Sarcoma Drugs Market Size, Share & Industry Analysis, By Drug (Imatinib, Pazopanib, Ripretinib, Nirogacestat, Trabectedin, Avapritinib, & Others), By Drug Class (Cytotoxic Chemotherapy, Tyrosine Kinase Inhibitors, Gamma Secretase Inhibitors, Immune Checkpoint Inhibitors, EZH2 Inhibitors), By Disease Indication (GIST, Leiomyosarcoma, Liposarcoma, Desmoid Tumors), By Age Group (Pediatric and Adults), By Therapy (Targeted Therapy, Immunotherapy, Chemotherapy), By Route of Administration, By Distribution Channel (Hospital Pharmacies, Retail/Online Pharmacies), and Regional Forecast, 2026-2034

Sarcoma Drugs Market Size and Future Outlook

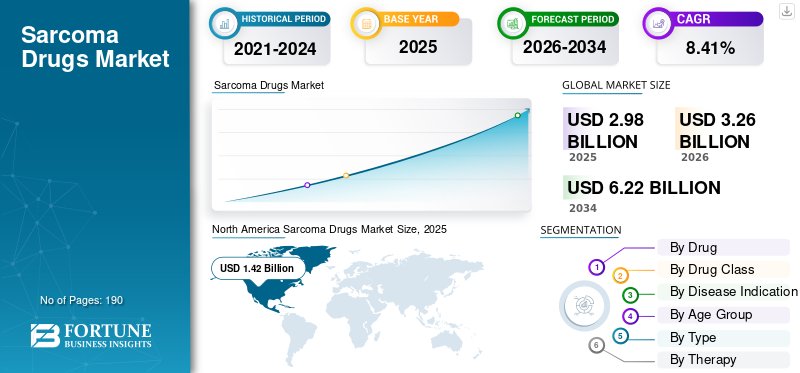

The global sarcoma drugs market size was valued at USD 2.98 billion in 2025. The market is projected to grow from USD 3.26 billion in 2026 to USD 6.22 billion by 2034, exhibiting a CAGR of 8.41% during the forecast period. North America dominated the sarcoma drugs market with a market share of 47.65% in 2025.

The global market is expected to grow steadily over the coming years, driven by the rising need for effective treatment options for rare and complex sarcoma subtypes. Sarcoma is a group of cancers with multiple histologies, which increases the demand for targeted, subtype-specific, and advanced therapeutic approaches. As more sarcoma patients with relapsed or advanced disease demand new lines of therapy, drug manufacturers are increasing their focus on precision oncology, cell therapy, and the development of drugs for rare cancers. Furthermore, regulatory support for orphan and breakthrough therapies is encouraging companies to invest more in this area. Such factors are expected to drive continuous innovation in sarcoma treatment, supporting the overall growth of the global market.

- For instance, in January 2026, Lantern Pharma received the U.S. FDA Orphan Drug Designation for its investigational candidate, LP-284, for soft tissue sarcomas. The designation expanded the development potential of LP-284 in a rare cancer setting with high unmet need. Such regulatory progress is expected to support clinical development, improve investor and industry confidence, and strengthen growth prospects for the global market.

Leading players in the industry, such as Novartis AG, Pfizer Inc., Deciphera Pharmaceuticals, LLC, and Blueprint Medicines Corporation, are focusing on research and development to strengthen their market positions.

Download Free sample to learn more about this report.

SARCOMA DRUGS MARKET TRENDS

Rising Shift Toward Histology-Specific and Precision-Based Sarcoma Therapies is an Emerging Market Trend

The global sarcoma drugs market is increasingly moving toward histology-specific and precision-based therapies, reflecting a prominent trend in the market. Sarcoma includes multiple rare subtypes that do not respond equally to a single treatment approach. As a result, drug developers are focusing on therapies designed for biomarker-defined and subtype-specific patient groups. This targeted approach enhances the clinical value of treatment by enabling companies to target patient populations with clearer biological markers and better-defined unmet needs. Such developments are strengthening innovation and commercial interest in the sarcoma space.

