Radioimmunoassay Market Size, Share & Industry Analysis, By Product Type (Kits and Reagents and Instruments), By Application (Endocrinology, Oncology, Cardiology, Infectious Diseases, Allergy and Autoimmune Disorders, and Others), By End-user (Standalone Clinical Diagnostics Laboratories, Hospital Laboratories, Pharmaceutical and Biotechnology Companies, and Others), and Regional Forecast, 2026-2034

Radioimmunoassay Market Size & Share Analysis

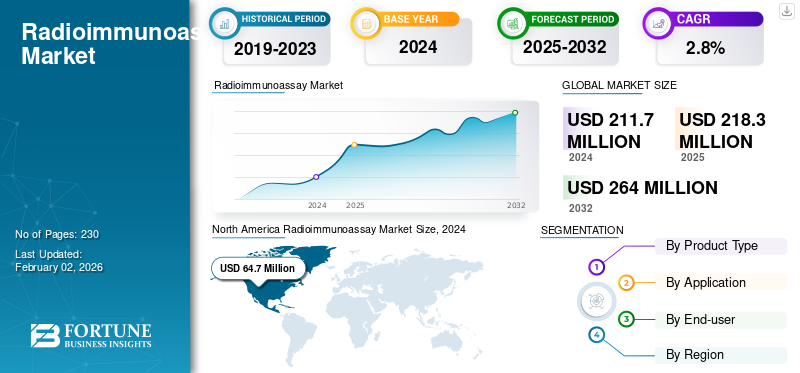

The global radioimmunoassay market size was valued at USD 218.35 million in 2025 and is expected to grow from USD 225.00 million in 2026 to USD 276.54 million by 2034, exhibiting a CAGR of 2.61% during the forecast period. North America dominated the radioimmunoassay market, accounting for 30.37% of the market share in 2025. Industry growth is driven by expanding diagnostic demand, chronic disease burden, precision immunoassay adoption, and increasing laboratory automation investments worldwide.

Radioimmunoassay (RIA) is a highly sensitive laboratory technique used to measure minute concentrations of biological substances, such as hormones, drugs, vitamins, or antigens, in samples such as blood, serum, plasma, or urine. It’s based on the principle of antigen–antibody binding and the use of a radioactively labeled substance to quantify the concentration of the analyte.

From Revvity, Inc. and DIAsource to MP Biomedicals, Danaher Corporation, and DiaSorin, key industry players are sharpening their focus on R&D activities, rolling out advanced technologies and novel platforms. Their efforts are setting the stage for strong global market growth.

As tech innovation accelerates and personalized medicine takes center stage, the market's future looks promising. Challenges do exist, tough regulations and strong competition among them, but the steady flow of new ideas and collaborative strategies keeps the industry moving toward a more streamlined and widely accessible healthcare environment.

Growth dynamics are shaped by the rising prevalence of chronic and hormonal disorders. Increased diagnostic testing volumes for thyroid dysfunction, fertility assessment, and oncology markers sustain consistent assay demand. While alternative platforms such as enzyme-linked immunosorbent assays and chemiluminescent immunoassays have expanded, radioimmunoassay retains niche clinical value where analytical sensitivity is critical.

Kits and reagents represent the dominant revenue contributor within the radioimmunoassay market. Recurring reagent consumption supports predictable revenue streams across laboratories. Instruments contribute comparatively lower revenue but remain essential for assay processing and detection standardization. From a market structure perspective, the radioimmunoassay market share is moderately consolidated. Established diagnostics manufacturers maintain strong distribution networks and regulatory compliance capabilities. Emerging suppliers focus on cost-efficient reagent production in developing regions.

Regional demand is concentrated in North America and Europe, where established diagnostic infrastructure and research activity support stable testing volumes. Asia-Pacific demonstrates gradual radioimmunoassay market growth driven by healthcare infrastructure expansion and increased laboratory capacity.

Download Free sample to learn more about this report.

