Semiconductor Bonding Market Size, Share & Growth Analysis, By Process Type (Die-to-Die, Die-to-Wafer, and Wafer-to-Wafer), By Application (Advanced Packaging, Micro-Electro-Mechanical Systems (MEMS) Fabrication, RF Devices, LEDs & Photonics, CMOS Image Sensor (CIS) Manufacturing, and Others), By Type (Flip-Chip Bonders, Wafer Bonders, Wire Bonders, Hybrid Bonders, Die Bonders, Thermocompression Bonders, and Others), and Regional Forecast, 2026-2034

Semiconductor Bonding Market Current & Forecast Market Size

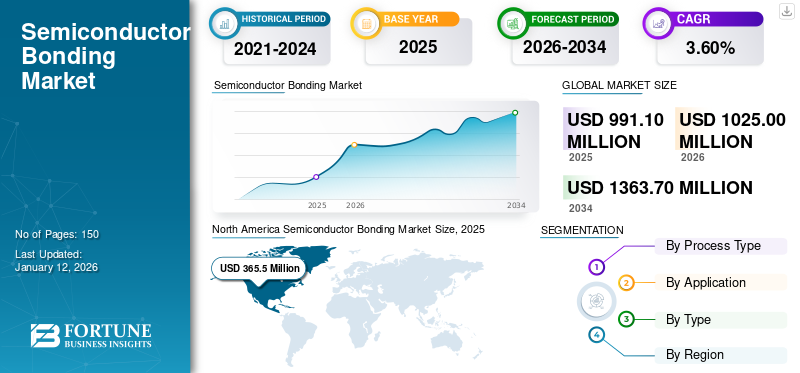

The global semiconductor bonding market size was valued at USD 991.1 million in 2025 and is projected to grow from USD 1025 million in 2026 to USD 1363.7 million by 2034, exhibiting a CAGR of 3.60% during the forecast period. North America dominated the semiconductor bonding market with a market share of 36.90% in 2025.

The market is driven by the continuous evolution in electronics, thus increasing demand for more sophisticated and miniaturized semiconductor devices. Additionally, the rising demand for smartphones, tablets, and other consumer electronics drives the market.

Semiconductor bonding joins semiconductor materials, typically silicon wafers or germanium wafers, to create Integrated Circuits (ICs) and other semiconductor devices. This bonding can be achieved through various methods, including wafer bonding, die bonding, and wire bonding, among others. These techniques are vital for the manufacturing of semiconductor devices, enabling the production of modern electronics from smartphones to advanced computing systems. This bonding caters to various applications, including Microelectromechanical Systems (MEMS) sensors and actuators, creating power electronics, and 3D stacking in advanced packaging, among others.

The COVID-19 pandemic affected the market growth. The lockdowns and restrictions led to significant disruptions in the global supply chain, affecting the availability of raw materials and components. However, the shift to remote work and online education increased the demand for electronic devices, thereby driving the need for semiconductor components.

Also, there is a growing demand for more efficient and compact electronic devices that is pushing the development of advanced packaging technologies, such as System-in-Package (SiP) and 3D ICs, which require sophisticated bonding techniques.

Moreover, the global rollout of 5G networks is driving the need for high-performance semiconductor devices, boosting the market.

Download Free sample to learn more about this report.

Semiconductor Bonding MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 991.1 Million

- 2026 Market Size: USD 1,025.0 Million

- 2034 Forecast Market Size: USD 1,363.7 Million

- CAGR: 3.60% from 2026–2034

- North America dominated the semiconductor bonding market with a 36.90% share in 2025.

- The die-to-die segment is projected to account for 51.89% of the market in 2026.

- The die bonders segment is expected to hold a 31.87% market share in 2026.

North American

North America led the market with USD 365.5 million in 2025.

Europe

Europe accounted for a 17.10% share of the global market in 2025.

Asia Pacific

Asia Pacific is expected to register the highest CAGR during the forecast period.

U.S.

The market is projected to reach USD 288.6 million by 2026.

Japan

The market is projected to reach USD 54.4 million by 2026.

