Railcar Unloader Market Size, Share & Industry Analysis, By Product Type (Rotary Car Dumpers, Railcar Tipplers, and Others), By Material Handling Mechanism (Mechanical Dumping Systems, Pneumatic Conveying Systems, and Hybrid Systems), By Material Type (Solid Material and Liquid Material), By End User Industry (Mining & metals, Power generation, Agriculture & food processing, and Others), and Regional Forecast, 2026-2034

Railcar Unloader Market Size and Future Outlook

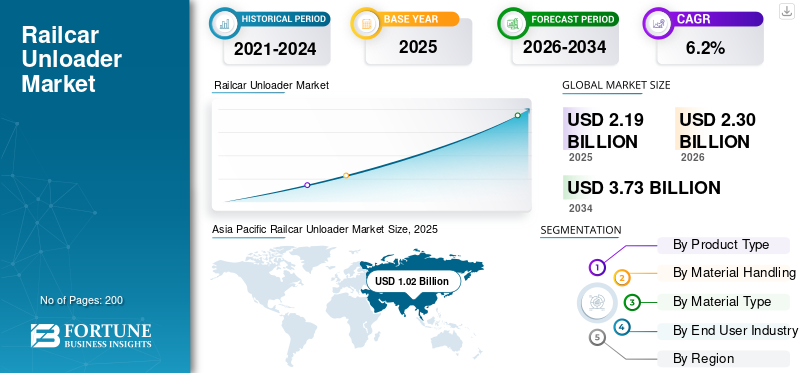

The global railcar unloader market size was valued at USD 2.19 billion in 2025. The market is projected to grow from USD 2.30 billion in 2026 to USD 3.73 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. Asia Pacific dominated the railcar unloader market with a market share of 46.58% in 2025.

The industry involves the design, manufacturing, installation, and servicing of equipment used to unload bulk materials from railcars. These systems handle commodities such as coal, grains, minerals, chemicals, cement, and fertilizers. Railcar unloaders improve operational efficiency, reduce manual labor, and enhance safety in ports, power plants, mining sites, and industrial facilities, supporting global bulk material handling and logistics operations.

Key drivers of the market include rising demand for efficient bulk material handling solutions, growing mining and power generation activities, expanding agricultural exports, and increasing industrialization. Demand for efficient material handling systems, automation adoption, improved safety standards, and infrastructure development in ports and rail networks further accelerate market growth.

Major players in the global railcar unloader market include Metso, FLSmidth, Process Controls Corporation, Thyssenkrupp Industrial Solutions, and BEUMER Group, competing through advanced bulk material handling technologies, automation integration, high-capacity systems, customized engineering solutions, and safety- and efficiency-focused innovations to strengthen their global presence.

Download Free sample to learn more about this report.

RAILCAR UNLOADER MARKET TRENDS

Growing Emphasis on Environmentally Compliant and Dust-Control Technologies is a Key Market Trend

Environmental sustainability and regulatory compliance are shaping design innovations in railcar unloading systems. Industries handling coal, cement, fertilizers, and other particulate materials face strict environmental norms related to dust emissions, spillage control, and noise levels. As a result, manufacturers are developing enclosed unloading systems, advanced dust suppression mechanisms, and energy-efficient equipment. Facilities are also incorporating covered conveyor systems and vacuum-based unloaders to minimize environmental impact. This trend aligns with broader corporate sustainability goals and regulatory requirements across North America, Europe, and parts of Asia Pacific. Demand for cleaner operations not only enhances workplace safety but also reduces environmental liabilities. Consequently, environmentally optimized unloading solutions are becoming a preferred choice in new infrastructure projects.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Bulk Commodity Trade and Industrial Output to Drive Unloading Equipment Demand

The steady growth in global trade of bulk commodities such as coal, iron ore, grains, cement, fertilizers, and chemicals is a primary driver of the market. Rapid industrialization in emerging economies and sustained demand from power generation, steel production, and agriculture sectors are increasing the volume of materials transported via rail. Rail remains a cost effective and efficient mode for long-distance bulk transportation, prompting higher utilization of rail networks. As cargo volumes rise, industries require faster, safer, and more efficient unloading systems to minimize turnaround time and reduce operational bottlenecks. Modern railcar unloaders enhance productivity, limit material loss, and support continuous operations, making them essential investments for ports, terminals, and processing facilities worldwide.

