Residential Battery Market Size, Share & Industry Analysis, By Battery Type (Lithium-Ion, {LFP, NMC/NCA}, Lead Acid, Sodium-Ion, and Others), By Capacity Range (≤ 5 kWh, >5–10 kWh, >10–20 kWh, and >20 kWh), By Installation Type (Hybrid {Solar + Battery} and Standalone), By Application (Self-Consumption Optimization, Backup/Emergency Power, Grid Services/Virtual Power Plants, and Time-of-Use (ToU) Load Shifting), and Regional Forecast, 2026-2034

Residential Battery Market Size and Future Outlook

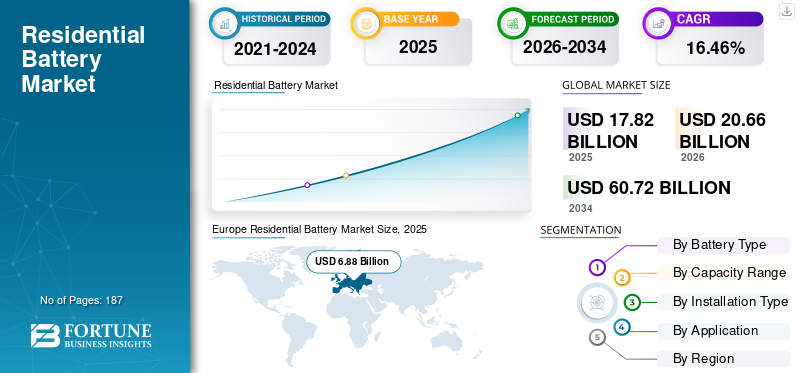

The global residential battery market size was valued at USD 17.82 billion in 2025. The market is projected to grow from USD 20.66 billion in 2026 to USD 60.72 billion by 2034, with a CAGR of 14.42% over the forecast period. Europe dominated the residential battery market with a market share of 38.60% in 2025.

Residential batteries are behind-the-meter energy storage systems installed in homes to store electricity, typically from rooftop solar power or the grid for later use, enhancing self-consumption, backup power availability, and household energy resilience. These systems play an increasingly important role in managing peak demand, improving grid stability, and enabling greater penetration of distributed renewable energy sources. Key performance attributes such as usable capacity, round-trip efficiency, cycle life, safety, and system integration capabilities directly influence homeowner economics and adoption, particularly in applications spanning solar-plus-storage, backup power, and energy arbitrage under time-of-use tariffs.

Demand for residential batteries is expected to expand rapidly, driven by rising residential solar installations, increasing electricity price volatility, grid reliability concerns, and supportive policy frameworks such as tax credits, feed-in tariff reforms, and net-metering rollbacks that favor self-consumption. In addition, growing adoption of electrified household loads (EV charging, heat pumps) and the emergence of virtual power plants (VPPs) are strengthening the value proposition for home storage. Technology trends are shifting toward lithium-ion chemistries, particularly LFP (Lithium Iron Phosphate), larger system capacities, and hybrid inverter-based installations that simplify system design and reduce balance-of-system costs.

The competitive landscape is shaped by established battery manufacturers, inverter-storage platform providers, and vertically integrated energy companies, including Tesla, LG Energy Solution, BYD, Sonnen, Enphase, and Panasonic. Competitive strategies increasingly focus on cost reduction through scale, safety-oriented chemistry choices, software and energy management capabilities, and regional manufacturing and assembly to align with local incentive structures and supply-chain localization policies. As residential storage transitions from an early-adoption phase toward mass-market deployment, differentiation is increasingly driven by system reliability, warranty terms, ecosystem integration, and participation in grid services and VPP programs.

Download Free sample to learn more about this report.

