Radiation Toxicity Treatment Market Size, Share & Industry Analysis, By Drug Class (Cytoprotective Agents, Salivary Stimulants/Cholinergic Agonists, Topical Corticosteroids, and Others), By Disease Indication (Oral Mucositis, Radiation Dermatitis, Xerostomia/Salivary Gland Dysfunction, Radiation Proctitis, and Others), By Age Group (Pediatric and Adults), By Type (Branded and Generics), By Route of Administration (Oral, Topical, Parenteral, Rectal, and Others), By Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, and Others) and Regional Forecast, 2026-2034

Radiation Toxicity Treatment Market Size and Future Outlook

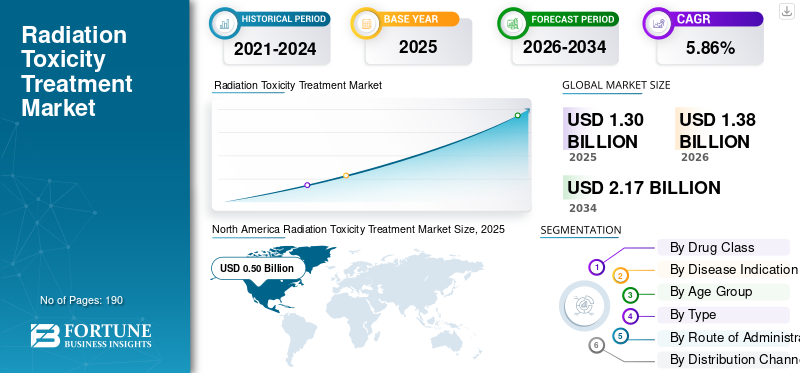

The global radiation toxicity treatment market size was valued at USD 1.30 billion in 2025. The market is projected to grow from USD 1.38 billion in 2026 to USD 2.17 billion by 2034, exhibiting a CAGR of 5.86% during the forecast period. North America dominated the radiation toxicity treatment market with a market share of 50.% in 2025.

The global radiation toxicity treatment market includes products and therapies used to prevent, reduce, or manage side effects caused by radiation exposure during cancer treatment. The market is growing because radiotherapy remains a major cancer treatment approach. Still, it can also damage nearby healthy tissue and lead to complications such as skin reactions, oral mucositis, fatigue, and other site-specific toxicities. As a result, healthcare providers are placing greater focus on supportive care solutions that help patients tolerate treatment better, avoid interruptions, and improve overall treatment outcomes.

- For instance, in March 2026, Siemens Healthineers announced that its Varian TrueBeam radiotherapy systems, including TrueBeam, TrueBeam STx, VitalBeam, and Edge, have received FDA 510(k) clearance for low-dose radiation therapy (LDRT) in adults with medically refractory osteoarthritis (OA). This clearance expanded the company’s radiotherapy systems beyond cancer care.

Furthermore, major players, such as Stratpharma AG, Flen Health, KeraNetics, and Solventum, are expanding their offerings.

Download Free sample to learn more about this report.

RADIATION TOXICITY TREATMENT MARKET TRENDS

Rising Focus on Supportive Care During Radiotherapy Treatment Driving Market Trend

Increasing aim on better care during radiotherapy treatment curates a new market trend as cancer centers are placing greater emphasis on managing radiation-related side effects alongside the primary treatment. When patients develop complications such as oral mucositis, skin injury, or other radiation-induced toxicities, treatment comfort declines and the risk of therapy interruption increases. This creates strong demand for products that can prevent, reduce, or better control these side effects during the radiotherapy cycle. As a result, companies are investing in new supportive care products and technologies that help improve patient tolerance, maintain treatment continuity, and support better overall outcomes.

- For instance, in March 2026, Soligenix announced that SGX945 received a Promising Innovative Medicine designation from the U.K. regulator. The dusquetide showed positive efficacy results in Phase 2 and 3 studies in patients with oral mucositis due to chemoradiation therapy for head and neck cancer. This supports the market by highlighting continued pipeline progress in a major radiation-toxicity indication.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Cancer Burden and Expanding Use of Radiotherapy Driving Market Growth

The market is growing due to the number of cancer patients requiring radiation-based treatment continues to rise, and this directly increases the number of patients at risk of radiation-related side effects. As radiotherapy is used across many solid tumors, more patients experience complications such as oral mucositis, skin injury, fatigue, and other treatment-related toxicities that need supportive care. This creates steady demand for products that can prevent, reduce, or manage these side effects, helping patients continue therapy without major interruptions. As a result, the growth of cancer care and radiotherapy use is directly supporting the radiation toxicity treatment market growth.

