Railway Braking System Market Size, Share & Industry Analysis, By Vehicle Type (Freight Cars, Locomotives, Passenger Coaches, Transit Cars), By Brake Type (Air Brakes (Pneumatic), Electro-pneumatic Brakes (EPB), Regenerative/Dynamic Braking, Vacuum Brakes), By Component (Brake Control & Actuation, Energy Supply & Transmission, Friction & Wear Parts, Wheel/Rail, Interface & Safety Add-ons, Parking & Auxiliary Systems, Monitoring & Diagnostics), By Offering (Complete Braking Systems (OEM Installation), Brake Components & Spares (Aftermarket)), and Regional Forecast, 2026-2034

Railway Braking System Market Size and Future Outlook

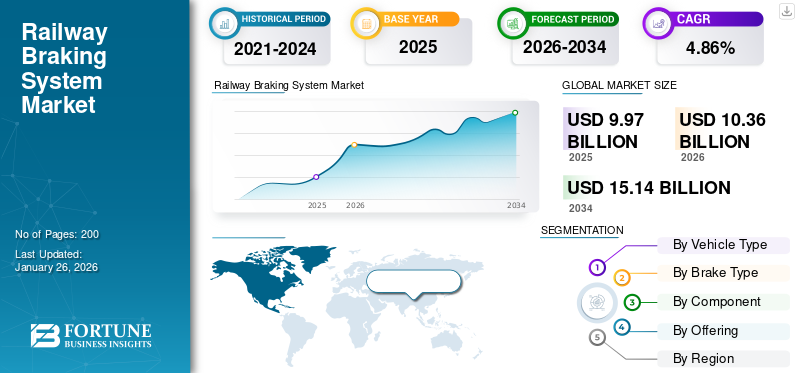

The global railway braking system market size was valued at USD 9.97 billion in 2025 and is projected to grow from USD 10.36 billion in 2026 to USD 15.14 billion by 2034, exhibiting a CAGR of 4.86% during the forecast period. Asia Pacific dominated the railway braking system market with a market share of 54.32% in 2025.

The railway braking system encompasses technologies and components that enable safe deceleration and stopping of trains, ensuring passenger safety and operational efficiency. Braking systems include pneumatic, hydraulic, mechanical brake, and advanced electronic controls, tailored for high-speed rail, freight, metros, and light rail networks. Market growth is driven by rising investments in rail infrastructure, stricter safety regulations, and increasing adoption of high-speed and urban transit systems. Advancements in electropneumatic, electromagnetic brakes, and regenerative braking, along with the use of digital monitoring systems, lightweight materials, and predictive maintenance, further support demand and enhance performance across global railway operations.

Key players in the railway braking system market include Knorr-Bremse AG, Wabtec Corporation, Faiveley Transport (a Wabtec company), CRRC Corporation Limited, and Hitachi Rail. These companies focus on developing advanced braking technologies such as electropneumatic and regenerative systems to improve safety, energy efficiency, and performance. Strategic investments in R&D, global service networks, and regional manufacturing facilities enhance their market presence. Collaborations with rail operators, innovations in digital monitoring and predictive maintenance, and sustainability-driven solutions further strengthen their role in shaping the global market landscape.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Expanding Rail Infrastructure and Regulatory Compliance Propel Market Demand

Rising investments in rail infrastructure, including high speed rail, metro projects, and dedicated freight corridors, significantly boost demand for advanced braking systems. These large-scale projects require braking solutions that ensure efficiency, reliability, and passenger safety under varying operational conditions. At the same time, stringent safety regulations from international and regional authorities mandate the adoption of cutting-edge technologies such as electropneumatic, electromagnetic brakes, and regenerative braking/electrodynamic brakes. Compliance with these norms compels operators and manufacturers to integrate innovative, high-performance braking systems. Together, infrastructure expansion and regulatory enforcement act as the strongest drivers, accelerating global market growth while fostering innovation and modernization in railway braking technology. In June 2025, Railways announced expansion of the Kavach automatic braking/ collision‐avoidance system across another 3,100 km in the South Central Railway zone; it intervenes by triggering train braking if signal or speed compliance fails.