Read More

Key Trends Shaping the Semiconductor Bonding Industry

Increasing Adoption of Artificial Intelligence (AI) and Machine Learning (ML) Algorithms to Drive Market Demand

The rise of Artificial Intelligence (AI) and Machine Learning (ML) across various industries is significantly impacting the global market. As AI and ML technologies become more dominant in applications, such as data centers, autonomous vehicles, healthcare diagnostics, and smart consumer electronics, the demand for advanced semiconductor devices is also growing exponentially. These applications require high-performance, reliable, and efficient chips, capable of handling complex computations and large data sets. To meet these requirements, semiconductor manufacturers are pushing the boundaries of innovation in bonding solutions. Advanced bonding techniques, such as 3D stacking and System-in-Package (SiP), are being developed to enhance the performance and miniaturization of semiconductor devices.

Moreover, as AI and ML algorithms become more sophisticated, the need for higher interconnect density and superior thermal management in semiconductor devices increases. Innovative bonding solutions address these challenges, ensuring optimal performance and longevity of AI and ML hardware. Consequently, the surge in AI and ML applications is a key trend driving advancements in semiconductor bonding technologies, shaping the future of the global semiconductor market. For instance,

- August 2023: Kulicke & Soffa Industries expanded its collaboration with UCLA’s Center for Heterogeneous Integration and Performance Scaling (UCLA CHIPS). The partnership aims to advance packaging technology for AI, high-performance computing, and data center applications by developing cost-effective solutions.

Download Free sample to learn more about this report.

Growth Drivers in the Semiconductor Bonding Market

Need for High-performance Electronic Components in EVs and Autonomous Vehicles to Drive Market Segment Growth

As the automotive industry shifts toward Electric Vehicles (EVs) and autonomous vehicles, the demand for advanced semiconductor bonding solutions is poised to rise significantly. This evolution is driven by the need for high-performance electronic components essential for the operation of EVs and the sophisticated systems in autonomous vehicles. Electric vehicles rely heavily on advanced power electronics to manage battery performance, energy conversion, and overall vehicle efficiency. Autonomous vehicles, on the other hand, integrate numerous sensors, cameras, and complex computing systems to enable self-driving capabilities. These systems depend on highly integrated semiconductor devices, which necessitate precise and advanced bonding techniques to achieve the required miniaturization, reliability, and performance. The rising demand for electric and hybrid vehicles is accelerating the demand for cutting-edge semiconductor bonding solutions that can meet the stringent requirements of the automotive sector. For instance,

- July 2024: Resonac unveiled a new joint consortium in the U.S. with ten partners to advance next-generation semiconductor back-end packaging technology in Silicon Valley. This collaboration aims to drive innovation and enhance the development of cutting-edge semiconductor solutions across generative AI and autonomous driving use cases.

Significant Restraining Factors for Market Growth

Technological Complexity and Need for Precision in Bonding Processes to Foster Challenges in Market

The global market faces few restraints that impact its growth and development. One major challenge is the high cost of advanced bonding equipment and materials, which limits accessibility for smaller manufacturers and increases overall production costs. This financial barrier can impede innovation and market entry for new players, further stifling the semiconductor bonding market growth.

Additionally, technological complexity and the need for precision in bonding processes present another significant restraint. Semiconductor bonding requires highly specialized skills and expertise, and any slight deviation can lead to defects, reducing yield and increasing waste. This complexity necessitates continuous investment in research and development, further straining resources.

Semiconductor Bonding Market Segmentation Analysis

By Process Type Analysis

Rising Need for Superior Electrical and Thermal Performance to Drive Demand for Die-to-Die Process Type

Based on process type, the market is divided among die-to-die, die-to-wafer, and wafer-to-wafer.

The die-to-die segment will account for 51.89% market share in 2026 due to its established use in high-performance applications and its ability to provide superior electrical and thermal performance. This process involves bonding individual dies directly to one another, which is essential for creating high-density interconnects and achieving the necessary performance levels in advanced electronic devices, such as high-performance computing and data centers. The precision and reliability of die-to-die bonding make it the preferred choice for industries requiring high-performance solutions, thus driving its dominant market share.

However, the die-to-wafer process holds the highest CAGR in the global market owing to its advantages in scalability and cost-efficiency, particularly for mass production. The rise in demand for consumer electronics, including smartphones, wearables, and other IoT devices, fuels the growth of die-to-wafer bonding processes. Additionally, advancements in 3D integration and heterogeneous integration technologies further enhance the appeal of die-to-wafer bonding, contributing to its rapid adoption and high growth rate.

By Application Analysis

Growing Versatility and Miniaturization Capabilities of MEMS to Fuel Segmental Demand

By application, the market is categorized into advanced packaging, Micro-Electro-Mechanical Systems (MEMS) fabrication, RF devices, LEDS & photonics, CMOS Image Sensor (CIS) manufacturing, and others.

