Satellite Modem Market Size, Share & Industry Analysis, By Offering (Satellite Modems, Software-Defined Modems, Modem Management Software, Services, and Others), By Modem Type (VSAT Modems, SCPC Modems, and Others), By Satellite Orbit (GEO Satellite Modems, MEO Satellite Modems, LEO Satellite Modems, and Others), By Platform, By Application (Broadband Connectivity, Cellular Backhaul, Government & Defense Communications, and Others), By End User (Defense & Military, Aviation Companies, Maritime Operators, Satellite Operators, and Others), and Regional Forecast, 2026-2034

Satellite Modem Market Size and Future Outlook

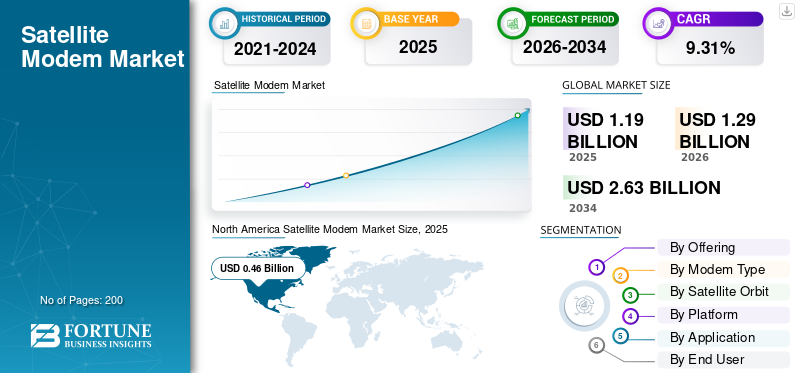

The global satellite modem market size was valued at USD 1.19 billion in 2025. The market is projected to grow from USD 1.29 billion in 2026 to USD 2.63 billion by 2034, exhibiting a CAGR of 9.31% during the forecast period. North America dominated the satellite modem market with a market share of 38.66% in 2025.

A satellite modem converts digital signals into RF transmissions and back, enabling two-way links between ground equipment and orbiting satellites. The market includes VSAT, SCPC, software-defined, and HTS-capable modems across C, Ku, and Ka-bands, serving maritime, aviation, oil & gas, military, emergency response, rural broadband, and enterprise networks. Growth is driven by demand for continuous high-speed connectivity, rising defense needs, and rapid LEO constellation deployment (e.g., Starlink, OneWeb). Leading vendors include Viasat, Hughes (EchoStar), ST Engineering iDirect, Comtech EF Data, Gilat, and MDA.

Download Free sample to learn more about this report.

SATELLITE MODEM MARKET TRENDS

LEO Constellation Proliferation and Software-Defined Architectures Redefining Satellite Modem Technology is a Notable Market Trend

The market is being reshaped by the rapid proliferation of low Earth orbit constellations and parallel shift toward software-defined modem architectures. LEO networks from operators like SpaceX's Starlink and Eutelsat OneWeb demand ground modems capable of handling high-speed handoffs and multi-orbit switching, pushing manufacturers to develop firmware-upgradable, reconfigurable platforms. Furthermore, players investing in SDMs and LEO ready features gain competitive advantage as operators prioritize flexibility, lifecycle economics, and rapid service rollout.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for High-Speed Broadband Connectivity in Remote and Underserved Regions is Accelerating Market Expansion

Rapid digitalization across industries operating in geographically isolated environments is compelling enterprises, governments, and service providers to invest aggressively in satellite communication infrastructure. Offshore energy platforms, commercial shipping fleets, mining operations, and rural healthcare facilities increasingly depend on high-throughput satellite modems to maintain uninterrupted broadband links where terrestrial networks remain economically unviable. The simultaneous deployment of high-throughput satellites by major operators is further amplifying ground-segment hardware demand, as existing modem infrastructure requires upgrades to make maximum use of available orbital capacity. Rising connectivity expectations across emerging economies in Asia Pacific, Africa, and Latin America are reinforcing this sustained, multi-sector procurement momentum.

