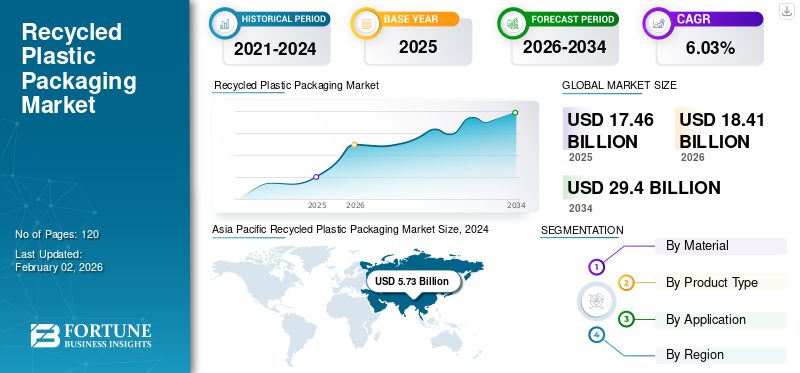

The global recycled plastic packaging market size was valued at USD 17.46 billion in 2025 and is projected to grow from USD 18.41 billion in 2026 to USD 29.40 billion by 2034, registering a CAGR of 6.03% over the forecast period. Asia Pacific dominated the recycled plastic packaging market with a market share of 34.46% in 2024.

Recycled Plastic Packaging Market Size, Share & Industry Analysis, By Material (Polyethylene (PE), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET), Polypropylene (PP), Polystyrene (PS), and Others), By Product Type (Bottles, Bags & Pouches, Wraps & Liners, Jars & Containers, and Others), By Application (Food & Beverages, Healthcare, Electronics, Cosmetics & Personal Care, Homecare, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

Recycled plastic packaging (RPET or recycled polyethylene terephthalate) is made from repurposed plastic waste. It provides various environmental advantages by minimizing waste, preserving resources, and lowering energy usage in the production process. Using recycled plastic prevents plastic waste from ending up in landfills or polluting the environment. Recycled plastic production generates fewer CO2 emissions compared to virgin plastic production. It promotes environmental awareness and encourages sustainable choices among consumers, and rising environmental concerns thus drive the market growth.

Amcor Plc and Berry Global Inc. are the leading manufacturers, accounting for the largest global market share.

Download Free sample to learn more about this report.

GLOBAL RECYCLED PLASTIC PACKAGING MARKET TAKEAWAYS

Market Size & Forecast:

- 2025 Market Size: USD 17.46 billion

- 2026 Market Size: USD 18.41 billion

- 2034 Forecast Market Size: USD 29.40 billion

- CAGR: 6.03% from 2026–2034

Market Share:

- Asia Pacific led in 2024 with a 34.46% share, rising from USD 5.38 billion in 2023 to USD 5.73 billion in 2024.

- By material: Polyethylene terephthalate (PET) dominated due to its high recyclability and use in food and beverage packaging.

- By product type: Bottles held the largest share owing to their high recycling rate and sustainability focus.

- By application: Food & beverages led the market, driven by increasing demand for eco-friendly packaging solutions.

Key Country Highlights:

- China: Major contributor with large recycling capacity and government-driven sustainability initiatives.

- India: Expanding infrastructure for plastic recycling supporting circular economy goals.

- U.S.: Advanced waste management systems and rising adoption in food and personal care packaging.

- Germany: Strong focus on sustainable packaging under EU circular economy regulations.

- Australia: Government investment in recycling facilities boosting local production.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Government Initiatives & Efforts to Reduce Plastic Waste and Drive Market Expansion

Plastic significantly contributes to ocean pollution, with approximately 14 million tons entering the water each year. Single-use plastics such as bags, straws, and disposable utensils are a major factor in this pollution. Some plastics contain harmful chemicals that can leach into the water and contaminate marine life, potentially leading to long-term health issues. These detrimental environmental impacts have prompted initiatives focused on recycling plastic. Various companies are minimizing the use of plastic packaging in their operations, which is anticipated to drive recycled plastic packaging market growth in the coming years. UNESCO reports that nearly 100,000 marine mammals and one million seabirds lose their lives each year due to plastic waste in the ocean.

- The European Union's approach to plastics within a circular economy suggests that by 2030, every plastic packaging introduced to the European Union market must be either reusable or recyclable. These regulatory measures encourage producers to use recycled plastics in their packaging options, which in turn enhances market expansion.