RADIOIMMUNOASSAY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 218.35 Million

- 2026 Market Size: USD 225.00 Million

- 2034 Forecast Market Size: USD 276.54 Million

- CAGR: 2.61% from 2026–2034

- North America dominated the radioimmunoassay market with a 30.37% share in 2025.

- Kits and reagents are expected to account for 87.23% of the market in 2026.

- Endocrinology is projected to hold a 44.23% market share in 2026.

North America

North America generated USD 66.30 million in 2025 and projected to reach USD 67.83 million in 2026.

Europe

Europe generated USD 60.06 million in 2025 and expected to reach USD 61.73 million in 2026.

Asia Pacific

Asia Pacific reached USD 57.94 million in 2025 and projected to reach USD 60.13 million in 2026.

U.S.

Radioimmunoassay market projected to reach USD 61.35 million by 2026.

Japan

Radioimmunoassay market projected to reach USD 12.69 million by 2026.

Read More

Market Dynamics

Market Drivers

Rise In Endocrine and Oncological Disorders to Support Market Growth

The growing prevalence of endocrine and cancer-related disorders continues to drive demand for radioimmunoassay, a trusted technique known for its remarkable sensitivity and accuracy. Hormone tests for analytes such as insulin, cortisol, and thyroid hormones (T3, T4, and TSH) still rely heavily on this method, especially in specialized and reference laboratories. At the same time, the expansion of biologics research and bioanalytical testing has further strengthened the role of radioimmunoassay in receptor-binding and tracer studies.

Rapid improvements in diagnostic infrastructure across countries such as China, India, and Brazil have also fueled reagent demand. In many of these settings, radioimmunoassay remains a practical and cost-effective option, particularly where advanced chemiluminescent systems are not yet widely available. Its ability to detect analytes at extremely low concentrations down to the picogram level makes it particularly valuable for niche research applications focused on low-abundance biomarkers. Despite the industry’s gradual move toward automated platforms such as CLIA and ELISA, the precision, reliability, and affordability of radioimmunoassay reagents are likely to sustain their market presence well into 2032.

The rising prevalence of endocrine disorders remains a primary driver of the radioimmunoassay market growth. Thyroid disease, reproductive hormone imbalances, and adrenal disorders require high-sensitivity detection of circulating biomarkers. Radioimmunoassay continues to deliver reliable quantification at very low analyte concentrations. Oncology diagnostics also contribute to sustained demand. Certain tumor markers are historically validated through radioimmunoassay protocols, supporting continued laboratory utilization. Pharmaceutical and biotechnology companies employ radioimmunoassay during drug development and pharmacokinetic studies due to assay precision.

Established clinical validation provides long-term credibility. Many laboratories maintain radioimmunoassay workflows because of decades of reference data. This legacy adoption reinforces market stability despite technological alternatives. Growth in reference laboratory networks supports increased testing volumes. Centralized diagnostic centers often retain radioimmunoassay capability for specialized cases. Laboratory automation systems have improved throughput and safety in radioactive handling.

Market Restraints

Stringent Radiation Regulation & Technological Shift to Restrict Market Growth

Stringent regulations on handling radioactive materials, managing waste, and maintaining licensed laboratories have slowed the growth of radioimmunoassay in developed markets. Agencies such as the U.S. Nuclear Regulatory Commission (NRC) and the European Atomic Energy Community (EURATOM) enforce extensive compliance standards, which significantly increase the operational burden on diagnostic facilities. The need for specialized storage, trained staff, and careful management of short-lived isotopes often discourages the establishment of new RIA setups.

At the same time, the industry’s gradual shift toward non-radioactive techniques, such as chemiluminescent (CLIA) and enzyme-linked immunoassays (ELISA), has accelerated the replacement of RIA in routine diagnostics. Major companies, including Siemens Healthineers, Abbott, and Roche Diagnostics, have already shifted to automated CLIA platforms that offer safer operations and higher efficiency. These transitions, combined with strict regulatory barriers, are expected to limit the radioimmunoassay market growth in the coming years.

