Second Life EV Battery Market Size, Share & Industry Analysis, By Battery Type (Lithium-ion (NMC/NCA), Lithium-ion (LFP) and Lithium-ion (LMO / blended)), By End User (Utilities & Grid Operators, Commercial & Industrial Users, Residential Users and Telecom & Infrastructure Operators), By Technology (Standalone Second-Life Battery Systems, Hybrid Systems, and Software-managed Energy Storage Platforms), and Regional Forecast, 2026-2034

second life electric vehicle battery market Overview

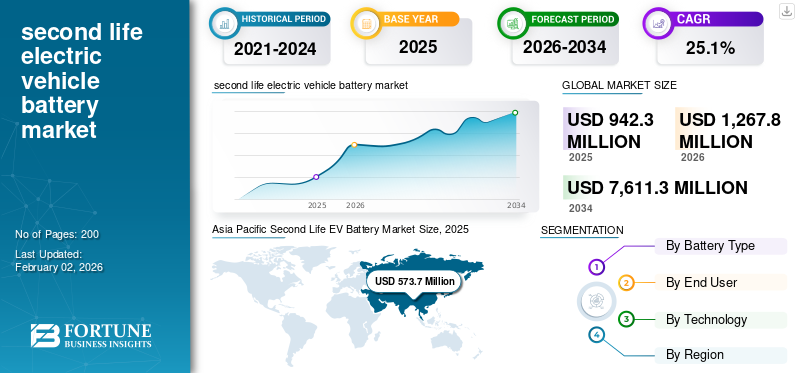

The global second life EV battery market size was valued at USD 942.3 million in 2025. The market is projected to grow from USD 1,267.8 million in 2026 to USD 7,611.3 million by 2034, exhibiting a CAGR of 25.1% during the forecast period. Asia Pacific dominated the global market with a market share of 60.86% in 2025.

The second Life EV battery market refers to the commercial ecosystem focused on the collection, assessment, refurbishment, and redeployment of lithium-ion batteries retired from electric vehicles into secondary, non-automotive applications. These electric vehicle batteries, although no longer meeting the stringent performance requirements of EV propulsion, typically retain sufficient capacity and reliability for stationary energy storage applications, such as residential, commercial & industrial (C&I), grid support, renewable energy integration, backup power, and microgrid systems. The second Life EV Battery market encompasses activities such as lithium-ion battery health diagnostics, disassembly, remanufacturing or reconfiguration, system integration with power electronics and battery management systems, and final deployment. Recycling activities and the use of newly manufactured battery cells are excluded from the scope unless explicitly stated.

Key market players in the second life EV Battery market include EV OEMs, battery manufacturers, energy storage integrators, and specialized electric vehicle battery lifecycle management companies. The major player in the market include Connected Energy, Element Energy and B2U Storage Solutions Automotive. OEMs and cell manufacturers are increasingly vertically integrating second-life solutions to optimize the value of residual batteries and comply with circular economy and sustainability mandates. Energy storage system providers and infrastructure companies play a critical role in adapting second-life batteries to stationary applications by addressing performance variability, safety certification, and system-level reliability. Battery diagnostics capabilities, scalable refurbishment processes, cost-effective system performance guarantees, and strategic partnerships across the EV, energy, and utilities value chain drive competitive differentiation in this market.

Download Free sample to learn more about this report.

Second Life EV Battery Market KEY TAKEAWAYS

- 2025 Market Size: USD 942.3 million

- 2026 Market Size: USD 1,267.8 million

- 2034 Forecast Market Size: USD 7,611.3 million

- CAGR: 25.1% from 2026–2034

- Asia Pacific dominated the market with a 60.86% share in 2025.

- Lithium-ion (LFP) segment is projected to grow at the fastest CAGR of 26.1% from 2026–2034.

- Commercial & industrial users segment is projected to grow at the fastest CAGR of 26.3% from 2026–2034.