MARKET RESTRAINTS

Inconsistent Regulatory Frameworks and High Spectrum Coordination Costs to Constrain Market Scalability

A persistent restraint across the satellite modem market growth is the absence of consistent international regulatory frameworks governing satellite communication protocols and frequency allocations. Spectrum licensing is tightly controlled by national regulators whose timelines and technical requirements vary substantially across jurisdictions, forcing manufacturers and operators to navigate fragmented compliance environments that delay product rollouts and inflate operational costs. For global satellite operators, deploying modem networks across multiple regions simultaneously, these regulatory inconsistencies create uncertainty in investment planning and can significantly extend the time-to-market. Additionally, orbital slot congestion and increasing interference risks between adjacent satellites elevate engineering complexity for modem designers.

MARKET OPPORTUNITIES

Expanding 5G Non-Terrestrial Network Integration and IoT Proliferation is Unlocking New Market Growth Opportunities

The convergence of satellite communication with 5G non-terrestrial networks and the rapid proliferation of IoT devices across industries are opening substantial new revenue avenues for satellite modem manufacturers. Telecom operators seeking to extend mobile broadband coverage into rural and remote corridors are increasingly evaluating satellite backhaul as a viable complement to terrestrial infrastructure, driving demand for compatible modem hardware. Simultaneously, industrial IoT deployments across agriculture, energy, and logistics sectors require reliable, low-latency satellite connectivity for real-time asset monitoring and data transmission, creating addressable demand well beyond conventional broadband applications and broadening the overall market scope.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in SATCOM Devices Present a Critical Operational Threat

Despite strong growth momentum, the satellite modem market faces a serious structural challenge due to rising cybersecurity vulnerabilities. SATCOM devices, due to their remote deployment and often limited on-site management, represent an exposed attack surface for state-sponsored and criminal cyber attacks. Incidents such as the Viasat KA-SAT network disruption at the outset of the Ukraine conflict in 2022 demonstrated the real-world consequences of modem-level cyberattacks on critical infrastructure. Strengthening firmware against intrusion, deploying encrypted communication channels, and enabling remote patch management without service interruption are engineering challenges that add both cost and development complexity, particularly for modems deployed in mission-critical defense or energy environments.

Segmentation Analysis

By Offering

Expansion of Higher-Capacity Satellites and Versatile Network Architectures to Sustain the Leading Position of Satellite Modem Segment

Based on the offering, the market is segmented into satellite modems, embedded modem modules / modem cards, software-defined modems, modem management software, services, and others.

The satellite modems segment is anticipated to account for the largest market share. The segment is growing as it serves as the foundational hardware layer delivering all satellite network services to end users. As operators launch higher-capacity HTS and LEO satellites, there is a consistent procurement demand across multi-orbit, multi-frequency networks for recurring hardware upgrade cycles and software-defined platforms.

The software-defined modems segment is anticipated to rise with a CAGR of 10.15% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Modem Type

Enterprise & Maritime -Grade Communication Reliability Propels VSAT Modems’ Market Leadership

Based on modem type, the market is segmented into VSAT modems, SCPC modems, DVB-S2 / DVB-S2X modems, software-defined radio modems, secure / encrypted SATCOM modems, and others.

In 2025, the VSAT modems segment dominated the global market as it remains the backbone of enterprise and maritime satellite communication, offering dedicated bandwidth and predictable latency for mission-critical operations. Furthermore, consistent hardware upgrade cycles driven by the transition to HTS-compatible platforms are reinforcing sustained segment demand across commercial and government end users.

The software-defined radio modems is projected to grow at a high CAGR of 10.08% over the forecast period.

By Satellite Orbit

Persistent Coverage Consistency Has Placed GEO Satellite Modems Most Favored Satellite Orbit

Based on the satellite orbit, the market is segmented into GEO satellite modems, MEO satellite modems, LEO satellite modems, multi-orbit satellite modems, and others.

The GEO satellite modems segment is anticipated to witness a dominating market share over the forecast period. The segment is growing as geostationary satellites provide unmatched coverage consistency, making them indispensable for broadcast distribution, enterprise backbones, and safety-critical communications.

The multi-orbit satellite modems segment is projected to grow at a high CAGR of 9.97% over the forecast period.

By Platform

Ground Infrastructure Stability and High-Throughput Terminal Capacity Support Fixed Ground Terminal Dominance

Based on platform, the market is segmented into fixed ground terminals, portable / manpack terminals, vehicle-mounted terminals, maritime terminals, aeronautical terminals, and others.