- For instance, in January 2025, Adaptimmune Therapeutics plc received Breakthrough Therapy Designation from the U.S. FDA for letetresgene autoleucel (lete-cel), intended for the treatment of patients with unresectable or metastatic myxoid/round cell liposarcoma (MRCLS). The therapy is designed for patients who have received prior anthracycline-based chemotherapy, test positive for HLA-A*02:01, HLA-A*02:05, or HLA-A*02:06, and whose tumor expresses the NY-ESO-1 antigen. Such increasingly advancing therapies for specific sarcoma subtypes are expected to support the broader global market trend toward precision-led sarcoma drug development.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Unmet Need for Effective Therapies Across Rare and Advanced Sarcoma Subtypes Fueling Market Growth

The global sarcoma drugs market is being driven by the significant unmet need for more effective therapies across rare and advanced sarcoma subtypes. Sarcoma includes many biologically diverse tumors, and patients with relapsed, metastatic, or treatment-resistant disease often face limited standard treatment options. Due to this, drug developers are increasingly focusing on novel therapies designed to address narrower patient groups with better clinical precision. This is driving stronger research activity, greater regulatory momentum, and greater commercial interest in the market. As companies continue to develop therapies for difficult-to-treat sarcoma segments, the market is expected to gain steady support from innovation-led demand.

- For instance, in August 2025, Eisai Co., Ltd., granted Orphan Drug Designation from the Ministry of Health, Labor and Welfare for tazemetostat for the treatment of unresectable INI1-negative epithelioid sarcoma that progressed following chemotherapy. This development highlights how companies are actively investing in rare sarcoma subtypes where treatment options remain limited, which is expected to support the global sarcoma drugs market growth.

MARKET RESTRAINTS

Rare and Highly Fragmented Group of Cancers to Restrain Market Growth

The global sarcoma drugs market faces a clear restraint due to the rare and highly fragmented group of cancers, resulting in a relatively small number of treatable patients compared with more common oncology indications. Soft Tissue Sarcomas account for less than 1% of all cancer cases worldwide, and the disease is further split across many histological and molecular subtypes, which reduces the patient pool available for any single drug program. Due to this, companies often face difficulty in building large clinical datasets, recruiting enough patients quickly, and achieving the commercial scale needed to justify broad investment across multiple sarcoma subtypes. As a result, development timelines tend to extend, per-patient clinical trial costs increase, and market expansion can remain slower than in larger oncology categories. This structural limitation is expected to continue restraining the growth of the market.

- For instance, in May 2025, an abstract published by the ASCO titled ‘Global inequities in sarcoma clinical trials: A comprehensive analysis over the last decade,’ highlighted the practical impact of this rarity challenge. The study reported a median sample size of only 46 participants in sarcoma trials. It also identified significant underrepresentation of low-income countries and pediatric populations, underscoring how the small, unevenly distributed patient pool continues to limit the scale and inclusiveness of sarcoma research.

MARKET OPPORTUNITIES

Rising Orphan Drug and Rare Disease Regulatory Support to Create Growth Opportunities

The global sarcoma drugs market is expected to witness strong growth opportunities from rising orphan drug and rare disease regulatory support. Sarcoma is a rare and highly fragmented cancer group, which often creates challenges related to small patient pools, complex trials, and high development risk. Due to this, orphan drug, fast track, and rare disease regulatory pathways become important, as they help improve development feasibility and encourage companies to invest in niche sarcoma indications. These regulatory advantages can support faster clinical progress, stronger investor confidence, and better commercial planning for therapies targeting underserved sarcoma subtypes. As a result, increasing regulatory support for rare cancers is creating favorable conditions for pipeline expansion and long-term global market growth.

- For instance, in January 2025, OS Therapies announced that its Phase 2b trial of OST-HER2 achieved its primary endpoint in recurrent, fully resected, lung metastatic osteosarcoma. The company also noted that OST-HER2 received Rare Pediatric Disease, Fast Track, and Orphan Drug designations from the U.S. FDA and EMA. This highlights how rare-disease regulatory support can strengthen development momentum in sarcoma-related indications and improve the commercial attractiveness of otherwise difficult-to-develop therapies.

