Semiconductor Test Equipment Market Size, Share & Industry Analysis By Product Type (Semiconductor Automated Test Equipment (ATE), Burn-in Systems, Handler Equipment, Probe Equipment, and Others), By Technology (Analog Testing, Digital Testing, Mixed-Signal Testing, RF Testing, and Power Semiconductor Testing), By End-Use Industry (Semiconductor Manufacturing, Consumer Electronics, Automotive, Military and Defense, IT and Telecom, and Others), and Regional Forecast, 2026 - 2034

KEY MARKET INSIGHTS

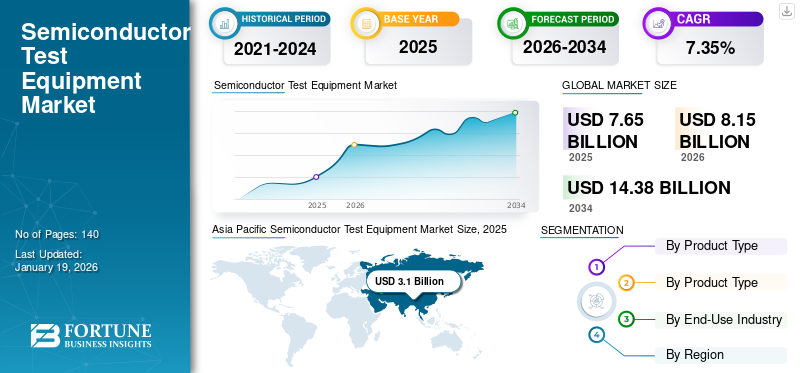

The global semiconductor test equipment market size was valued at USD 7.65 billion in 2025. The market is projected to grow from USD 8.15 billion in 2026 to USD 14.38 billion by 2034, exhibiting a CAGR of 7.35% during the forecast period. Asia Pacific dominated the semiconductor test equipment market with a market share of 40.49% in 2025.

Semiconductor test equipment is a system that applies electrical signals to a semiconductor device, allowing for the comparison of output signals with anticipated values to determine if the device operates according to its design specifications. The major players included in this market are Virginia Panel Corporation, Tokyo Electron Limited, NATIONAL INSTRUMENTS CORP., SPEA S.p.A., Teradyne Inc., ADVANTEST CORPORATION, Cohu, Inc., Astronics Corporation, Chroma Systems Solutions, Inc., and Tokyo Seimitsu Co., Ltd.

Semiconductor test equipment is witnessing significant demand mainly due to technological advancements such as 5G, HPC, AI, and automated vehicles. As reported by PatentPC in 2025, the uptake of 5G Internet is accelerating, with certain sectors experiencing a 50% year-over-year growth in subscribers. Continuous growth in combining the different electronic components into vehicle safety systems, navigation systems, and entertainment systems will continue to expand market value. The semiconductor market also sees an increasing adoption of consumer electronics, for instance, tablets, smartphones, laptops, and others, which is further driving semiconductor test equipment market growth. Furthermore, the market is likely to gain from the heightened integration of Internet of Things (IoT) technology across various industrial applications.

During the COVID-19 pandemic, the semiconductor test equipment market faced lower-than-expected demand due to economic instability and interruptions initially. Nevertheless, the latter increase in demand for electronics in multiple sectors resulted in notable long-term expansion. The rapid growth in the market, as indicated by the rise in CAGR, can be attributed to the robust recovery of the market and heightened demand fueled by the accelerated trend of digitalization set off during the pandemic period.

Download Free sample to learn more about this report.

Semiconductor Test Equipment Market Takeaways

- 2025 Market Size: USD 7.65 billion

- 2026 Market Size: USD 8.15 billion

- 2034 Forecast Market Size: USD 14.38 billion

- CAGR: 7.35% from 2026–2034

- Asia Pacific dominated the semiconductor test equipment market with a market share of 40.49% in 2025.

- The semiconductor Automated Test Equipment (ATE) segment will account for 32.89% market share in 2026.

- In 2026, the analog testing segment is projected to lead the market with a 30.09% share.

Asia Pacific

The Asia Pacific market accounted for USD 3.1 billion in 2025, representing 40.49% of the global industry, and is expected to reach USD 3.29 billion in 2026.

Europe

In 2025, Europe generated USD 1.32 billion, contributing 17.25% to global market revenue, and is projected to grow to USD 1.4 billion in 2026.

North America

North America maintained a strong presence in the global market, reaching USD 2.4 billion in 2025, accounting for 31.38% share, and is expected to reach USD 2.59 billion in 2026, fueled by the presence of major semiconductor firms and a strong technological framework.

U.S.

The U.S. market is valued at USD 1.97 billion by 2026.

Japan

The Japan market is valued at USD 0.73 billion by 2026.