- For instance, in April 2025, Jaguar Health, Inc. expanded its footprint beyond HIV-related supportive care to include cancer-related supportive care, and the U.S. FDA-approved oral mucositis product Gelclair.

MARKET RESTRAINTS

Limited Availability of Approved, Highly Specific Therapies Restrains Market Growth

The market faces a restraint because radiation toxicity treatment still has a limited number of highly specific and widely approved therapies, especially for complications such as severe oral mucositis and radiation dermatitis. When treatment options remain narrow, hospitals and clinicians continue to rely on supportive care protocols, symptom management, and institution-specific practices rather than standardized product adoption. This reduces commercial penetration for newer products and slows market expansion across care settings. In addition, recent reviews note that existing prevention and treatment measures still have significant limitations. That guideline development in some radiation-toxicity settings remains challenging because evidence for several interventions is insufficient, conflicting, or variable.

- For instance, in August 2023, Galera Therapeutics announced that the U.S. FDA issued a Complete Response Letter (CRL) for avasopasem manganese, its candidate for the treatment of radiotherapy-induced severe oral mucositis in patients with head and neck cancer. In that press release, Galera said the FDA found the submitted Phase 3 and supporting data were not sufficiently persuasive to establish substantial evidence of effectiveness and safety, and that an additional clinical trial would be required for resubmission. This is a negative market signal because it shows how difficult it is to bring a specialized radiation-toxicity therapy to market, which in turn limits the number of approved treatment options.

MARKET OPPORTUNITIES

Development of Targeted Therapies for Oral Mucositis and Radiation Dermatitis Creates New Market Opportunities

The market is gaining momentum as oral mucositis and radiation dermatitis remain among the most common and clinically challenging side effects of radiotherapy, while effective, highly specific treatment options remain limited in many care settings. When these complications become severe, they can increase pain, reduce quality of life, and even disrupt cancer treatment schedules. This creates a clear need for more targeted products that can prevent tissue damage, reduce symptom severity, and improve treatment continuity. As a result, companies developing focused therapies and supportive care technologies for these conditions have a strong opportunity to address unmet clinical demand and expand adoption in oncology care.

- For instance, in October 2025, MiraDx, a molecular diagnostics company focused on genetic testing to personalize cancer treatment, announced today that its PROSTOX ultra test is now available for ordering in the U.S. The test, which helps identify localized prostate cancer patients at increased risk of developing side effects from stereotactic body radiation therapy (SBRT), has already helped over 3,500 patients as part of an Early Access Program involving select academic centers and private practices.

MARKET CHALLENGES

High Variability and Reimbursement Gaps Pose a Significant Challenge in Supportive Oncology Care

The market faces a high variability and reimbursement gaps challenge because radiation toxicity treatment is often positioned as supportive care rather than the primary cancer therapy. This can make reimbursement less consistent and budget approval more difficult. When hospitals and cancer centers face financial pressure, spending is usually prioritized toward core oncology treatments, while adjunctive products for toxicity management may be adopted more slowly. This affects the uptake of newer oral mucositis, radiation dermatitis, and other supportive care solutions, even when they may improve patient comfort and treatment continuity. As a result, uneven reimbursement and cost sensitivity can slow commercialization and broader market penetration of radiation-toxicity treatment products.

- For instance, in April 2022, the Radiotherapy and Oncology Publication published an article titled ‘Innovation, value and reimbursement in radiation and complex surgical oncology: Time to rethink’ that reported high variability in reimbursement across countries in radiation and surgical oncology.

Segmentation Analysis

By Drug Class

Wide Prescription Volume of Statins to Lead the Salivary Stimulants/Cholinergic Agonists Segmental Growth

Based on the drug class, the market is categorized into cytoprotective agents, salivary stimulants/cholinergic agonists, topical corticosteroids, topical local anesthetics, gastrointestinal anti-inflammatory & mucosal protectants, analgesics, and others.