MARKET CHALLENGES

High Development Cost and Elevated Clinical Risk to Challenge Market Growth

The global market faces a major challenge as sarcoma is a rare and highly heterogeneous cancer group, which makes drug development more expensive and clinically risky. Since the disease is divided into many subtypes, companies often need narrower trials, specialized patient selection, and longer development timelines to generate meaningful clinical evidence. This requirement increases per-program cost and also raises the risk that a therapy may not show a strong enough benefit-to-risk profile across such limited patient populations. Due to this, even promising products can face setbacks late in development or after launch, which can reduce commercial confidence and slow further investment in the market. As a result, high development cost combined with elevated clinical risk remains an important challenge for the global sarcoma drugs market.

- For instance, in March 2026, Ipsen voluntarily withdrew Tazverik (tazemetostat) from all its commercial markets, including the indication for Epithelioid Sarcoma. The decision followed emerging safety data from the ongoing SYMPHONY-1 trial, which showed cases of secondary hematologic malignancies. The Independent Data Monitoring Committee advises that the risks may outweigh the potential benefits in this setting. Such instances showcase how clinical risk can directly affect the commercial pathway of sarcoma-related therapies, even after approval, and can create uncertainty for companies operating in the market.

Segmentation Analysis

By Drug

Wider Treatment Eligibility of Imatinib Led the Segment Growth

Based on drug, the market is categorized into imatinib, pazopanib, ripretinib, nirogacestat, trabectedin, avapritinib, and others.

The imatinib segment accounted for the larger share of the market, supported by its strong historical treatment role in sarcoma-related drug therapy, especially in Gastrointestinal Stromal Tumor (GIST). It became the first major targeted treatment to change the standard of care for GIST. As imatinib is used in both unresectable/metastatic and adjuvant high-risk resected GIST settings, it has had broader and longer clinical use than newer drugs such as ripretinib, avapritinib, or nirogacestat, which are more limited to specific lines of therapy or narrower patient subsets. This broader treatment eligibility, long-standing physician familiarity, and strong role as the benchmark first-line therapy are expected to have helped imatinib maintain the largest share in the drug segment. Even as newer agents expand into later-line and niche indications settings, imatinib continues to anchor the sarcoma treatment pathway, particularly in commercially significant indications.

- For instance, in April 2026, Cogent Biosciences announced the completion of its NDA submission for bezuclastinib in GIST patients who had previously received imatinib. This is important as it shows that new sarcoma-related drug development in GIST is still positioned after imatinib, reinforcing imatinib’s role as the key baseline therapy and supporting its likely continued dominance within the drug segment.

The ripretinib segment is expected to grow at a CAGR of 49.13% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Drug Class

Broad Establishment Commercial Presence of Tyrosine Kinase Inhibitors (TKIs) Across Sarcoma-related Treatment Led the Segmental Growth

Based on drug class, the market is categorized into cytotoxic chemotherapy, Tyrosine Kinase Inhibitors (TKIs), gamma secretase inhibitors, immune checkpoint inhibitors, cell therapies, Epigenetic/EZH2 inhibitors, and others.

The tyrosine kinase inhibitors (TKIs) segment dominated the market as they have the broadest established commercial presence across sarcoma-related treatment, especially in GIST, where kinase-driven disease biology has supported long-term use of agents such as imatinib, sunitinib, regorafenib, and ripretinib. As these drugs are used across multiple lines of therapy and are integrated into treatment pathways, they generate stronger market revenue than newer niche classes that are limited to smaller patient subsets. This wider clinical use, better physician familiarity, and longer commercialization history are expected to keep TKIs ahead of other drug classes in the current market.

- For instance, in February 2026, Ono Pharma submitted an application in Japan for ripretinib in advanced GIST. These developments highlight the continued commercial and regulatory expansion of the TKI class in sarcoma-related care, reinforcing its leading position in the market.