MARKET RESTRAINTS

Contamination & Quality-Related Issues in Recycled Plastics Hampers Market Expansion

A major factor hampering the market for recycled plastic packaging is the challenge of contamination and the resulting quality of the recycled materials. Recycled plastics frequently contain residues from their previous applications, such as food, chemicals, or other substances, which can undermine the safety and integrity of the recycled packaging. This is especially troubling in sectors including food and beverages and healthcare, where the safety of packaging is vital. The inconsistency in the quality of recycled plastics can result in variable product characteristics, impacting the performance and appearance of the packaging.

MARKET OPPORTUNITIES

Rising Environmental Concerns & Government Investments Generate Growth Opportunities

As consumers, businesses, and governments become more conscious of environmental issues, there has been a dramatic increase in the demand for sustainable packaging options. This global shift toward sustainability is primarily driven by worries about plastic waste, climate change, and the overall effects of packaging waste on the environment. Funding from both public agencies and private companies is crucial in driving advancements in recycling technologies and sustainable packaging. These investments aim to enhance recycling effectiveness, improve the quality of recycled materials, and develop innovative packaging solutions. It thus offers potential growth opportunities to the global market.

- In July 2024, the Australian Government committed approximately USD 13.5 million to set up a soft plastics recycling center in Kilburn, South Australia. Led by Recycling Plastics Australia, this initiative aims to prevent more than 14,000 tons of soft plastics from ending up in landfills each year. The facility will utilize mechanical recycling technology to transform materials such as shopping bags, chip packets, and food wrappers into new feedstock for packaging.

RECYCLED PLASTIC PACKAGING MARKET TRENDS

Increased Demand for Post-Consumer Recycled Materials Emerges as a Key Trend

The recycled plastic packaging market is experiencing a shift toward a greater reliance on post-consumer recycled (PCR) materials, influenced by consumer preferences for eco-friendly options and regulatory requirements. This process includes utilizing materials retrieved from discarded items, which are then cleaned, processed, and used in the creation of new packaging. Companies are actively incorporating PCR content into their packaging to reduce reliance on virgin plastics and promote a circular economy. The concept of a circular economy, which emphasizes reuse and repurposing of materials, is gaining traction as a cornerstone of sustainable packaging strategies. The increased use of post-consumer recycled (PCR) materials across various industries, driven by a desire for sustainability and a circular economy, is thus emerging as a key market trend. Asia Pacific witnessed a Recycled Plastic Packaging Market growth from USD 5.38 billion in 2023 to USD 5.73 billion in 2024.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Potential Benefits Offered by Polyethylene Terephthalate (PET) Boosted Segmental Growth

Based on material, the market is divided into polyethylene (PE), polyvinyl chloride (PVC), polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS), and others.

The Polyethylene terephthalate (PET) segment accounted for the largest recycled plastic packaging market share in 2024. This type of plastic is among the most frequently recycled plastics due to its excellent clarity and durability. PES can be additionally transformed into fibers for use in clothing, carpets, insulation, and new containers for food and beverages. This characteristic not only makes it appealing but also recyclable, making it an attractive option for sustainable production in both the textile and packaging sectors.

The Polyethylene (PE) segment will continue to account for a considerably larger share of the market. The material is dense and heavy, ensuring that the use of materials meets standards for structural strength, thus serving as a dependable source for recycled goods.

By Product Type

Bottles Led Market Due to Their Increasing Demand from Several End-use Industries

Based on product type, the market is divided into bottles, bags & pouches, wraps & liners, jars & containers, and others.

Bottles accounted for the larger share of the market in 2024. A rapid increase in efforts to decrease plastic waste is driving the demand for recycled plastic bottles. The increased use of PET bottles has raised worries about environmental contamination. To tackle this problem, the adoption of recycled plastic bottles is becoming more popular across different sectors. Utilizing these bottles contributes to minimizing the spread of plastic waste in the environment.

Bags and pouches will continue to account for a considerably larger share of the market. Recycled plastic bags and pouches offer several benefits, mainly focusing on environmental sustainability and potential cost savings. They reduce waste, conserve natural resources, and can be more cost-effective in the long run, specifically when considering regulations regarding single-use plastics.

By Application

Increasing Need for Sustainable Packaging Options in Food & Beverage Sector Contributed to Segmental Growth

Based on the application, the market is segmented into food & beverages, healthcare, electronics, cosmetics & personal care, homecare, and others.