Among these, the salivary stimulants/cholinergic agonists dominated the market. The segment dominated because xerostomia and salivary gland dysfunction are common and persistent radiation-related complications, especially in head and neck cancer care, and cholinergic agents directly address the underlying symptom by stimulating salivary secretion. Dry mouth can affect eating, speaking, swallowing, and long-term quality of life, clinicians continue to use these agents in routine supportive care where symptom control is a priority. Their established mechanism, oral dosing convenience, and repeat-use potential also support greater treatment demand than narrower or more procedure-specific options.

- For instance, in October 2024, Jaguar Health, Inc. initiated the commercial launch of the U.S.FDA-approved oral mucositis prescription product Gelclair in the U.S. GELCLAIR is indicated for the management of pain and relief of pain by adhering to the mucosal surface of the mouth, soothing oral lesions of various etiologies, including oral mucositis/stomatitis caused by chemotherapy or radiation therapy.

The topical corticosteroids segment is expected to grow at a CAGR of 6.11% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

High Clinical Burden Due to Rising Oral Mucositis Led the Dominance of the Segment

Based on the disease indication, the market is segmented into oral mucositis, radiation dermatitis, xerostomia/salivary gland dysfunction, radiation proctitis, radiation esophagitis, radiation enteritis, and others.

In 2025, oral mucositis accounted for the largest radiation toxicity treatment market share. This segment dominated because oral mucositis is one of the most common, painful, and treatment-disrupting toxicities seen in patients receiving radiotherapy, particularly in head and neck cancer. When mucositis becomes severe, patients may have difficulty eating and drinking, require opioid support or hospitalization, and face interruptions in cancer treatment. Because of this high clinical burden, oral mucositis drives consistent demand for preventive and symptom-management products, making it the most commercially visible indication within radiation toxicity treatment.

- For instance, in March 2025, GenSci launched Episil in China. Through a strategic partnership, Solasia Pharma K.K. granted GenSci exclusive commercialization rights for Episil in China.

The xerostomia/salivary gland dysfunction segment is projected to grow at a CAGR of 6.67% during the forecast period.

By Age Group

Increasing Cancer Burden and Radiotherapy Treatment to Boost the Adult Segmental Growth

Based on age group, the market is bifurcated into pediatric and adult.

In 2025, the adults segment dominated the market based on age group. This segment accounted for a larger share due to the overall cancer burden, radiotherapy treatment volume, and supportive care demand are much higher in adults. Adult patients account for most head and neck, lung, gastrointestinal, pelvic, and other solid tumors, where radiation-related toxicities commonly occur. Hence, the treated population requiring management of mucositis, xerostomia, dermatitis, or GI toxicity is naturally larger. As a result, product use, prescribing frequency, and healthcare spending are more concentrated among adults.

- For instance, in September 2025, Partner Therapeutics, Inc. received marketing authorization from the European Commission for IMREPLYS (sargramostim, rhu GM-CSF) for the treatment of patients acutely exposed to myelosuppressive doses of radiation with Hematopoietic Sub-syndrome of Acute Radiation Syndrome (H-ARS).

The pediatric segment is projected to grow at a CAGR of 3.87% during the forecast period.

By Type

Rising Demand for Low-Cost Therapies to Boost Generics Segmental Growth

Based on type, the market is divided into branded and generics.

In 2025, the generics product type dominated the market. The segment dominated because many products used in radiation toxicity management belong to mature supportive-care categories such as analgesics, local anesthetics, corticosteroids, GI anti-inflammatory agents, and salivary stimulants, where generic prescribing is common. Since these therapies are often used for symptom control throughout treatment, hospitals and prescribers tend to prefer lower-cost generic options when clinical outcomes are comparable. This cost-driven prescribing pattern supports broader uptake of generics across routine supportive oncology care.

- For instance, in March 2026, Zydus Lifesciences Limited received approval from the U.S. FDA for Cevimeline Hydrochloride Capsules 30 mg, indicated for the symptomatic treatment of dry mouth (xerostomia) associated with Sjögren’s syndrome. This development improved the availability of lower-cost salivary stimulant options and is the closest validated generic-type development relevant to xerostomia management.

The branded segment is projected to grow at a CAGR of 4.38% during the forecast period.

By Route of Administration

Convenience Offered by Oral Route of Administration in Supportive Cancer Care to Boost Segmental Growth

Based on the route of administration, the market is segmented into oral, topical, parenteral, rectal, and others.

