Radiation Detection, Monitoring & Safety Market Size, Share & Industry Analysis, By End User (Military & Defense, Space & Aerospace Agencies, & Research & Emergency Response), By Offering (Hardware, Software, & Services), By Technology (Geiger-Muller, Scintillation, Spectroscopic, Neutron Detection), By Radiation Type (Alpha, Beta, Gamma, X-ray, Neutron, & Mixed-field), By Product Type (Personal Radiation Detectors & Dosimeters, Handheld Survey & Identification Instruments, Area & Environmental Radiation Monitors, Portal & Fixed Radiation Monitoring Systems), & Regional Forecast, 2026-2034

Radiation Detection Monitoring and Safety Market

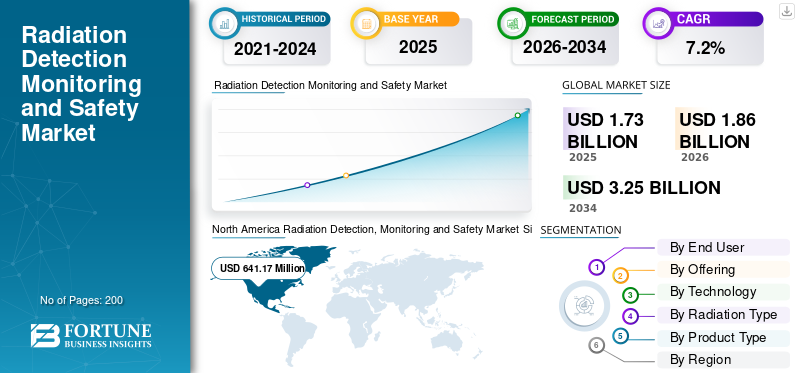

The global radiation detection, monitoring and safety market size was valued at USD 1,739.2 million in 2025. The market is projected to grow from USD 1,865.4 million in 2026 to USD 3,259.2 million by 2034, exhibiting a CAGR of 7.2% during the forecast period. North America dominated the radiation detection monitoring and safety market with a market share of 36.87% in 2025.

The radiation detection, monitoring and safety market is centered on technologies used to detect, identify, measure, and manage radiological threats and exposure across military, homeland security, emergency response, and aerospace operations. The market is supported by sustained emphasis on nuclear security detection architectures, layered screening systems, and rapid field identification of radioactive sources. Demand is also reinforced by the need for reliable radiation awareness in mission-critical environments, including base security, border protection, incident response, and space operations. As procurement priorities evolve, buyers are increasingly favoring integrated solutions that combine detection hardware, analytics, monitoring software, calibration, and lifecycle support services.

Key players in the market include Mirion Technologies, Thermo Fisher Scientific, Kromek Group, AMETEK ORTEC, and Polimaster. These companies compete through stronger radiation detection accuracy, broader product portfolios, handheld and fixed monitoring systems, isotope identification capabilities, and integrated safety solutions tailored for defense, border security, emergency response, critical infrastructure, and aerospace-related applications.

Download Free sample to learn more about this report.

RADIATION DETECTION, MONITORING AND SAFETY MARKET TRENDS

Integrated & Networked Detection Architectures are Emerging as Defining Market Trend

Shift from standalone radiation instruments toward integrated detection architectures that connect handheld tools, portal systems, area monitors, spectroscopy, analytics, and command-level visibility. Buyers increasingly want systems that do more than just alarm; they want platforms that can identify sources, support rapid decision-making, and integrate into broader security and response workflows. This is pushing vendors toward smarter software layers, better isotope identification, stronger interoperability, and mission-ready packages rather than single-device sales. The trend is especially visible in border security, emergency response, and defense environments, where layered detection and coordinated response matter more than isolated hardware performance.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Nuclear Security Preparedness and Persistent Threat Awareness Continue to Support Market Expansion

A primary driver of the radiation detection, monitoring and safety market growth is the sustained requirement to detect, identify, and respond to unauthorized or hazardous radioactive material across defense and security environments. Governments and related agencies are continuing to strengthen nuclear security detection architectures to support interdiction, screening, and coordinated incident response, thereby sustaining demand for personal detectors, handheld identifiers, portal systems, and radiation monitoring networks. This demand also extends into aerospace applications, where radiation monitoring remains essential for mission assurance and operational safety. As a result, radiation awareness has become an integral component of preparedness planning, safety management, and broader national security strategy.

