Sensor-based Sorting Machine Market Size, Share & Industry Analysis, By Sensor Type (Optical, Near-Infrared (NIR), X-ray, Laser, Electromagnetic, and Hyperspectral), By Machine Type (Conveyor-Based and Free-Fall), By Application (Recycling & Waste Management, (Municipal Solid Waste (MSW), Commercial & Industrial Waste (C&I), Construction & Demolition Waste (C&D), and E-waste), Food Sorting (Grains & Cereals, Fruits & Vegetables, Nuts & Seeds, and Other Food Products), and Mining & Minerals)), and Regional Forecast, 2026 – 2034

Sensor-based Sorting Machine Market Size and Future Outlook

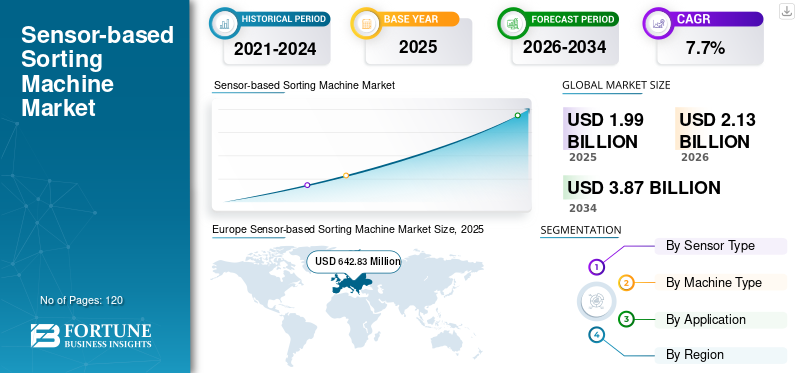

The global sensor-based sorting machine market size was valued at USD 1,991.09 million in 2025. The market is projected to grow from USD 2,132.79 million in 2026 to USD 3,870.63 million by 2034, exhibiting a CAGR of 7.7% during the forecast period. Europe dominated the sensor-based sorting machine market with a market share of 32.25% in 2025.

Sensor-based sorting machine are increasingly being adopted in semiconductor manufacturing environments to streamline wafer transport and handling operations with high precision and minimal human intervention. These systems represent a cutting edge advancement within the broader sorting machine industry, leveraging advanced robotics, intelligent motion systems, and contamination-controlled interfaces to ensure safe and accurate wafer movement across critical production stages such as lithography, etching, inspection, and packaging. The growing complexity of semiconductor devices and shrinking node sizes are intensifying the need for highly reliable and automated wafer handling solutions powered by advanced sensor based sorting technology. The expansion of semiconductor fabrication capacity, particularly in advanced logic and memory production, is accelerating demand for automation technologies that can support high throughput while maintaining stringent quality standards. Additionally, increasing focus on reducing labor costs and improving operational efficiency is further driving adoption. Investments in next-generation fabs and the transition toward fully automated smart manufacturing facilities are contributing to the growth of the global sensor based sorting market, especially across Asia Pacific, North America, and Europe, where semiconductor companies are prioritizing yield optimization and contamination control.

- For instance, in February 2026, RORZE Corporation introduced next-generation vacuum sensor-based sorting machine designed for advanced semiconductor nodes. Further, featuring enhanced precision control and optimized cleanroom performance to support high-throughput wafer processing in modern fabrication environments.

Brooks Automation (Azenta Inc.), RORZE Corporation, Hirata Corporation, Kawasaki Heavy Industries Ltd., and DAIHEN Corporation are among the key players holding a significant share of the market. Their competitive positioning is strengthened by deep expertise in semiconductor automation, and the ability to deliver highly precise and contamination-controlled robotic systems. It is further supported by strong collaborations with semiconductor equipment manufacturers, and continuous innovation in wafer handling technologies to support evolving semiconductor fabrication requirements.

Download Free sample to learn more about this report.

