Self Defense Weapons Market Size, Share & Industry Analysis, By Weapons Type (Non-lethal/less-lethal Weapons (Conducted Energy Devices (CED), Chemical Irritant Devices, Impact & Control Tools, and Acoustic and Visual Deterrents) and Lethal Self defense Weapons (Personal Firearms and Edged and Impact Weapons)), By End-user (Military, Law Enforcement, Civilians, and Private Security), By Application (On-Duty Professional Carry, Off-Duty/Personal Carry by Professionals, Civilian Personal, Sport/Training & Practice, and Crowd Management & Public Order), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

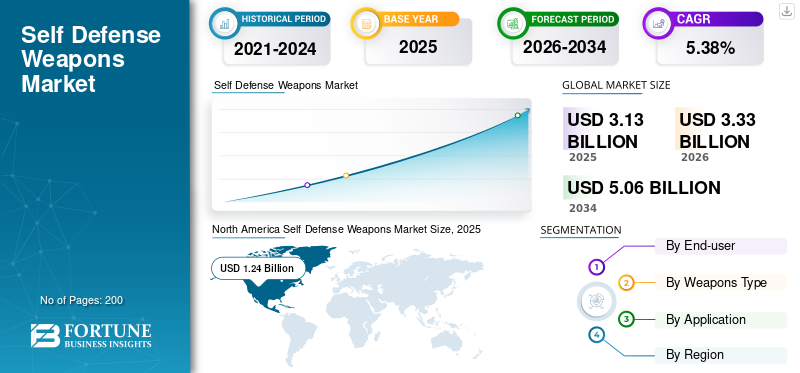

The global self defense weapons market size was valued at USD 3.13 billion in 2025. The market is projected to grow from USD 3.33 billion in 2026 to USD 5.06 billion by 2034, exhibiting a CAGR of 5.38% during the forecast period. North America dominated the global market with a market share of 39.62% in 2025.

Self defense weapons are personal protection and defense tools designed to help individuals deter, disable, or escape an immediate threat at close range. They span lethal solutions, such as compact handguns, and a rapidly growing set of less-lethal options, including pepper sprays, stun guns, conducted-energy weapons, and CO₂-powered launchers. The rising perceptions of personal and workplace risk are expanding the demand from civilian users, corporate security programs, and public-sector agencies. Additionally, regulators, insurers, and employers are increasingly favoring less-lethal force options to reduce liability and reputational risk, which directly drives the demand for conducted-energy weapons, sprays, and launchers.

Furthermore, product innovation and branding are repositioning self-defense weapons from niche self-defense gear to lifestyle safety products, supported by training content, mobile apps, and subscription models. Taken together, these dynamics are creating a resilient growth runway in which Axon (TASER), Byrna, Mace, and SABRE emerge as reference players. At the same time, firearm manufacturers and regional specialists compete for share in specific channels, price points, and regulatory environments.

Download Free sample to learn more about this report.

SELF DEFENSE WEAPONS MARKET TRENDS

Shift toward GNSS-Based and Automated Inspection Systems Poses as a Technological Trend

The most prominent technological trend in the market is the shift toward GNSS-based navigation validation and automated flight profiles. These systems enable higher accuracy in navigation aid calibration while minimizing human error and mission duration. Advanced data logging, AI-assisted route planning, and real-time signal integrity assessment tools are enhancing the efficiency of self defense weapons. The adoption of dual-use inspection aircraft capable of handling both conventional and satellite-based systems is increasing among ANSPs and defense operators. Automation is also extending into mission management, improving repeatability and operational safety.

- In August 2025, Germany’s Aerodata AG unveiled an upgraded automated self defense weapons system integrating GNSS signal mapping and AI-driven mission planning, designed for both civil and defense calibration fleets.

MARKET DYNAMICS

MARKET DRIVERS

Shift toward Less-Lethal “Middle Ground” Self-Defense to Drive Market Growth

The self defense weapons market growth is increasingly driven by the demand for a less lethal usage of a firearm. Households, employers, and public agencies are seeking tools that deter or disable an attacker while minimizing the risk of fatalities, political backlash, and litigation. This expands the overall industry beyond traditional gun owners to include first-time buyers, corporate security programs, and public-sector customers. Less-lethal projectile launchers, conducted-energy weapons, and smart pepper sprays are being positioned as everyday safety products rather than niche tactical gear, supported by training, digital content, and brand-led communities. The result is a structural shift in spending from purely lethal platforms to a broader personal-safety portfolio, with a strong pull in North America and a gradual catch-up in Europe and Asia.

