Prostate Cancer Therapeutics Market Size, Share & Industry Analysis, By Drug Class (Androgen Receptor & Microtubule Inhibitors, Gonadotropin Releasing Hormone (GnRH) Agonist, Gonadotropin-Releasing Hormone (GnRH) Receptor Antagonist), By Route of Administration (Oral & Parenteral), By Therapy (Chemo, Hormonal, Targeted, and Immuno Therapy), By Disease State (Metastatic Castration-Resistant Prostate Cancer & Non-Metastatic Castration-Resistant Prostate Cancer), By Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, & Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

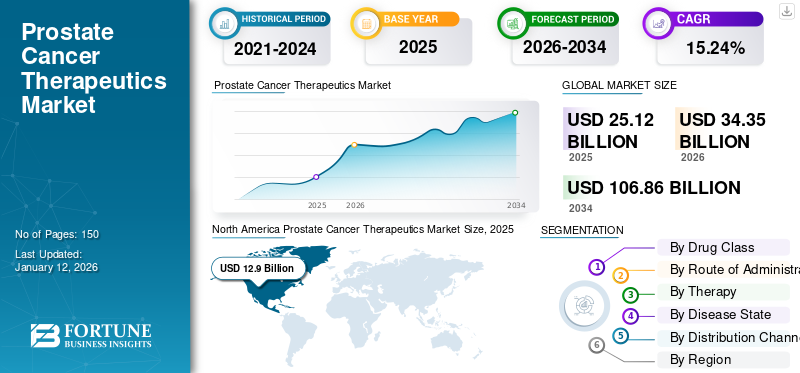

The global prostate cancer therapeutics market size was valued at USD 25.12 billion in 2025 and is projected to grow from USD 34.35 billion in 2026 to USD 106.86 billion by 2034, exhibiting a CAGR of 15.24% during the forecast period. North America dominated the prostate cancer therapeutics market with a market share of 51.37% in 2025.

Prostate cancer is a type of cancer that develops in the prostate gland and is one of the most common cancers affecting men, particularly in the older population. The rising prevalence of prostate cancer among geriatric male is a key factor driving the growth of the market.

- For instance, according to the data published by the American Cancer Society, Inc., prostate cancer is more prevalent among older men, with approximately 6 in 10 diagnoses occurring in those aged 65 and above, while it is uncommon in men under 40. The typical age for a man's first diagnosis is around 67. Such a large number of vulnerable populations affected by prostate cancer drives the demand for prostate cancer therapeutics.

Moreover, the therapy for prostate cancer involves standard treatments such as hormone therapy and advanced therapies such as targeted therapy, immunotherapy, and chemotherapy. Rising awareness and diagnosis of prostate cancer in males tend to boost the adoption of early treatment to mitigate the risk associated with cancer, thus escalating the demand for the treatment options and eventually leading to market growth.

The presence of key pharmaceutical companies and biopharmaceutical companies such as Pfizer Inc., Sanofi, AstraZeneca, and others are actively engaged in developing innovative treatments. Their advanced product offerings and robust research and development programs strengthen their standing in the market.

Download Free sample to learn more about this report.

Global Prostate Cancer Therapeutics Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 25.12 billion

- 2026 Market Size: USD 34.35 billion

- 2034 Forecast Market Size: USD 106.86 billion

- CAGR: 15.24% from 2026–2034

Market Share:

- North America dominated the prostate cancer therapeutics market with a 51.37% share in 2025, driven by the high prevalence of prostate cancer, presence of advanced healthcare infrastructure, and strong adoption of innovative therapies.

- By drug class, Androgen Receptor Inhibitors is expected to retain its largest market share, supported by their crucial role in blocking androgen receptors and the rising adoption for first-line treatments in advanced prostate cancer cases.

Key Country Highlights:

- United States: Growth is driven by the increasing burden of prostate cancer, higher adoption of radiopharmaceuticals, and favorable regulatory approvals accelerating access to advanced therapeutics.

- Europe: The region's growth is supported by the expanding availability of advanced prostate cancer drugs, strong healthcare infrastructure, and strategic market entries by leading pharmaceutical players.