In 2025, the oral drugs dominated the market by route of administration. Many leading radiation-toxicity treatments are designed for easy oral use, including mouth rinses, oral gels, lozenges, capsules, and tablets used for mucositis, xerostomia, pain relief, and GI symptom management. Oral administration is preferred in supportive care as it is convenient, non-invasive, suitable for repeated daily use, and easier to continue in outpatient settings during radiotherapy. Underscoring these advantages, many key companies are focusing on new product development in oral formats.

- For instance, in April 2025, OncoZenge AB partnered with Avernus Pharma to commercialize and distribute BupiZenge oral lozenges in the GCC region. The development strengthened the oral segment by demonstrating expanding regional commercialization of an easy-to-administer oral product for the treatment of oral mucositis pain in cancer patients.

The others segment is projected to grow at a CAGR of 6.68% during the forecast period.

By Distribution Channel

Integrated Cancer Care of Hospitals and Supportive Care to Lead the Hospital Pharmacies Segment

Based on the distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

By distribution channel, the hospital pharmacies dominated the market for radiation toxicity treatment. The high share was allocated to these hospital pharmacies as most radiation toxicity treatments are initiated, prescribed, or recommended within oncology treatment pathways that are closely linked to hospitals and cancer centers. Patients receiving radiotherapy are commonly monitored in institutional settings, and supportive-care products are often selected as part of integrated cancer care. Since these products are tied to treatment cycles, adverse-event management, and specialist supervision, hospital pharmacies typically remain the main access point.

- For instance, in September 2025, OncoZenge collaborated with UCLA for a patient engagement study on BupiZenge for oral mucositis pain. The partnership focused on a patient engagement study to gather insights on the unmet needs in managing oral mucositis pain. This development supported the hospital pharmacy segment because adoption, evaluation, and prescribing of such products are closely tied to cancer centers and hospital-based oncology care.

The online pharmacies segment is projected to grow at a CAGR of 9.34% over the forecast period.

Radiation Toxicity Treatment Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Radiation Toxicity Treatment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.47 billion and maintained its leading position in 2025 at USD 0.50 billion. The market growth is due to the region having a high volume of cancer treatment, widespread use of radiotherapy, and strong adoption of supportive care in oncology practice. As more patients receive radiation and clinicians focus on preventing treatment interruptions, demand for treatments for mucositis, xerostomia, dermatitis, and GI toxicity continues to rise.

U.S. Radiation Toxicity Treatment Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.50 billion in 2026, accounting for roughly 36.03% of the global revenue.

Europe

Europe is projected to grow at 4.89% over the coming years, the second-highest among all regions, and expected to reach a valuation of USD 8.73 billion by 2026. Europe has a large and well-documented cancer burden, along with broad radiotherapy use and increasing attention to survivorship and toxicity management. This supports steady demand for products that help manage side effects and keep patients on treatment, driving global market growth.

U.K. Radiation Toxicity Treatment Market

The U.K. market is estimated at around USD 0.07 billion in 2026, representing roughly 4.84% of the global market.

Germany Radiation Toxicity Treatment Market

Germany's market is projected to reach approximately USD 0.07 billion in 2026, equivalent to around 5.43% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 0.33 billion in 2026 and secure the position of the third-largest region in the market. The region accounts for a major share of the global cancer burden and continues to expand cancer care capacity. As access to radiotherapy and oncology infrastructure improves across many Asia Pacific countries, the need for radiation-toxicity management products also rises, propelling market growth.

Japan Radiation Toxicity Treatment Market

The Japanese market in 2026 is estimated at around USD 0.06 billion, accounting for approximately 4.53% of the global market.

China Radiation Toxicity Treatment Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.11 billion, representing approximately 8.22% of global sales.

India Radiation Toxicity Treatment Market

The Indian market in 2026 is estimated at around USD 0.05 billion, accounting for roughly 3.90% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The market in Latin America is estimated to reach a valuation of USD 0.08 billion in 2026. The market is growing as cancer cases rise, while regional healthcare systems are working to expand radiotherapy and cancer care access. In the Middle East & Africa, the GCC market is set to reach USD 0.02 billion in 2026.