MARKET RESTRAINTS

Regulatory Fragmentation and Legal Uncertainty to Act as a Restraint for Market Growth

Despite attractive growth fundamentals, the self defense weapons market is constrained by a fragmented and volatile regulatory environment. The definitions of “firearm,” “electronic weapon,” and “chemical spray” vary widely by jurisdiction, affecting who may purchase, carry, or sell devices and under what conditions. For manufacturers and distributors, this creates complex compliance requirements, frequent label changes, and limitations on direct-to-consumer channels. For end users, legal ambiguity surrounding where products can be carried (e.g., schools, public transport, workplaces) hinders adoption and increases perceived legal risk. Court decisions can also move against the industry, with some judgments with a restrictive view of constitutional protection for stun guns and tasers. To overcome these restraints, companies started designing products and training manuals to avoid conflicts with regulators in the self-defense weapons industry.

- In March 2025, a U.S. federal district judge upheld the New York State and New York City bans on stun guns and tasers, confirming that civilians there remain prohibited from possessing these devices despite broader national liberalization trends.

MARKET OPPORTUNITIES

Institutional and Corporate Security Adoption Posing as a Major Market Opportunity

A significant upside opportunity lies in institutional and corporate security customers that are re-evaluating force options. Large employers, logistics operators, critical infrastructure sites, and correctional systems are under pressure to protect their staff while limiting lethal-force incidents and associated liabilities. For vendors, this opens multi-year frameworks for conducted-energy weapons, launchers, pepper spray, and training services, often bundled with digital evidence and incident-management tools. As self-defense technology becomes more standardized and auditable, it becomes easier for boards, insurers, and regulators to accept less-lethal solutions as part of formal duty-of-care programs.

- In August 2025, Axon raised its 2025 revenue forecast on the back of strong demand for self-defense and its TASER devices and security technology from government and corporate customers. This also includes a large international logistics firm seeking to upgrade non-lethal capabilities.

MARKET CHALLENGES

Safety, Misuse, and Effectiveness under Scrutiny Present Threats to Market Growth

The self defense weapons market faces challenges around safety, misuse, and real-world performance. Increased civilian deployment has led to more accidental discharges and secondary exposure incidents in crowded environments, prompting calls for tighter training and clearer labelling. At the same time, law-enforcement data and independent reviews have highlighted non-trivial failure rates for some conducted-energy weapons, raising questions about reliability in high-stress scenarios and fueling activist and media criticism. Misuse cases—such as assaults involving legally purchased sprays or devices used outside lawful self-defense—create reputational and regulatory risk for the category as a whole. Vendors, therefore, must invest in product design, training content, usage analytics, and transparent incident reporting to maintain stakeholder confidence, especially as volumes grow.

Download Free sample to learn more about this report.

Segmentation Analysis

By Weapons Type

Lethal Self-Defense Weapons Segment to Grow Due to Higher Unit Price of Lethal Weapons and Growing Demand

Based on weapons type, the market is classified into non-lethal/less-lethal weapons and lethal self-defense weapons.

The lethal self-defense weapons segment is the largest weapon type, accounting for over 60% of global market. This dominance of the segment is driven by the comparatively higher unit price of lethal weapons as compared to non-lethal weapons, with a stagnant civilian demand for personal protection, and compulsory sidearm procurement process across military and law-enforcement uses. Additionally, defense regulatory bodies continue to prioritize compact lethal weapons for close-encounters and protective roles, leading to overall segmental growth.

- In November 2024, the U.S. Army awarded new contracts for next-generation SIG Sauer M17/M18 sidearm to expand availability across active duty and National Guard units, reinforcing continued global investment into lethal personal-defense weapons.

The non-lethal/less-lethal weapons segment is expected to grow at a higher CAGR of 5.6% over the forecast period.

By End-User

Law Enforcement Segment to Grow Due to Recurring Bulk Purchases of Weapons

In terms of end-user, the market is categorized into military, law enforcement, civilians, and private security.

The law enforcement segment holds the largest self defense weapons market share as police and security agencies are continuously updating and standardizing their equipment. This leads to recurring bulk purchases of firearms, CEDs, sprays, and batons. Clear policies and officer-safety regulations also secure dedicated budgets for these upgrades in self-defense weapons, keeping law enforcement dominating as compared to civilian and private security demand.