- China: The market is fueled by rising cancer incidence, expanding R&D collaborations between global and domestic firms, and the growing focus on enhancing access to oncology therapeutics.

- Japan: Increasing healthcare expenditure, strong adoption of precision medicine approaches, and efforts to introduce novel targeted therapies are key growth factors for the prostate cancer therapeutics market.

MARKET DYNAMICS

MARKET DRIVERS

Rising Prevalence of Prostate Cancer to Boost Demand for the Product

One of the most critical drivers that positively impact the prostate cancer treatment market is the extensive increase in the global prevalence of prostate cancer, leading to increased product adoption.

For instance, according to the report published by the Global Cancer Observatory GLOBOCAN 2022, prostate cancer ranked 4th in all types of cancers, with a total incidence of prostate cancer being around 1.47 million in 2022. Thus, such a large number of the population affected by prostate cancer every year increases the demand for effective treatment options and thus bolsters market growth.

Additionally, increasing awareness programs to educate people to understand the symptoms and importance of early screening are leading to higher diagnosis rates and subsequent treatment.

For instance, the month of November every year is globally recognized and celebrated to raise awareness for prostate cancer in males. In November 2024, Europa Uomo members in Hungary and Italy raised awareness of prostate cancer by launching testing programs during the "Movember" Campaign.

Such rising prevalence and rising awareness programs are expected to increase the adoption of prostate cancer drugs and thus drive the global prostate cancer therapeutics market growth.

MARKET RESTRAINT

Resistance to Hormone Therapy and Adverse Effects of Prostate Cancer Drugs to Hamper Market Growth

Prostate cancer occurs due to the activation of the Androgen Receptor (AR) by androgens. Hormone therapies are designed to lower androgen levels or inhibit their effects. However, during treatment, mutations in the androgen receptor take place, leading to abnormal activation of AR, resulting in castration-resistant prostate cancer. Thus, such mutation diminishes the effectiveness of hormone therapy and leads to a decrease in the adoption of the drug and impacting the growth of the market.

Moreover, adverse effects associated with chemotherapy and hormonal therapy can be extensive, including erectile dysfunction, decreased libido, hot flashes, reduced bone density, bone fractures, loss of muscle mass and physical strength, insulin resistance, weight gain, mood swings, fatigue, and gynecomastia, others. These side effects can significantly affect a patient's quality of life and may lead to the discontinuation of treatment.

MARKET OPPORTUNITIES

Focus on Research and Development Activities to Launch Combination Therapy to Determine Growth Trajectory

Numerous research and development initiatives have been undertaken to launch effective treatment strategies for managing Metastatic Castration-Resistant Prostate Cancer (mCRPC). To mitigate resistance associated with hormonal therapies, many key companies are focusing on developing and launching combination therapies to enhance treatment efficacy and combat resistance.

The companies are pairing Poly ADP-ribose Polymerase (PARP) inhibitors with androgen deprivation therapies and Androgen Receptor Inhibitors (ARIs). Additionally, the rising number of regulatory approvals for these therapies is anticipated to drive market growth during the forecast period.

- For instance, in November 2024, Bayer AG announced that the U.S. Food and Drug Administration (FDA) had accepted the Supplemental New Drug Application (sNDA) for NUBEQA (darolutamide) in combination with Androgen Deprivation Therapy (ADT) for treating patients with Metastatic Hormone-Sensitive Prostate Cancer (mHSPC). Such scenarios propel the growth of the market during the forecast timeframe.

MARKET CHALLENGES

High Treatment Cost to Restraint Market Growth

The advanced therapies for prostate cancer are significantly high in cost. This is due to the high cost of research, development, and clinical trials, making them less accessible in emerging low-middle-economic countries.

Moreover, the lack of a proper reimbursement structure for prostate cancer drugs and treatment among the majority of the emerging countries makes it difficult for the population to undergo the treatment due to financial burden. Such restrictions may limit the adoption of the drugs and market growth.

