Radioligand Therapies Market Size, Share & Industry Analysis, By Product (Lutetium Lu 177 Vipivotide Tetraxetan, Lutetium Lu 177 Dotatate, and Others), By Indication (Prostate Cancer, Neuroendocrine Tumors, and Others), By Target (Prostate-Specific Membrane Antigen (PSMA), Somatostatin Receptor, and Others), By End User (Tertiary Care Academic/Comprehensive Cancer Centers, Specialized Nuclear Medicine Centers, and Others), and Regional Forecast, 2026-2034

Radioligand Therapies Market Size and Future Outlook

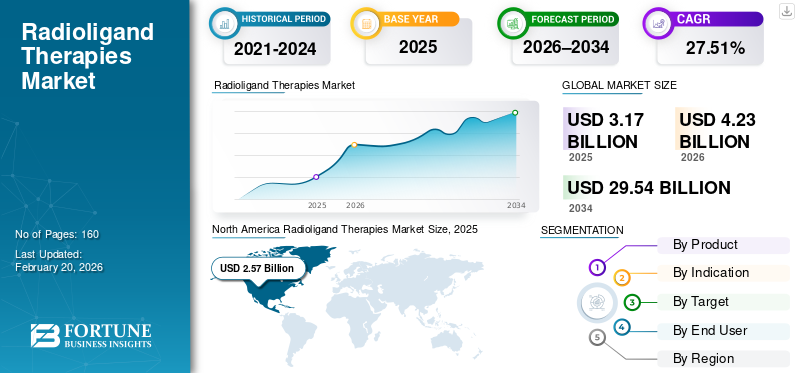

The global radioligand therapies market size was valued at USD 3.17 billion in 2025. The market is projected to grow from USD 4.23 billion in 2026 to USD 29.54 billion by 2034, exhibiting a CAGR of 27.51% during the forecast period. North America dominated the global radioligand therapies market with a market share of 81.07% in 2025.

Radioligand therapies are a part of the broader therapeutic radiopharmaceuticals market and refer to a cancer treatment modality where the targeting molecule (ligand) is chemically linked to a therapeutic radioisotope such as Lu-177. The market is expected to grow considerably across the forecast period, primarily driven by the booming sales revenues of its key products and the high probability of favorable regulatory approvals for major products. Furthermore, the market growth is augmented by a large number of eligible patients, recent regulatory approvals to allow therapy administration at early stages, and premium pricing. Also, presence of prominent emerging companies with notable pipeline candidates for radioligand therapies is anticipated to boost the market growth.

For instance, in November 2025, ITM Isotope Technologies Munich SE, announced that the U.S. FDA had accepted the company’s application for a New Drug Application (NDA) and had set a Prescription Drug User Fee Act (PDUFA) of August 28, 2026, for its pipeline product of n.c.a. 177Lu-edotreotide (ITM-11). This pipeline radioligand therapy is approved for gastroenteropancreatic neuroendocrine tumors (GEP-NETs).

In the current market scenario, the market is dominated by Novartis AG, due to the presence of the top two approved radioligand therapies in its product portfolio that is PLUVICTO and LUTATHERA. Other notable pharmaceutical companies are Bristol-Myers Squibb Company, AstraZeneca, and Eli Lilly and Company owing to their prominent radioligand therapy pipelines.

Download Free sample to learn more about this report.

RADIOLIGAND THERAPIES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.17 Billion

- 2026 Market Size: USD 4.23 Billion

- 2034 Forecast Market Size: USD 29.54 Billion

- CAGR: 27.51% from 2026–2034

- North America dominated the radioligand therapies market with an 81.07% share in 2025.

- The Lutetium Lu 177 Vipivotide Tetraxetan segment held the largest market share in 2025.

- The prostate cancer segment accounted for the dominant market share in 2025.

North America

North America reached USD 2.57 billion in 2025, accounting for 81.07% of global market revenue.

Europe

Europe is projected to reach USD 0.56 billion by 2026 and record the highest regional CAGR of 38.87%.

Asia Pacific

Asia Pacific was valued at USD 0.15 billion in 2025, ranking as the third-largest regional market.

U.S.

The market is projected to reach USD 3.20 billion by 2026.

Japan

The market was valued at USD 0.04 billion in 2025, accounting for 1.3% of global revenue.

Read More

RADIOLIGAND THERAPIES MARKET TRENDS

Development of Dedicated Manufacturing Sites is a Leading Market Trend

An important trend in the global market is the transition toward the creation of supply chains at an industrial scale level for these therapies. Key players are developing multi-site manufacturing networks, tighter cold chain logistics to ensure consistent availability of radioligand therapies. In recent times, companies are considering the presence of regular radioisotope supply as a strategic asset and investing in acquisitions, developing in-house supply of isotopes, and engaging in long term contracts. Hence, companies are transitioning from a capability of having a radioligand therapy in their product portfolio to possessing a repeatable end-to-end platform for the developing and manufacturing of radioligand therapies. These include the capabilities of target discovery, chelation chemistry, dosimetry/optimization, manufacturing, and rapid distribution.