Sensor-based Sorting Machine Market Key Takeaways

- 2025 Market Size: USD 1,991.09 million

- 2026 Market Size: USD 2,132.79 million

- 2034 Forecast Market Size: USD 3,870.63 million

- CAGR: 7.7% from 2026–2034

- Europe dominated the sensor-based sorting machine market with a 32.25% share in 2025.

- The optical segment held the largest market share in 2025.

- The conveyor-based segment dominated the market due to high-volume processing capabilities.

Europe

Europe led the market with USD 642.83 million in 2025, supported by advanced recycling infrastructure.

Asia Pacific

Asia Pacific generated USD 609.16 million in 2025 and is the fastest-growing regional market.

North America

North America reached USD 466.90 million in 2025, driven by automation in recycling and food processing.

U.S

The U.S. market is projected to reach USD 403.33 million in 2026.

Japan

Japan's market is projected to reach USD 84.67 million in 2026.

Read More

SENSOR-BASED SORTING MACHINE MARKET TRENDS

Rising Adoption of Multi-Sensor Fusion and AI-Driven Sorting is Transforming Market Capabilities

The demand for such machine is increasingly being shaped by the growing need for higher sorting accuracy and the ability to process complex and heterogeneous material streams across recycling, mining, and food industries. Operators within the sorting machine industry are focusing on deploying cutting edge systems that combine multiple sensing technologies such as optical sorters, NIR, and X-ray with artificial intelligence-driven recognition algorithms to improve material identification and separation efficiency. This shift is enabling facilities to handle mixed waste streams, low-grade ores, and variable-quality food products with greater precision and consistency. Increasing pressure to achieve higher recovery rates and reduce material losses is driving investments in intelligent sorting solutions capable of real-time data processing and adaptive decision-making. Industries are also prioritizing flexible and modular sorting systems that can be easily integrated into existing processing lines while supporting scalability for future capacity expansion. These advancements are influencing market dynamics as companies transition toward smart sorting ecosystems that enhance operational efficiency, reduce manual dependency, and optimize resource utilization. Equipment manufacturers are responding by developing next-generation machine with enhanced detection capabilities, improved processing speeds, and seamless integration with digital monitoring platforms, enabling more efficient and automated sorting operations across diverse industrial applications.

- For instance, in May 2025, TOMRA Systems ASA introduced an advanced multi-sensor sorting solution integrating AI-based material recognition, designed to improve sorting accuracy and throughput in complex recycling environments.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Throughput Material Processing and Automation to Drive Market Growth

The market is witnessing strong growth as industries increasingly adopt automated sorting technologies to handle rising volumes of materials with greater efficiency and accuracy. Sectors such as recycling, food processing, and mining are prioritizing automation to improve throughput, reduce manual dependency, and ensure consistent quality in sorting operations. The increasing complexity of material streams, particularly in mixed waste and low-grade ores, is further driving the need for advanced sorting systems capable of precise identification and separation. Additionally, the growing focus on resource optimization and recovery is encouraging operators to deploy high-performance sensor-based solutions that enhance yield and minimize material loss. As industries expand processing capacities and modernize infrastructure, there is a rising demand for systems that can operate continuously under high-volume conditions while maintaining reliability and precision. Equipment manufacturers are responding by introducing advanced machine with improved detection accuracy, faster processing speeds, and enhanced integration capabilities with digital control systems. Further, enabling end users to optimize operational efficiency and achieve higher productivity across diverse industrial applications.