The gamma secretase inhibitors segment is expected to grow at a CAGR of 62.23% over the forecast period.

By Disease Indication

Revenue Generation Potential of Gastrointestinal Stromal Tumor (GISTs) Boosted Segmental Growth

Based on disease indication, the market is segmented into GIST, leiomyosarcoma, liposarcoma, synovial sarcoma, desmoid tumors, osteosarcoma, and others.

In 2025, GIST accounted for the largest market share. GIST has clearly established a systemic treatment pathway among sarcoma indications. Unlike many other sarcoma subtypes that still depend heavily on chemotherapy or have limited approved options, GIST benefits from multiple approved targeted agents across different treatment lines, which supports higher treatment continuity and stronger drug spending. Due to this, GIST contributes a larger commercial base than other individual sarcoma subtypes, making it the most likely leading disease indication segment. Key companies are focusing on technologically advanced offerings and the regulatory approvals that accompany them to strengthen their market position.

- For instance, in June 2025, Onco360 was selected as a national specialty pharmacy partner for QINLOCK (ripretinib), a drug approved for advanced GIST. This development reflects the continued strengthening of distribution infrastructure supporting GIST therapies, which supports the segment’s leadership in the market.

The desmoid tumors segment is projected to grow at a CAGR of 23.37% during the forecast period.

By Age Group

Large Adult Patient Pool Led the Growth of the Segment

Based on age group, the market is segmented into pediatric and adult.

In 2025, the adult segment dominated the market. The commercially active sarcoma drug landscape is more concentrated in adult indications than in pediatric use. Many approved, and late-stage sarcoma therapies are indicated for adult patients with advanced soft-tissue sarcoma, desmoid tumors, GIST, liposarcoma, or epithelioid sarcoma. Adult patients represent the larger treated population across currently marketed products, and regulatory approvals are initially granted for adult indications before expanding into adult pediatric populations. The trend has contributed to the adult segment holding the largest market share.

- For instance, in August 2025, SpringWorks announced that the European Commission approved OGSIVEO (nirogacestat) for adults with desmoid tumors. This supports the view that adult-focused approvals continue to drive a larger share of market value in sarcoma-related drug treatment.

The pediatric segment is projected to grow at a CAGR of 7.65% during the study period.

By Type

Generics Segment Dominated due to Expanding Patient Access Across Broader Treatment Settings

Based on type, the market is segmented into branded and generic.

The generics segment accounted for the largest global sarcoma drugs market share during the forecast period. Older sarcoma-related therapies such as imatinib and pazopanib have entered the generic market, improving affordability and expanding patient access across broader treatment settings. As sarcoma treatment requires long therapy duration in eligible patients, lower-cost generic options can support higher prescription volume and wider use. This creates a volume advantage for generics, leading to their dominance.

- For instance, in December 2025, Camber Pharmaceuticals launched the Imatinib Mesylate Tablets. The development is crucial as imatinib remains one of the most established drugs used in GIST, and the continued launch of generic imatinib products shows how mature sarcoma-related molecules are supporting broader market access through the generic channel.

The branded segment is projected to grow at a CAGR of 9.83% during the study period.

By Therapy

Increasing Shift Toward Molecularly Directed and Subtype-Specific Treatment Led the Targeted Therapy Segment Growth

Based on therapy, the market is segmented into targeted therapy, immunotherapy, chemotherapy, and others.

In 2025, targeted therapy accounted for the leading market share as sarcoma drug development has increasingly shifted toward molecularly directed and subtype-specific treatment, especially in GIST, desmoid tumors, and selected rare sarcoma subtypes. This has reduced reliance on broad-spectrum chemotherapy in commercially important segments and enabled targeted drugs to command higher clinical and economic value. As targeted therapies offer more precise treatment targeting and strong regulatory support in rare tumor settings, they are expected to lead the segment.