- For instance, In July 2025, Canadian National Railway released its 2025 - 2026 Grain Plan, forecasting 27.0 - 29.5 billion metric tons of grain and processed grain movement in the crop year, signaling sustained high-volume bulk flows that keep rail-linked terminals and processors focused on faster, higher-throughput unloading capacity.

MARKET RESTRAINTS

Volatility in Bulk Commodity Demand and Freight Patterns to Restrain Equipment Investments

Fluctuations in global demand for bulk commodities such as coal, iron ore, and agricultural products can significantly influence investment decisions in railcar unloading infrastructure. Commodity markets are highly sensitive to economic cycles, trade policies, energy transitions, and geopolitical developments. For instance, shifts toward renewable energy sources may reduce coal transportation volumes in certain regions, while trade restrictions can disrupt grain or mineral exports. Such uncertainty makes terminal operators and industrial facilities cautious about committing to large-scale capital expenditures for new unloading systems. When freight volumes decline or become unpredictable, capacity expansion projects are often postponed. This demand variability can limit consistent order inflows for manufacturers and slow the overall railcar unloader market growth.

MARKET OPPORTUNITIES

Automation and Smart Material Handling Integration to Create Growth Opportunities

The integration of automation, digital monitoring, and smart control systems presents significant growth opportunities. Industries are increasingly adopting automated unloaders solutions equipped with sensors, remote monitoring, and predictive maintenance capabilities to enhance efficiency and reduce labor dependency. Smart systems enable real-time performance tracking, optimized unloading cycles, and improved safety compliance. The shift toward Industry 4.0 practices across mining, ports, and manufacturing facilities supports demand for railcar unloaders. Furthermore, retrofitting existing unloaders with automation upgrades offers an additional revenue stream for manufacturers. As operators prioritize operational transparency, data-driven decision-making, and reduced downtime, suppliers offering intelligent, integrated unloading systems are well-positioned to capture new business opportunities.

MARKET CHALLENGES

Operational Complexity and Maintenance Requirements to Challenge Efficient Performance

Railcar unloading systems operate in demanding industrial environments, handling abrasive, heavy, or corrosive materials under continuous workloads. This exposes critical components to wear and tear, increasing the need for regular inspection, maintenance, and part replacement. Unplanned downtime can disrupt supply chains, delay production schedules, and increase operational costs for end users. Additionally, system integration with conveyors, storage silos, and unloading processes units requires technical expertise and precise coordination. Skilled labor shortages in certain regions further complicate maintenance and operational efficiency. While technological advancements aim to simplify operations, ensuring consistent system performance across varying material types and climatic conditions remains a significant challenge for operators.

Segmentation Analysis

By Product Type

High Throughput Efficiency and Heavy-Duty Handling to Strengthen Rotary Car Dumpers Leadership

Based on product type, the market is rotary car dumpers, railcar tipplers, and others.

The rotary car dumpers segment dominates the market due to its ability to handle high-capacity bulk materials efficiently and continuously. Widely deployed in mining, coal-fired power plants, ports, and steel production facilities, these systems enable rapid unloading with minimal manual intervention. Their suitability for unit trains and large-scale operations ensures reduced turnaround time and optimized material flow. Established infrastructure across major commodity-exporting regions further reinforces replacement demand and system upgrades, sustaining segmental dominance.

The railcar tipplers segment is projected to grow at a CAGR of 7.0% over the forecast period, driven by rising demand for flexible and cost-effective unloading solutions. Their suitability for medium-capacity operations and compatibility with varied railcar designs support increasing adoption across emerging industrial and port facilities.

By Material Handling Mechanism

Robust Load Handling and High Operational Reliability to Drive Mechanical Dumping Systems Dominance

In terms of material handling mechanism, the market is categorized into mechanical dumping systems, pneumatic conveying systems, and hybrid systems.

The mechanical dumping systems segment dominates with the largest railcar unloader market share owing to its strong load-bearing capacity, operational durability, and suitability for heavy bulk commodities such as coal, iron ore, and aggregates. These systems are widely adopted across mining, ports, and power generation facilities where high-volume, continuous unloading is required. Their proven performance, lower operational complexity compared to advanced systems, and long service life encourage repeat installations and refurbishment projects. Established infrastructure in mature industrial regions further sustains steady demand, reinforcing segmental leadership across large-scale bulk handling operations.