MARKET RESTRAINTS:

High Initial Investment and Maintenance Costs Restrain Market Growth

The market faces a major restraint due to the high initial investment and ongoing maintenance costs associated with advanced technologies. Systems such as electronically controlled pneumatic ecp braking and regenerative braking require substantial capital for development, installation, and integration into new or existing rolling stock. Furthermore, their operation and upkeep demand specialized tools, replacement parts, and highly skilled technicians, increasing lifecycle costs. For cost-sensitive operators and emerging economies, these expenses pose significant barriers, often delaying modernization projects despite recognized safety and efficiency benefits. Consequently, high costs remain the most critical factor restraining the broader adoption of advanced braking solutions globally. In October 2024, Alstom reported that maintaining brake systems consumes about 15% of overall train maintenance costs, driven by expensive components from a few suppliers.

MARKET OPPORTUNITIES:

Digitalization and Smart Braking Solutions Unlock New Value

The growing adoption of digital technologies creates a major opportunity in the railway braking system market. Integration of IoT, sensors, and AI into braking solutions enables real-time monitoring, predictive maintenance, and data-driven decision-making. These innovations enhance safety, reduce downtime, and lower operating costs, making them highly attractive to rail operators. Smart braking systems also align with broader industry trends toward automation and connected mobility. For OEMs and technology providers, offering digitalized solutions not only strengthens customer relationships through service-based models but also opens recurring revenue streams, positioning digitalization as one of the most lucrative future opportunities. In September 2024, Knorr-Bremse showcased advanced digital-electropneumatic (brake-by-air) and digital-electromechanical (brake-by-wire) braking systems at InnoTrans, aiming to boost rail traffic capacity, shorten braking distances, and improve system availability.

RAILWAY BRAKING SYSTEM MARKET TRENDS:

Sustainability and Regenerative Braking Shape Future Market

Sustainability is emerging as a defining railway brake system market trend in the railway braking system market. With global emphasis on reducing carbon emissions and improving energy efficiency, operators are increasingly adopting regenerative braking systems. These systems recover kinetic energy during deceleration and feed it back into the train’s power system or grid, reducing energy consumption and operating costs. Coupled with lightweight materials and eco-friendly designs, regenerative braking supports both environmental goals and cost savings. As governments and operators prioritize green mobility, the integration of sustainable technologies will dominate product development, shaping the future direction of the global braking system market in the railway industry. In December 2024, Barcelona launched its MetroCharge system: capturing regenerative braking energy from subway trains to power stations and charging EVs. Sixteen metro stations now feed excess braking energy via cables to street-level electric car chargers.

MARKET CHALLENGES:

Supply Chain Disruptions and Rising Raw Material Costs Pressure Manufacturers

The market faces challenges from supply chain disruptions and rising raw material costs. Components such as advanced alloys, composites, sensors, and semiconductors are critical for modern braking systems. Volatility in raw material prices, combined with geopolitical tensions, trade restrictions, and pandemic-related supply shortages, increases production costs and delays deliveries. These disruptions affect the timely execution of large-scale rail projects and strain profitability. Manufacturers are compelled to optimize sourcing strategies, diversify suppliers, and invest in local production, yet uncertainties in global supply networks remain a persistent challenge to stable market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

Rising Urbanization and Metro Network Expansion Drive Transit Cars Segment Growth

On the basis of the segmentation of vehicle type, the market is classified into freight cars, locomotives, passenger coaches, and transit cars.