The fixed ground terminals segment dominated the market share as permanent installations at enterprise sites, military bases, and teleports represent the highest-volume procurement segment, accommodating larger antennas and more powerful modem hardware.

In addition, aeronautical terminals are projected to grow at a high CAGR of 10.15% during the forecast period.

By Application

Universal Connectivity High-Speed Internet Positions Broadband Connectivity as the Dominant Application

Based on application, the market is segmented into broadband connectivity, cellular backhaul, government & defense communications, maritime connectivity, in-flight connectivity, and others.

The broadband connectivity segment dominated the segmental market share as connecting remote worksites, underserved populations, and mobility platforms to high-speed internet remains the most broadly pursued satellite use case across commercial and government programs.

In addition, government & defense communications are projected to grow at a high CAGR of 9.97% over the forecast period.

By End User

Transition Towards Satellite-Dependent Operations is Driving Rapid Modem Adoption Across Defense & Military End Users

Based on end user, the market is segmented into defense & military, telecom operators / mobile network operators, aviation companies, maritime operators, satellite operators, and others.

Defense & military segment dominated the market share as armed forces globally are transitioning toward satellite-dependent operations requiring advanced modems with encrypted, anti-jam, and multi-orbit capabilities.

In addition, aviation companies are projected to grow at a CAGR of 9.97% during the forecast period.

Satellite Modem Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and Rest of the World.

North America

North America Satellite Modem Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant satellite modem market share in 2024, valuing at USD 0.40 billion, and also maintained the leading share in 2025, with USD 0.46 billion. Growth is driven by strong U.S. defense communication requirements, ongoing military modernization programs, and rapid deployment of LEO constellations requiring compatible ground-segment modems. The region benefits from sustained government investment in tactical networking, secure SATCOM, and high-throughput satellite infrastructure.

U.S Satellite Modem Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.31 billion in 2026, growing at roughly 9.56% CAGR. Expansion is fueled by rising defense communication needs, multi-year Army and Air Force contracts for high-speed satellite modems, and integration of software-defined architectures into tactical networks. Strong R&D investment and commercial-military dual-use technology development further accelerate the adoption.

Europe

Europe is projected to record a steady growth rate of 9.36% during the forecast period, which is the second highest among all regions, and reach a valuation of USD 0.31 billion by 2026. Growth stems from evolving consumer demand for high-speed connectivity, technological advancements in modem design, and government-backed satellite digital connectivity initiatives.

U.K Satellite Modem Market

The U.K. market in 2026 is estimated at around USD 0.10 billion, growing with roughly 9.79% CAGR during the forecast period. The U. K’s modem market is expanding due to the MoD's Skynet program requiring next-generation secure military modems, with Airbus delivering U.K.-made systems.

Germany Satellite Modem Market

Germany’s market is projected to reach approximately USD 0.09 billion in 2026. Germany leads in optical/laser satellite communication modems, with Tesat-Spacecom deploying gigabit-per-second optical terminals. This technological leadership in secure, high-speed data relay drives modem innovation and export competitiveness.

Asia Pacific

Asia Pacific region is estimated to reach USD 0.28 billion in 2026 and secure the position of third-largest and fastest growing region in the satellite modem market during the forecast period. The regional market growth is driven by state-led space strategies, rapid LEO constellation development, and government-backed optical satellite communication programs. Demand for rural broadband, maritime connectivity, and defense SATCOM further accelerates modem adoption.

China Satellite Modem Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.09 billion. Growth is propelled by state-led expansion of satellite infrastructure aligned with national space development strategy. Massive investments in LEO constellations, high-throughput satellites, and optical communication systems drive modem demand.

India Satellite Modem Market

The India market in 2026 is estimated at around USD 0.08 billion. Growth is fueled by Digital India initiatives, 5G satellite communication integration, and government support for rural internet connectivity. Rising demand for high-speed links in remote areas, combined with ISRO/Antrix commercial activities and private sector LEO launches, accelerates modem deployment.