- For instance, in June 2025, Bühler Group introduced an advanced optical sorting platform designed to enhance sorting efficiency and throughput in high-volume food processing and grain handling applications.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

High Capital Investment and Operational Complexity to Limit Market Adoption

The adoption of these machine is often constrained by the high initial capital investment required for advanced sensor technologies, precision hardware, and integrated software systems. These machines involve sophisticated components such as multi-sensor detection units, high-speed processing systems, and automated control platforms, which increase overall system costs. Additionally, integrating these solutions into existing processing lines can be complex, requiring customization based on material sensor type, operational requirements, and facility layout. The need for regular calibration, maintenance, and technical expertise to ensure optimal performance further adds to operational challenges. Industries operating in cost-sensitive environments may face difficulties in justifying the investment, particularly where return on investment depends on processing volumes and material recovery rates. Furthermore, variability in input material quality and composition can affect sorting efficiency, requiring continuous system optimization. These factors may limit adoption, especially among small and mid-sized operators, and can slow the pace of technology deployment in emerging markets where infrastructure and technical capabilities are still developing.

MARKET OPPORTUNITIES

Increasing Focus on Resource Efficiency and High-Value Material Recovery Creating New Growth Avenues

An emerging opportunity in the sensor-based sorting machine market growth is the increasing emphasis on maximizing material recovery and improving resource efficiency across industries such as recycling, mining, and food processing. Traditionally, sorting systems were primarily deployed for basic separation tasks. However, the shift toward extracting higher-value materials from complex and mixed streams is driving demand for more advanced and precise sorting technologies. Industries are increasingly investing in intelligent sorting solutions capable of identifying subtle material differences, enabling recovery of valuable fractions such as high-grade plastics, rare metals, and premium food products. Additionally, the growing adoption of circular economy practices and stricter environmental regulations is encouraging operators to upgrade legacy systems with advanced sensor-based technologies that improve yield and reduce waste. Manufacturers are developing next-generation machine with enhanced detection capabilities, AI-driven sorting algorithms, and modular designs that allow easy upgrades and scalability. These advancements are enabling end users to optimize operational efficiency while unlocking new revenue streams from recovered materials, creating significant growth opportunities across both developed and emerging markets.

- For instance, in May 2025, Steinert GmbH introduced an advanced sensor-based sorting solution designed to enhance recovery of high-value metals from complex recycling streams, improving material purity and operational efficiency in modern processing facilities.

MARKET CHALLENGES

Variability in Input Material Streams and System Calibration Complexity Impacting Operational Efficiency

A key challenge in the market is the high variability in input material characteristics, which can significantly impact sorting accuracy and system performance. Unlike controlled manufacturing environments, industries such as recycling and mining deal with heterogeneous and inconsistent material streams that vary in composition, size, moisture content, and contamination levels. This variability requires continuous system calibration and fine-tuning of sensor parameters to maintain optimal sorting efficiency. Additionally, differences in material properties can affect sensor detection accuracy, particularly when processing mixed or low-quality inputs, leading to potential misclassification or reduced recovery rates. The need for frequent adjustments and skilled operators to manage system performance increases operational complexity and can limit efficiency gains. Furthermore, integrating advanced sorting systems into existing processing lines without disrupting operations remains a challenge, especially in facilities with legacy infrastructure. These factors can create barriers to achieving consistent performance and may impact the overall effectiveness of sorting operations, particularly in high-volume and variable processing environments.

Segmentation Analysis

By Sensor Type

Optical Segment Led as It Represents Most Widely Adopted Technology across High-Volume Sorting Applications

By sensor type, the market is segmented into optical, Near-Infrared (NIR), X-ray, laser, electromagnetic, and hyperspectral.

Optical held the largest sensor-based sorting machine market share as it represents the most extensively deployed and versatile technology across industries such as recycling, food processing, and mining. Optical sorting systems are widely used due to their ability to perform high-speed, real-time material identification based on color, shape, and surface characteristics, making them highly effective in large-scale processing environments. The demand is particularly strong in food and recycling applications, where high throughput and consistent sorting accuracy are critical for maintaining product quality and operational efficiency. Additionally, optical systems offer cost-effective deployment compared to more advanced sensor technologies, further supporting their widespread adoption. As industries continue to process increasing volumes of materials and focus on improving sorting precision, there is growing integration of optical systems with advanced software and automation platforms. These systems enable enhanced operational control, improved sorting consistency, and higher processing speeds, reinforcing optical technology as the foundational segment within the market.