MARKET RESTRAINTS

Calibration, Compliance, and Lifecycle Support Requirements Limit the Pace of Adoption

A key restraint affecting market expansion is the operational burden associated with maintaining system accuracy, compliance, and long-term readiness. Radiation detection instruments require rigorous calibration, traceability, testing, and maintenance, all of which increase operational complexity and add to ownership costs over time. In addition, many programs must comply with technical standards, regulatory frameworks, and procurement requirements before systems can be deployed at scale. This creates a more demanding adoption pathway compared with other sensing technologies. Consequently, even where demand is well established, installation, certification, maintenance planning, and lifecycle support obligations can delay procurement and lengthen deployment timelines.

MARKET OPPORTUNITIES

Expanding Border Security, Mobile Detection, and Space Monitoring Needs are Creating a Strong Market Opportunity

The strongest opportunity lies in modernizing legacy radiation-monitoring fleets with more mobile, connected, and mission-specific systems. Border checkpoints, ports, critical infrastructure, and emergency-response agencies continue to need better screening and identification tools. At the same time, aerial and vehicle-mounted systems open the door to wider-area detection missions. Another major opportunity is emerging in aerospace and space operations, where continuous radiation awareness is becoming more important for human spaceflight, satellite resilience, and mission planning. Vendors that can combine portable hardware, reliable analytics, traceable calibration, and flexible deployment models are well-positioned to capture new demand across defense, homeland security, and aerospace use cases.

MARKET CHALLENGES

Balancing Detection Accuracy with False Alarm Reduction and Operational Simplicity is a Key Market Challenge

A major challenge in this market is achieving high-confidence detection performance under real-world operating conditions while minimizing false alarms, misidentification risks, and user complexity. End users require systems that can reliably distinguish benign radioactive sources from genuine threats, while also remaining practical and efficient to operate in time-sensitive environments. This creates a persistent trade-off between sensitivity, selectivity, response speed, and ease of use. The challenge becomes more pronounced when solutions must operate consistently across handheld, mobile, portal, and aerial platforms while maintaining interoperability and serviceability. Therefore, market success depends on technical performance, usability, training effectiveness, and long-term sustainment capability.

Segmentation Analysis

By End User

Rising Force-Protection and Counter-Smuggling Missions to Foster Military & Defense Segment Growth

Based on end user, the market is segmented into military and defense, space and aerospace agencies, and research and emergency response.

The military and defense segment is anticipated to account for the largest radiation detection, monitoring and safety market share. Military users drive the market, as national nuclear security detection architectures require deployable, rugged systems for border screening, base protection, CBRN response, and nuclear material interdiction. As defense budgets rise and radiological threat preparedness stays active, procurement remains focused on dosimeters, portable detectors, portal systems, and networked monitoring tools.

The space and aerospace agencies segment is anticipated to rise with a CAGR of 7.9% over the forecast period.

By Offering

Expanding Frontline Screening and Fixed-Site Monitoring Needs Boosted Hardware Demand

Based on offering, the market is segmented into hardware, software, and services.

In 2025, the hardware segment dominated the global market. This market is still hardware-heavy as the frontline mission depends on physical equipment: personal detectors, handheld identifiers, portal monitors, area monitors, and vehicle-mounted systems. As ports, borders, bases, and emergency teams modernize layered detection, hardware keeps taking the largest procurement share and the biggest replacement burden.

The software segment is projected to grow at a CAGR of 8.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Fast Response and Broad Deployment Flexibility to Boost Demand for Scintillation Systems

Based on technology, the market is segmented into Geiger-Muller, scintillation, spectroscopic, neutron detection, and others.