Transit cars will dominate the market and will be the fastest-growing segment, driven by rapid urbanization and rising investments in metro and suburban rail networks, accounting for a 34.47% market share in 2026. Governments prioritize mass transit solutions to reduce congestion and emissions, driving demand for reliable braking systems. Frequent stop-and-go operations in dense cities require highly efficient, low-maintenance brakes. The growth of smart city initiatives and expanding commuter populations ensures transit cars remain the leading segment in the market. In September 2025, Mumbai Railway Vikas Corporation floated a USD 2.36 billion (INR 21,000 Crore) tender for 2,856 Vande Metro suburban coaches with long-term maintenance contracts.

By Brake Type

Proven Reliability and Cost-Effectiveness Drive Air Brake Adoption

In terms of brake type, the market is categorized into air brakes (pneumatic), electro-pneumatic brakes (EPB), regenerative/dynamic braking, and vacuum brakes.

Air brakes (pneumatic) will dominate the market due to their long-standing reliability, simplicity, and cost-effectiveness, accounting for a 57.06% market share in 2026. Widely used across freight trains and passenger trains, they provide robust performance under diverse operating conditions. Their established infrastructure, ease of maintenance, and compliance with safety standards make them the preferred choice for many operators. Especially in freight-heavy regions, pneumatic air brakes remain critical, driving sustained demand within the braking technology segment despite advances in electronic alternatives.

In January 2025, Progress Rail introduced the upgraded CCBIIe system that supports remote diagnostics and self-testing for air-brake maintenance. While the air brake segment owns the largest railway braking system market share, the adoption of regenerative/dynamic braking is growing fast due to energy efficiency, sustainability mandates, electrification, and reduced operational costs.

To know how our report can help streamline your business, Speak to Analyst

By Component

Focus on Crashworthiness and Adhesion Control Enhances Demand for Wheel/Rail Interface Components

Based on component, the market is bifurcated into brake control & actuation, energy supply & transmission, friction & wear parts, wheel/rail interface & safety add-ons, parking & auxiliary systems, and monitoring & diagnostics.

Wheel/rail interface and safety add-ons will dominate the market, as they will be critical for ensuring braking efficiency, minimizing slippage, and enhancing passenger safety. Components such as sanders, adhesion control systems, and monitoring devices will help optimize braking performance under varying track conditions, accounting for a 47.50% market share in 2026. Growing focus on crashworthiness, reliability, and compliance with international safety standards fuels demand. With operators prioritizing accident prevention and performance stability, this segment leads as a fundamental enabler of safe, efficient braking operations.

In September 2025, ENSCO presented research on a strain gauge-based system that monitors wheel loads and rail-tie forces to detect degraded track support and improve safety. The monitoring & diagnostics segment is expected to grow at the fastest CAGR over the railway braking system market forecast period. The growth of the segmental market is driven by predictive maintenance, digitalization, IoT adoption, and regulatory safety compliance.

By Offering

Long Service Lifespan of Rolling Stock Sustains Aftermarket Demand for Braking Solutions

Based on offering, the market is segmented into complete braking systems (OEM installation) and brake components & spares (aftermarket). The brake components & spares (aftermarket) are further divided into brake pads/brake shoes, brake discs/wheels, brake cylinders, compressors & reservoirs, control valves, electronics, sensors, and couplers & linkages.

The aftermarket will dominate the market and will be the fastest-growing segment due to the long operational lifespan of rolling stock, which will drive continuous demand for replacement parts, maintenance, and upgrades, accounting for an 86.12% market share in 2026. Brake pads, discs, cylinders, and digital retrofit kits require regular servicing to ensure safety and compliance. Operators rely on aftermarket services for predictive maintenance and performance optimization. This consistent need for upkeep and modernization makes aftermarket solutions the largest contributor to revenue within the market. In September 2025, Kazakhstan’s national railway (KTZ) placed a USD 4.2 billion order with Wabtec that includes service support and likely long-term parts/maintenance contracts.