Residential Battery Market Trends

Grid-interactive “Virtual Power Plant (VPP) -Ready” Home Batteries are Becoming a Core Trend

The market is shifting from standalone backup systems toward grid-interactive assets that can be aggregated and dispatched as virtual power plants (VPPs), as utilities increasingly recognize residential batteries as reliable peak-capacity resources. This transition is supported by real-world deployment evidence: during a large-scale coordinated test in California in 2025, aggregated residential batteries delivered over 500 MW of dispatchable power for two consecutive evening peak hours, demonstrating that fleets of home batteries can perform at utility-relevant scale. Such programs are creating incremental homeowner value through bill credits, incentives, and performance-based payments, beyond traditional self-consumption benefits. As a result, system requirements are evolving toward always-connected, dispatch-ready architectures with robust telemetry, interoperability with utility platforms, and secure control layers, pushing vendors to differentiate through software capability, VPP program compatibility, and ease of enrollment rather than battery hardware alone.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Tariff Reform, Incentives, and Grid Reliability Concerns are Structurally Accelerating Residential Battery Adoption

The residential battery market growth is increasingly driven by changes in electricity tariff design and growing concerns about grid reliability, shifting batteries from “optional backup” to an economically rational household asset. In markets such as California, the transition away from traditional net metering toward net billing and time-of-use pricing has materially improved the value of storing solar generation rather than exporting it to the grid. Empirical deployment data shows that residential solar-plus-storage attachment rates rose sharply following tariff reform, with storage becoming the default companion to rooftop PV rather than a niche add-on. In parallel, extreme weather events, outage risks, and aging grid infrastructure are reinforcing the resilience value proposition of home batteries, particularly for higher-capacity systems capable of supporting extended backup.

Policy support is reinforcing these structural drivers. In the U.S., the extension of a standalone 30% federal tax credit for residential battery storage (≥3 kWh) has lowered effective system costs and broadened adoption beyond early adopters, while similar rebate-led programs in markets such as Australia and parts of Europe are stimulating volume growth. Together, these factors are pushing the market into a more sustained growth phase, with demand increasingly tied to regulatory design and long-term household energy cost optimization rather than short-term incentive cycles alone.

Market Restraints

High Installed System Costs and Regulatory Complexity Continue to Limit Mass-market Penetration

Despite declining battery prices, residential storage adoption remains constrained by high upfront installation costs and “soft costs” related to financing, permitting, and safety compliance. Interest rate environments materially affect homeowner economics, particularly in loan- or lease-based financing models, extending payback periods and dampening demand among price-sensitive customer segments. As a result, adoption is often concentrated in higher-income households or regions with strong incentives, limiting uniform penetration across broader residential markets.

In addition, safety and permitting requirements are becoming more stringent as residential battery deployments scale. Enhanced fire-safety standards, testing protocols, and local authority approvals, while necessary for long-term market credibility, can increase installation timelines, add compliance costs, and introduce jurisdiction-specific uncertainty. These factors collectively slow rollout speed and can constrain installer capacity, especially in regions where permitting frameworks for residential energy storage systems have not yet been streamlined.

Market Opportunities

Utility Programs and Virtual Power Plants are Opening New Monetization Pathways For Residential Batteries

A significant growth opportunity is emerging from integrating residential batteries into utility-led grid services and virtual power plant (VPP) programs. Utilities and system operators are increasingly recognizing aggregated home batteries as fast-response, dispatchable resources capable of supporting peak demand, grid stability, and emergency response. Large-scale demonstrations, where tens of thousands of residential batteries have been dispatched simultaneously to deliver hundreds of megawatts during peak hours, have validated the technical and operational viability of this model at utility-relevant scale.

For homeowners, VPP participation introduces incremental value streams through bill credits, incentives, or performance-based payments, improving system payback and encouraging adoption of always-connected, dispatch-ready systems. For manufacturers and platform providers, this creates whitespace for differentiation through software, energy management systems, interoperability, and utility program compatibility. Over time, this is expected to shift demand toward larger-capacity systems, hybrid inverter architectures, and ecosystems designed explicitly for grid interaction rather than standalone backup.

