Radar Security Market Size, Share & Industry Analysis, By Offering (Hardware, Software, and Services), By Radar Type (Mechanical Scanning Radar, Electronic Scanning Radar, Pulse-Doppler Radar, & Others), By Frequency (HF/VHF/UHF, L-Band, S-Band, C-Band, X-Band, and Ku/K/Ka Band), By Range (Capability, Short, Medium, Long & Ultra-Long Range), By Security Application (Perimeter & Border Security, Critical Infrastructure Protection, Maritime & Coastal Security, and Others), By Platform (Ground-Based, Airborne, Naval Maritime and Space), By End User, and Regional Forecast, 2026-2034

Radar Security Market Size and Future Outlook

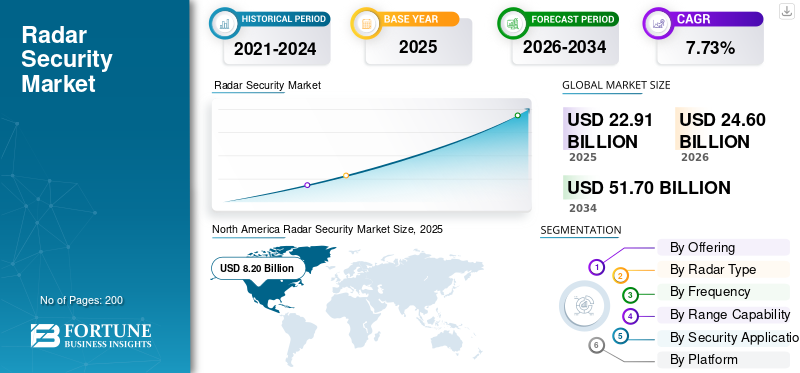

The global radar security market size was valued at USD 22.91 billion in 2025. The market is projected to grow from USD 24.60 billion in 2026 to USD 51.70 billion by 2034, exhibiting a CAGR of 9.73% during the forecast period. North America dominated the global radar security market with a market share of 35.8% in 2025.

The radar security systems allow for the detection, tracking, and classification of intruding targets in real-time, whether it be humans, vehicles, or drones, by using radio frequency technology. Unlike traditional optical surveillance, these systems work well in all weather conditions, from fog and rain to total darkness. That is why they are so important for perimeter protection. They are widely deployed across high-stakes environments, including national border control, marine surveillance radar (MSR) systems, ground surveillance radar (GSR) systems, air surveillance radar (ASR) systems and critical infrastructure including airports, seaports, and oil refineries.

Major defense primes lead the sector, with RTX, Lockheed Martin, and Northrop Grumman dominating high-end military contracts, while European innovators including Thales and Saab strongly compete based on specialized critical infrastructure solutions.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Escalating Global Security Concerns and Geopolitical Instability Cater Robust Security Demand

The radar security market continues to see strong growth due to increasing security apprehensions and geopolitical unrest across the world. Increasing territorial disputes, cross-border intrusions, and terrorism compelled many governments to invest extensively in state-of-the-art long range radar surveillance systems to ensure real-time threat detection and quick response capabilities. In addition, the increasing usage of UAVs and drones for various applications has created new demands for radar systems with air traffic control, perimeter surveillance, and counter-drone operations, thereby expanding the market.

Market Restraints

High Cost of Systems Can Hinder Market Growth

The radar security market growth is hindered by various critical restraints despite the rapid pace of technological advancement. A major barrier remains the high cost of development and maintenance, especially considering sophisticated systems with advanced infrastructure, networking, and software integration.

Deploying and operating radar systems in especially populated or urban environments can be extremely complex, usually promoting higher power consumption, heat dissipation, and interference issues, which become a disadvantage for widespread adoption. Furthermore, complications such as the lack of skilled personnel who can interpret radar data and manage AI-driven platforms add to system deployment and operational efficiency.

Market Opportunities

Growing Sensor Fusion Technology Catalyze Global Market Growth

Multi-sensor fusion technologies are going to enable a wide range of new security applications for the growth of the radar security sector. Thus, putting together radar with video surveillance, LiDAR, and thermal imaging enhances the accuracy of detection and situational awareness, therefore opening up new frontiers in both defense and smart city applications.

It also increases the scope of the market by opening new revenues for other non-traditional areas such as transportation safety, monitoring of highways, and anti-collision systems of trains. The growing demand for autonomous vehicles and industrial automation will keep the pressure on innovation for smaller, affordable radar sensors that will be of higher resolution and multifunctional.