Read More

IMPACT OF GENERATIVE AI

Integration of Generative AI with Semiconductor Test Equipment for Enhancing Capabilities to Fuel Market Growth

Generative AI is fueling innovation in the semiconductor test equipment industry and improving efficiency, accuracy, and scalability. As the demand for complex semiconductors - especially for AI and HPC applications - continues to grow, generative AI will help keep pace with a continually evolving semiconductor industry, maintain competitive advantage, and ensure product quality control in companies that integrate generative AI into their testing equipment.

IMPACT OF RECIPROCAL TARIFFS

Reciprocal tariffs have generated cost pressures, supply chain disruptions, and competitive pressures for the semiconductor test equipment industry, creating uncertainty for both manufacturers and customers. While the impact will ultimately depend on domestic suppliers' ability to scale and innovate, along with global trade policy developments, it seems likely that the costs to both manufacturers and consumers will continue to rise.

MARKET DYNAMICS

Market Drivers

Rising Complexity of Semiconductor Devices to Aid Market Growth

The market for semiconductor test equipment is set to expand rapidly since semiconductor devices are advancing continuously, driving more complex designs, 3D stacking, chiplet packaging, and reduction in the size of semiconductor test devices. The need for advanced testing solutions will increase as companies require performance testing criteria that focuses on reliability to ensure functional verification of semiconductor devices.

Market Restraints

High Cost of Advanced Test Equipment and Economic Downturns May Hinder Market Expansion

The market encounters obstacles to growth due to the costly high-end equipment, leading to significant capital needs of semiconductor manufacturers. As the semiconductor economic cycles soften, the acquisition of test equipment diminishes, and capital spending declines.

Market Opportunities

Integration with Advanced Test Systems to Create Lucrative Market Opportunities

The combination of semiconductor testing boards with sophisticated testing systems is enhancing efficiency and productivity in semiconductor manufacturing. The integration of these systems allows for seamless automated wafer loading and unloading, precise positioning of probe cards, and immediate analysis of results. Manufacturers are developing probe cards that can be used with different types of testing systems, which allow compatibility and interoperability for semiconductor companies. Manufacturers are creating probe cards that work with various testing systems, guaranteeing compatibility and interoperability for semiconductor producers.

SEMICONDUCTOR TEST EQUIPMENT MARKET TRENDS

Increased Adoption of Advanced Packaging Solutions and AI-Powered Testing to Emerge as a Key Market Trend

The semiconductor testing landscape is seeing an increased integration of ML and AI technologies within testing systems. Companies can achieve improved performance through AI-driven predictive maintenance analysis of real-time data, which boosts their yield rates. Moreover, there is a focused development of dedicated solutions for advanced packaging technologies and 3D integrated circuits in this domain. Modern technology-driven signal maintenance systems facilitate the testing of complex structures by employing instrumentation techniques.

SEGMENTATION ANALYSIS

By Product Type

Rising Need for IoT and Smart Devices Boosted the Expansion of the Semiconductor Automated Test Equipment (ATE) Segment

Based on product type, the market is segmented into semiconductor automated test equipment (ATE), burn-in systems, handler equipment, probe equipment, and others.

The semiconductor Automated Test Equipment (ATE) segment will account for 32.89% market share in 2026 With the rise of Internet of Things applications, prevalence of smart devices, and small semiconductors is increasing the demand for superior semiconductor automated testing equipment is increasing. Ericsson anticipates the number of connected devices globally to increase almost twofold from 2022 to 2028. This increase is expected to be fueled by a rise in short-range IoT devices, with an estimated 28.72 billion such devices by 2028. The continuous evolution of complex devices aimed at improving applications drives the necessity for ATE.

The probe equipment segment is set to achieve the highest compound annual growth rate (CAGR) over the forecast period. This growth is driven by the increasing chip complexity, advancements in technologies such as 5G and AI and the demand for more advanced testing solutions.

By Technology

Analog Testing Dominated the Market with Its Enhanced Features in Semiconductor Test Equipment Technology

Based on technology, the market is categorized into analog testing, digital testing, mixed-signal testing, RF testing, and power semiconductor testing.

In 2026, the analog testing segment is projected to lead the market with a 30.09% share. Analog testing plays a crucial role in evaluating devices that handle continuous signals. The increasing use of analog semiconductors in wireless communication and consumer electronics fuels the need for accurate analog testing solutions that can maintain signal integrity and optimize device performance.

The RF testing segment is expected to record the highest CAGR during the forecast period due to the relentless expansion of wireless technologies and connected devices.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Semiconductor Manufacturing Dominated the Market with Increasing Need for Customized Semiconductor Solutions

Based on end-use industry, the market is categorized into semiconductor manufacturing, consumer electronics, automotive, military and defense, IT and telecom, and others.