For instance, in November 2025, Novartis AG announced the opening of a new 0,000-square-foot radioligand therapy (RLT) manufacturing facility in Carlsbad, California in the U.S. This allows Novartis to seamlessly meet the demand for their radioligand therapies without any disruptions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Strong Regulatory Approvals Catering to Wider Patient Population Base Drive Market Growth

The demand for radioligand therapies are undergoing considerable growth as they are at the intersection of radiation oncology and precision oncology, allowing clinicians to treat disseminated disease with targeted and systemic radiation. Recent regulatory approvals have allowed for these therapies to be administered in the earlier stages of notable diseases such as prostate cancer. This significantly increases the patient volume undertaking these therapies and drives value growth. Furthermore, increasing incidences of advanced prostate cancer patients necessitate the administration of efficient therapies such as radioligand therapies, especially after Androgen Receptor Pathway Inhibitor (ARPI) therapies. Moreover, the strong prevalence of Neuroendocrine Tumors (NETs) and the associated long survivorship, keep the demand for these therapies growing.

For instance, in March 2025, the U.S. FDA approved Novartis AG’s radioligand therapy of PLUVICTO to be used in patients after one Androgen Receptor Pathway Inhibitor (ARPI) and before the administration of chemotherapy. This new indication approval approximately triples the eligible patient population for these therapies.

MARKET RESTRAINTS

Issues with Operational Scalability is a Major Market Restraint

Some of the most important factors that affect the continued growth of the global market are the drawbacks associated with the supply chain process as it uses short-lived isotopes. Operational constraints such as limited manufacturing capacity, transportation bottlenecks and insufficient number of qualified nuclear medicine sites prevent demand from translating into actual treated patient volumes. This gap delays value realization and further restricts market growth. Additionally, the administration of radioligand therapy is highly dependent on companion imaging workflow such as a positron emission tomography test, PSMA PET. Issues in the accessibility and necessary reimbursement coverage along with lack of preparedness of medical centers such as absence of appropriately trained staff and radiation safety protocols also further dampens growth prospects.

For example, in August 2025, Agência Nacional de Vigilância Sanitária (ANVISA), Brazil’s regulatory agency described the practical issues associated with the administration of PLUVICTO in Brazil, such as logistics/clearances and dose import realities.

MARKET OPPORTUNITIES

Focus Toward Newer Application Areas to Provide Avenues for Market Growth

One of the opportunities for market growth is the expansion of the several approved products beyond LUTATHERA and PLUVICTO. This expansion into multiple and newer targets and isotopes considerably increases the addressable market. Another critical area of market opportunity for the established and prospective companies is the focus on geographical expansion. In many developing countries, the lack of adequate infrastructure for nuclear medicine procedures, including the administration of radioligand therapies remains a critical limitation. Hence, strengthening diagnostic capabilities and improving site readiness across these regions can considerably increase the opportunities for market expansion.

For instance, in April 2025, Perspective Therapeutics, Inc. announced that the first patient had been dosed with [212Pb] VMT01 Monotherapy at 1.5 mCi, in a Phase 1/2a clinical trial of MC1R-Positive Metastatic Melanoma.

MARKET CHALLENGES

Issues with Reliable Isotopes Supply to Pose Significant Market Growth Challenges

A core challenge pertaining to the radioligand therapies market growth is the issue associated with consistent availability of radioisotopes for its manufacturing. This is particularly applicable for the upcoming class of alpha emitting radioligand therapies, where manufacturing capacities are often limited and complex. Furthermore, another critical challenge is demonstrating value in broader populations, this involves multi-country trials which leads to hurdles in clinical development. The manufacturing process must meet the challenges associated with biologics manufacturing coupled with radiochemical constraints such as time and delays.

For instance, in June 2025, Telix Pharmaceuticals Limited announced a shortage in Portugal of gallium-68 tracers, which has resulted in a national waiting list of up to six months. This shortage impacts the detection and localization of prostate-specific membrane antigen (PSMA)-positive lesions in adults with prostate cancer.

Segmentation Analysis

By Product

Considerable Sales Revenue of PLUVICTO (lutetium Lu 177 vipivotide tetraxetan) Supports its Leadership

On the basis of product, the market is segmented into Lutetium Lu 177 Vipivotide Tetraxetan, Lutetium Lu 177 Dotatate, and others.