PROSTATE CANCER THERAPEUTICS MARKET TRENDS

Emergence of New Therapies for Prostate Cancer Treatment is a Prominent Trend

The shift toward targeted, personalized, and effective therapies marks a significant trend in the market. The landscape of targeted therapies is broadening, particularly with agents that focus on specific molecular pathways associated with cancer progression.

The leading companies in the market are developing drugs aimed at managing metastatic castration-resistant prostate cancer (mCRPC) in patients with BRCA1 or BRCA2 mutations.

- For instance, in August 2023, Johnson & Johnson Services, Inc. announced that the U.S. Food and Drug Administration (FDA) had approved AKEEGA, a combination therapy of niraparib and abiraterone acetate with prednisone, specifically for mCRPC patients with BRCA1 or BRCA2 mutations. Such approvals for launching specific treatment options for genetic mutations are expected to shift companies' focus toward developing new drugs, providing long-term opportunities for market growth.

Download Free sample to learn more about this report.

COVID-19 IMPACT ON MARKET

The COVID-19 pandemic had a slightly positive impact on the prostate cancer therapeutics market, primarily attributed to the ongoing research & development initiatives. The pandemic also accelerated the adoption of telemedicine, enabling continued care for prostate cancer patients. However, surgical treatment options for prostate cancer were hampered due to a decrease in hospital visits, leading to a shift in focus toward long-acting hormone therapies. Such scenarios propelled the growth of the market during the pandemic. In 2021, there was an increase in the revenue of key players from their key products. Additionally, the approvals and launches of the rising clinical studies are expected to propel market growth during the forecast period.

SEGMENTATION ANALYSIS

By Drug Class

Androgen Receptor Inhibitors Segment Led due to Increasing Prevalence of Prostate Cancer

Based on drug class, the global market is categorized into androgen receptor inhibitors, microtubule inhibitors, Gonadotropin Releasing Hormone (GnRH) agonist, Gonadotropin-Releasing Hormone (GnRH) receptor antagonist, and others.

The androgen receptor inhibitors segment held a dominant global prostate cancer therapeutics market share in 2026. The growth of the segment is augmented by the increasing prevalence of prostate cancer and the rising demand for androgen receptor inhibitors to block androgen receptors and prevent testosterone from fueling cancer growth. The androgen receptor inhibitors segment segment will account for 72.86% market share in 2026.

The Gonadotropin-Releasing Hormone (GnRH) agonist segment is expected to grow with significant CAGR during the forecast period. GnRH agonist, also known as Luteinizing Hormone Releasing Hormone (LnRH) agonist, is one of the most prominent treatments for prostate cancer. These drugs are highly effective at suppressing the testosterone levels, and their increased efficacy, safety, and convenience are driving the adoption of these drugs for treatment. Additionally, rising GnRH agonist product launches by key players are propelling the segment's growth.

- For instance, in March 2022, Accord BioPharma announced the launch of CAMCEVI (leuprolide) 42mg injection emulsion in the U.S. to treat patients with advanced prostate cancer in adults.

Microtubule inhibitor, Gonadotropin-Releasing Hormone (GnRH) receptor antagonist, held a comparatively lower share of the market but is expected to grow during the forecast period.

The other segment comprises Poly (ADP-ribose) Polymerase (PARP) inhibitor and CYP17 inhibitor is also poised for growth during the forecast period. Rising demand for targeted treatments and increasing resistance to androgen deprivation therapy is shifting the focus of patients and caregivers to adopt more precise treatment options.

To know how our report can help streamline your business, Speak to Analyst

By Route of Administration

Oral Segment Led the market due to Better Patient Compliance

Based on route of administration, the market is segmented into oral and parenteral.

The oral segment held the dominant share of the market in 2026. The ease of administration, better patient compliance, and retention of treatment for long-term plans augment the growth of the segment. Additionally, oral dosage forms are easier to manage and incorporate into daily routines, as high compliance is crucial in managing chronic diseases such as prostate cancer.

Additionally, some of the newer oral therapies are showcasing positive results in clinical trials, making them attractive options for treating prostate cancer. Key market players are focusing on launching new oral drugs, propelling the segment growth. The oral segment is expected to account for 86.45% of the market in 2026.