- For instance, in August 2025, Eisai announced that Japan’s Ministry of Health, Labor and Welfare granted orphan drug designation to tazemetostat for unresectable INI1-negative epithelioid sarcoma. This shows how targeted, biomarker-defined approaches are continuing to expand in sarcoma treatment, supporting the leading role of targeted therapy.

The immunotherapy segment is projected to grow at a CAGR of 12.63% over the study period.

By Route of Administration

Ease of Administration Provided by Oral Drugs Propelled Segmental Growth

Based on route of administration, the market is segmented into oral and parenteral.

The oral segment dominated the market as many of the key, commercially important sarcoma therapies, especially TKIs and gamma-secretase inhibitors, are designed for oral administration. Oral therapy improves treatment convenience, supports long-term outpatient use, and can reduce dependence on infusion-based hospital visits for suitable patients. As several leading branded sarcoma therapies are oral products, the oral segment is estimated to hold the largest share of the market during the study period.

- For instance, in April 2025, Bluesight released its 11th Annual Hospital Pharmacy Operations Report, highlighting the rising adoption of technology to address compliance and procurement pressures facing hospital pharmacies. This supports the dominance of the hospital pharmacy segment as it shows that hospitals remain a major buyer group for software that improves pharmacy supply chain and operational performance.

The parenteral segment is projected to grow at a CAGR of 7.29% over the study period.

By Distribution Channel

Increasing Demand in Hospitals & ASCs Due to Large Patient Volumes to Lead Growth in the Segment

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

Hospital pharmacies accounted for the largest share of the market, as sarcoma treatment often involves specialist oncology centers, multidisciplinary care, biomarker testing, and controlled administration pathways, particularly for advanced-stage disease and high-cost therapies. Even for orally administered treatments, therapy initiation, patient monitoring, reimbursement coordination, and complex treatment management are centered around hospital-based cancer networks. As a result, hospital pharmacies are estimated to account for the largest share of dispensing and treatment-related drug access within the market.

- For instance, in May 2025, Adaptimmune reported that 28 Authorized Treatment Centers were accepting referrals for Tecelra, with successful patient access and no payer denials reported at that time. This development shows how sarcoma drug delivery, especially for advanced specialty therapies, is concentrated in institution-led treatment networks, which supports the dominance of hospital pharmacies in the distribution landscape.

The online pharmacies segment is projected to grow at a CAGR of 10.70% over the study period.

Sarcoma Drugs Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Sarcoma Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant market share in 2024, valued at USD 1.31 billion, and maintained its leading position in 2025 at USD 1.42 billion. Market growth in the region is supported by a strong commercial base for rare oncology drugs, earlier uptake of newly approved sarcoma therapies, and broader access to specialty cancer centers. The region also benefits from faster regulatory pathways and the widespread use of biomarker-led treatment approaches, helping new drugs move into clinical practice more quickly.

U.S. Sarcoma Drugs Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated to reach around USD 1.43 billion by 2026, accounting for roughly 43.97% of global sales.

Europe

Europe is projected to grow at a CAGR of 7.47% over the coming years, representing the second-highest position among all regions, and is expected to reach a valuation of USD 0.87 billion by 2026. Market growth in the region is supported by an increasing number of regulatory approvals for rare sarcoma indications and the stronger integration of orphan oncology therapies into specialist care pathways.

U.K. Sarcoma Drugs Market

The U.K. market is estimated to reach around USD 0.19 billion by 2026, representing roughly 5.85% of the global market sales.

Germany Sarcoma Drugs Market

Germany's market is projected to reach approximately USD 0.21 billion by 2026, equivalent to around 6.38% of the global market sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.56 billion by 2026, securing its position as the third-largest regional market. The region is growing as countries such as Japan are expanding regulatory support for rare-cancer drugs, while regional oncology systems continue to invest in advanced cancer treatment.

Japan Sarcoma Drugs Market

The Japanese market is estimated to reach around USD 0.16 billion by 2026, accounting for approximately 4.77% of the global market sales.

China Sarcoma Drugs Market

China's market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.20 billion, representing approximately 6.17% of global sales.