Market Challenges

Technical Complexity Associated With Advanced Systems Hinder Market Growth

Different challenges continue to confront the radar security industry, including high costs and technical complexity associated with advanced systems. Deployment of multi-function radars and cognitive radar platforms often involves hefty investment in research and development and special infrastructure for mounting, powering, and networking.

Regulatory hurdles, especially within the defense sector, create additional complications for international expansion and radar technology transfer, while cybersecurity vulnerabilities continue to present ongoing risks to system integrity and data confidentiality. The requirement for this convergence of physical and information security frameworks calls for comprehensive approaches that meet hardware and software protection needs.

Radar Security Market Trends

Escalating Massive Technological Development Such As AI and ML Drives Technology Trend

The radar security sector is seeing massive technological development, wherein AI and machine learning are at the forefront of innovation. Cognitive radars, which would employ the power of AI in adapting to dynamic environments and enhancing target identification, are becoming increasingly prevalent in both military and commercial deployments. Integration of 5G and above technologies can enable enhanced connectivity and real-time data transfer, supporting the deployment of networked radar systems for improved situational awareness and collaborative operations. Miniaturization and portability are among the developing trends, where firms are working toward developing smaller and more cost-effective sensors for consumer electronics and industrial security applications anticipate the demand for advanced radar systems across globally.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Offering

Real-Time Data Processing and AI-Driven Operator Assistance Catalyze Segmental Growth

The global market is segmented by offering into hardware, software, and services

The software sub-segment of the radar security market is exhibiting the fastest growth trajectory, driven by the industry's structural transition toward software-defined radar architectures, AI-enabled signal processing, and cloud-based operational frameworks. The software components have expanded from basic target tracking and display functions to sophisticated AI and machine learning algorithms capable of real-time threat classification, adaptive threat assessment, and autonomous decision support across complex electromagnetic environments.

The hardware sub-segment is accounted for the largest market share with holding the 60.60% share of the global radar security market share.

To know how our report can help streamline your business, Speak to Analyst

By Radar Type

Multi-Function 4D Situational Awareness and Beam forming Superiority Drives Segmental Growth

The global market is segmented by radar type into mechanical scanning radar, electronic scanning radar, pulse-doppler radar, continuous-wave radar, synthetic aperture radar (SAR), and others.

The electronic scanning radar sub-segment covers AESA and PESA technologies, holding the dominant market position with around 42.67% of the total value of the global market share. Additionally, it has the fastest growth trajectory among all radar type classifications. Growth is much greater than decline rates on mechanical scanning radars and reflects a methodical transition toward modern electronically steered architectures from previous mechanically scanned array (MSA) platforms.

The continuous-wave radar sub-segment is estimated to the second fastest growing during the forecast period of 2026-2034 with a CAGR of 10.75%.

By Frequency

Frequency Modulated Continuous-Wave (FMCW) Miniaturization and Autonomous Vehicle Integration Anticipate Segmental Growth

The global market is segmented by frequency into HF/VHF/UHF, L-band, S-band, C-band, X-band, and Ku/K/Ka band.

The Ku/K/Ka band sub segment is expected to represent the fastest growth with a compound annual growth rate of 15%, higher than any other band, through the forecast period, 2026-2034, since regulatory mandates require the installation of advanced driver assistance systems with features such as automatic emergency braking, adaptive cruise control, and blind spot detection in global automotive markets. Moreover, Ku/K/Ka band FMCW radar demonstrates excellent miniaturization capability for compact integration across autonomous vehicle platforms, passenger vehicle ADAS systems, and emerging civil infrastructure applications such as robotics, drone detection, and smart city surveillance.

The S-band sub-segment dominates the global market size and the segment is growing with a 10.62% CAGR.

By Range Capability

Strategic Ballistic Missile Detection and Hypersonic Threat Early Warning Anticipate Market Growth

The global market is segmented by range capability into short range < 5 km, medium range 5-30 km, long range 30-250 km, and ultra-long range > 250 km+.

The ultra-long range radar sub-segment includes early warning radars, over-the-horizon systems, and strategic air defense platforms, and it is the fastest-growing range classification, with a compound annual growth rate of around 11.09% through 2026-2034, significantly outpacing medium-range tactical radar growth rates. Strategic requirements for early warning and ballistic missile defense are driving systematic investment in extended-range surveillance capabilities, and globally, defense budgets are prioritizing platforms capable of providing strategic warning for nuclear missile attacks.

The medium range 5-30 km accounted for the largest market share in the global market and grow at 10.53% CAGR form 2026-2034.