The MEMS (Micro-Electro-Mechanical Systems) segment is expected to account for 26.16% of the market in 2026. MEMS are integral components in consumer electronics, automotive, healthcare, and industrial applications. They are essential in devices such as smartphones, wearables, automotive sensors, and medical equipment, driving consistent demand. The versatility and miniaturization capabilities of MEMS make them highly attractive for manufacturers, leading to their dominant market share.

Advanced packaging application holds the highest CAGR due to several factors. Advanced packaging technologies, such as 3D stacking, wafer-level packaging, and system-in-package (SiP), are becoming increasingly crucial as they offer significant benefits in terms of performance, size reduction, and power efficiency. Moreover, the rapid advancements in AI, IoT, and 5G technologies further propel the demand for advanced packaging.

To know how our report can help streamline your business, Speak to Analyst

By Type Analysis

Growing Demand for Consumer Electronics, Automotive Electronics, and Telecommunications to Drive Segmental Growth

By type, the market is categorized into flip-chip bonders, wafer bonders, wire bonders, hybrid bonders, die bonders, thermocompression bonders, and others.

The Die bonders segment is anticipated to hold a dominant market share of 31.87% in 2026. They are essential for attaching semiconductor chips (dies) to their substrates or packages, ensuring proper electrical connections and mechanical stability. The high demand for consumer electronics, automotive electronics, and telecommunications devices drives the need for reliable die bonding, solidifying their market dominance. Additionally, advancements in die bonding technology, such as improved accuracy and speed, have enhanced production efficiency and yield, further boosting their widespread adoption.

Hybrid bonders hold the highest CAGR due to their advanced capabilities and growing applications in next-generation semiconductor devices. Hybrid bonding combines traditional bonding techniques with new approaches, such as direct bonding of wafers, to achieve higher density, improved performance, and better thermal management. For instance,

- May 2024: SUSS MicroTec unveiled the XBC300 Gen2, a versatile hybrid bonding solution designed to meet various semiconductor packaging needs. This advanced tool offers enhanced performance and flexibility for semiconductor manufacturers, addressing a broad range of bonding requirements.

Regional Insights and Market Dynamics

The global semiconductor bonding market scope is classified across five regions, North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

North America Semiconductor Bonding Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America held 36.90% of the global market share, reaching a valuation of USD 365.5 million, and is projected to grow to USD 374.2 million in 2026. Substantial investments in research and development, coupled with strong government support and favorable policies, enhance the market's growth. North America's robust ecosystem of skilled labor, advanced manufacturing facilities, and innovative start-ups also contributes to its dominant market position. The U.S. market is projected to reach USD 288.6 billion by 2026.

Asia Pacific

Asia Pacific contributed approximately USD 301.6 million to the global market in 2025, accounting for 30.40% share, and is expected to reach USD 317.5 million in 2026. Asia Pacific (APAC) is experiencing the highest CAGR in the market. This rapid growth is driven by several factors, including the region's expanding consumer electronics industry and the increasing adoption of advanced technologies, such as AI, IoT, and 5G. APAC is a hub for semiconductor manufacturing, with China, Taiwan, South Korea, and Japan leading in production capacity and technological advancements. The Japan market is projected to reach USD 54.4 billion by 2026, the China market is projected to reach USD 79.5 billion by 2026, and the India market is projected to reach USD 67.9 billion by 2026. For instance,

- July 2022: Palomar Technologies is expanding its Innovation Center in Singapore to meet the rising demand for specialized OSAT (Outsourced Semiconductor Assembly and Test) process development. This expansion aims to enhance their capabilities in delivering cutting-edge semiconductor packaging solutions to a growing global market.

Europe

The market in Europe reached USD 169.4 million in 2025, representing 17.10% of total market revenue, and is projected to reach USD 174.3 million in 2026. Europe's market is poised for steady growth, propelled by several factors. The region boasts a strong automotive industry, increasingly reliant on advanced semiconductor technologies for Electric Vehicles (EVs), autonomous driving systems, and connectivity solutions. This demand fuels investments in semiconductor manufacturing and bonding processes. Additionally, government initiatives, such as the European Union's push for technological sovereignty, further bolster the market. The UK market is projected to reach USD 36.4 billion by 2026, while the Germany market is projected to reach USD 36 billion by 2026.