Regulatory and safety requirements represent significant constraints within the radioimmunoassay market. Handling radioactive isotopes requires strict compliance with radiation safety standards. Licensing procedures increase operational complexity and cost. Alternative immunoassay technologies present competitive pressure. Chemiluminescent and enzyme-based assays eliminate radioactive materials while offering comparable sensitivity in many applications. Laboratories seeking simplified compliance increasingly evaluate non-radioactive platforms.

Waste disposal regulations add operational burden. Radioactive waste management involves documentation, storage protocols, and environmental oversight. These requirements increase per-test cost and administrative effort. Supply chain dependence on radioisotope production introduces vulnerability. Shortages or transportation restrictions can disrupt reagent availability. Isotope half-life limitations also create logistical constraints.

Market Opportunities

Rise in Research and Development Spending and Academic Research Funding to Open New Market Growth Avenues

Emerging economies and the global expansion of biopharmaceutical research are opening new growth avenues for the market. Rising pharmaceutical R&D investments have expanded the application of RIA in pharmacokinetic and ligand-binding studies, where precise and highly sensitive analysis is crucial.

- According to several credible sources, global pharmaceutical R&D spending was nearly USD 288 billion in 2024, a 1.5% increase from 2023.

Companies such as DIAsource and the Institute of Isotopes are capitalizing on this demand by introducing multianalyte RIA panels and low-volume kits designed for contract research organizations and academic laboratories. In countries such as India and China, growing research funding and relatively lenient isotope-use regulations are driving new orders for gamma counters and radiolabeled reagents.

There is also renewed interest in applying RIA to veterinary endocrinology and toxicology testing, where affordability and reproducibility are valued more than automation. Meanwhile, the relocation of reagent manufacturing to Eastern Europe and Asia has helped lower isotope supply costs and shorten delivery times. Although radioimmunoassay is a well-established technology, regional manufacturing and research-driven applications are expected to continue creating promising niche opportunities for market players in the coming years.

Expansion of specialized endocrine testing offers a measurable opportunity within the radioimmunoassay market. Complex hormonal conditions often require precise quantification beyond the sensitivity of some alternative assays. Laboratories emphasizing diagnostic differentiation may retain or expand radioimmunoassay capability.

Pharmaceutical development pipelines also present an opportunity. Drug metabolism and hormone interaction studies frequently require validated radioimmunoassay methodologies. Contract research organizations represent a stable end-user segment. Emerging healthcare systems provide incremental expansion potential. As diagnostic standards improve, tertiary laboratories may adopt radioimmunoassay for specialized testing. Partnerships with local distributors can facilitate entry.

Technological improvements in isotope labeling and detection sensitivity may extend assay lifespan. Enhanced automation reduces safety concerns and increases throughput. Regulatory harmonization across regions could simplify compliance procedures, lowering entry barriers. Manufacturers investing in user-friendly kits and standardized workflows may gain a competitive advantage.

Market Challenges

Niche Demand and Several Structural Challenges Hinder Radioimmunoassay Scalability

Although radioimmunoassay continues to serve a niche segment, several structural barriers limit its broader growth potential. A key issue lies in the fragile supply chain for isotopes such as I-125 and Co-57, where even minor disruptions can halt reagent production and distribution. For instance, the Iodine-125 shortage in Europe in 2022 led to visible delays in kit availability. Compounding this challenge is the shrinking pool of skilled professionals trained in traditional RIA procedures, as most laboratory staff now specialize in chemiluminescent or molecular platforms.

In advanced markets, reimbursement inconsistencies also weigh on adoption. Many insurers prioritize non-radioactive testing alternatives, making RIA financially less attractive. After the COVID-19 pandemic, numerous hospitals permanently decommissioned RIA facilities due to high waste disposal costs and lower testing volumes.

In developing regions, the demand for RIA reagents is growing; however, the lack of nuclear waste management infrastructure and dependence on imported isotopes create significant operational risks. Frequent licensing renewals, regulatory inspections, and sourcing challenges further add to the cost burden. While RIA continues to play a vital role in certain research and diagnostic areas, its long-term viability depends on resolving these workforce, infrastructure, and compliance challenges.