Rest of the World

The rest of the world include Middle East and Africa and Latin America. Growth is driven by maritime shipping, aviation connectivity, oil & gas exploration, and defense operations where terrestrial infrastructure is absent. Latin America benefits from expanding SATCOM demand for remote areas. Middle East & Africa see strong defense modem contracts and VSAT deployments for secure mission-critical communications. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.12 billion and USD 0.08 billion in 2026, respectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Integration of Technical Advancements By Prominent Players is Reshaping the Competitive Landscape

The satellite modem market is moderately consolidated, led by Viasat Inc., Hughes Network Systems (EchoStar), ST Engineering iDirect, Comtech EF Data, Gilat Satellite Networks, Teledyne Technologies, and Novelsat. Furthermore, MDA Space's acquisition of SatixFy strengthened its software-defined modem portfolio.

Technical advancements are defining the competition as vendors are contesting to deliver software-defined, LEO-compatible, and high-throughput modems. Hughes launched its Jupiter 4 modem platform with multi-gigabit speeds and integrated cloud-based network management for enterprise and maritime segments. ST Engineering iDirect's Intuition suite embeds container-based network functions to accelerate service rollouts. The industry is shifting toward modems supporting dynamic beam handovers, multi-band operation, and virtualized network functions, enabling agile waveform updates and reduced hardware refresh cycles as LEO constellations like Starlink and OneWeb demand compatible ground-segment infrastructure.

LIST OF KEY SATELLITE MODEM COMPANIES PROFILED

- Viasat Inc. (U.S.)

- Hughes Network Systems LLC (U.S.)

- ST Engineering (Singapore)

- Comtech Telecommunications Corp. (U.S.)

- Gilat Satellite Networks Ltd. (Israel)

- Teledyne Technologies (U.S.)

- NOVELSAT (Israel)

- ORBCOMM Inc. (U.S.)

- Datum Systems (U.S.)

- WORK Microwave GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The U.S. Army received the first set of Enterprise Digital Intermediate Frequency Multicarrier ("EDIM") modems, from Comtech Telecommunications Corp. ("Comtech" or "the Company"), a leader in communications technology for a contract worth USD 48.6 million.

- May 2025: iDirect Government (iDirectGov), a premier satellite communications provider for the U.S. military and government, announced the successful integration and testing of its 450 Software Defined Radio (SDR) satellite modem with Airbus DS Government Solutions' Ranger Flyaway Terminal.

- February 2025: Viasat, Inc. announced that Inmarsat Government, operating as Viasat, has been awarded a Task Order to deliver satellite communications (SATCOM) services as part of the Proliferated Low Earth Orbit (PLEO) Satellite-Based Services (SBS) Indefinite Delivery, Indefinite Quantity (IDIQ) contract. This contract was granted in 2023 to several vendors by the U.S. Defense Information Systems Agency (DISA) on behalf of the U.S. Space Force and Space Systems Command (SSC) Commercial Satellite Communications Office (CSCO).

- November 2024: The U.S. Navy Information Warfare Systems Command awarded Comtech Telecommunications Corp. a sole source contract for its U.S. sovereign software-defined SLM-5650B satellite communications ("SATCOM") modems, upgrade kits, firmware options, and technical support. The contract is worth more than USD 50.0 million and has a four-year performance period.

- February 2024: A multimillion-dollar defense satellite connectivity project has been awarded to Gilat Satellite Networks Ltd., a global leader in satellite networking technology, solutions, and services.

REPORT COVERAGE

The global satellite modem industry analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements the regulatory environment, porter’s five forces analysis, company profiles and retrofitting program. Additionally, it details partnerships, mergers & acquisitions, as well as key aviation industry developments and prevalence by key regions. The global market report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.31% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Modem Type, Satellite Orbit, Platform, Application, End User and Region |

| By Offering |

|

| By Modem Type |

|

| By Satellite Orbit |

|

| By Platform |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.19 billion in 2025 and is projected to reach USD 2.63 billion by 2034.

In 2025, the market value stood at USD 0.46 billion.

The market is expected to grow at a CAGR of 9.31% during the forecast period of 2026-2034.

By offering, the satellite modems segment is expected to dominate the market.

Increasing Demand for High-Speed Broadband Connectivity in Remote and Underserved Regions Accelerating Market Expansion

Viasat Inc., Hughes Network Systems (EchoStar), ST Engineering iDirect, Comtech EF Data, Gilat Satellite Networks, Teledyne Technologies, and Novelsat are the key players in the global market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us