Shared Mobility Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Vehicle, Commercial Vehicles, and Two-Wheelers), By Business Model (Ride-Hailing, Car-Sharing, Peer Peer Rental, and Others), By Propulsion Type (Electric and Conventional Engine), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

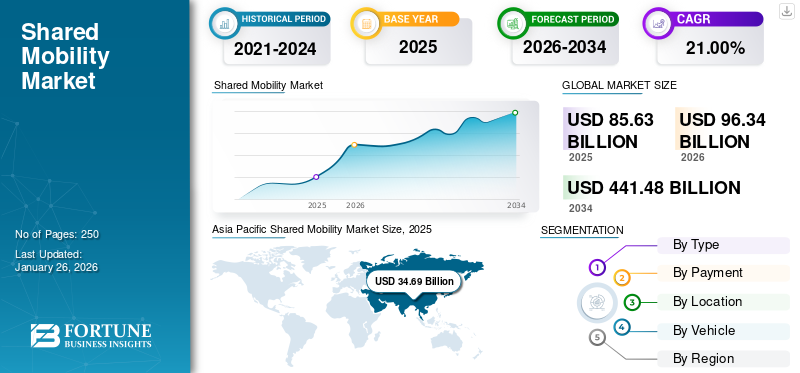

The global shared mobility market size was valued at USD 85.63 billion in 2025 and is projected to grow from USD 96.34 billion in 2026 to USD 441.48 billion by 2034, registering a CAGR of 21.00% over the forecast period. Asia Pacific dominated the shared mobility market with a market share of 40.51% in 2025. The Shared Mobility Market in the U.S. is projected to grow significantly, is projected to reach an estimated value of USD 45.45 Billion By 2032.

The market is driven by cost savings, increasing urbanization, rising fuel costs, and growing environmental concerns. Government initiatives, technological advancements like AI and IoT, and the adoption of Mobility-as-a-Service (MaaS) further propel growth, alongside expanding micromobility options and evolving consumer preferences for flexible transportation solutions.

Shared mobility is a modern approach to transportation that involves the shared use of vehicles as required. This concept encompasses various services such as car sharing, ride-hailing services, carpooling, bike-sharing, and others. By leveraging technology such as mobile apps and digital platforms, the approach aims to reduce private vehicle ownership and usage while increasing the efficiency and accessibility of transportation.

Download Free sample to learn more about this report.

Shared Mobility Market Key Takeaways

- 2025 Market Size: USD 85.63 billion

- 2026 Market Size: USD 96.34 billion

- 2034 Forecast Market Size: USD 441.48 billion

- CAGR: 21.00% from 2026–2034

- The E-hailing segment is projected to account for 90.11% of the market in 2026.

- The Non-cash payment segment is expected to hold 90.12% market share in 2026.

- The Non-airport segment is projected to capture 87.36% market share in 2026.

North America

North America represented 19.83% of the global market in 2025, valued at USD 16.98 billion.

Asia Pacific

Asia Pacific accounted for 40.51% of global revenue in 2025, valued at USD 34.69 billion.

Europe

Europe held a 36.49% share in 2025, generating USD 31.24 billion.

U.S.

The market projected to reach USD 16.88 billion by 2026 and USD 45.45 billion by 2032.

Japan

The market projected to reach USD 5.57 billion by 2026.

Read More

Shared Mobility Market Trends

Favorable Trends Associated with Autonomous Vehicles to Drive Market Growth

Autonomous vehicles represent a significant trend in the market, with the potential to revolutionize transportation. Companies such as Waymo, Cruise, and Uber are spearheading efforts to integrate self-driving cars into ride-hailing transport services. Currently, this technology is in an extensive testing phase, operating in controlled environments or specific geographic areas. Autonomous vehicles are likely to reduce operational costs for service providers by eliminating the need for human drivers.

Safety improvements associated with autonomous vehicles may increase consumer trust in shared mobility services. This could encourage more people to shift away from private car ownership, further boosting the market. Additionally, autonomous vehicles could enable new service models, such as dynamic ride-sharing with more efficient route optimization.

However, the integration of autonomous vehicles into mobility services presents challenges. These include regulatory hurdles, the need for significant infrastructure investments, and potential job displacement in the transportation sector. The timeline for widespread autonomous vehicle adoption remains uncertain, which could affect the pace of change in the market.