- For instance, in September 2025, Pellenc ST expanded its recycling solutions portfolio with advanced optical sorting technologies designed to improve material recovery efficiency and support high-performance sorting operations in modern recycling facilities.

Near-Infrared (NIR) technology is the fastest-growing segment and is projected to expand at a CAGR of 8.2% over the forecast period. The growth of this segment is driven by increasing demand for precise material identification, particularly in applications where differentiation based on chemical composition is essential, such as plastic recycling and food quality inspection. NIR-based sensor-based sorting machine enable accurate detection of materials that are visually similar but chemically distinct, improving sorting accuracy and recovery rates.

To know how our report can help streamline your business, Speak to Analyst

By Machine Type

Conveyor-Based Segment Led as It Enables Continuous High-Volume Processing and Operational Efficiency

By machine type, the market is segmented into conveyor-based and free-fall.

Conveyor-based held the largest share of the market, driven by its ability to support continuous, high-throughput material processing across industries such as recycling, food processing, and mining. These systems enable stable and controlled material flow, allowing precise sensor detection and accurate sorting of materials on a moving belt. Conveyor-based configurations are widely adopted in large-scale processing facilities where maintaining consistent feed rates and handling high material volumes are critical for operational efficiency. The demand is particularly strong in recycling and food industries, where continuous processing and high sorting accuracy directly impact output quality and productivity. Additionally, conveyor-based systems offer greater flexibility for integrating multiple sensor technologies and automation solutions, enabling enhanced process control and scalability.

- For instance, in June 2025, Steinert GmbH introduced its advanced conveyor-based sorting systems under the KSS platform, designed to enhance metal separation efficiency and support continuous high-capacity processing in recycling operations.

Free-fall is emerging as a high-growth segment and is projected to expand at a CAGR of 7.4% over the study period. The growth of this segment is driven by increasing adoption in applications requiring rapid sorting of bulk materials, such as food grains, plastics, and lightweight recyclables. Free-fall sensor-based sorting machine enable materials to be sorted in mid-air, allowing faster processing speeds and reduced mechanical complexity.

By Application

Recycling & Waste Management Segment Led as it is the Primary Demand Center for High-Volume Material Sorting

By application, the market is segmented into recycling & waste management, food sorting, and mining & minerals.

Recycling & waste management held the largest share of the market, driven by the increasing need for efficient separation and recovery of materials from complex waste streams. Industries are prioritizing advanced sorting technologies to improve recycling rates, reduce landfill dependency, and enhance the quality of recovered materials such as plastics, metals, and paper. They play a critical role in material recovery facilities by enabling accurate identification and separation of mixed waste under high-throughput conditions. The demand is particularly strong in regions with stringent environmental regulations and established recycling infrastructure, where improving resource efficiency and achieving sustainability targets are key operational priorities.

Food sorting is expected to register the highest growth and is projected to expand at a CAGR of 8.5% over the study period. The growth of this segment is driven by increasing demand for quality assurance, contamination removal, and high-speed processing in food production. They are increasingly being adopted to ensure consistent product quality and meet stringent food safety standards, particularly in applications such as grains, fruits, and processed food products.

Sensor-based Sorting Machine Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Sensor-based Sorting Machine Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The European market is the dominating region driven by a strong focus on sustainability, advanced industrial infrastructure, and increasing adoption of automation technologies across key economies such as Germany, U.K., France, Italy, and Netherlands. The demand for such machine is closely linked to the region’s well-developed recycling ecosystem, stringent environmental regulations, and growing emphasis on resource efficiency across industries. Organizations are increasingly investing in advanced sorting solutions to improve material recovery rates, enhance product quality, and comply with evolving regulatory standards related to waste management and recycling.