Asia Pacific

Dominates the market, driven by rapid EV adoption, large-scale battery manufacturing, and growing renewable energy deployment.

North America

A key market, supported by expanding EV adoption, grid modernization, and increasing investments in energy storage.

Europe

Witnessing steady growth, driven by circular economy policies, high EV adoption, and demand for sustainable energy storage.

U.S.

Expected to witness steady growth, supported by rising grid-scale storage projects and renewable energy integration.

Japan

Expected to witness steady growth, driven by expanding EV adoption and increasing focus on battery reuse and energy storage solutions.

Read More

SECOND LIFE EV BATTERY MARKET TRENDS

Increasing Integration of Second-life Batteries into Stationary Energy Storage Systems Is Shaping Market Evolution

The growing integration of second-life EV batteries into stationary demand for energy storage systems is a prominent trend influencing the development of the Second Life EV Battery market. As energy storage demand rises across residential, commercial & industrial, and grid-support applications, stakeholders are increasingly deploying repurposed batteries where energy density and weight constraints are less critical than cost and sustainability. These batteries are being utilized for applications such as peak shaving, backup power, renewable energy smoothing, and microgrid support, offering a viable and economical alternative to newly manufactured storage systems. Improvements in battery health diagnostics, system integration, and performance monitoring are further enabling smoother adoption in stationary environments. This trend reflects a broader market shift toward maximizing the value of battery lifecycles while supporting energy transition goals, thereby strengthening the commercial viability of second Life EV Battery solutions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing EV Adoption Accelerates Market Growth

The rapid increase in electric vehicle adoption worldwide is a major factor driving the growth of the second Life EV battery market. As EV sales continue to rise, a growing volume of lithium-ion batteries is reaching the end of their first-life automotive usage due to capacity degradation rather than complete failure. These old batteries retain substantial residual capacity, making them suitable for secondary applications such as stationary energy storage. The expanding stock of end-of-life EV batteries thereby increases the availability of raw materials for second-life solutions and improves supply-side visibility for market participants. This growing battery pool is encouraging OEMs, energy storage providers, and refurbishment specialists to invest in testing, remanufacturing, and redeployment capabilities. Consequently, the increasing penetration of electric vehicles is directly accelerating the commercialization and adoption of second Life EV battery systems across multiple energy storage applications.

MARKET RESTRAINTS

Variability in Battery Health Is Restricting the Growth of the Second-life EV Battery Market

High variability in battery health, performance, and remaining useful life is a key factor restraining the growth of the second Life EV Battery market. EV batteries reaching the end of their vehicle use exhibit significant differences in degradation levels due to variations in driving behavior, charging patterns, thermal exposure, and battery chemistry. This inconsistency makes the accurate assessment of the state of health (SoH) and remaining lifespan challenging, thereby increasing uncertainty for second-life deployment. As a result, refurbishing and integrating these batteries into reliable stationary energy storage systems requires extensive testing, sorting, and customization, which raises operational costs and limits scalability. The lack of predictable performance and standardized quality benchmarks also affects warranty offerings and project bankability, discouraging utilities and commercial users from large-scale adoption. Collectively, these factors limit the commercialization potential of second Life EV Battery solutions, despite increasing battery availability.

MARKET OPPORTUNITIES

Expansion of EV Charging Infrastructure Is Creating Growth Opportunities for the Second-life EV Battery Market

The rapid expansion of electric vehicle charging infrastructure is creating a significant opportunity for the second Life EV Battery market, as charging operators increasingly require on-site energy storage to manage power demand and grid constraints. High-power fast-charging stations often place a substantial load on local grids, leading to high demand charges and infrastructure upgrade costs. Second-life EV batteries provide a cost-effective solution for energy buffering, peak shaving, and load balancing at charging stations, while also supporting the integration of renewable energy sources, such as rooftop solar. Their lower upfront cost compared to new battery systems makes them particularly attractive for public, commercial, and fleet-based charging installations. As governments and private players accelerate investments in EV charging networks, the need for economical and sustainable on-site energy storage is expected to drive increased adoption of Second Life EV Battery systems, thereby unlocking new revenue streams for market participants.