- For instance, in December 2020, Myovant Sciences GmbH collaborated with Pfizer Inc. to develop and commercialize relugolix, a once-daily oral GnRH receptor antagonist, in the U.S. and Canada.

The parenteral segment held a comparatively lower share of the market owing to its invasive nature, higher costs, and inconvenience of frequent clinic visits for injection or infusions. The segment is anticipated to grow with a substantial CAGR of 24.70% during the forecast period (2025-2032).

By Therapy

Hormonal Therapy Segment Lead due to Presence of Key Players

Based on therapy, the market is segmented into chemotherapy, hormonal therapy, targeted therapy, and immunotherapy.

Hormonal therapy holds a significant portion of the market, with the growth of the segment augmented by the widespread adoption of androgen deprivation therapy for treating both early and advanced stages of prostate cancer. Its efficacy in targeting androgen-dependent tumors and managing the growth of cancer cells. Additionally, the presence of various major players in the market with a robust product portfolio of hormonal therapy drugs is propelling market growth. The hormonal therapy segment is anticipated to hold a dominant market share of 80.91% in 2026.

The immunotherapy segment held the second-largest share of the market, driven by innovative approaches that harness immune systems to combat cancer. Sipuleucel-T (Provenge), launched by Dendreon Pharmaceuticals LLC, is the only FDA-approved vaccine that spurs a patient's immune system to attack prostate cancer cells. Additionally, positive studies on the vaccine are increasing its adoption among patients.

- For instance, in October 2020, Dendreon Pharmaceuticals LLC announced a new analysis revealing that incorporating PROVENGE into treatment plans for men with Metastatic Castrate-Resistant Prostate Cancer (mCRPC) significantly enhances survival outcomes. The study, which utilized Medicare claims data from over 6,000 beneficiaries, found that adding PROVENGE to either abiraterone acetate (Zytiga) or enzalutamide (Xtandi) reduced the risk of death by 41% and increased median overall survival by 14.5 months.

The targeted therapy held a substantial share of the market. The growing demand for treatments targeting mutated prostate cancer genes and the increasing shift of patients and healthcare providers toward precise therapy options will boost segment growth during the forecast period.

The chemotherapy segment held a comparatively lower share of the market due to its nonspecific mechanism of action and significant side effects over other therapies. The segment is anticipated to hold 2.8% of the market share in 2025.

By Disease State

Metastatic Castration-Resistant Prostate Cancer Segment Led due to Rising Disease Burden

Based on disease state, the market is sub-segmented into metastatic castration-resistant prostate cancer and non-metastatic castration-resistant prostate cancer.

The metastatic castration-resistant prostate cancer segment held a dominant share of the prostate cancer therapeutics market. Metastatic Castration-Resistant Prostate Cancer (mCRPC) is an advanced stage of prostate cancer that spreads beyond the prostate and becomes resistant to androgen deprivation therapy. The significant disease burden and increasing approvals by regulatory bodies for new treatments to treat mCRPC are driving the growth of the segment. The metastatic castration-resistant prostate cancer segment will account for 84.65% market share in 2026.

- For instance, in June 2023, AstraZeneca revealed that Lynparza (olaparib), in combination with abiraterone and prednisone or prednisolone, has been approved in the U.S. for treating adult patients with Metastatic Castration-Resistant Prostate Cancer (mCRPC) who have deleterious or suspected deleterious BRCA mutations.

Non-metastatic castration-resistant prostate cancer is expected to grow during the forecast period with a significant CAGR. The growth of the segment is attributed to the increasing focus of key companies to expand the indication of their key prostate cancer drugs for treating non-metastatic castration-resistant prostate cancer. This segment is foreseen to gain 20.20% of the market share in 2025.

- For instance, in August 2023, Astellas Pharma Inc. announced that the U.S. FDA accepted a supplemental New Drug Application for XTANDI for the treatment of patients with non-metastatic castration-sensitive prostate cancer. Such scenarios promoted the growth of the segment during 2025-2032.