The pneumatic conveying systems segment is projected to expand at a CAGR of 7.1% during the forecast period, driven by increasing demand for enclosed, dust-free material transfer. Growing environmental regulations and the need for cleaner handling of cement, chemicals, and fine powders support accelerated adoption across industrial facilities.

To know how our report can help streamline your business, Speak to Analyst

By Material Type

Extensive Bulk Commodity Transportation to Reinforce Solid Material Segment Dominance

Based on material type, the market is segmented into solid material and liquid material.

The solid material segment dominates the market due to the substantial volume of bulk solids transported globally, including coal, iron ore, grains, cement, aggregates, and fertilizers. Rail remains a primary mode for long-distance movement of these commodities, particularly across mining, agriculture, construction, and power generation sectors. Unloading solid materials requires heavy-duty mechanical systems such as rotary dumpers and tipplers, ensuring consistent equipment demand. Large-scale industrial infrastructure and established rail freight corridors further support recurring upgrades, maintenance contracts, and capacity expansions, solidifying the segment’s market share across both developed and emerging economies.

The liquid material segment is projected to grow at a CAGR of 8.2% over the forecast period, driven by increasing rail transport of petroleum products, chemicals, and industrial liquids. Rising safety regulations and demand for efficient tank car unloading systems are accelerating infrastructure investments.

By End User Industry

High Bulk Ore Transportation Volumes to Strengthen Mining & Metals Segment’s Dominance

Based on end user industry, the market is segmented into mining & metals, power generation, agriculture & food processing, and others.

The mining & metals segment dominates the market due to the massive volumes of iron ore, coal, bauxite, and other minerals transported via rail to processing plants and export terminals. Large-scale mining operations depend on high-capacity, continuous unloading systems such as rotary dumpers and heavy-duty mechanical solutions to maintain productivity and reduce turnaround times. Established rail-linked mining corridors across Australia, North America, Latin America, and parts of Asia further sustain equipment demand. Ongoing capacity expansions, modernization of bulk terminals, and replacement of aging unloading infrastructure reinforce the segment’s leading market share globally.

The agriculture & food processing segment is projected to expand at a CAGR of 7.5% during the forecast period, supported by increasing global grain trade and fertilizer movement. Growing demand for efficient, contamination-free bulk handling systems is driving investments in modern railcar unloading infrastructure.

Railcar Unloader Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Railcar Unloader Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is projected to register the fastest CAGR during the forecast period. Strong mining output in Australia, expanding steel production in China and India, and rising bulk commodity trade across Southeast Asia drive high-capacity rail infrastructure demand. Rapid industrialization, port modernization projects, and government investments in freight corridors further accelerate installations. Growing energy demand and agricultural exports also support sustained procurement of advanced unloading systems across the region.

China Railcar Unloader Market

In 2026, China is estimated to achieve around USD 0.59 billion, accounting for a significant share of the global market revenues. Strong mining output, steel production, and port infrastructure expansion continue driving high-capacity rotary dumper installations and bulk terminal modernization projects.

India Railcar Unloader Market

The Indian market is projected to hit USD 0.14 billion in 2026, accounting for a growing share of global revenues. Dedicated freight corridors, rising coal transportation, and expanding fertilizer and cement logistics support new unloading infrastructure investments.

North America

North America holds the second-largest market share and is expected to grow at a CAGR of 5.7%. The region benefits from established rail freight networks and significant bulk transportation of coal, grains, chemicals, and aggregates. Replacement of aging unloading infrastructure and modernization of mining and port facilities drive steady equipment demand. Additionally, technological upgrades, including automation and safety enhancements, support continued investments across the U.S. and Canada.

U.S. Railcar Unloader Market

The U.S. will reach around USD 0.35 billion in 2026 driven by replacement of aging infrastructure, grain exports, and mining logistics modernization sustain steady demand for automated unloading systems.

Europe

Europe represents the third-largest market, supported by well-developed rail logistics and industrial infrastructure. Demand is driven by cross-border bulk trade, agricultural exports, and metals processing activities. Strict environmental regulations encourage adoption of enclosed and dust-controlled unloading systems. Infrastructure refurbishment projects and the shift toward energy-efficient material handling technologies further support stable market growth across Germany, France, and Eastern Europe.

Germany Railcar Unloader Market

The German market in 2026 is estimated at around USD 0.12 billion, accounting for a moderate share of global revenues. Cross-border bulk trade, industrial material handling upgrades, and environmental compliance requirements drive adoption of enclosed and efficient unloading systems.