MARKET CHALLENGES

Safety Risks Related to Thermal Management and Fire Hazards Are Challenging Product Adoption

Safety risks associated with thermal management and fire hazards represent a significant challenge for the second Life EV Battery market. Retired EV batteries often exhibit uneven degradation, internal defects, or cell-level inconsistencies that can increase the risk of thermal runaway when repurposed for stationary applications. Managing heat dissipation, ensuring stable operating conditions, and integrating reliable battery management systems become more complex when batteries originate from varied usage histories and chemistries. These safety concerns raise apprehension among end users, insurers, utilities, and regulators, leading to stringent compliance requirements and higher system integration costs. Consequently, addressing fire safety and thermal stability remains crucial for enhancing market confidence and facilitating the wider commercial deployment of second Life EV Battery systems.

Segmentation Analysis

By Battery Type

Lithium-ion (NMC/NCA) Batteries Segment Leads due to its Growing Usage in EVs

Based on battery type, the second-life EV battery market is segmented into lithium-ion (NMC/NCA), lithium-ion (LFP), and lithium-ion (LMO/blended) batteries.

The lithium-ion (NMC/NCA) segment dominates the market owing to its extensive use in electric vehicles and a favorable combination of energy density and performance characteristics. NMC (Nickel-Manganese-Cobalt) and NCA (Nickel-Cobalt-Aluminum) chemistries have been widely adopted by EV manufacturers for long-range and high-performance EV models, resulting in a substantial installed base of these batteries entering retirement. This large retiree pool enhances availability for second life applications and supports economies of scale for repurposing initiatives. In addition, established diagnostic methodologies and refurbishing expertise for NMC/NCA chemistries further streamline the integration of these chemistries into stationary energy storage systems. The continuous expansion of EV production with these chemistries reinforces their segmental lead and positions NMC/NCA battery reuse as a central driver of the second Life EV Battery market.

The Lithium-ion (LFP) segment is poised to grow at a CAGR of 26.1%, showcasing the fastest growth over the analysis period.

By End User

Rising Demand for Grid Flexibility to Drive Dominance of Utilities & Grid Operators Segment

Based on end user, the second-life EV battery market is segmented into utilities & grid operators, commercial & industrial users, residential users, and telecom & infrastructure operators.

The utilities & grid operators segment is expected to account for the dominant market share, driven by the increasing need for flexible, cost-effective energy storage solutions to support grid stability and renewable energy integration. Utilities are deploying second life EV batteries for applications such as peak load management, frequency regulation, renewable energy smoothing, and backup power, where energy density constraints are relatively low and cost efficiency is critical. The availability of large-scale battery capacities from retired EV fleets aligns well with utility-scale storage requirements, making second life batteries an attractive alternative to new systems. Furthermore, grid operators are under growing pressure to modernize their aging infrastructure and manage the intermittency of solar and wind power sources, which further accelerates their adoption. These factors, combined with the pilot-to-commercial scale transition of utility-led storage projects, are reinforcing the dominant position of the segment in the second Life EV battery market.

The commercial & industrial users segment is poised to grow at a CAGR of 26.3%, showcasing the fastest growth over the study period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Cost-Effective Deployment Supports the Dominance of Standalone Second-life Battery Systems

Based on technology, the second-life EV battery market is segmented into standalone second-life battery systems, hybrid systems, and software-managed energy storage platforms.