Market Challenges

Policy-Driven Demand Volatility and Shifting Economics Can Disrupt Near-Term Installation Momentum

Long-term fundamentals for residential batteries remain strong; near-term demand is susceptible to policy transitions, tariff changes, and consumer confidence. The same regulatory shifts that improve storage attachment rates can simultaneously reduce overall solar demand, creating volatile installation cycles. Evidence from major markets shows that while battery pairing increases under less favorable export tariffs, total customer inquiry and quote volumes can decline following abrupt policy changes—introducing short-term uncertainty into deployment pipelines.

This volatility poses challenges for manufacturers, installers, and financiers, as residential batteries are often sold as part of integrated solar, financing, and service offerings. Rapid changes in incentives, electricity pricing structures, or financing conditions can lead to stop-start demand patterns, inventory imbalances, and fluctuating installer activity. As a result, market participants must increasingly balance long-term growth expectations with short-term execution risk driven by regulatory and macroeconomic shifts.

Segmentation Analysis

By Battery Type

Lithium-ion Dominates Market as LFP Gains Share on Safety, Cost, and Cycle-Life Advantages

Based on battery type, the global market is segmented into Lithium-ion, Lead-acid, Sodium-ion, and others.

Lithium-ion represents the largest share of global residential deployments as it offers the best combination of energy density, round-trip efficiency, and ecosystem maturity (inverter compatibility, warranty structures, and installer familiarity). Within lithium-ion, LFP is the fastest-growing sub-chemistry, supported by improving volumetric design, strong thermal stability, long cycle life for daily cycling (self-consumption and ToU use cases), and pricing advantages as supply chains deepen.

The sodium-ion segment is expected to grow at a CAGR of 23.82% during the forecast period. Sodium-ion is emerging as a niche alternative with potential advantages in cost stability and cold-temperature performance, but it remains limited by early-stage scaling and product availability. Others capture niche/legacy chemistries that remain application-specific.

By Capacity Range

>10–20 kWh Segment Led Market as Households Shift from Backup-Only to Daily Cycling and Electrification Loads

Based on capacity range, the global market is segmented into ≤5 kWh, >5–10 kWh, >10–20 kWh, and >20 kWh.

The >10–20 kWh segment led the market as households target higher self-consumption, ToU arbitrage, and resilience coverage for longer outage durations. This range aligns well with typical residential solar PV pairing and is expandable via modular architectures. It also represents an optimal balance between upfront system cost and achievable economic returns, making it the preferred choice for both new solar-plus-storage installations and retrofit expansions. In addition, this capacity band supports daily cycling without accelerated degradation, which is critical as batteries shift from backup-only assets to revenue- and savings-generating energy management systems.

The >20 kWh segment is expected to grow at a CAGR of 21.81% during the forecast period. The >20 kWh segment is the fastest-expanding capacity tier in many advanced markets, supported by rising electrification loads (heat pumps, EV charging), whole-home backup expectations, and multi-battery stacking. Growth in this segment is further reinforced by increasing adoption of all-electric homes and multi-EV households, where smaller systems are insufficient to cover peak demand and overnight resilience needs. As system costs decline and inverter platforms increasingly support parallel battery configurations, >20 kWh systems are transitioning from a niche premium offering to a mainstream choice in high-consumption residences.

By Installation Type

Hybrid (Solar + Battery) Systems Lead as They Justified Economically Through Solar Self-Consumption Uplift

Based on installation type, the global market is segmented into hybrid (solar + battery) and standalone.

The hybrid (solar + battery) segment accounts for the largest residential battery market share as batteries are often justified economically through solar self-consumption uplift, bill optimization, and improved utilization of PV generation. Hybrid deployments also benefit from “single project” customer decisions and integrated installer channels. In many markets, incentive structures and permitting processes further favor bundled solar-plus-storage installations, reducing customer friction and accelerating adoption. Additionally, hybrid systems enable higher battery utilization rates, improving payback periods as households increasingly adopt ToU tariffs and dynamic pricing.