By Distribution Channel

Strong Presence of Patients in Hospital Settings Contribute to Hospital Pharmacies’ Segmental Dominance in 2024

Based on distribution channel, the global market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

The hospital pharmacies segment held a dominant share of the market in 2024. The presence of advanced healthcare facilities in the hospitals and the shift of focus of patients and caregivers towards these settings is propelling the segment’s growth in the market. This segment is expected to capture 55.2% of the market share in 2025.

Additionally, the increasing number of inclusions of prostate cancer therapeutics under reimbursement policies is one of the major factors contributing to the growth of the segment.

The retail pharmacies and online pharmacies segments are also expected to grow considerably in the market during the forecast period. The increasing penetration of the internet and the preferential shift of patients to buying medicines online appeal to e-commerce players who want to invest in online healthcare platforms.

- For instance, according to a 2022 study published by Frontiers in Pharmacology, approximately 55.5% of the population purchases medications online among patients.

The drug stores & retail pharmacies are predicted to grow at a CAGR of 22.77% during the forecast period (2025-2032).

PROSTATE CANCER THERAPEUTICS MARKET REGIONAL OUTLOOK

Based on region, the market is studied across Europe, North America, the Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Prostate Cancer Therapeutics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 12.9 billion in 2025, representing 51.37% of the global industry, and is expected to reach USD 18.08 billion in 2026. The region is anticipated to grow at a moderate CAGR during the forecast period. The growth of the region is due to the increase in prevalence of prostate cancer, the presence of advanced healthcare facilities, comparatively higher diagnosis and treatment rates and increasing expenditure on cancer care. Additionally, the presence of key players in the market with advanced research and development facilities is boosting the region's growth.

Additionally, the U.S. dominated the North American market. The significant share of the country is due to growing incidences of prostate cancer in the U.S., along with higher adoption of advanced and superior radiopharmaceuticals for its management.

Furthermore, presence of key players with the surge in regulatory approvals for radiopharmaceuticals, are driving the demand for the prostate cancer therapeutics in the U.S. market. The U.S. market is poised to reach USD 17.29 billion in 2026.

- For instance, in March 2022, Novartis AG received the U.S. FDA approval for Pluvicto to treat a patient with Metastatic Castration-Resistant Prostate Cancer (mCRPC).

Europe

Europe recorded a market size of USD 5.89 billion in 2025, capturing 23.45% of the global market share, and is projected to reach USD 7.84 billion in 2026, driven by the rising prevalence of prostate cancer, availability of advanced healthcare facilities with skilled medical professionals, and increase in demand for prostate cancer therapeutics. Additionally, the rising shift of focus of pharmaceutical companies to launch drugs in the region is expected to propel the growth. The U.K. market is expanding and is set to expand with a valuation of USD 1.41 billion in 2026.

- In April 2022, Myovant Sciences GmbH announced that the European Commission (EC) had approved the marketing authorization application for ORGOVYX for the treatment of advanced hormone-sensitive prostate cancer.

Germany is anticipated to reach a market value of USD 2.17 billion in 2026, while France is set to be worth USD 0.69 billion in the same year.

Asia Pacific

In 2025, Asia Pacific represented USD 4.48 billion, accounting for 17.83% of the worldwide market, and is projected to grow to USD 6.21 billion in 2026. The region is growing due to the rising prevalence of cancer and the presence of key companies with advanced strategies to expand their presence in the global market. The market in China is expected to gain USD 2.22 billion in 2026.

- For instance, in April 2022, Sanofi collaborated with Innovent Biologics with the aim of developing oncology medicines and expanding its geographical reach in China.

India is expected to attain USD 0.8 billion in 2026, while Japan is set to be valued at USD 1.14 billion in the same year.

