast period. The segment is expected to capture 38% of the market share in 2025.

The naval segment is also growing as countries invest in modernizing their naval fleets with advanced radar systems.The naval segment is expected to hold a 27.91% share in 2024. These systems are essential for maritime surveillance, anti-submarine warfare, and fleet defense operations. The increasing focus on securing maritime borders and enhancing naval operational capabilities is driving demand for sophisticated radar technologies in this sector.

RADAR LINK MARKET REGIONAL OUTLOOK

The global market is segmented, based on region, into North America, Europe, Asia Pacific, and the rest of the world.

North America Radar Link Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America recorded a market size of USD 0.83 billion in 2025, capturing 41.45% of the global market share, and is projected to reach USD 0.9 billion in 2026. North America is expected to witness the largest radar link market share during the projected period. The regional market value in 2024 was USD 1.041.5 million, and in 2023, the market value led the region by USD 858.7 million. The increased spending on the procurement of advanced radar systems for military solutions and the presence of a large number of hardware and software developers across the region drive the growth of the market size and forecast. The demand for radar link in North America is primarily driven by substantial government investments in defense technology, particularly in the U.S., which has the world's most advanced military capabilities. Ongoing modernization efforts in military aircraft, naval vessels, and border surveillance systems are critical factors contributing to this growth. Important manufacturers such as Lockheed Martin Corporation, General Dynamics Corporation, and Raytheon Technologies Corporation in North America are expected to strengthen the region's dominance in the global market. In June 2022, Carlisle Interconnect Technologies launched two new high-voltage composite wire families for aerospace applications, a high-voltage composite wire series and an ultra-flexible high-voltage shielded composite wire series. The U.S. market is projected to reach USD 0.57 billion by 2026.

Asia Pacific

The Asia Pacific market generated USD 0.46 billion in 2025, representing 22.94% of the global market landscape, and is expected to reach USD 0.49 billion in 2026. Factors such as rising terrorist activities, inter-country conflicts, and border security needs are driving demand for advanced radar systems. China and India are significantly investing in their military capabilities, which includes upgrading their radar technologies. In December 2024, Maxar Intelligence announced it was awarded USD 35 million in new tasking contracts from two government customers in the Asia Pacific region. These contracts focus on providing high-resolution imagery and Synthetic Aperture Radar (SAR) capabilities through Maxar’s advanced satellite systems, enhancing situational awareness for defense operations. The Japan market is projected to reach USD 0.13 billion by 2026, the China market is projected to reach USD 0.16 billion by 2026, and the India market is projected to reach USD 0.11 billion by 2026.

Europe

In 2025, Europe represented USD 0.52 billion, accounting for 26.12% of the worldwide market, and is projected to grow to USD 0.56 billion in 2026. Europe is anticipated to account for the second-highest market size of USD 855.6 million in 2025, exhibiting the second-fastest growing CAGR of 13.02% during the forecast period. Rising security concerns and the need for enhanced defense capabilities amid geopolitical tensions influence the European market. Additionally, collaborations among countries for joint defense projects are expected to bolster the radar systems market further. The presence of key players such as Radiall, TE Connectivity, and others drives the radar link market growth across Europe. In June 2023, Elbit Systems UK received a contract from the UK Ministry of Defence (MoD) to supply a range of ground-based surveillance radars, produced and created in the U.K. and Europe, to the British military to aid in frontline threat identification. The UK market is projected to reach USD 0.18 billion by 2026 and the Germany market is projected to reach USD 0.14 billion by 2026.

During the projection period, the rest of the world is anticipated to also witness significant growth during the forecast period. The rest of the world includes regions such as Latin America and the Middle East & Africa, where growth is slower compared to North America, Europe, and Asia Pacific. However, there are emerging opportunities due to increasing security concerns and investments in infrastructure. The market in Rest of the World reached USD 0.19 billion in 2025, representing 9.49% of total market revenue, and is projected to reach USD 0.2 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Increase in Utilization of Advanced Radar Systems Utilizing Fiber Optics by Major Participants to Propel Market Expansion

In the radar link sector, advanced radar systems using fiber optics technology are manufactured for military, naval, and other operations. Multiple key players such as Elbit Systems, Optical Cable Corporation, and others are focused on technology advancements and developing radar link systems to reduce the number of fiber optics, increase efficiency, and reduce the weight and size of the radar link system.

LIST OF KEY RADAR LINK COMPANIES PROFILED

- AFL (U.S.)

- Amphenol Corporation (U.S.)

- Carlisle Companies Inc. (U.S.)

- Elbit Systems (Israel)

- II-VI Incorporated (U.S.)

- Ofs Fitel, LLC (U.S.)

- Optical Cable Corporation (U.S.)

- Radiall (France)

- TE Connectivity (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- October 2024 - HENSOLDT entered into a contract with Space Centre Australia (SCA) to provide two advanced Air Surveillance Radar - Next Generation systems (ASR-NG), coupled with a 20-year maintenance plan to enhance Australia's essential air surveillance abilities. The overall order value of the initial phase amounts to approximately USD 20. 93 million.

- August 2024 - Northrop Grumman Corporation received its Deep-Space Advanced Radar Capability (DARC) Site 2 contract from the U. S. Space Force. The second location, situated in the U.K., furthers DARC’s goal of becoming one of the globe’s leading radars for monitoring objects in deep space. This contract comes after the earlier competitive award of DARC Site 1.

- June 2024 - Raytheon Technologies received a contract worth USD 677 million to carry on producing AN/SPY-6(V) radars for the U. S. Navy. This marks the third option executed from the hardware, production, and sustainment contract awarded in March 2022, which is valued at up to USD 3 billion over five years. Through this contract, the U. S. Navy will obtain seven more radars, raising the total number of radars under the procurement contract to 38.

- July 2024 - Indonesia has set up a Thales Ground Master 403 (GM403) air surveillance radar in the East Kalimantan province, situated in the Eastern region of Borneo Island. The GM403 radar has been placed to safeguard the airspace above the city of Nusantara, which is under construction to serve as Indonesia's future capital.

- June 2023 - The Ministry of Defence (MOD) granted BAE Systems a contract lasting 10 years valued at USD 341. 06 million to assist the Royal Navy with its three primary radar systems: Artisan, Sampson, and Long Range Radar (LRR).

REPORT COVERAGE

The research report provides qualitative and quantitative insights into the market and a complete analysis of market size and growth rate for all market segments. The report also includes an in-depth look at market dynamics, emerging trends, and the competitive landscape. It offers the adoption trends of fiber optics by individual segments, recent industry developments such as partnerships, mergers, and acquisitions, consolidated SWOT analysis of key players, Porter's Five Forces analysis, leading business strategies of market players, and key industry trends are among the key insights offered in the report.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.54% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Link Type

|

|

By Component

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 1.99 billion in 2025 and is projected to grow from USD 2.15 billion in 2026 to USD 4.14 billion by 2034

The market is likely to grow at a CAGR of 8.54% during the forecast period of 2026-2034.

Link type is the fastest segment in the market.

AFL, Amphenol Corporation, Carlisle Companies Inc., Elbit Systems, and II-VI Incorporated are the major players in the market.

North America dominated the market in terms of share in 2024.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us