The semiconductor manufacturing segment is forecast to represent 27.72% of total market share in 2026. The demand for modified semiconductor solutions has led to a rise in manufacturing units, increasing the need for updated testing equipment. Foundries need detailed test solutions to ensure that the manufactured wafers meet their clients' requirements. As semiconductor designs become more complex, manufacturers are channeling investments into advanced testing equipment to sustain their competitive advantage and fulfill the requirements of a varied customer base.

The military & defense segment is anticipated to depict the highest CAGR during the forecast period as a result of increased defense budgets and the growing number of UAVs. Major factors driving the demand for advanced semiconductors and their testing equipment are government commitments to defense infrastructure, especially to areas such as radar, surveillance, and cybersecurity. Besides this, the UAVs also depend on advanced semiconductor technologies for their navigation, control, and communication, which will further drive segment growth.

SEMICONDUCTOR TEST EQUIPMENT MARKET REGIONAL OUTLOOK

By region, the market is divided into North America, Europe, South America, the Middle East & Africa, and Asia Pacific.

Asia Pacific

Asia Pacific Semiconductor Test Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region held the largest semiconductor test equipment market share in 2024. The Asia Pacific market accounted for USD 3.1 billion in 2025, representing 40.49% of the global industry, and is expected to reach USD 3.29 billion in 2026. The region's leadership position in the semiconductor market is due to the fact that it is the semiconductor manufacturing center of the world. Countries such as China, Taiwan, Japan, and South Korea house the largest foundries and integrated device manufacturers globally. The rapid growth of electronic devices and auto sectors in this region, along with substantial government funding for semiconductor infrastructure, drives a significant market share. The Japan market is valued at USD 0.73 billion by 2026, and the India market is valued at USD 0.45 billion by 2026.

Download Free sample to learn more about this report.

China has already accomplished multiple steps to improve its semiconductor industry such as a vast growth and presence in the foundry, gallium-nitride (GaN), and silicon carbide (SiC) sectors, to name a few. The multiplication of the semiconductor area and reinforcing of the chip manufacturing ability in the region are expected to lead the market for testing appliances over the coming years. The China market is valued at USD 1.2 billion by 2026

To know how our report can help streamline your business, Speak to Analyst

Europe

In 2025, Europe generated USD 1.32 billion, contributing 17.25% to global market revenue, and is projected to grow to USD 1.4 billion in 2026. Europe possesses a robust industrial sector and is enhancing its investments in chip manufacturing, especially in nations such as Germany and the Netherlands. The exponentially increasing demand for semiconductors in the automotive sector, industrial automation, and communications, combined with the governments' support of the European semiconductor landscape, is expected to continue providing test equipment with a steady market. The UK market is valued at USD 0.3 billion by 2026, and the Germany market is valued at USD 0.27 billion by 2026.

South America

The South American region has a smaller market presence. Increasing industrialization, government support for technology adoption, and the expanding use of advanced technologies in key sectors created a positive impact, while economic diversification could be challenging.

Middle East & Africa

In 2025, Middle East & Africa represented USD 0.55 billion, accounting for 7.17% of the worldwide market, and is projected to grow to USD 0.57 billion in 2026. The Middle East & Africa market is undergoing stable growth due to recent shifts in the local economy and initial government funding for digital transformation and research initiatives. Moreover, significant investments in data centers in the UAE and Saudi Arabia, along with AI implementations, increase the need for advanced chips, which in turn raises the demand for testing equipment utilized in high-reliability server, optical, and networking chips.

North America

North America maintained a strong presence in the global market, reaching USD 2.4 billion in 2025, accounting for 31.38% share, and is expected to reach USD 2.59 billion in 2026, fueled by the presence of major semiconductor firms and a strong technological framework. The region's dedication to innovation and research, and development has enabled the creation of sophisticated testing solutions suitable for various applications, including consumer electronics and telecommunications. The U.S., especially, is pivotal in the market due to its strong focus on technological progress and the advancement of high-performance semiconductors. The U.S. market is valued at USD 1.97 billion by 2026.

Latin America

The Latin America contributed 3.72% to the global market in 2025, with a valuation of USD 0.28 billion, and is projected to reach USD 0.3 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Notable Players to Implement Strategic Strategies to Expand Business Reach

Key players present in this market are offering semiconductor test equipment to provide users with enhanced product reliability, improved performance, cost savings, and compliance with industry standards. They concentrate on holding contracts with small and local businesses to grow their business. Moreover, such mergers & acquisitions, partnerships, and investments will create a surge in demand for this technology.

List of Key Semiconductor Test Equipment Companies Studied (including but not limited to)

- Virginia Panel Corporation (U.S.)