The food and beverages segment dominated the market in 2024. The rapidly growing food and beverage industry presents a significant opportunity for the market. As global food consumption increases, companies are seeking sustainable packaging options to address consumer demands and meet environmental goals. Recycled plastic packages, known for their eco-friendly image and lower carbon footprint, are ideally suited to fulfil this need. Numerous food companies are transitioning to recycled plastic materials to demonstrate their commitment to sustainability and reduce their dependence on new plastic sources.

On the other hand, the electronics segment is expected to witness steady growth during the forecast period. Electronics manufacturers are progressively embracing the principles of a circular economy to reduce waste and enhance the recycling processes of materials. The use of recyclable packaging is vital in reaching these objectives by including post-consumer recycled materials in product packaging.

Recycled Plastic Packaging Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Recycled Plastic Packaging Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market. The massive growth in plastic recycling capacities is boosting the market growth in the region. As the global push for a circular economy accelerates, awareness of the need to tackle waste management in Asia is gaining momentum. China's initiatives in recycling plastic waste have played a crucial role in combating climate change by lowering crude oil usage and averting millions of metric tons of carbon emissions.

- ICIS states that mechanical recycling has a strong presence in Asia, especially in Northeast Asia and the Indian subcontinent. The current capacity for mechanical recycling stands at more than 18 million tons annually, with China representing 66% of this total and India contributing approximately 8%. ICIS projects that mechanical recycling output will rise from over 14 million tons in 2024 to 34 million tons by 2040.

North America

North America is the second-largest market. The region has established packaging practices and strict regulatory requirements. In North America, the market for recycled plastic packaging is fueled by a comprehensive waste management and recycling infrastructure, which includes sophisticated sorting and processing facilities. The growing emphasis on food safety and convenience packaging, especially in frozen and ready-to-eat segments, boosts market growth.

- According to Unifor Organization, in terms of production value, the food and beverage sector ranks as the second largest manufacturing industry in Canada, with total sales approaching USD 118 billion in 2019. In 2021, the sector added USD 34.5 billion to the national gross domestic product (GDP), representing almost 2% of the overall GDP. The food and beverage sector is the biggest employer in Canada’s manufacturing industry, offering jobs to over 300,000 Canadians.

Europe

Europe is a significant market for recycled plastic packaging. The rising global push for sustainability is driving the adoption of recyclable and eco-friendly materials in pallet packaging. Businesses are seeking recyclable, reusable, and biodegradable materials for pallets to lessen their ecological footprint, resulting in a rise in the use of wooden, plastic, and corrugated cardboard pallets.

For instance, the European Environment Agency states that, in 2023, Europe had a circularity rate of 11.8%, indicating it utilized a greater share of recycled materials compared to other global regions despite only modest advancements in recent years. Speeding up the shift to a circular economy has emerged as a key policy focus.

Latin America

The market in Latin America is expected to witness considerable growth in the near future. The growing trend toward minimalist packaging solutions is embracing this growth. By decreasing the use of excessive materials and choosing recyclable plastics, minimalist packaging contributes to a smaller environmental footprint.

Middle East & Africa

The Middle East & Africa region will see substantial growth in the coming years. Governments and consumers in the region are increasingly pushing for more sustainable packaging products, further creating a favorable environment for recycled plastic packaging. The growing demand for sustainable packaging solutions is cushioning the market growth in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Continuous Development and Introduction of New Products by Key Companies Resulted in their Dominating Market Positions

The global recycled plastic packaging market is concentrated with companies such as Amcor Plc, Berry Global Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, Sealed Air Corporation, Constantia Flexibles, and Plastipak Holdings, Inc., accounting for a significant market share.

Amcor plc is the leading global manufacturer of flexible packaging and specialty folding cartons. The company has a presence in 40 countries and has established over 230 manufacturing sites globally. The company concentrates on making packaging that is lightweight, reusable, and prepared using recycled content.

Sealed Air Corporation is a leading global provider of packaging solutions, offering a wide range of products and services that protect goods, preserve food, and automate packaging processes. The company is committed to sustainable packaging solutions, aiming for 100% recyclable or reusable packaging materials by 2025 and net-zero carbon emissions in its global operations by 2040.

Additionally, ALPLA Werke Alwin Lehner GmbH & Co KG and Berry Global Inc. are among the other prominent players in the market. Focus on significant investments in the research & development of innovative products has supported the companies’ share in the market.