To know how our report can help streamline your business, Speak to Analyst

The civilians segment accounted for a significant share in the global market and is expected to grow at the highest CAGR of 5.96% over 2026-2034.

By Application

On-Duty Professional Carry Segment due to Mandatory Procurement and Replacement Cycle

Based on application, the market is segmented into on-duty professional carry, off-duty/personal carry by professionals, civilian personal, sport/training & practice, and crowd management & public order.

The on-duty professional carry segment is the largest segment and is driven by mandatory, policy-regulated procurement across military, law-enforcement, and licensed security forces. These agencies must equip every active officer with standardized lethal and non-lethal tools, follow strict replacement cycles, and purchase in bulk through multi-year contracts. This creates a steady, high-value demand base that naturally exceeds civilian or discretionary purchasing.

The civilian personal segment accounted for a significant share in the global market and is expected to grow at the highest CAGR of 6.16% from 2026-2034.

Self Defense Weapons Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Self Defense Weapons Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 1.10 billion, and also took the leading share in 2025 with USD 1.24 billion. North America is the largest regional market, underpinned by the U.S.’s dominant share of global defense spending and a sizeable, legally armed civilian population. U.S. defense and homeland-security agencies procure compact carbines, SMGs, PDWs, and less-lethal systems at scale, while federal, state, and municipal police forces represent a major installed base for conducted-energy weapons and connected safety platforms. The civilian market further reinforces volumes through retail channels. Canada contributes a smaller but material demand from national and provincial forces, particularly for less-lethal and patrol-carbine capabilities.

- In April 2025, SIPRI reported that the U.S. military expenditure reached roughly USD 997 billion in 2024, accounting for 37% of global defense spending and providing a substantial anchor for North American weapons demand.

Europe

Europe is the second-largest PDW and self-defense weapons market, driven by a rise in accelerated defense spending and internal security priorities. European NATO members are moving toward or surpassing the 2% of GDP benchmark, triggering upgrades of small arms for both armed forces and gendarmerie, along with expanded less-lethal capabilities for riot and border security units. The war in Ukraine has sharpened the focus on readiness and stockpiles, while recurring protests and migration pressures reinforce the need for scalable response options. Procurement often favors European OEMs but is increasingly open to transatlantic solutions where capability gaps exist.

Asia Pacific

The Asia Pacific region is experiencing rapid growth and is expected to grow at the highest CAGR over 2026-2032. Asia Pacific is the fastest-growing region, reflecting rising defense budgets, complex security environments, and a push for indigenous capability. China, India, Australia, South Korea, and several Southeast Asian states are modernizing close-quarters weapons for armed forces and internal-security units. Programs often blend domestic development with selective imports, as governments seek to reduce dependency on foreign suppliers while improving performance over legacy 9 mm SMGs. Demand is the strongest in counter-insurgency, border security, and urban operations units, where compact carbines and PDWs offer a step change over older platforms without requiring wholesale doctrinal shifts.

Rest of the World

Latin America and the Middle East and Africa collectively represent the smallest regional block by value, yet remain significant in strategic and political terms. Many states face high rates of violent crimes, organized crime, and insurgency, as well as periodic civil unrest. This drives the recurring procurement of compact weapons for police, gendarmerie, and special forces, alongside less-lethal kits for public order and corrections units. However, budget volatility, foreign-exchange constraints, and competing social priorities limit scale and encourage incremental buying, often through government-to-government frameworks. Suppliers from Europe, the U.S., Russia, and emerging local manufacturers all compete in these markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players’ Wide Product Offerings Range and Strong Distribution Network to Support their Dominant Positions

Axon anchors the institutional less-lethal segment with TASER devices integrated into a software and cloud ecosystem, giving it high switching costs and strong pricing power with police and government buyers. Byrna is positioned in the market as a key player in the non-lethal launch weapons category, scaling rapidly through e-commerce and retail channels with CO₂-powered launchers and accessories. Mace competes in personal sprays and alarms while rapidly growing into e-commerce and product partnerships, such as smart pepper sprays and launchers. At the weapons end, firms such as B&T and major rifle OEMs supply PDW-length carbines and SMGs to defense and law enforcement tenders, often via framework contracts. Overall, the market remains fragmented, with regional brands and distributors playing an outsized role in consumer channels.

LIST OF KEY SELF DEFENSE WEAPONS COMPANIES PROFILED

- Axon Enterprise (U.S.)