The Lutetium Lu 177 Vipivotide Tetraxetan segment is projected to account for the dominant radioligand therapies market share owing to PLUVICTO’s considerable sales revenue coupled with the therapy approval for the earlier stages of disease treatment. This approval by the U.S. FDA is critical as it positions PLUVICTO to be administered before chemotherapy, and may help boost its adoption as many patients may not reach the later stages of disease and treatment.

- For example, in October 2025, Novartis AG announced that data from PLUVICTO, from the Phase III PSMAddition trial in a Presidential Symposium at the European Society for Medical Oncology (ESMO) Congress 2025 indicated that the therapy stopped the progression to end stage prostate cancer.

The Lutetium Lu 177 Dotatate segment is anticipated to rise with a CAGR of 19.35% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Indication

Favorable Regulatory Approvals to Enable Prostate Cancer’s Segmental Dominance

On the basis of indication, the market is segmented into prostate cancer, neuroendocrine tumors, and others.

In 2025, the prostate cancer segment accounted for the dominant revenue share of the global market due to its considerably wide patient population prone to disease metastasis and a validated target (PSMA) that has an established imaging-to-therapy workflow. Also, the increasing penetration of PSMA PET diagnostics across the globe is expected to broadly increase the patients that can be screened and treated.

For instance, in September 2025, data published by the American Cancer Society (ACS), there will be an estimated 313,780 new cases of prostate cancer in the U.S.

The neuroendocrine tumors segment is projected to grow at a CAGR of 18.15% over the forecast period.

By Target

Wider Adoption of Prostate-Specific Membrane Antigen (PSMA) Diagnostics to Allow for Segmental Dominance

On the basis of target, the market is segmented into prostate-specific membrane antigen (PSMA), somatostatin receptor, and others.

The prostate-specific membrane antigen (PSMA) segment accounted for the dominant market share over the forecast period as PSMA is a highly validated, high-contrast target in terms of both, diagnostics and therapy. This allows for clear selection of patients and also the measurable outcomes. The expression of the PSMA target allows for a scalable theranostics pathway that ends treatment uncertainty for many patients and supports favorable decisions from clinicians and healthcare payers.

- For instance, in June 2025, Siemens Healthineers Molecular Imaging announced a research collaboration on theranostics with Massachusetts General Hospital (MGH). This collaboration will include the utilization of Biograph Vision Quadra and Biograph Trinion positron emission tomography/computed tomography (PET/CT) scanners for the management of various cancers including prostate cancers.

The others segment is projected to grow at a CAGR of 45.12% over the forecast period.

By End User

Strong Treatment Initiation Rates in Tertiary Care Academic/Comprehensive Cancer Centers to Boost Segmental Dominance

On the basis of end user, the market is segmented into tertiary care academic/comprehensive cancer centers, specialized nuclear medicine centers, and others.

The tertiary care academic/comprehensive cancer centers segment accounted for the largest market share as the administration of radioligand therapy requires the coordination of nuclear medicine and oncology departments coupled with radiation safety and handling infrastructure. Furthermore, these capabilities are mostly consistently concentrated in large academic/comprehensive centers, who are also the early adopters of new radioligand therapy clinical trials.

- For instance, in November 2025, UCLA Health announced the establishment of the Department of Nuclear Medicine and Theranostics, formalizing theranostics into its own dedicated department through the integration of imaging and therapy.

The specialized nuclear medicine centers segment is projected to grow at a CAGR of 22.41% over the forecast period.

Radioligand Therapies Market Regional Outlook

In terms of geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Radioligand Therapies Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 1.99 billion, and also maintained the leading share in 2025, with USD 2.57 billion. The market in North America is projected to grow significantly across the forecast period owing to a strong patient population base, presence of reimbursement maturity, high penetration of PET diagnostics and concentrated theranostics centers. These factors coupled with advancements in supply chain and favorable regulatory approval scenario drives market growth in the region.

U.S. Radioligand Therapies Market

Based on North America’s regional dominance and the U.S.’s largest share within the region, the U.S. market can be analytically approximated around USD 3.20 billion in 2026, accounting for roughly 75.7% of global sales.

Europe

Europe is on track to record a growth rate of 38.87% in the coming years, the highest amongst all regions, and reach a valuation of USD 0.56 billion in 2026. Some of the parameters to the region’s strong market share includes strong penetration of radioligand therapies for neuroendocrine tumors coupled with presence of strong academic center leadership and high trial participation.

U.K. Radioligand Therapies Market

The U.K. market in 2025 is estimated at around USD 0.06 billion, representing roughly 2.0% of global revenues.

Germany Radioligand Therapies Market

The market in Germany reached approximately USD 0.10 billion in 2025, equivalent to around 3.2% of global sales.