- In July 2023, Berry Global introduced a selection of reusable bottles crafted entirely from post-consumer recycled (PCR) plastic for The Bio-D Company, a prominent ethical cleaning brand in the U.K. This collection features 750ml, 1 liter, and 5-liter sizes for various Bio-D liquid products, such as Laundry Liquid, Fabric Conditioner, Dishwasher Rinse Aid, Washing Up Liquid, and Home & Garden Cleaner.

LIST OF KEY RECYCLED PLASTIC PACKAGING COMPANIES PROFILED

- Amcor Plc (Switzerland)

- Berry Global Inc. (U.S.)

- ALPLA Werke Alwin Lehner GmbH & Co KG (Austria)

- Sealed Air Corporation (U.S.)

- Constantia Flexibles (Austria)

- Plastipak Holdings, Inc. (U.S.)

- UFlex Limited (India)

- Placon Corp (U.S.)

- Genpak, LLC (U.S.)

- Retal Industries LTD. (Cyprus)

- Alpha Packaging (India)

- CKF, Inc. (Canada)

- Pactiv Evergreen (U.S.)

- Anchor Packaging Inc. (U.S.)

- Regent Plast Private Limited (India)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Tetra Pak has launched packaging that incorporates 5% certified recycled polymers for food and beverage items in India, making it a pioneer in this sector within the country. The new carton designs contain 5% certified recycled polymers and adhere to the Plastic Waste Management (Amendment) Rules 2022. This move aligns with Tetra Pak's commitment to circularity and reducing reliance on fossil-based resources.

- January 2025: Mondelēz collaborated with Amcor and Jindal Films to develop the new packaging, which is recycle-ready and incorporates Amcor’s AmFiniti recycled plastic. Mondelēz International is introducing packaging made from 80% certified recycled plastic for Cadbury sharing bars available in the British Isles. Beginning this year, the company is gradually implementing the new packaging for bars produced in Bournville, England, and Coolock, Ireland.

- October 2024: SCG Chemicals, known as SCGC, made significant progress by creating advanced recycling solutions for eco-friendly packaging. The company has introduced packaging for skincare products made entirely from recycled plastics, making it a pioneering effort in the ASEAN region. This groundbreaking packaging utilizes High-Quality PCR Resin under the SCGC GREEN POLYMERTM label, which has received certification in accordance with international standards.

- April 2024: Amcor, a worldwide leader in creating and manufacturing sustainable packaging solutions, is introducing a one-liter polyethylene terephthalate (PET) bottle designed for carbonated soft drinks (CSD) that is produced entirely from 100% post-consumer recycled (PCR) materials. This innovative stock option is the first of its kind and will assist customers in achieving their sustainability goals and obligations.

- March 2024: INEOS introduced innovative, high-quality snack packaging that incorporates 50% recycled plastics. PepsiCo has unveiled new packaging for the popular Sunbites snack brand in the UK and Ireland. This packaging is produced by recycling plastic waste through an advanced recycling method, showcasing its crucial contribution to fulfilling strict EU regulations for food contact packaging.

REPORT COVERAGE

The global recycled plastic packaging industry analysis provides market size & forecast by all the segments included in the report. It contains details on the market dynamics and recycled plastic packaging market trends expected to drive the market over the forecast period. It offers information on the utilization of recycled plastic packaging in key regions/countries, company profiles, key industry developments, new product launches, and details on partnerships, mergers & acquisitions in key countries. The report covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.03% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Material

|

|

By Product Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

The global recycled plastic packaging market size is projected to grow from USD 18.41 billion in 2026 to USD 29.40 billion by 2034, exhibiting a CAGR of 6.03% during the forecast period.

In 2024, the market value in Asia Pacific stood at USD 5.73 billion.

The market is expected to grow at a CAGR of 6.03% during the forecast period of 2026-2034.

The food and beverages segment led the market by application.

The key factor driving the market is the increasing government initiatives & efforts to reduce plastic waste.

Amcor Plc, Berry Global Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, Sealed Air Corporation, Constantia Flexibles, and Plastipak Holdings, Inc., are the top players in the market.

Asia Pacific holds the largest share of the market.

Seeking Comprehensive Intelligence on Different Markets?Get in Touch with Our Experts

Speak to an Expert

- 2021-2034

- 2025

- 2021-2024

- 120

Download Free Sample

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Packaging

Clients

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us