- Byrna Technologies (U.S.)

- Mace Security International (U.S.)

- SABRE (Security Equipment Corporation) (U.S.)

- Glock GmbH (Austria)

- FN Herstal (Belgium)

- Heckler & Koch GmbH (Germany)

- B&T AG (Switzerland)

- SIG Sauer AG (Switzerland)

- Smith & Wesson Brands, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2025 – Axon reported Q1 2025 revenue of USD 603.6 million, up 31% year on year, and raised full-year revenue guidance to USD 2.6–2.7 billion on strong demand for TASER 10 and Axon Body 4. The beat-and-raise quarter underscores robust institutional spending on less-lethal weapons and connected safety systems.

- February 2025 – Byrna reported its final FY 2024 results, confirming USD 85.8 million in revenue and USD 12.8 million in net income, marking a sharp turnaround from the prior-year losses. The profitability milestone strengthens its position as a leading non-lethal brand, supporting further investment in product development and marketing.

- December 2024 – Byrna Technologies announced preliminary FY 2024 revenues of USD 85.8 million, representing more than 100% growth compared to 2023, with Q4 revenue reaching USD 28 million. The surge, driven by non-lethal launchers and accessories, signals accelerating mainstream adoption of “ungun” self-defense options in consumer and professional channels.

- May 2024 – The City of Pasadena approved a five-year, USD 4.51 million not-to-exceed contract with Axon to consolidate body-worn camera and TASER agreements and add new products. The deal deepens Axon’s municipal footprint and illustrates how weapons are increasingly bundled with sensors and cloud evidence platforms.

- January 2024 – SABRE showcased its SMART Pepper Spray at CES 2024, integrating GPS tracking, app alerts, and 24/7 monitoring to create a connected self-defense device. The launch positions SABRE at the premium end of the consumer segment, pushing the market toward subscription- and service-led safety ecosystems.

- August 2023 – Mace Security International partnered with U.S. LawShield to bundle pepper sprays with nationwide self-defense training and legal-support services, on undisclosed financial terms. The collaboration is designed to expand Mace products into a broader safety offering and is expected to enhance customer lifetime value through paid online and in-person courses.

- January 2023 – Axon launched its TASER 10 energy weapon as a next-generation conducted-energy device with 10 probes and a 45-foot range, aimed at improving standoff distance and hit probability for officers. The launch is expected to accelerate migration from older TASER models and support Axon’s “moonshot” to cut gun deaths in police encounters.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.38% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By End-user, Weapons Type, Application, and Region |

|

By End User |

· Military · Law Enforcement · Civilians · Private security |

|

By Weapons Type |

· Non-lethal/less-lethal Weapons o Conducted Energy Devices (CED) o Chemical Irritant Devices o Impact & Control Tools o Acoustic and Visual Deterrents · Lethal Self defense Weapons o Personal Firearms o Edged and Impact Weapons |

|

By Application |

· On-Duty Professional Carry · Off-Duty / Personal Carry by Professionals · Civilian Personal · Sport / Training & Practice · Crowd Management & Public Order |

|

By Geography |

· North America (By End-user, Weapons Type, Application, and Country) o U.S. (By Weapons Type) o Canada (By Weapons Type) · Europe (By End-user, Weapons Type, Application, and Country ) o U.K. (By Weapons Type) o Germany (By Weapons Type) o France (By Weapons Type) o Russia (By Weapons Type) o Nordic Countries (By Weapons Type) o Rest of Europe (By Weapons Type) · Asia Pacific ( By End-user, Weapons Type, Application, and Country ) o China (By Weapons Type) o India (By Weapons Type) o Japan (By Weapons Type) o Australia (By Weapons Type) o South Korea (By Weapons Type) o Rest of Asia Pacific (By Weapons Type) · Rest of the World ( By End-user, Weapons Type, Application, and Country ) o Latin America (By Weapons Type) o Middle East & Africa (By Weapons Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.14 billion in 2025 and is projected to reach USD 5.06 billion by 2034.

In 2024, the North America market value stood at USD 1.24 billion.

The market is expected to exhibit a CAGR of 5.38% during the forecast period of 2025-2032.

The law enforcement segment leads the market in terms of end-user.

Shift toward less-lethal “middle ground” self-defense is a key factor driving market growth.

Axon Enterprise (U.S.) and Byrna Technologies (U.S.) are two prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us