Radioimmunoassay Market Trends

Decentralization & Innovative Technology Adaptation is Transforming RIA Platforms

In recent years, radioimmunoassay systems have undergone steady modernization through miniaturization and digital upgrades. Leading manufacturers such as Revvity, Beckman Coulter, and Izotop are introducing automated gamma counters equipped with software for precise dose calibration and advanced quality control, helping to update and extend the life of older laboratory setups.

A notable trend shaping the market is the regional localization of manufacturing, particularly in the Asia Pacific and Eastern Europe regions. This shift helps reduce the high costs associated with importing and transporting isotopes. For example, the Beijing North Institute of Biological Technology (BNIBT) expanded its domestic RIA kit production in 2023 to meet the growing demand for endocrinology testing within China.

Another development involves hybrid testing workflows that pair RIA with ELISA or CLIA confirmation steps to improve result accuracy in complex research applications. At the same time, the use of radiation-safe consumables and disposable shielding materials is addressing stricter safety and regulatory expectations.

Digitalization is also transforming the field, with many laboratories adopting cloud-based systems for storing RIA data and automating dose normalization. These advances are enhancing reproducibility and data integrity. Together, such innovations are shifting radioimmunoassay from a traditional manual procedure into a semi-automated, digitally enabled tool tailored for modern research environments.

Automation integration represents a notable trend within the radioimmunoassay industry. Laboratories increasingly adopt automated pipetting and detection systems to enhance reproducibility and reduce manual exposure risks. This trend improves workflow efficiency and supports quality assurance compliance. Niche clinical specialization is also shaping radioimmunoassay market trends. Rather than broad diagnostic use, radioimmunoassay is increasingly positioned for highly sensitive endocrine and research applications. Laboratories optimize portfolios by maintaining selective assay capabilities.

Emerging economies are investing in advanced diagnostic infrastructure. Although growth remains gradual, the increasing tertiary care hospitals in Asia-Pacific and Latin America is expanding testing capacity. Research applications continue to support relevance. Academic institutions and biotechnology firms use radioimmunoassay for experimental hormone and biomarker studies requiring high analytical sensitivity. Digital laboratory management systems are improving traceability and documentation. Integration with laboratory information systems enhances regulatory compliance and quality control processes.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Kits and Reagents Led Market Due to Frequent Test Volume in Healthcare Settings

Based on product type, the market is divided into kits, reagents, and instruments.

Kits and Reagents

The kits and reagents segment dominated the market with a share of 87.23% in 2026, owing to emerging regions' dependence on consumables due to slower instrument replacement. Additionally, kits and reagents are dominant due to the high frequency of testing in healthcare settings. Kits and reagents account for the largest share of the radioimmunoassay market size. These consumables generate recurring revenue streams, as laboratories require continuous replenishment for routine testing.

Demand is closely tied to testing volumes in endocrinology, oncology, and research applications. Reagent sensitivity and stability remain key differentiators. Laboratories prioritize assay reproducibility, isotope integrity, and shelf-life optimization. Vendors focusing on standardized calibration controls and validated reference ranges strengthen customer retention.

Growth in this segment reflects consistent clinical demand rather than rapid expansion. While the overall radioimmunoassay market growth rate is moderate, recurring reagent consumption ensures stable revenue generation. Regional expansion in tertiary hospitals and reference laboratories contributes incremental demand. Competitive pressure centers on pricing and regulatory compliance. Manufacturers must maintain strict quality control for radioactive labeling processes. Supply chain reliability remains essential due to isotope half-life limitations.

Instruments

The instrument segment is expected to grow at a CAGR of 2.1% over the forecast period. Instruments represent a smaller portion of the total radioimmunoassay market size but play a critical enabling role. These systems support sample preparation, detection, and radiation measurement. Investment cycles for instruments are longer compared to consumables. Laboratories typically procure instruments as part of integrated diagnostic workflows. Automation enhancements reduce manual handling and improve throughput consistency. Modern systems incorporate shielding and safety features that align with regulatory requirements.