Railway Braking System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific Railway Braking System Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

ASIA PACIFIC

The Asia Pacific market was valued at USD 5.42 billion in 2025, capturing 54.32% of global revenue, and is estimated to reach USD 5.65 billion in 2026. High-speed rail expansion, metro projects, and rising passenger volumes drive demand for advanced braking solutions. Government initiatives promoting sustainable transport and urban mobility accelerate the adoption of regenerative and electropneumatic brakes. Rapid urbanization, economic growth, and rising freight requirements position the Asia Pacific as the fastest-growing region, offering significant opportunities for OEMs and suppliers to expand market share.The Japan market is projected to reach USD 1.23 Billion by 2026, the China market is projected to reach USD 2.75 Billion by 2026, and the India market is projected to reach USD 0.78 Billion by 2026.

In July 2025, China unveiled its next-generation high-speed train CR450, with trials targeting commercial operation at 400 km/h, pushing braking and aerodynamic performance boundaries

NORTH AMERICA

North America contributed 11.85% to the global market in 2025, with a valuation of USD 1.18 billion, and is projected to reach USD 1.21 billion in 2026. In North America, market growth is driven by the modernization of aging rail infrastructure, the adoption of advanced freight corridors, and regulatory emphasis on safety compliance by agencies such as the FRA. Expanding urban transit networks, particularly metro and light rail projects, create demand for reliable, digitally enabled braking solutions. Investment in predictive maintenance and smart braking technologies further supports regional dominance, ensuring operational efficiency and safety across passenger and freight segments.

The U.S. dominates the regional demand of North America with large-scale freight operations and strong investment in commuter rail upgrades. Federal initiatives to improve safety standards and reduce carbon emissions drive the adoption of regenerative and electro-pneumatic braking systems. Expansion of Amtrak’s high-speed corridors and urban rail projects further fuels growth. The U.S. market also benefits from technology integration, including IoT-based monitoring, enhancing operational reliability and efficiency, making it a leading market for braking system adoption. In August 2025, Amtrak launched its NextGen Acela high-speed train service on the Northeast Corridor. The U.S. market is projected to reach USD 0.94 Billion by 2026.

EUROPE

Europe accounted for USD 3.08 billion in 2025, representing 30.91% of the global market share, and is projected to reach USD 3.2 billion in 2026. Europe’s railway braking system market growth is driven by extensive high-speed rail networks, strong sustainability mandates, and strict safety standards set by the ERA. Countries such as Germany, France, and the U.K. prioritize green mobility, fostering the adoption of regenerative braking technologies. Ongoing cross-border rail integration and European Union funded infrastructure programs boost demand. Advanced digital systems and lightweight materials are widely deployed, ensuring Europe remains a technological leader and a mature, innovation-driven market for railway braking systems. Alstom's Avelia Stream Nordic X80, introduced in July 2025, is designed for high-speed travel in Nordic conditions. It features regenerative braking systems that contribute to energy efficiency and a 37% reduction in carbon footprint compared to previous models. The train is also equipped with the European Train Control System (ETCS) for enhanced safety. The UK market is projected to reach USD 0.34 Billion by 2026, while the Germany market is projected to reach USD 0.64 Billion by 2026.

REST OF THE WORLD

In regions such as the Middle East, Africa, and South America, the market is driven by growing investments in new rail infrastructure to support urbanization, economic diversification, and freight connectivity. The Rest of the World region captured 2.91% of the global market in 2025, generating USD 0.29 billion in revenue, and is projected to reach USD 0.3 billion in 2026. Projects such as GCC railway links and Latin American metro expansions boost demand for modern braking systems. Although adoption is slower compared to developed regions, increasing government funding, international partnerships, and sustainability-focused initiatives create emerging opportunities for suppliers in these developing markets. In July 2025, Alstom delivered its first trainset for São Paulo’s Metro Line 6-Orange, featuring regenerative braking technology to enhance energy efficiency and sustainability.