By Security Application

Perimeter Protection and Critical Infrastructure Defense against Emerging Threats Catalyze Market Growth

The global market is segmented by security application into perimeter & border security, critical infrastructure protection, maritime & coastal security, airspace security, military & defense security, homeland security, and civil security.

The perimeter and border security sub-segment is the fastest-growing security application classification by a wide margin, substantial outpacing growth rates in military and defense security segments. Border security priorities have systematically risen due to transnational terrorism threats, smuggling networks, human trafficking organizations, and irregular migration pressures that have established perimeter and border security as key government responsibilities.

Military & Defense Security dominates the global market share and grow at a 10.07% CAGR during the forecast period.

By Platform

Space-Based SAR Technology Advantages and All-Weather Operational Capability Cater Market Growth

The global market is segmented by platform into ground-based, airborne, naval / maritime, and space.

The space-based radar sub-segment is the fastest-growing classification of platform, with compound annual growth rates of 10.16% through 2026-2034 significantly outpacing expansion rates on the ground and reflecting systematic government investment in strategic orbital surveillance infrastructure. Commercial space-based Synthetic Aperture Radar (SAR) satellite constellations are seeing explosive growth driven by commercial demand for persistent all-weather imagery, environmental monitoring, disaster response, and maritime domain awareness applications.

The ground-based radar sub-segment maintains commanding market dominance with approximately 53.22% of total radar market value. Ground radars work as a backbone for air defense systems, air traffic control systems, and weather radars. Ground radars have higher production quantities in contrast to naval radars, which are limited by the number of ships, and aircraft radars, which are constrained by aircraft numbers.

By End User

The Growing Application of Commercial Flights and Increasing Infrastructure Drives the Segmental Growth

The global market is segmented by end user into government & defense and commercial & civil.

The commercial and civil is the fastest-growing sub-segment, representing a compound annual growth rate of approximately 10.98%. Growth is driven by autonomous vehicle development, regulatory mandates for ADAS, proliferation of industrial automation, and modernization initiatives in commercial aviation.

The government and defense end-user sub-segment maintains commanding market dominance with approximately 81.80% of total radar security market value, reflecting sustained government defense spending exceeding significantly.

Radar Security Market Regional Outlook

By geographic, the market is categorized into North America, Europe, Asia Pacific, and Rest of World

NORTH AMERICA

North America continues to dominate the market due to hefty government investments in defense and due to technological advancements. Indeed, the strategic commitment of the U.S. Navy to the SPY-6 family of radars is a trend marker that shapes the landscape of radar security in this region. In June 2025, Raytheon Technologies received a USD 536 million contract from the U.S. Navy, which involves the integration, test, and software upgrade for the SPY-6 system deployed across naval platforms and expected to equip more than 60 ships over the next decade.

The U.S. market is a mirror image of the global market but with an intensity factor prevalent in defense expenditure. The market is largely imbalanced toward Military/Defense. The U.S. defense industry represents over 89.83% of the total market share in the North American radar market. Their intensity is driven by the Great Power Competition strategy against rival nations (China/Russia). The U.S. Army is replacing old technology with LTAMDS (Lower Tier Air and Missile Defense Sensor) technology, which is a 360-degree Gallium Nitride (GaN) Radar, a major income driver in this market.

North America Radar Security Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

EUROPE

The European region represents the fastest growth trajectory driven by NATO's IAMD refresh policy and multinational procurement initiatives. A case in point is Denmark's announced procurement of the SAMP/T NG air-defense system in September 2025, which underlines momentum within Europe toward state-of-the-art, long-range surveillance capabilities. These synchronized European government contracts underpin a structural shift toward indigenous, interoperable radar solutions to address cruise missile, ballistic missile and hypersonic threats across the continent.

ASIA PACIFIC

The expansion in the Asia Pacific region is rapid, driven by regional defense modernization programs and growing geopolitical tensions both in maritime and terrestrial domains. India's roadmap for defense modernization has included the Akash-NG Surface-to-Air Missile system, which was operationalized in tandem with the DRDO and Bharat Electronics Limited, allowing longer-range detection capability of up to 70 km with better reaction times.

REST OF THE WORLD

The Middle East and Africa offer significant growth opportunities, driven by security imperatives and investments in infrastructure modernization. Both Middle East & Africa and Latin America regions remain dependent on international defense contractors and radar technology providers, as avenues for partnership, localized manufacturing, and solutions adapted to regional security priorities continue. Implementation is still severely limited by cybersecurity concerns, technical expertise, and variable government funding cycles.