Instrument demand is influenced by laboratory modernization initiatives. Replacement cycles occur as facilities upgrade to improve efficiency or comply with updated radiation safety standards. Emerging markets' expanding diagnostic capacity may generate additional instrument sales. Although instruments contribute less recurring revenue than kits, their installation base influences long-term consumable purchasing behavior. Vendors with established instrument platforms often secure ongoing reagent contracts.

To know how our report can help streamline your business, Speak to Analyst

By Application

Endocrinology Dominated Market Due to Rising Prevalence of Endocrine Disorders

Based on application, the market is segmented into endocrinology, oncology, cardiology, infectious diseases, allergy and autoimmune disorders, and others.

Endocrinology

The endocrinology segment dominated the market in 2026, driven by the growing prevalence of endocrine disorders among the global and U.S. patient population. Diabetes is the most prevalent endocrine disorder worldwide and in the U.S., followed by thyroid disorders and metabolic syndrome. Additionally, in 2026, the segment is expected to account for a 44.23% share of the market.

- For instance, according to the 2024 statistics published by the International Diabetes Federation (IDF), globally, an estimated 589 million adults have diabetes, with that number projected to reach USD 853 million by 2050.

Endocrinology remains the dominant application within the radioimmunoassay market. Hormonal assays for thyroid-stimulating hormone, cortisol, insulin, and reproductive hormones rely on high analytical sensitivity. Historical clinical validation reinforces continued use. Testing volumes are driven by the rising prevalence of metabolic and reproductive disorders. Reference laboratories frequently retain radioimmunoassay capability for low-concentration analytes. This application significantly influences the radioimmunoassay market share concentration.

Oncology

Oncology applications support steady radioimmunoassay market growth, particularly in tumor marker quantification. Certain markers maintain established radioimmunoassay protocols due to validated sensitivity profiles. Pharmaceutical research also employs oncology-related assays for drug monitoring and biomarker studies. While alternative platforms exist, radioimmunoassay retains relevance in specialized laboratories requiring precision measurement.

Cardiology

Cardiology represents a smaller but stable segment. Select cardiac biomarkers historically utilize radioimmunoassay methodologies. However, automated chemiluminescent platforms increasingly dominate routine cardiology diagnostics. Radioimmunoassay demand in this segment is concentrated in research and reference settings rather than high-volume hospital testing. Growth remains limited but stable.

Infectious Diseases

Infectious disease testing contributes a modest impact on the radioimmunoassay market size. Most routine diagnostics have transitioned to non-radioactive immunoassays. Nevertheless, certain research-based viral and antigen studies continue to employ radioimmunoassay. Laboratory preference in this segment depends on sensitivity requirements and the regulatory environment.

Allergy and Autoimmune Disorders

Allergy and autoimmune testing maintain selective radioimmunoassay usage, particularly for specific immunoglobulin detection. Clinical validation and assay sensitivity support niche demand. Adoption patterns vary regionally. In advanced markets, alternative technologies dominate. In developing regions, existing infrastructure supports continued radioimmunoassay use. The allergy and autoimmune disorders segment is set to flourish with a growth rate of 3.3% over the forecast period.

By End-user

Higher Test Volume Boosted Adoption of Radioimmunoassay at Standalone Clinical Diagnostics Laboratories

Based on end-user, the market is segmented into standalone clinical diagnostics laboratories, hospital laboratories, pharmaceutical and biotechnology companies, and others.

Standalone Clinical Diagnostics Laboratories

The standalone clinical diagnostics laboratories segment dominated the market in 2025, driven by the increasing number of these laboratories, which in turn supports the growing number of diagnostic procedures among patients. Additionally, the outsourcing of clinical diagnostic services by public hospitals to standalone clinical laboratories is a significant factor contributing to the high volume of tests performed in these settings. Furthermore, the segment is set to hold a 34.61% share in 2026.