COMPETITIVE LANDSCAPE

Key Industry Players:

Digitalization, Predictive Maintenance, and Regenerative Braking Strengthen Market Leadership

The railway braking system market is highly competitive, led by global players such as Knorr-Bremse, Wabtec Corporation, Faiveley Transport, CRRC, and Hitachi Rail. Companies focus on R&D, regional manufacturing, and digital innovations to enhance safety and efficiency. Strategic collaborations with rail operators, investments in predictive maintenance solutions, and sustainability-driven technologies such as regenerative braking strengthen their positions. Intense competition fosters continuous innovation, ensuring reliable, compliant, and energy-efficient braking solutions globally.

LIST OF KEY RAILWAY BRAKING SYSTEM COMPANIES PROFILED:

- Knorr-Bremse AG (Germany)

- Wabtec Corporation (U.S.)

- Alstom (France)

- Siemens Mobility GmbH (Germany)

- CRRC Corporation Limited (China)

- Stadler Rail AG (Switzerland)

- Hyundai Rotem Company (South Korea)

- Dako-CZ, a.s. (Czech Republic)

- Akebono Brake Industry Co Ltd (Japan)

- Nabtesco Corporation (Japan)

- Jupiter Wagons (India)

- Greysham International (India)

- Amsted Rail (U.S.)

- Kirloskar Pneumatic (India)

- Sundaram Brake Linings Ltd. (India)

- Siemens Mobility (Germany)

- YUJIN Machinery Ltd. (South Korea)

- Verkko Global (India)

KEY INDUSTRY DEVELOPMENTS:

- In July 2025, Bhopal Metro completed oscillation and emergency braking trials for new rolling stock. Successful tests validated safety, stability, and braking efficiency, paving the way for certification and commercial operations, supporting India’s expanding metro infrastructure and urban mobility.

- In June 2025, Siemens announced the Charger B+AC battery-electric locomotive launch for U.S. passenger service. The design integrates regenerative braking and digital controls, supporting decarbonization goals and strengthening the adoption of eco-friendly braking technologies in the North American railway sector.

- In June 2024, Wabtec launched Green Friction braking materials on Paris’s RER A line. These advanced linings reduce particulate emissions, enhance sustainability, and improve braking performance, reinforcing global efforts toward eco-friendly, reliable, and regulation-compliant railway braking solutions.

- In May 2024, Knorr-Bremse signed a long-term service contract with Stadler to overhaul braking systems across European fleets. Covering 20,000 brake calipers, the agreement runs until 2028, underscoring the importance of aftermarket and lifecycle services in stable revenue growth.

- In January 2024, Wabtec was awarded a USD 157 million brake system contract from Siemens India for a 9,000 HP locomotive project for Indian Railways. The deal covers supplying brake systems (from Wabtec’s Hosur plant) plus 35 years of maintenance.

- In September 2023, Knorr-Bremse launched its next-generation CubeControl brake platform, integrating electropneumatic, mechatronic, and software functions. Alstom selected the system for Sweden’s high-speed trains, with deliveries from 2024–2028, aiming for efficiency, lower maintenance costs, and enhanced digital readiness in rail braking technology.

REPORT COVERAGE

The global railway braking system market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.86% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, By Brake Type, By Component, By Offering, and Region |

| By Vehicle Type |

|

| By Brake Type |

|

| By Component |

|

| By Offering |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.97 billion in 2025 and is projected to reach USD 15.14 billion by 2034.

In 2025, the market value stood at USD 5.42 billion.

The market is expected to exhibit a CAGR of 4.86% during the forecast period of 2026-2034.

The aftermarket segment led the market by offering.

Rail infrastructure investments and safety regulations fuel market growth.

Leading companies such as Knorr-Bremse, Wabtec Corporation, Faiveley Transport, CRRC, and Hitachi Rail dominate the market.

Asia Pacific dominated the railway braking system market with a market share of 54.32% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us