COMPETATIVE LANDSCAPE

Key Industry Players

Growing Development of Technological Capability, Geopolitical Positioning by Major Key Players Drives Market Growth

These solutions form a competitive landscape segregated into three distinct tiers, reflecting technological capability, scale of contract procurement, and geopolitical positioning. The first tier consists of six primary defense contractors including Raytheon Technologies, Thales Group, Lockheed Martin, Northrop Grumman, Leonardo SpA, and Indra Group, which together capture around 45-50% of the value in the global military radar market through their respective offerings for integrated air and missile defense systems, space surveillance platforms, and NATO-standardized command and control architectures.

The second tier consists of regional and emerging innovators such as Saab, Hensoldt, BAE Systems, L3Harris Technologies, and Bharat Electronics Limited, which will compete based on a range of specialized tactical radar systems, counter-UAS capabilities, and indigenous manufacturing models targeting regional customers and specific military operational needs. It is the third tier that will see emerging technology providers and niche specialists working on advanced 4D imaging radars, passive electro-optic/infrared sensing systems, and AI-enabled signal processing solutions for autonomous vehicle safety, smart city applications, and next-generation tactical maneuver platforms.

List of Key Radar Security Companies Profiled

- Thales Group (France)

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Saab AB (Sweden)

- Leonardo S.p.A. (Italy)

- HENSOLDT AG (Germany)

- Bharat Electronics Limited (BEL) (India)

- Elbit Systems Ltd. (Israel)

- Indra Sistemas, S.A. (Spain)

- ST Engineering Ltd (Singapore)

- BAE Systems plc (U.K.)

- Mitsubishi Electric Corporation (Japan)

- ASELSAN A.Ş. (Turkiye)

- Airbus SE (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Blighter has secured a follow-on contract with a military client in South East Asia to provide its Blighter B400 series radars for border surveillance purposes. These radars will be mounted by Blighter’s regional systems integration partner on specialized army vehicles for quick deployment to areas prone to border infiltrations.

- July 2025: The Navratna Defence Public Sector Undertaking, Bharat Electronics Limited, has finalized an important agreement with the Ministry of Defence worth USD 13.23 million for delivering Air Defence Fire Control Radars to the Indian Army.

- September 2025: Parsons Corporation has received an USD 81 million Task Order through the Responsive Strategic Sourcing for Services (RS3) contract vehicle from the U.S. Army Combat Capabilities Development Command's (DEVCOM) Command, Control, Communications, Computers, Cyber, Intelligence, Surveillance, and Reconnaissance (C5ISR).

- October 2025: Blighter has obtained a follow-up contract from an unnamed military client in Southeast Asia to provide B400 series radar systems for monitoring borders. These systems are engineered to enhance situational awareness, allowing operators to identify, monitor, and categorize small surface targets and low-flying aerial threats.

- October 2025: Saab has been awarded a contract by the NATO Support and Procurement Agency (NSPA) to extend the operational life of the Spanish Army’s Arthur radar systems. This extension will enhance the mobility of the Spanish Arthur radars while enabling accurate counter-battery operations, allowing for the detection of a greater number of targets over longer distances while maintaining a lower electronic signature.

REPORT COVERAGE

The global radar security market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.73% fro, 2026-2034 |

| Unit | USD Billion |

| Segmentation | By Offering, By Radar Type, By Frequency, By Range Capability, By Security Application, By Platform, By End User, By Region |

|

By Offering

By Radar Type

By Frequency

By Range Capability

By Security Application

By Platform

By End User

|

|

| By Region |

North America (By Offering, By Radar Type, By Frequency, By Range Capability, By Security Application, By Platform, By End User, By Country)

Europe (By Offering, By Radar Type, By Frequency, By Range Capability, By Security Application, By Platform, By End User, By Country)

Asia Pacific (By Offering, By Radar Type, By Frequency, By Range Capability, By Security Application, By Platform, By End User, By Country)

Rest of World (By Offering, By Radar Type, By Frequency, By Range Capability, By Security Application, By Platform, By End User, By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 22.91 billion in 2025 and is projected to reach USD 51.70 billion by 2034.

In 2025, the market value stood at USD 5.80 billion

The market is expected to exhibit a CAGR of 9.73% during the forecast period of 2026-2034.

The ground based radar segment is expected to hold the highest market share over the forecast period.

Escalating global security concerns and geopolitical instability cater the robust security demand.

Raytheon Technologies, Lockheed Martin, Thales Group, Saab AB, Bharat Electronics Limited, and among others are top players in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us