Latin America and Middle East & Africa

The Latin America market was valued at USD 1.19 billion in 2025, capturing 4.75% of global revenue, and is estimated to reach USD 1.44 billion in 2026. The Latin America and the Middle East & Africa regions are anticipated to grow considerably during the forecast period. This growth is due to the rising awareness of prostate cancer and the increasing regulatory approvals for key drugs, which will contribute to regional growth. Middle East & Africa contributed 2.61% to the global market in 2025, with a valuation of USD 0.66 billion, and is projected to reach USD 0.78 billion in 2026. The GCC market is estimated to reach USD 0.34 billion in 2025.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Collaborations to Hold Key Market Share

Pfizer Inc. and Johnson & Johnson Services, Inc. are prominent players in the prostate cancer therapeutics industry, contributing significantly to the global market in 2024. Their strong product portfolio, regulatory approvals, and product launches help maintain their position in the market. Additionally, strategic initiatives such as collaborations and product approvals further strengthen their position in the industry.

Other leading companies include Astellas Pharma Inc., AbbVie Inc, AstraZeneca, and others. These companies employ various strategies, including launching new products, forming joint ventures and partnerships, and expanding into new regions to increase their market share.

LIST OF KEY PROSTATE CANCER THERAPEUTICS COMPANIES PROFILED

- Astellas Pharma Inc. (Japan)

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Sanofi (France)

- Ferring Pharmaceuticals Inc. (Switzerland)

- Sumitomo Pharma Co., Ltd. (Myovant Sciences GmbH) (Japan)

- AbbVie Inc. (U.S.)

- AstraZeneca (U.K.)

- Tolmar, Inc. (U.S.)

- Dendreon Pharmaceuticals LLC. (U.S.)

- Bayer AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- December 2024: AbbVie Inc. initiated the Phase 1 clinical trial for the ABBV-969 candidate for the treatment of Metastatic Castration-Resistant Prostate Cancer (mCRPC).

- December 2024: Janux Therapeutics, Inc. announced clinical data for its JANX007 program. They utilized its proprietary Tumor Activated T Cell Engager (TRACTr) and Tumor Activated Immunomodulator (TRACIr) platforms and found substantial clinical activity with JANX007in 5L mCRPC patients.

- October 2024: Sanofi partnered with Orano Med, a leader in targeted alpha therapies for oncology, to leverage their combined expertise in combating rare cancers and to expedite the advancement of next-generation radioligand therapies.

- September 2024: Tolmar, Inc. collaborated with pharma and GmbH in which Tolmar promoted Rubraca (rucaparib) in the U.S. for the treatment of metastatic castration-resistant prostate cancer (mCRPC). Meanwhile, pharma& continued its promotion of Rubraca in the U.S. and Europe for the approved indications related to advanced ovarian cancer.

- December 2022: Novartis AG announced that the European Commission (EC) approved Pluvicto (lutetium (177Lu) vipivotide tetraxetan) in combination with Androgen Deprivation Therapy (ADT) as a targeted radioligand therapy to treat Metastatic Castration-Resistant Prostate Cancer (mCRPC).

REPORT COVERAGE

The global prostate cancer therapeutics market research report centers on providing an industry overview and examining the market dynamics. This includes market analysis, analyzing the drivers, restraints, opportunities, and trends influencing the market. Moreover, the report also presents data on the prevalence of prostate cancer in different countries/regions within the market. Additionally, it highlights key developments within the industry, conducts pipeline analysis, and discusses the launch of new products by major players with alternative treatment options for prostate cancer. Furthermore, the report delves into the impact of the COVID-19 pandemic on the industry and provides an overview of the market situation during this period.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 15.24% from 2026-2034 |

|

Segmentation |

By Drug Class

|

|

By Route of Administration

|

|

|

By Therapy

|

|

|

By Disease State

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 25.12 billion in 2025 and is projected to reach USD 106.86 billion by 2034.

In 2025, the North America market stood at USD 12.9 billion.

The market is expected to exhibit a CAGR of 15.24% during the forecast period (2026-2034).

Androgen receptor inhibitors dominate the market due to their effectiveness in blocking cancer growth by targeting androgen receptors.

North America region dominated the market in 2026.

Rising prostate cancer prevalence and increasing awareness programs are driving higher diagnosis rates and demand for advanced treatment options globally.

The key trend in this market is the rising shift of focus toward new therapies.

Pfizer Inc., Johnson & Johnson Services, Inc., and Astellas Pharma Inc. Ltd are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us