The standalone second-life battery systems segment holds a dominant position in the market, primarily due to its relatively simple architecture, lower integration complexity, and cost advantages. These systems involve direct repurposing of retired EV batteries into stationary storage units without extensive coupling with new batteries or advanced digital platforms, making them easier and faster to deploy. Utilities, commercial users, and infrastructure operators are increasingly opting for standalone systems for applications such as backup power, peak shaving, and renewable energy support, where basic energy storage functionality is sufficient. Additionally, the lower upfront investment and reduced technical risk associated with standalone configurations enhance their attractiveness, particularly in early-stage and pilot deployments. As a result, the widespread adoption and scalability of standalone second-life battery systems continue to reinforce their dominance within the technology segment.

The hybrid systems segment is poised to grow at a CAGR of 26.4%, showcasing the fastest growth over the analysis period.

Second Life EV Battery Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Second Life EV Battery Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is dominated region for the second-life EV battery market, driven by rapid EV adoption, large-scale battery manufacturing, and expanding renewable energy deployment. Countries in the region have a substantial installed base of EV batteries, creating strong long-term potential for second-life applications. Utilities and industrial users are increasingly seeking cost-effective energy storage solutions to address grid congestion and support the integration of renewable energy sources. Additionally, growing investments in EV charging infrastructure and microgrid projects are creating new opportunities for the utilization of second-life batteries. Advancements in battery refurbishing capabilities and cost-sensitive energy markets further enhance regional growth prospects.

China

China’s market growth is fueled by its massive EV fleet, large battery manufacturing base, and increasing focus on cost-effective energy storage solutions to support grid stability and renewable energy expansion.

North America

North America represents a prominent market for second-life EV batteries, driven by the growing adoption of electric vehicles, expanding renewable energy capacity, and a strong focus on grid modernization. The region has a well-established EV ecosystem, resulting in an increasing volume of retired lithium-ion batteries suitable for secondary use. Utilities and grid operators are actively exploring second-life battery deployments for peak shaving, grid balancing, and renewable energy integration to manage rising electricity demand and challenges associated with intermittency. Additionally, supportive sustainability initiatives, corporate decarbonization targets, and investments in energy storage infrastructure are accelerating the adoption of these technologies. The presence of advanced battery diagnostics capabilities and technology-driven energy storage companies further strengthens the region’s market position.

U.S.

Rising EV adoption, expanding grid-scale energy storage deployments, and increasing investments in grid resilience and renewable energy integration are driving demand for second-life EV battery systems across the U.S.

Europe

Europe is experiencing steady growth in the second-life EV battery market, driven by stringent environmental regulations, circular economy mandates, and ambitious electrification goals. The region places strong emphasis on extending battery lifecycles to reduce waste and dependency on raw material imports. Utilities and energy companies are increasingly adopting second-life batteries for stationary storage applications, particularly for integrating renewable energy and providing grid support. High EV adoption rates across major economies are contributing to a growing supply of end-of-life electric vehicle (EV) batteries. Furthermore, policy-driven support for sustainable energy systems and cross-industry collaborations between automakers and energy providers are fostering market development across Europe.

U.K.

The U.K.’s second-life EV battery market is driven by strong decarbonization targets, rapid EV adoption, grid balancing needs, and increasing deployment of stationary energy storage to support renewable energy integration.

Rest of the World

The Rest of the World region, encompassing Latin America and the Middle East and Africa, is currently at an early stage of adoption in the second-life EV battery market, yet it offers significant long-term growth potential. The increasing number of renewable energy projects, challenges to grid reliability, and growing interest in affordable energy storage solutions are driving initial demand. Second-life EV batteries are gaining attention for applications such as backup power, off-grid systems, and microgrids, particularly in regions with limited grid infrastructure. Although EV penetration remains comparatively lower, gradual electrification trends and improving energy storage awareness are expected to support the market’s gradual expansion over the forecast period.