South Africa Radiation Toxicity Treatment Market

The South African market is projected to reach approximately USD 0.70 billion in 2026, accounting for roughly 0.70% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Launches and Strategic Partnerships Among Key Players to Propel Market Position

The global radiation toxicity treatment market is highly consolidated, with companies such as Stratpharma AG, Flen Health, KeraNetics, Inc, Solventum, Soligenix, Inc., RedHill Biopharma Ltd, and Galera Therapeutics, Inc. holding significant market share. Strategic partnerships, new product launches, and regulatory approvals in the sector drive these companies' market share.

- For instance, in March 2024, ReAlta Life Sciences collaborated with the US National Institute of Allergy and Infectious Diseases (NIAID) to develop and evaluate its acute radiation syndrome (ARS) drug RLS-0071 (PIC1-01) for radiation poisoning.

Other notable players in the global market include Monopar Therapeutics Inc., Soleva Pharma LLC, Recordati, and Partner Therapeutics, Inc. These companies are expected to prioritize strategic collaborations and new product launches to strengthen their positions during the forecast period.

LIST OF KEY RADIATION TOXICITY TREATMENT COMPANIES PROFILED

- Stratpharma AG (Switzerland)

- Flen Health (U.S.)

- KeraNetics, Inc. (U.S.)

- Solventum (U.S.)

- Soligenix, Inc. (U.S.)

- Galera Therapeutics, Inc. (U.S.)

- Monopar Therapeutics Inc. (U.S.)

- Soleva Pharma LLC (U.S.)

- Recordati (Italy)

- Partner Therapeutics, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Hoth Therapeutics, Inc expanded its intellectual property portfolio for HT-001, its lead topical therapeutic candidate. The Company filed multiple U.S. Provisional Patent Applications covering novel dermatological indications, broadening the commercial and clinical potential of HT-001, which targets drug-induced hypersensitivity, radiotherapy-induced rash, and menin inhibitor-associated skin toxicities.

- June 2025: Plus Therapeutics, Inc. received Investigational New Drug (IND) approval from the U.S. FDA for its application for REYOBIQTM (Rhenium Re186 Obisbemeda) for the treatment of pediatric patients with supratentorial recurrent, refractory, or progressive high-grade glioma (HGG) and ependymoma.

- April 2025: OncoZenge AB entered an exclusive licensing agreement with Avernus Pharma for the commercialization and distribution of BupiZenge oral lozenges in the GCC region.

- March 2025: RiboX Therapeutics Ltd. announced that the first patient was dosed last week in its first-in-human (FIH) Phase I/IIa clinical trial (SPRINX-1) evaluating the safety and efficacy of RXRG001 in patients with radiation-induced xerostomia (RIX) and hyposalivation.

- February 2023: RedHill Biopharma Ltd. announced that the Radiation and Nuclear Countermeasures Program (RNCP) of the National Institute of Allergy and Infectious Diseases, part of the National Institutes of Health, has selected opaganib for the nuclear medical countermeasures product development pipeline as a potential treatment for Acute Radiation Syndrome (ARS).

REPORT COVERAGE

The report provides a detailed global radiation toxicity treatment market analysis across key segments such as drug type, disease indication, age group, type, route of administration, and distribution channel. It examines the commercial landscape for products used to manage radiation-induced complications, including oral mucositis, radiation dermatitis, xerostomia, radiation proctitis, radiation esophagitis, and radiation enteritis, while also assessing treatment trends across branded and generic product categories. The study further covers regional market insights for North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, highlighting the factors driving market growth in each region. It also includes an evaluation of market drivers, restraints, opportunities, and challenges, along with an analysis of recent product developments, collaborations, regulatory updates, and company activities shaping market competition. In addition, the report provides a profiling of key companies operating in the space, with a focus on their product offerings, strategic developments, and market presence.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.86% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Age Group, Type, Route of Administration, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.30 billion in 2025 and is projected to reach USD 2.17 billion by 2034.

In 2025, the North American market value stood at USD 0.50 billion.

The market is expected to grow at a CAGR of 5.86% over the forecast period.

The salivary stimulants/cholinergic agonists drug segment dominated the market.

The market is driven by the rising global cancer burden and expanding use of radiotherapy, driving treatment demand and market growth

Stratpharma AG, Flen Health, KeraNetics, Inc, Solventum, and Sanofi are the major industry players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us