The standalone segment is expected to grow at a CAGR of 8.91% during the forecast period. Standalone systems are growing steadily in markets with high outage risk, aging grid infrastructure, or strong incentives for demand response/VPP participation. Standalone demand is also supported by retrofit additions to existing solar PV households and by replacement cycles in which older storage systems are upgraded. This segment benefits from the large installed base of legacy rooftop solar, particularly in early-adopter regions where batteries were not included in the initial PV investment.

To know how our report can help streamline your business, Speak to Analyst

By Application

Backup/Emergency Power Dominated Market Due to Its Resilience

Based on application, the global market is segmented into self-consumption optimization, backup/emergency power, grid services/virtual power plants, and time-of-use (ToU) load shifting.

The backup/emergency power segment dominated the market, accounting for 46.47% share in 2025. The dominance of backup/emergency power as resilience is the most intuitive customer value proposition, especially in markets experiencing reliability issues, extreme weather, or high perceived outage costs. In many regions, backup remains the initial purchase driver even when systems are later utilized for daily cycling, making it the foundation of multi-use value stacking.

The grid services/virtual power plants segment is the fastest-scaling “new” value pool, as utilities and aggregators expand program availability; it supports incremental revenue streams and can materially improve payback when participation is well incentivized. Over time, application stacking (backup + ToU + VPP) becomes more common, supported by advances in software orchestration, aggregation platforms, and regulatory acceptance of distributed flexibility.

Residential Battery Market Regional Outlook

By geography, the market has been studied geographically across North America, Europe, Asia Pacific, and the Rest of the World.

Europe

Europe Residential Battery Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe dominated the global market share. The region accounted for USD 6.88 billion in 2025, or approximately 38.63% of global revenues. Growth is driven by the region’s high sensitivity to retail electricity prices, accelerating adoption of self-consumption-maximizing PV + battery systems, and the shift toward smart tariffs that reward flexible demand. Europe also shows strong momentum in higher-capacity systems as households increasingly stack applications such as backup, ToU optimization, and emerging grid-interactive programs, supported by mature installer ecosystems and policy-led clean energy targets.

Germany Residential Battery Market

Germany was valued at USD 2.19 billion in 2025 and is expected to reach USD 2.48 billion in 2026, supported by Europe’s strongest installed base of residential solar, strong consumer preference for energy autonomy, and widespread pairing of batteries with new and retrofit PV to maximize onsite consumption under evolving export economics.

U.K. Residential Battery Market

The U.K. market was valued at USD 0.92 billion in 2025 and is expected to reach USD 1.07 billion in 2026, supported by increasing adoption of smart tariffs, growing consumer focus on bill optimization, and steady growth in hybrid solar-plus-storage installations.

North America

North America was valued at USD 4.47 billion in 2025, accounting for approximately 25.07% of the global market. The region is supported by strong uptake of solar + storage, rising grid reliability concerns (storm-driven outages), and accelerating adoption of tariff-driven optimization (ToU and demand charges) that increases the value of daily cycling. In addition, growing penetration of VPP/DR programs and installer-led bundled offerings strengthens hybrid attach rates and expands addressable demand beyond backup-only buyers.

U.S. Residential Battery Market

The U.S. market was valued at USD 4.17 billion in 2025 and is expected to reach USD 4.90 billion in 2026, supported by the country’s large installed base of rooftop solar, increasing interest in whole-home resilience, and improving economics for self-consumption and ToU arbitrage as rate structures evolve. Adoption is also reinforced by expanding aggregator programs that monetize dispatchable capacity and improve payback through recurring incentives.

Asia Pacific

Asia Pacific accounted for approximately 33.91% of global revenues, valued at USD 6.04 billion in 2025. The region benefits from strong momentum in distributed solar adoption, expanding demand for resilience in select markets, and growing relevance of daily cycling, where tariff spreads and household electrification (cooling, EV charging) improve savings from storage. Asia Pacific also benefits from a deepening supply ecosystem, enabling broader product availability across capacity tiers and faster adoption of newer chemistries such as LFP, where cost-per-cycle and safety are prioritized.