COMPETITIVE LANDSCAPE

Strategic Partnerships and Lifecycle Management Initiatives by Key Players to Propel Market Progress

The global second-life EV battery market exhibits a moderately fragmented to semi-consolidated competitive landscape, with participation from EV OEMs, battery manufacturers, energy storage system integrators, and specialized companies focused on battery lifecycle management. Key players maintain their market positions through strategic initiatives, including partnerships, pilot deployments, and vertical integration across battery collection, diagnostics, refurbishment, and stationary energy storage deployment. Automotive OEMs and battery producers are increasingly utilizing second-life solutions to enhance the residual value of batteries, support sustainability goals, and comply with circular economy regulations. Their strong access to end-of-life battery supply provides a competitive advantage over independent players.

Other notable players in the market include energy storage system providers, power electronics companies, and technology firms specializing in battery analytics and lifecycle software platforms. These players are expected to focus on scaling refurbishment capabilities, improving safety and performance assurance, and expanding regional deployments through collaborations with utilities and infrastructure operators. Such strategic efforts are anticipated to intensify competition and drive market expansion over the forecast period.

LIST OF KEY SECOND LIFE EV BATTERY MARKET COMPANIES PROFILED

- Connected Energy (U.K.)

- Element Energy (U.S.)

- B2U Storage Solutions (U.S.)

- Zenobē Energy Limited (U.K.)

- BeePlanet Factory (Spain)

- Allye Energy (U.K.)

- Smartville (U.S.)

- Forsee Power (France)

- Renault Group (France)

- Toyota Motor Corporation (Japan)

- Tokyo Electric Power Co. Holdings (Japan)

KEY INDUSTRY DEVELOPMENTS

- December 2025- B2U launched its first structured finance fund, comprising seven second-life battery BESS projects across California and Texas, with the intention of accelerating large-scale deployments and expanding its grid storage footprint.

- December 2025- General Motors and Redwood Materials signed a memorandum of understanding to accelerate the deployment of energy storage systems incorporating both new, US-manufactured, and second-life EV battery packs, thereby expanding domestic reuse and energy resilience efforts.

- May 2025- Forsee Power extended its collaboration with Connected Energy to design and deliver a modular second-life battery energy storage solution using retired EV and electric bus batteries across Europe.

- June 2025- Redwood Materials partnered with Crusoe to unveil what was described as North America’s largest second-life battery microgrid, using repurposed EV batteries to power modular AI data centers off-grid.

- October 2024- Nissan Americas announced the deployment of two second-life battery energy storage systems at its Franklin, Tennessee headquarters, utilizing retired Nissan LEAF batteries to offset peak electricity demand, thereby helping validate the stationary repurposing of batteries in corporate facilities.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 25.1% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Battery Type, By End User, By Technology, and By Region |

|

By Battery Type |

· Lithium-ion (NMC/NCA) · Lithium-ion (LFP) · Lithium-ion (LMO/blended) |

|

By End User |

· Utilities & grid operators · Commercial & industrial users · Residential users · Telecom & infrastructure operators |

|

By Technology |

· Standalone second-life battery systems · Hybrid systems · Software-managed energy storage platforms |

|

By Geography |

· North America (By Battery Type, By End User, By Technology, and by Country) o U.S. (By End User) o Canada (By End User) o Mexico (By End User) · Europe (By Battery Type, By End User, By Technology, and by Country) o Germany (By End User) o U.K. (By End User) o France (By End User) o Rest of Europe (By End User) · Asia Pacific (By Battery Type, By End User, By Technology, and by Country) o China (By End User) o Japan (By End User) o India (By End User) o Rest of Asia Pacific (By End User) · Rest of the World ( By Battery Type, By End User, By Technology, and by Country ) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 942.3 million in 2025 and is projected to reach USD 7,611.3 million by 2034.

In 2025, the market value stood at USD 573.70 million.

The market is expected to exhibit a CAGR of 25.1% during the forecast period (2026-2034).

The Lithium-ion (NMC/NCA) segment leads the market by battery type.

Increasing EV Adoption is the key factor driving market growth.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us