Standalone clinical laboratories represent a substantial share of the radioimmunoassay market. These facilities often handle specialized testing referred from smaller hospitals. Centralized infrastructure supports regulatory compliance and radiation safety management. High testing volumes in endocrinology sustain recurring reagent demand. Laboratories prioritize assay precision and standardized protocols to maintain accreditation. This segment significantly influences overall radioimmunoassay market share stability.

- For instance, according to data published by the American Clinical Laboratory Association in 2023, there are approximately 322,488 clinical laboratories in the U.S.

Hospital Laboratories

Hospital laboratories contribute to moderate demand. Larger tertiary hospitals may maintain radioimmunoassay capability for specialized endocrine testing. However, many hospitals have transitioned routine diagnostics to non-radioactive systems. Adoption depends on institutional resources and regulatory capacity. Growth in hospital-based testing remains limited compared to centralized reference laboratories.

Pharmaceutical and Biotechnology Companies

Pharmaceutical and biotechnology firms represent an important but specialized end-user segment. Drug development studies often require sensitive hormone and biomarker quantification. Radioimmunoassay provides validated methodologies for pharmacokinetic evaluation. In addition, the pharmaceutical and biotechnology companies segment is projected to grow at a CAGR of 3.2% during the study period.

Regional Insights

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Radioimmunoassay Market Analysis

North America Radioimmunoassay Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 66.3 Million, accounting for 30.37% of the worldwide market, and is projected to grow to USD 67.83 Million in 2026. Some of the prominent factors contributing to the region’s dominance include the presence of major companies, such as Revvity, Inc., MP Biomedicals, and Danaher Corporation, especially in the U.S. Favorable government regulations, a well-established diagnostic infrastructure, and the adoption of technologically advanced diagnostic techniques are fueling market expansion in the region.

North America leads the radioimmunoassay market due to established diagnostic infrastructure and strong regulatory compliance frameworks. High prevalence of endocrine disorders supports sustained testing volumes. Reference laboratories maintain specialized assay capability despite alternative technologies. Pharmaceutical research activity further contributes to the radioimmunoassay market size stability. While growth remains moderate, consistent demand preserves the regional radioimmunoassay market share.

United States Radioimmunoassay Market:

The United States represents the largest contributor within the regional radioimmunoassay market. Advanced laboratory networks and robust pharmaceutical research pipelines sustain assay utilization. Regulatory oversight ensures standardized radiation handling protocols. Although chemiluminescent platforms dominate routine testing, specialized endocrine diagnostics preserve radioimmunoassay market growth in reference laboratories and research institutions.

The U.S. market is estimated to reach USD 61.35 billion by 2026. The increasing prevalence of chronic and infectious diseases in the U.S. is one of the factors driving the market growth. This, along with the growing presence of a well-established healthcare infrastructure, a favorable reimbursement scenario for radioimmunoassay diagnostic tests, and higher awareness among the patient population about primary diagnosis, is leading to the higher adoption of advanced instruments and tests by healthcare settings in the country.

Europe Radioimmunoassay Market Analysis

The Europe market generated USD 60.06 Million in 2025, representing 27.51% of the global market landscape, and is expected to reach USD 61.73 Million in 2026. The growth is attributed to several factors, including well-established healthcare infrastructures, increased healthcare expenditure, and a rising prevalence of chronic endocrine disorders, cancer, and other diseases.

Europe maintains steady radioimmunoassay market growth driven by mature healthcare systems and academic research institutions. Endocrinology testing remains the principal application. Strict regulatory compliance shapes operational practices. Market share is concentrated among established diagnostics providers with strong distribution networks. Expansion remains gradual, reflecting balanced adoption alongside non-radioactive immunoassay alternatives.

Germany Radioimmunoassay Market:

Germany plays a key role in the European radioimmunoassay market. Advanced clinical laboratories and pharmaceutical research centers support continued assay usage. Compliance with radiation safety standards remains stringent. Demand is concentrated in endocrine and oncology applications. While alternative technologies gain traction, validated radioimmunoassay protocols maintain selective clinical relevance, and the Germany market is estimated to reach USD 13.16 billion by 2026.