The scintillation segment is anticipated to witness a dominating market share over the forecast period. Scintillation technology stays in demand as it is widely used in portal monitors and many handheld systems for practical gamma screening and rapid alarms. Its combination of sensitivity, speed, and operational scalability makes it attractive for high-throughput checkpointing, emergency screening, and field deployments where large-area coverage is critical.

The spectroscopic segment is projected to grow at a high CAGR of 8.3% over the forecast period.

By Radiation Type

Gamma Segment Led Market Due to Wide Operational Relevance in Screening and Surveillance

Based on radiation type, the market is segmented into alpha, beta, gamma, X-ray, neutron, mixed-field.

The gamma segment dominated the market share. Gamma detection remains central as it is the principal mobile instrument for radiation monitoring and a core function in portal and emergency screening systems. Since border control, incident response, and routine surveillance all depend heavily on gamma measurement, this segment continues to absorb the broadest operational demand.

The mixed-field segment is projected to grow at a CAGR of 8.4% during the study period.

By Product Type

Second-Line Inspection and Rapid Isotope Assessment Bolstered Handheld Survey and Identification Instrument Demand

Based on product type, the market is segmented into personal radiation detectors and dosimeters, handheld survey and identification instruments, area and environmental radiation monitors, portal and fixed radiation monitoring systems, and others.

The handheld survey and identification instruments segment dominated the market. Once a portal or personal detector alarms, operators need portable tools that can localize radiation and distinguish harmless sources from genuine threats. That keeps handheld survey meters and radioisotope identifiers in steady demand across ports, checkpoints, emergency teams, and military response units handling radiological incidents.

Area and environmental radiation monitors are projected to grow at a CAGR of 8.1% during the study period.

Radiation Detection, Monitoring and Safety Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Radiation Detection, Monitoring and Safety Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 598.65 million, and also maintained the leading share in 2025, with USD 641.17 million. North America leads, with the U.S. combining the world’s largest defense budget with large-scale cargo screening, while Canada also uses border radiation portals, carborne units, and national radiological monitoring networks.

U.S. Radiation Detection, Monitoring and Safety Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 625.9 million in 2026, accounting for roughly 6.7% of global sales. The demand in the country is strongest as it pairs the world’s largest defense budget with extensive port and border screening using portal monitors and RIIDs, creating constant upgrade and replacement demand.

Europe

Europe is estimated to reach USD 530.3 million in 2026 and secure its position as the third-largest region in the market. Europe’s demand is rising as military expenditure jumped sharply in 2024, and governments are reinforcing radiation response resilience. The U.K. is upgrading its monitoring network, while Germany maintains nationwide radioactivity surveillance through IMIS.

U.K. Radiation Detection, Monitoring and Safety Market

The U.K. market size in 2026 is estimated at around USD 91.5 million, representing roughly 6.9% of global sales. The U.K. market is rising as defense spending remains above 2% of GDP and the government is upgrading the Radiation Monitoring Network, supporting fresh demand for resilient sensors and response systems.

Germany Radiation Detection, Monitoring and Safety Market

Germany’s market is projected to reach approximately USD 109.7 million in 2026. Germany’s demand is rising as military expenditure surged, and IMIS continues nationwide environmental radioactivity surveillance, supporting investment in fixed monitoring, analytics, portable instruments, and radiological civil-protection capabilities.

Asia Pacific

Asia Pacific is projected to grow at 8.0% during the forecast period, the highest among all regions, and reach a valuation of USD 480.9 million in 2026. Asia Pacific is the fastest-rising market as defense modernization and radiation-monitoring expansion are moving together. China operates a large national monitoring system, Japan maintains environmental radiation monitoring, and India maintains radiological emergency preparedness.

China Radiation Detection, Monitoring and Safety Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 206.3 million. China remains a major demand center as military modernization continues, while a three-tier national radiation environment monitoring system supports ongoing procurement of fixed, mobile, and emergency-monitoring equipment.