India Sarcoma Drugs Market

The Indian market is estimated to reach around USD 0.08 billion by 2026, accounting for roughly 2.37% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin American market is set to reach a valuation of USD 0.13 billion by 2026. Growth in the region is driven by ongoing efforts to address access gaps in sarcoma care, creating catch-up opportunities in areas such as early diagnosis, patient referral networks, rare-cancer policy, and drug availability across healthcare systems. In the Middle East & Africa, the GCC is set to reach a valuation of USD 0.04 billion by 2026.

South Africa Sarcoma Drugs Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.30% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Emphasize New Product Launches to Reinforce Their Market Presence

The global market reflects a consolidated market structure, with companies such as Novartis AG, Pfizer Inc., Deciphera Pharmaceuticals, LLC, Blueprint Medicines Corporation, Eisai Co., Ltd., and PharmaMar, S.A. holding significant market share. These companies continue to strengthen their market presence through strategic partnerships, new product launches, technological advancements, and increased investments in targeted oncology therapies.

- For instance, in February 2026, Deciphera Pharmaceuticals received acceptance from the U.S. FDA for filing the New Drug Application (NDA) under the accelerated approval pathway for tirabrutinib, a highly selective, irreversible, second-generation Bruton tyrosine kinase inhibitor, intended for the treatment of relapsed or refractory primary central nervous system lymphoma (R/R PCNSL).

Other notable players in the global market include Johnson & Johnson, Adaptimmune Therapeutics plc, and Aadi Bioscience, Inc. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions.

LIST OF KEY SARCOMA DRUGS COMPANIES PROFILED

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Deciphera Pharmaceuticals, LLC (U.S.)

- Blueprint Medicines Corporation (U.S.)

- Eisai Co., Ltd. (U.S.)

- PharmaMar, S.A. (Spain)

- Johnson & Johnson (U.S.)

- Adaptimmune Therapeutics plc (U.S.)

- Aadi Bioscience, Inc. (U.S.)

- Genentech, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Biodexa Pharmaceuticals PLC partnered with Syngene International Ltd for the manufacture of both the active pharmaceutical ingredient and dosage form of MTX240. This collaboration supports scaled production capabilities and strengthens supply readiness for gastrointestinal cancer-related therapies.

- February 2026: Biodexa Pharmaceuticals PLC announced the closing of an exclusive license with Otsuka Pharmaceutical Co., Ltd (Otsuka) for OPB-171775, a novel molecular glue intended to be developed for the treatment of gastrointestinal stromal tumors (GIST). The compound has the potential to be useful in additional indications for rare cancer therapies.

- January 2026: Lantern Pharma Inc. announced that the U.S. FDA granted Orphan Drug Designation (ODD) to its lead candidate, LP-284, for the treatment of soft tissue sarcomas.

- December 2025: Immunome, Inc. announced positive topline results from its global pivotal Phase 3 RINGSIDE trial of varegacestat, an investigational oral, once-daily gamma secretase inhibitor (GSI), in patients with progressing desmoid tumors.

- August 2025: Merck KGaA received marketing authorization from the European Commission for OGSIVEO (nirogacestat), an oral gamma-secretase inhibitor, as monotherapy for adults with progressing desmoid tumors who require systemic treatment.

REPORT COVERAGE

The global sarcoma drugs market research report offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.41% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug, Drug Class, Disease Indication, Age Group, Type, Therapy, Route of Administration, Distribution Channel, and Region |

| By Drug |

|

| By Drug Class |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Therapy |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.98 billion in 2025 and is projected to reach USD 6.22 billion by 2034.

In 2025, the market value stood at USD 1.42 billion.

The market is expected to grow at a CAGR of 8.41% over the forecast period.

By drug class, the tyrosine kinase inhibitors (TKIs) segment led the market.

The rising unmet need for effective therapies in rare and advanced sarcoma subtypes is the key factor driving the market.

Novartis AG, Pfizer Inc., Deciphera Pharmaceuticals, LLC, Blueprint Medicines Corporation, and Eisai Co., Ltd. are the major market players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us