China Residential Battery Market

China was valued at USD 2.29 billion in 2025 and is expected to reach USD 2.68 billion in 2026, supported by expanding residential distributed energy adoption, improving product affordability, and increasing interest in household-level backup and bill optimization in targeted provinces and programs.

India Residential Battery Market

India was valued at USD 0.62 billion in 2025 and is expected to reach USD 0.77 billion in 2026, reflecting the rapid expansion of rooftop solar adoption in select segments, strong demand for backup power where reliability is a concern, and increasing visibility of storage as a household asset for energy stability.

Japan Residential Battery Market

Japan was valued at USD 0.99 billion in 2025 and is expected to reach USD 1.13 billion in 2026, supported by a mature residential energy management culture, resilience-driven buying behavior, and steady adoption of solar-plus-storage systems optimized for household reliability and self-consumption.

Rest of the World

The Rest of the World was valued at USD 0.43 billion in 2025, and the gradual expansion of rooftop solar supports growth, increased attention to grid reliability and power quality, and early-stage adoption of home storage that improves resilience or complements distributed PV. While smaller today, this region can scale meaningfully as financing access improves, installer ecosystems mature, and tariff/incentive structures become more storage-friendly.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Software-enabled Platforms, Ecosystem Control, and Grid Integration are Becoming Primary Competitive Levers in Market

The residential battery market is moderately fragmented, comprising a mix of global battery manufacturers, inverter-centric energy platforms, and vertically integrated solar-plus-storage providers, all competing across hardware performance, safety credentials, system integration, and software capabilities. While battery cell chemistry and enclosure safety remain baseline requirements, competition is increasingly shifting toward system-level differentiation, including inverter integration, energy management software, virtual power plant (VPP) readiness, and ease of participation in utility programs. As residential storage adoption scales, customers and installers are prioritizing turnkey ecosystems that simplify commissioning, monitoring, and long-term operation over standalone battery hardware.

List of Key Residential Battery Companies Profiled

- Tesla (U.S.)

- LG Energy Solution (South Korea)

- BYD Companies (China)

- Enphase Energy (U.S.)

- Panasonic (Japan)

- Samsung SDI (South Korea)

- FranklinWH (U.S.)

- Alpha ESS (China)

- Sigenergy (China)

- Sonnen (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Tesla continued expanding its Virtual Power Plant footprint in North America, with Powerwall fleets participating in multiple utility dispatch events, reinforcing Tesla’s competitive advantage in software orchestration, scale, and grid integration rather than battery hardware alone.

- August 2025: Enphase expanded its IQ Battery deployments integrated with the Enphase Energy System, emphasizing AC-coupled architectures and software-driven energy optimization, highlighting how inverter-centric platforms are using ecosystem control to defend market share.

- June 2025: Sonnen announced further expansion of its community battery and VPP programs in Europe and the U.S., leveraging its grid services expertise and utility partnerships to position residential batteries as grid assets rather than standalone backup solutions.

- April 2025: BYD increased international shipments of residential LFP battery systems, reinforcing its cost and chemistry leadership while expanding certifications and installer support in Europe and emerging Asia Pacific markets.

- February 2025: LG Energy Solution strengthened its residential storage portfolio, focusing on long-life LFP-based systems and expanding warranty offerings, signaling growing competition around durability, safety assurance, and lifecycle economics rather than headline capacity alone.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.46% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Battery Type

|

|

By Capacity Range

|

|

|

By Installation Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

According to a Fortune Business Insights study, the market size was USD 17.82 billion in 2025 and is expected to reach USD 60.72 billion by 2034.

The market is likely to grow at a CAGR of 14.42% over the forecast period (2026-2034).

By installation type, the Hybrid (Solar + Battery) segment leads the market.

The European market size stood at USD 6.88 billion in 2025.

Tariff reform, incentives, and grid reliability concerns are structurally accelerating residential battery adoption.

Some of the top players in the market include BYD, Panasonic, Samsung SDI, Tesla, and others.

- 2021-2034

- 2025

- 2021-2024

- 187

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us