The market in MEA is in an emerging stage and holds a significant potential. The region's growing focus on technological development, coupled with increasing investments in smart infrastructure and IoT applications, drives the demand for semiconductors. Israel, with its strong technology sector, plays a pivotal role in regional market dynamics.

South America

Similarly, South America is gradually evolving, driven by increasing digitalization and the growing electronics industry. Brazil and Argentina are key players, with their expanding consumer electronics markets and automotive industries contributing to the demand for semiconductors. For instance, Brazil's initiatives to boost local electronics manufacturing align with the rising demand for semiconductor components, necessitating advanced bonding techniques.

Rest of the World

The Middle East & Africa region captured 6.80% of the global market in 2025, generating USD 67.5 million in revenue, and is projected to reach USD 69.9 million in 2026.

In 2025, Latin America generated USD 87.1 million, contributing 10.00% to global market revenue, and is projected to grow to USD 89.1 million in 2026.

KEY INDUSTRY PLAYERS

Strategic Partnerships and Collaborations to Boost Market Presence of Key Players

The key players operating in the global semiconductor bonding market are entering into strategic partnerships and collaborating with other significant market leaders to expand their portfolio and provide enhanced solutions to fulfill their customer's application requirements. Also, through collaboration, the companies are gaining expertise and expanding their business by reaching a mass customer base.

List of Top Semiconductor Bonding Companies:

- Besi (Netherlands)

- Intel Corporation (U.S.)

- Palomar Technologies (U.S.)

- Panasonic Connect Co., Ltd. (Japan)

- Kulicke and Soffa Industries, Inc. (Singapore)

- SHIBAURA MECHATRONICS CORPORATION (Japan)

- TDK Corporation (Japan)

- ASMPT (Singapore)

- Tokyo Electron Limited (Japan)

- EV Group (EVG) (Austria)

- Fasford Technology (Japan)

- SUSS MicroTec SE (Germany)

KEY INDUSTRY DEVELOPMENTS:

- July 2024: Hanmi Semiconductor plans to introduce new 2.5D TC bonders to capitalize on anticipated growth in the semiconductor industry from 2024 to 2026. The company's strategic move aims to enhance its position in the market as demand for advanced packaging technologies increases.

- June 2024: EV Group (EVG) and Fraunhofer IZM-ASSID extended their partnership to advance wafer bonding technologies for quantum computing, marked by the installation of an EVG850 DB automated laser debonding system at the Center for Advanced CMOS image sensors and Heterointegration Saxony (CEASAX) in Dresden, Germany.

- May 2024: ITEC Equipment unveiled a groundbreaking flip-chip die bonder that operates five times faster than the leading models on the market. This revolutionary technology is set to significantly enhance the efficiency and speed of semiconductor packaging processes. There are two rotating heads (‘TwinRevolve’), so there’s less inertia and less vibration.

- August 2023: EV Group showcased its hybrid bonding and nanoimprint lithography technologies at SEMICON Taiwan 2023, emphasizing its advanced capabilities. The company aims to demonstrate how these solutions can enhance semiconductor manufacturing processes and drive innovation in the industry.

- August 2023: Kulicke & Soffa announced a collaboration with TSMT to advance semiconductor packaging solutions, aiming to enhance their manufacturing capabilities. This partnership will focus on integrating TSMT's innovative technologies with Kulicke & Soffa expertise to drive advancements in the semiconductor industry.

REPORT COVERAGE

The report provides a competitive landscape of the market overview and focuses on key aspects such as market players, product/service types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key semiconductor bonding industry developments. In addition to the factors mentioned above, the market report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million) |

|

Growth Rate |

CAGR of 3.60% from 2026 to 2034 |

|

Segmentation |

By Process Type

By Application

By Type

By Region

|

Frequently Asked Questions

The market is projected to record a valuation of USD 1363.7 million by 2034.

In 2026, the market size stood at USD 1025 million.

The market is projected to record a CAGR of 3.60% during the forecast period of 2026-2034.

Die bonders are the leading type segment in the market.

The need for high-performance electronic components in EVs and autonomous vehicles is expected to drive market segment growth.

Besi, Intel Corporation, Palomar Technologies, Panasonic Connect Co., Ltd., Kulicke and Soffa Industries, Inc., SHIBAURA MECHATRONICS CORPORATION, TDK Corporation, ASMPT, Tokyo Electron Limited, EV Group (EVG), Fasford Technology, and SUSS MicroTec SE are the top players in the market.

North America dominated the semiconductor bonding market with a market share of 36.90% in 2025.

Asia Pacific is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us