Asia Pacific

In Asia Pacific, the market reached USD 0.15 billion in 2025 and secured the third position, in terms of value. In the region, India and China achieved USD 0.02 billion and USD 0.05 billion, respectively in 2025.

Japan Radioligand Therapies Market

In 2025, Japan captured USD 0.04 billion, accounting for roughly 1.3% of global revenues. Japan holds a large share of the global market owing to high clinical sophistication, strong cancer care infrastructure, and rapid adoption when reimbursement and logistics are solved.

China Radioligand Therapies Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 0.05 billion, representing roughly 1.6% of global sales.

India Radioligand Therapies Market

India’s market in 2025 reached USD 0.02 billion, accounting for roughly 0.5% of global revenues.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa are expected to witness steady positive growth during the forecast period. The market in Latin America hit USD 0.04 billion in 2025. Increasing diagnostics capabilities, strong disease prevalence and favorable regulatory scenario is to drive the market growth in these regions. In the Middle East & Africa, the GCC achieved USD 0.01 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Presence of Cornerstone Radioligand Therapies to Ensure Novartis’ Market Dominance

The global radioligand therapies market comprises a consolidated competitive structure, with Novartis AG holding a considerable, dominant proportion of the market. The company’s dominance is due to the presence of radioligand assets of LUTATHERA and PLUVICTO in its product portfolio. Moreover, to ensure its continued market dominance, the company has significantly boosted its manufacturing readiness and positive clinical trial readouts to allow for the same.

- For instance, in January 2024, Novartis presented data from the Phase III NETTER-2 trial that demonstrated LUTATHERA, considerably reduced the risk of disease progression or death by an estimated 72%, when used as a first line therapy for patients with advanced gastroenteropancreatic neuroendocrine tumors.

Other major companies include Bristol-Myers Squibb Company, AstraZeneca, and Eli Lilly and Company among others. These companies are focused on developing their radioligand therapies’ pipeline which may eventually lead to new product approvals and are emphasizing on building their radioisotope supply capacities to allow for consistent product supply.

LIST OF KEY RADIOLIGAND THERAPIES COMPANIES PROFILED

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.S.)

- Eli Lilly and Company (U.S.)

- ITM Isotope Technologies Munich SE (Germany)

- Telix Pharmaceuticals Limited (Australia)

- Perspective Therapeutics (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Bristol Myers Squibb and RayzeBio announced the opening of its radiopharmaceutical manufacturing facility in Indianapolis, U.S. The 77,000-square foot complex is equipped to manufacture the next generation of radioligand therapies based on alpha-emitting isotope actinium-225 (Ac-225).

- June 2025: ITM Isotope Technologies Munich SE (ITM) and the Institut Laue-Langevin (ILL) announced an extension of their medical radioisotope production collaboration for the supply of medical Lutetium-177 radioisotope.

- March 2025: Eckert & Ziegler SE and AtomVie Global Radiopharma Inc., signed a global agreement for the supply of Lutetium-177 chloride (n.c.a. Lu-177, Theralugand)

- May 2024: Novartis AG announced the acquisition of Mariana Oncology for strengthening of the company’s radioligand therapy pipeline.

- January 2024: Fusion Pharmaceuticals (AstraZeneca), announced that its state of the art manufacturing facility was now fully functional, with the production of the first clinical doses.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 27.51% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Indication, Target, End User, and Region |

|

By Product |

· Lutetium Lu 177 Vipivotide Tetraxetan · Lutetium Lu 177 Dotatate · Others |

|

By Indication |

· Prostate Cancer · Neuroendocrine Tumors · Others |

|

By Target |

· Prostate-Specific Membrane Antigen (PSMA) · Somatostatin Receptor · Others |

|

By End User |

· Tertiary Care Academic/Comprehensive Cancer Centers · Specialized Nuclear Medicine Centers · Others |

|

By Region |

· North America (By Product, Indication, Target, End User, and Country) o U.S. o Canada · Europe (By Product, Indication, Target, End User, and Country/Sub-Region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Product, Indication, Target, End User, and Country/Sub-Region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Product, Indication, Target, End User, and Country/Sub-Region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Product, Indication, Target, End User, and Country/Sub-Region) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.17 billion in 2025 and is projected to reach USD 29.54 billion by 2034.

In 2025, the market value of North America stood at USD 2.57 billion.

The market is expected to exhibit a CAGR of 27.51% during the forecast period of 2026-2034.

By product, the lutetium Lu 177 vipivotide tetraxetan segment is expected to lead the market.

Strong regulatory approvals catering to wider patient population base are the key factors that drive the market growth.

Novartis AG, Bristol-Myers Squibb Company, AstraZeneca, Eli Lilly and Company, ITM Isotope Technologies Munich SE are the dominant players in the global market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us