United Kingdom Radioimmunoassay Market:

The UK market is estimated to reach USD 8.80 billion by 2026. The United Kingdom exhibits a stable radioimmunoassay market size supported by centralized diagnostic networks. Public healthcare laboratories retain selective assay capability for specialized hormone testing. Academic research institutions further contribute to market demand. Growth remains limited but consistent, reflecting niche clinical adoption rather than broad diagnostic expansion.

Asia-Pacific Radioimmunoassay Market Analysis

Asia Pacific contributed 26.53% to the global market in 2025, with a valuation of USD 57.94 Million, and is projected to reach USD 60.13 Million in 2026.

The Japan market is estimated to reach USD 12.69 billion by 2026, the China market is estimated to reach USD 15.35 billion by 2026, and the India market is estimated to reach USD 11.75 billion by 2026. Asia-Pacific demonstrates moderate radioimmunoassay market growth supported by expanding tertiary healthcare infrastructure. Increasing awareness of endocrine disorders drives testing demand.

Regulatory environments vary across countries, influencing adoption patterns. Market share is fragmented, with local distributors supporting reagent supply. Long-term growth potential exists in emerging economies and in improving laboratory capacity.

Japan Radioimmunoassay Market:

Japan’s radioimmunoassay market benefits from advanced diagnostic standards and strong endocrine testing demand. Laboratories emphasize precision and compliance with radiation safety guidelines. Pharmaceutical research activity supports assay utilization. Growth remains stable, supported by specialized clinical needs rather than widespread diagnostic replacement cycles.

China Radioimmunoassay Market:

China shows gradual radioimmunoassay market growth as healthcare infrastructure expands. Tertiary hospitals and research institutions maintain selective assay use. Regulatory oversight continues to evolve, influencing operational practices. Market share includes domestic suppliers providing cost-efficient reagents. Expansion remains measured due to the increasing adoption of alternative immunoassay technologies.

Latin America Radioimmunoassay Market Analysis

The market in Latin America reached USD 14.5 Million in 2025, representing 6.64% of total market revenue, and is projected to reach USD 15. Million in 2026. The growing geriatric population, along with the increasing prevalence of several disorders, further drives usage in these regions. Latin America demonstrates a limited but stable radioimmunoassay market size driven by specialized reference laboratories. Infrastructure disparities influence regional demand distribution. Endocrine testing remains the primary application. Regulatory processes vary, impacting radioactive material handling. Growth potential depends on laboratory modernization and healthcare investment levels.

Middle East & Africa Radioimmunoassay Market Analysis

The Middle East & Africa market was valued at USD 19.55 Million in 2025, capturing 6.64% of global revenue, and is estimated to reach USD 20.31 Million in 2026. The Middle East and Africa region reflects modest radioimmunoassay market growth supported by select tertiary hospitals and research centers. Limited infrastructure and regulatory complexity constrain broader adoption. Demand is concentrated in specialized endocrine diagnostics. Market expansion depends on healthcare investment and laboratory capability improvements.

Radioimmunoassay Industry Competitive Landscape:

Key Industry Players

Top Participants Emphasize R&D Efforts to Maintain Their Dominance

The global market is semi-consolidated. A few prominent players, such as Revvity, Inc., DIAsource, MP Biomedicals, Institute of Isotopes, and DiaSorin S.p.A., hold a majority share of the global market. The increasing focus of companies on R&D activities to develop and introduce technologically advanced products and novel systems is a significant factor contributing to the growing share of these companies.

Other market players include Danaher Corporation, Biosigma S.p.A., Tecan Group Ltd., and several small-scale companies. These players are concentrating on launching new products, expanding their geographic presence, and establishing a strong brand presence, further supporting the global radioimmunoassay market share.