U.K. Sensor-based Sorting Machine Market

The U.K. market in 2026 is estimated at around USD 90.27 million, representing roughly 4.2% of global sales.

Germany Sensor-based Sorting Machine Market

Germany’s market is projected to reach approximately USD 146.35 million in 2026, equivalent to around 6.9% of global sales.

North America

The North America market accounted for over USD 466.90 million in revenue in 2025, supported by strong adoption of automation across recycling, food processing, and mining industries in the U.S., Canada, and Mexico. Regional demand is closely linked to increasing investments in material recovery infrastructure, growing emphasis on sustainable waste management, and the need for high-throughput sorting solutions across industrial applications. Companies are increasingly deploying advanced sensor-based sorting systems to improve material recovery rates, enhance product quality, and reduce operational costs. Additionally, stringent environmental regulations and circular economy initiatives are encouraging the modernization of existing processing facilities with automated sorting technologies. The presence of established recycling ecosystems and advanced food processing industries further supports the widespread adoption of high-performance sorting systems across the region.

U.S. Sensor-based Sorting Machine Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 403.33 million in 2026. It is driven by its well-established recycling infrastructure, large-scale food processing industry, and increasing adoption of advanced automation technologies. Unlike many regions, U.S.-based operators are focusing on deploying highly efficient and scalable sorting systems capable of handling complex and high-volume material streams. The country is witnessing significant investments in upgrading material recovery facilities and integrating advanced sensor technologies to improve sorting accuracy and operational efficiency.

Asia Pacific

Asia Pacific remains the fastest-growing market, generating revenue of USD 609.16 million in 2025 globally. Within the region, China and Japan are projected to reach approximately USD 228.87 million and USD 84.67 million, respectively by 2026. Asia Pacific market driven by rapid industrialization, increasing waste generation, and expanding food processing and recycling industries across key economies such as China, Japan, South Korea, and India. The region’s growth is primarily supported by rising investments in material recovery facilities, growing emphasis on improving recycling efficiency, and the need for high-throughput sorting solutions to manage large and complex material streams. China leads the regional market due to its large-scale industrial base and increasing adoption of automated sorting technologies in recycling and manufacturing sectors. On the other hand, Japan and South Korea are characterized by advanced technology adoption and high-precision sorting requirements. Emerging markets such as India and Southeast Asia are witnessing growing deployment of such systems as industries focus on improving operational efficiency, reducing manual labor dependency, and meeting evolving environmental and quality standards.

China Sensor-based Sorting Machine Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 228.87 million, representing roughly 10.7% of global sales.

Japan Sensor-based Sorting Machine Market

The Japan market in 2026 is estimated at around USD 84.67 million, accounting for roughly 4.0% of the global sales.

India Sensor-based Sorting Machine Market

The India market in 2026 is estimated at around USD 93.93 million, accounting for roughly 4.4% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in waste management infrastructure, industrial diversification, and growing adoption of automation technologies across key regions such as GCC countries, South Africa, Israel, and North Africa. The demand for such machine is closely linked to the region’s efforts to improve material recovery efficiency, reduce landfill dependency, and modernize processing facilities across recycling, mining, and food industries. GCC countries are investing in advanced waste sorting and recycling projects as part of sustainability and circular economy initiatives, supporting the deployment of automated sorting systems. Israel represents a technologically advanced market within the region, with higher adoption of precision-based sorting solutions across industrial and research-driven applications.

GCC Sensor-based Sorting Machine Market

The GCC market is projected to reach around USD 81.16 million in 2026, representing roughly 3.8% of the global sales.

South America

The South America market is driven by growing industrial activities, increasing focus on resource recovery, and gradual adoption of automation technologies across key economies such as Brazil, Argentina, and Chile. The demand for such machine is primarily supported by expanding recycling infrastructure, rising food processing activities, and strong mining operations across the region. Countries such as Brazil are witnessing increased deployment of automated sorting systems in material recovery facilities and agricultural processing industries, where improving efficiency and reducing material loss are key priorities.