U.K. Railcar Unloader Market

The U.K. is projected to acquire USD 0.08 billion in 2026, accounting for a smaller share of global revenues. Port redevelopment initiatives, aggregates transport, and infrastructure renewal projects support gradual adoption of advanced railcar unloading technologies.

Rest of the World

The rest of the world, including Latin America and the Middle East & Africa, is witnessing gradual market expansion driven by mining investments and port development projects. Brazil, South Africa, and Saudi Arabia are strengthening rail connectivity to support mineral exports and industrial diversification. Although infrastructure gaps remain, increasing foreign direct investment and commodity trade activities are expected to create steady opportunities for railcar unloading system providers.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Customized Engineering Strengthening Market Competition

The market is characterized by the presence of established bulk material handling equipment manufacturers competing on technological capability, system reliability, and project execution expertise. Leading players such as Metso, FLSmidth, TAKRAF Group, Thyssenkrupp Industrial Solutions, and BEUMER Group focus on delivering high-capacity rotary dumpers, wagon tipplers, and integrated conveying systems tailored to mining, ports, and power generation facilities. Companies emphasize engineered-to-order solutions, ensuring compatibility with site-specific rail configurations and material characteristics, strengthening long-term client relationships and repeat contracts.

Competition is further shaped by advancements in automation, digital monitoring, and environmentally compliant unloading technologies. Market participants are investing in predictive maintenance tools, dust suppression systems, and energy-efficient designs to differentiate their offerings. Strategic partnerships, service agreements, and lifecycle support contracts enhance recurring revenue streams and customer retention. Additionally, regional expansion into emerging mining and export hubs enables companies to secure infrastructure-linked projects. Strong aftersales service networks and the ability to manage complex, large-scale installations remain critical competitive differentiators.

LIST OF KEY RAILCAR UNLOADER MARKET COMPANIES PROFILED

- Thyssenkrupp AG (Germany)

- Dover Corporation (DoverMEI) (U.S.)

- Coperion GmbH (Germany)

- Martin Engineering (U.S.)

- Kinergy Group (U.S.)

- Vortex Global Limited (U.K.)

- Bruks Siwertell (Sweden)

- NPK Construction Equipment Inc. (U.S.)

- Airmatic Inc. (U.S.)

- BEUMER Group (Germany)

- Cambelt International Corporation (U.S.)

- Telestack Ltd. (Ireland)

- AUMUND Fördererbau GmbH (Germany)

- Metso Outotec Corporation (Finland)

- Process Controls Corporation (U.S.)

- FLSmidth (Denmark)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Metso advanced smart bulk material handling solutions by integrating MRA Automation’s technologies into its global offerings, enhancing digital control for railcar dumpers and unloaders.

- February 2026: Bruks Siwertell launched a next-generation Siwertell road-mobile ship unloader featuring advanced control systems to optimize performance, safety, and operation across dry bulk handling sites.

- January 2026: BEUMER Group inaugurated a state-of-the-art manufacturing facility in Taicang, China, expanding global production capacity to support material handling and automation solutions.

- January 2026: Thyssenkrupp confirmed robust EBIT and maintained full-year forecasts amid portfolio transformation, underscoring continued strategic focus on industrial solutions that include material handling infrastructure.

- December 2025: Fluor’s Virta subsidiary acquired FLSmidth’s Overland Conveyor Products Group, transferring IP, technology, and personnel, signaling strategic portfolio reshaping in bulk material handling sectors including rail freight infrastructure.

- September 2025: Metso secured a USD 18 million order to replace aging railcar dumper cells for a mining customer in Pilbara, Australia, including design, supply, and installation to enhance safety, reliability, and maintainability in bulk handling operations.

- October 2024: Metso confirmed a USD 12 million contract to deliver an upgraded railcar dumper with enhanced efficiency and reduced spillage for a mining customer in the Asia Pacific region.

REPORT COVERAGE

The global railcar unloader market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Material Handling Mechanism, Material Type, Material, End User Industry, and Region |

| By Product Type |

|

| By Material Handling Mechanism |

|

| By Material Type |

|

| By End User Industry |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.19 billion in 2025 and is projected to reach USD 3.73 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 1.02 billion.

The market is expected to exhibit a CAGR of 6.2% during the forecast period.

The rotary car dumpers segment led the market.

Rising bulk commodity trade and industrial output drive unloading equipment demand.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us