The radioimmunoassay industry is moderately consolidated, characterized by established diagnostic manufacturers with longstanding technical expertise in radioactive labeling and assay development. Competitive positioning depends on reagent quality, regulatory compliance, distribution strength, and laboratory relationships rather than rapid technological disruption. Innovation within the radioimmunoassay market is incremental rather than disruptive. Companies invest in automation compatibility, improved isotope stability, and enhanced detection sensitivity. These enhancements strengthen operational efficiency without fundamentally altering assay methodology.

The market is concentrated among suppliers with integrated product portfolios combining kits, reagents, and compatible instrumentation. Vendors emphasize validated assay protocols and standardized calibration systems to support laboratory accreditation requirements. Recurring reagent sales form the primary revenue base, reinforcing customer retention.

Competition increasingly centers on cost efficiency and supply chain reliability. Radioisotope procurement and transportation logistics require robust coordination. Manufacturers capable of ensuring stable isotope availability gain a strategic advantage. Quality assurance remains critical, as assay reproducibility directly impacts clinical credibility.

LIST OF KEY RADIOIMMUNOASSAY COMPANIES PROFILED

- Revvity, Inc. (U.S.)

- DIAsource (Belgium)

- MP Biomedicals (U.S.)

- Danaher Corporation (U.S.)

- DiaSorin S.p.A. (Italy)

- Shenzhen New Industry Biomedical Engineering Co., Ltd. (China)

- Institute of Isotopes (Hungary)

- Biosigma S.p.A. (Italy)

- Tecan Group Ltd. (Switzerland)

- Beijing Chemclin Biotech Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- October 2025: ARCHIMED Diagnostics acquired ARK Diagnostics, a global leader in disease and drug monitoring & detection.

- September 2025: BioVendor Group, a leading European innovator in immunodiagnostics and molecular diagnostics, announced a strategic transformation of its organizational structure and a unified presentation under the BioVendor Group brand. It is structured into three global strategic divisions: Immunodiagnostics, Molecular Diagnostics, and Radio-immunodiagnostics.

- January 2025: Medipan GmbH announced an extension of the shelf life for its radioimmunoassay (RIA) kits, specifically the SELco TSH Rapid, SELco Tg 1-Step, and SELco Calcitonin kits.

- February 2025: Euro Diagnostica: Expanded distribution partnerships across Asia-Pacific: to increase regional radioimmunoassay market size presence: implementing localized regulatory compliance support and optimized reagent logistics.

- April 2025: PerkinElmer: Enhanced isotope supply chain capabilities: to ensure consistent reagent availability amid transportation constraints: deploying advanced cold-chain monitoring systems and quality-controlled isotope production processes.

- March 2024: Beckman Coulter Life Sciences: Introduced updated gamma counter instrumentation to improve radiation detection accuracy and laboratory workflow efficiency, integrating automated sample handling and enhanced shielding technology.

- July 2024: DRG International: Launched new thyroid hormone radioimmunoassay kits to address growing diagnostic demand in endocrine disorders, utilizing refined tracer labeling processes and improved assay sensitivity parameters.

REPORT COVERAGE

The global radioimmunoassay market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation:

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 2.61% from 2026-2034 |

| Unit | Value (USD million) |

| Segmentation | By Product Type, Application, End-user, and Region |

| By Product Type |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 225.00 million in 2026 and is projected to reach USD 276.54million by 2034.

In 2025, North America was valued at USD 66.3million.

Registering a CAGR of 2.61%, the market is expected to exhibit healthy growth during the forecast period of2026-2034.

By product type, the kits and reagents segment is expected to lead this market during the forecast period.

The rising endocrine and oncological disorders prevalence are major factor driving the markets growth.

Revvity, Inc., DIAsource, MP Biomedicals, Institute of Isotopes, and DiaSorin S.p.A. are the major players in the market.

North America held a dominant market share in 2025.

Decentralization & innovative technology adaptation are transforming the radioimmunoassay platforms.

- 2021-2034

- 2025

- 2021-2024

- 230

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us