Brazil Sensor-based Sorting Machine Market

The Brazil market is projected to reach around USD 75.13 million in 2026, representing roughly 3.5% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage is Driven by Advanced Sensor Technologies, Application Expertise, and System Integration Capabilities

The market is moderately consolidated, with competitive positioning driven by technological capabilities, application-specific expertise, and the ability to deliver high-performance sorting solutions across diverse industries such as recycling, food processing, and mining. Leading players such as TOMRA Systems ASA, Bühler Group, Steinert GmbH, Pellenc ST, and Sesotec GmbH maintain strong market positions by offering advanced sensor-based sorting systems capable of high-speed, accurate material identification and separation. Their competitive strength is reinforced by continuous innovation in sensor technologies, strong domain expertise in specific applications, and the ability to integrate sorting systems with broader processing and automation infrastructure.

Competitive differentiation is increasingly shaped by the ability to combine multiple sensor technologies such as optical, NIR, and X-ray with intelligent software and data-driven control systems to enhance sorting accuracy and operational efficiency. As industries focus on improving material recovery rates, product quality, and process optimization, market players are investing in next-generation sorting solutions with enhanced detection capabilities, modular system design, and improved adaptability to complex material streams. Additionally, the ability to deliver customized solutions tailored to specific material sensor types, processing requirements, and facility configurations is becoming a key factor in maintaining competitive advantage and expanding global customer relationships. Companies are also strengthening their service capabilities, including remote monitoring, predictive maintenance, and performance optimization, to support long-term operational efficiency for end users.

- For instance, in October 2024, Steinert GmbH expanded its sensor-based sorting solutions portfolio with advanced systems designed to improve metal recovery efficiency and enhance performance in complex recycling environments.

LIST OF KEY SENSOR-BASED SORTING MACHINE COMPANIES PROFILED:

- TOMRA Systems ASA (Norway)

- Bühler Group (Switzerland)

- Steinert GmbH (Germany)

- Pellenc ST (France)

- Sesotec GmbH (Germany)

- Binder+Co AG (Austria)

- CP Manufacturing (U.S.)

- MSS, Inc. (U.S.)

- Raytec Vision S.p.A. (Italy)

- Cimbria (AGCO Corporation) (Denmark)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Binder+Co AG expanded its sensor-based sorting solutions for glass recycling applications, focusing on improving cullet purity and processing efficiency in high-volume recycling plants.

- October 2025: MSS, Inc. (CP Group) advanced its optical sorting technologies for material recovery facilities, enhancing automation capabilities and throughput efficiency in waste processing operations.

- September 2025: Raytec Vision S.p.A. introduced enhanced optical sorting systems for food applications, aimed at improving defect detection and product quality in fruit and vegetable processing.

- August 2025: Cimbria (AGCO Corporation) strengthened its grain sorting portfolio by integrating advanced sensor technologies to support higher accuracy and productivity in agricultural processing.

- July 2025: REDWAVE (BT-Wolfgang Binder GmbH) expanded its sensor-based sorting systems with improved detection capabilities for complex recycling streams, targeting higher recovery rates and operational efficiency.

REPORT COVERAGE

The global sensor-based sorting machine market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.7% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Sensor Type, Machine Type, Application, and Region |

| By Sensor Type |

|

| By Machine Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1,991.09 million in 2025 and is projected to reach USD 3,870.63 million by 2034.

In 2025, the market value stood at USD 466.90 million.

The market is expected to exhibit a CAGR of 7.7% during the forecast period.

By application, the recycling & waste management segment leads the market.

The rising demand for efficient material sorting, increasing recycling initiatives, automation adoption, need for high accuracy, and advancements in sensor technologies drive market growth.

TOMRA Systems ASA, Bühler Group, Steinert GmbH, Pellenc ST, and Sesotec GmbH are the top players in the market.

Europe held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us