Japan Radiation Detection, Monitoring and Safety Market

The Japanese market size in 2026 is estimated at around USD 78.8 million, accounting for roughly 7.2% of global revenues. Japan’s demand stays firm as defense spending rose sharply and the Nuclear Regulation Authority maintains environmental radioactivity monitoring, supporting procurement of fixed monitoring systems, portable survey tools, and emergency-response equipment.

India Radiation Detection, Monitoring and Safety Market

The India market in 2026 is estimated at around USD 88.4 million. India’s demand is increasing as defense spending grows and radiological emergency preparedness remains important. That keeps the need high for handheld detectors, area monitoring systems, and response-ready radiation-safety equipment.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market space during the forecast period. The Middle East & Africa and Latin America markets are set to reach a valuation of USD 116.4 million and USD 52.8 million in 2026, respectively. The rest of the world demand is smaller but steady, led by Middle East security spending and selective Latin American and African preparedness needs. Border control, critical-infrastructure security, and emergency response still support detector procurement.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated Product Expansion, Detection Innovation, and Lifecycle Support Strategies by Key Players are Strengthening Market Growth

Key players such as Mirion Technologies, Thermo Fisher Scientific, Teledyne FLIR Defense, Smiths Detection, Rapiscan Systems, Leidos, Bertin Technologies, Kromek Group, AMETEK ORTEC, and Polimaster are supporting market growth through strategies centered on broader product portfolios, stronger handheld and portal-based detection capabilities, higher-accuracy isotope identification, and more integrated monitoring solutions. Several companies are moving beyond standalone instruments toward networked, mission-ready offerings that combine hardware, software, analytics, training, calibration, and maintenance support. Their continued focus on rugged field performance, interoperability, rapid threat identification, and full-lifecycle service is improving user confidence, expanding operational adoption, and helping accelerate modernization across defense, border security, emergency response, and aerospace radiation-safety applications.

LIST OF KEY RADIATION DETECTION, MONITORING AND SAFETY COMPANIES PROFILED

- Mirion Technologies (U.S.)

- Thermo Fisher Scientific (U.S.)

- Teledyne FLIR Defense (U.S.)

- Smiths Detection (U.K.)

- Rapiscan Systems (U.S.)

- Leidos (U.S.)

- Bertin Technologies (France)

- Kromek Group (U.K.)

- AMETEK ORTEC (U.S.)

- Polimaster (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Ukraine published tenders for the construction of radiation shelters and the disposal of Cobalt-60 sources.

- March 2026: Adani Airport Mumbai issued an Expression of Interest for the supply, installation, testing, and commissioning of Radiological Detection Equipment (RDE).

- March 2026: IAEA launched a Coordinated Research Project (CRP) to develop advanced nuclear-based Non-Destructive Testing (NDT)

- September 2025: Mirion Technologies partnered with the International Atomic Energy Agency (IAEA) to strengthen radiation detection and measurement capabilities at the Terrestrial Environmental Radiochemistry (TERC) Laboratory.

- July 2024: Teledyne FLIR secured a USD 35 million contract from the US Department of Homeland Security (DHS) for cargo-inspection spectrometers.

REPORT COVERAGE

The global radiation detection, monitoring and safety market research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.2% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By End User, By Offering, By Technology, By Radiation Type, By Product Type, and Region |

| By End User |

|

| By Offering |

|

| By Technology |

|

| By Radiation Type |

|

| By Product Type |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1,739.2 million in 2025 and is projected to reach USD 3,259.2 million by 2034.

In 2025, the market value in North America stood at USD 641.17 million.

The market is expected to exhibit a CAGR of 7.2% during the forecast period of 2026-2034.

By end user, the military & defense segment is expected to dominate the market.

Nuclear security preparedness and persistent threat awareness continue to support market expansion.

Mirion Technologies, Thermo Fisher Scientific, Teledyne FLIR Defense, Smiths Detection, Rapiscan Systems, and Leidos are a few major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us