- Tokyo Electron Limited (Japan)

- NATIONAL INSTRUMENTS CORP. (U.S.)

- SPEA S.p.A. (Italy)

- Teradyne Inc. (U.S.)

- ADVANTEST CORPORATION (Japan)

- Cohu, Inc. (U.S.)

- Astronics Corporation (U.S.)

- Chroma Systems Solutions, Inc. (Taiwan)

- Tokyo Seimitsu Co., Ltd. (Japan)

- Shibasoku Co., Ltd. (Japan)

- Hangzhou ChangChuan Technology Co., Ltd. (China)

- ROOS INSTRUMENTS, INC. (U.S.)

- STAr Technologies Inc. (U.S.)

- Aeroflex USA, Inc. (U.S.)

- HIOKI E.E. CORPORATION (Japan)

- Aemulus Corporation Sdn Bhd. (Malaysia)

- Marvin Test Solutions, Inc. (U.S.)

- miconindia.com (India)

- Averna (Canada)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Teradyne introduced a new production-ready system designed to test double-sided wafer probes aimed at Silicon Photonics applications. This complex testing system offers the necessary features to meet the growing demand for data communication and AI system evaluations. This technology allows for simultaneous full-wafer testing on both sides, assisting manufacturers in the rapidly expanding industry to reduce their testing time and costs.

- February 2024: Cohu Inc. declared that its new MEMS testing solution, the Sense+ system, has been chosen by a fabless semiconductor manufacturer in the U.S. in collaboration with µ-sense to evaluate their upcoming high-fidelity microphones.

- December 2023: Advantest Corporation unveiled the ACS Real-time Data Infrastructure (RTDI) to ease decision-making through AI, ML, and data analytics in one platform. In such infrastructure, the test data is collected, processed, analyzed, and monitored securely, tracking the customer’s work of automating the conversion from the insight to the testing action.

- November 2023: For the purpose of enlarging the business and giving the clients better semiconductor test interfaces, Teradyne Inc. and Technoprobe SpA announced their strategic partnership. Teradyne plans to inject USD 516 million of equity into Technoprobe as part of the agreement. Furthermore, Technoprobe will invest USD 85 million to acquire Teradyne's Device Interface Solutions (DIS) business.

- March 2023: Astronics Corporation, a provider of advanced technologies for the global aerospace, defense, and other mission-critical industries, introduced its new Defense test and measurement platform, the Thermally-controlled Operational Reliability CHip Tester (TORCH). TORCH is a highly automated, massively parallel testing system that streamlines reliability assessments through accelerated thermal technology and can simultaneously evaluate up to 384 sites/Devices Under Test (DUTs) with distinct test profiles.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investment in this market is attractive due to technological innovation, expanding application markets, and strategic policy support. Focusing on semiconductor manufacturing and enhanced packaging technologies will help capture growth opportunities and address evolving market demands. For instance,

- In June 2025, Texas Instruments (TI) announced that it would allocate more than USD 60 billion to fund wafer fabrication in the U.S., becoming the largest semiconductor investment the U.S. has ever seen.

- In December 2024, Tata Electronics announced an investment of around USD 3 billion for an OSAT facility in India, utilizing indigenous packaging technologies.

Therefore, it presents a huge opportunity for players operating in this market.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies, product/types, and the leading end-use industry of the product. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.35% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

By Technology

By End-Use Industry

By Region

|

|

Companies Profiled in the Report |

Virginia Panel Corporation (U.S.) Tokyo Electron Limited (Japan) NATIONAL INSTRUMENTS CORP. (U.S.) SPEA S.p.A. (Italy) Teradyne Inc. (U.S.) ADVANTEST CORPORATION (Japan) Cohu, Inc. (U.S.) Astronics Corporation (U.S.) Chroma Systems Solutions, Inc. (Taiwan) Tokyo Seimitsu Co., Ltd. (Japan) |

Frequently Asked Questions

According to Fortune Business Insights, the market is projected to reach a valuation of USD 14.38 billion by 2034.

In 2025, the market was valued at USD 7.65 billion.

The market is projected to record a CAGR of 7.35 % during the forecast period.

By product type, the Semiconductor Automated Test Equipment (ATE) segment led the market in 2025.

The rising complexity of semiconductor devices is a key factor driving market growth.

Virginia Panel Corporation, Tokyo Electron Limited, NATIONAL INSTRUMENTS CORP., SPEA S.p.A., Teradyne Inc., ADVANTEST CORPORATION, Cohu, Inc., Astronics Corporation, Chroma Systems Solutions, Inc., and Tokyo Seimitsu Co., Ltd. are the top players in the market.

Asia Pacific held the highest market share in 2025.

By end-use industry, the military and defense segment is expected to record the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us