Furthermore, AI-driven predictive analytics is playing a crucial role in optimizing fleet management, demand forecasting, and reducing idle time for shared vehicles. Companies are increasingly leveraging machine learning to enhance vehicle allocation, improving customer experience and profitability. Additionally, the development of vehicle-to-infrastructure (V2I) technology is expected to improve traffic flow and increase the efficiency of shared mobility solutions.

Download Free sample to learn more about this report.

Shared Mobility Market Growth Factors

Benefit of Cost Savings to Drive the Growth of the Market

Cost savings is a significant driving factor in the shared mobility market. For many individuals, especially those living in urban areas, these services offer a more economical alternative to private vehicle ownership. The expenses associated with owning a car – including purchase costs, insurance, fuel, maintenance, and parking – can be substantial. In contrast, shared mobility allows users to access transportation as required, paying only for their actual usage. This pay-per-use model eliminates the need for large upfront investments and ongoing fixed costs.

Shared mobility users can avoid unexpected expenses such as repairs or depreciation. For occasional drivers or those who primarily need transportation for short trips, shared services can result in significant savings compared to the total cost of ownership. This economic advantage is particularly appealing to budget-conscious consumers, young professionals, and urban dwellers who have access to multiple transportation options. As awareness of these cost benefits grows, more people are likely to consider the shared approach as a viable and financially prudent transportation solution.

Additionally, the growing popularity of subscription-based mobility services is further enhancing cost efficiency. Companies are offering flexible subscription models, allowing users to access various types of vehicles on demand without long-term commitments. These models are particularly gaining traction among corporate clients looking to optimize employee travel costs.

RESTRAINING FACTORS

Regulatory Challenges to Affect Market Expansion

Regulatory challenges pose a significant hurdle for the shared mobility market share expansion. The regulatory landscape for these services is often complex, inconsistent, and rapidly evolving, creating hurdles for companies operating in this space. Different cities, states, and countries may have varying rules and requirements regarding licensing, insurance, driver background checks, vehicle safety standards, and operational practices. This regulatory patchwork makes it difficult for companies to scale their operations across multiple jurisdictions, as they must navigate and comply with a diverse set of regulations.

In some cases, existing transportation laws may not adequately address new shared mobility models, leading to legal gray areas or outright bans. Additionally, regulatory bodies may struggle to keep pace with technological innovations, resulting in outdated or inappropriate regulations. The process of working with local authorities to develop suitable regulations can be time-consuming and resource-intensive for mobility companies. Furthermore, sudden regulatory changes or stricter enforcement can disrupt established services or business models, creating uncertainty for both providers and users. This regulatory complexity increases operational costs and can slow down market entry and innovation, potentially restraining the growth of the market.

Cybersecurity and data privacy concerns also pose significant challenges to market expansion. As shared mobility platforms rely on vast amounts of user data, ensuring robust cybersecurity measures is crucial to maintaining consumer trust. Regulatory scrutiny around data protection is increasing, requiring mobility providers to implement stringent compliance measures. Additionally, environmental regulations aimed at reducing emissions are pushing companies to transition towards electric and hybrid vehicle fleets, necessitating substantial capital investments.

Shared Mobility Market Segmentation Analysis

By Type Analysis

Convenience and Accessibility to Propel Demand for E-hailing Services

By type, the market is segmented into e-hailing, micromobility, ride pooling, and car sharing.

The e-hailing segment led the market, accounting for 90.11% of the global market share in 2026. The demand for e-hailing services has been on a significant upward trajectory in recent years and is expected to dominate the market over the next few years. E-hailing apps provide users with the ability to request rides at any time and from any location, simply using their smartphones. This ease of use has made transportation more accessible, especially in areas underserved by traditional taxi services or public transit. The reliability and transparency offered by e-hailing platforms have also contributed to their growing popularity. Features such as real-time tracking, estimated arrival times, and upfront pricing give users a sense of control and predictability that traditional taxi services often lack.

Competitive pricing strategies employed by car sharing companies have made their services an attractive alternative. Dynamic pricing models, while sometimes controversial, have helped balance supply and demand. The integration of multiple transportation options within a single app has further enhanced the appeal of car sharing platforms, making them central to many users’ urban mobility strategies. Moreover, advancements in AI and data analytics are enabling service providers to optimize routes, reduce wait times, and offer personalized ride options based on user preferences. This technological evolution is expected to further streamline operations and drive market penetration.

To know how our report can help streamline your business, Speak to Analyst

By Payment Analysis

Safety and Security Measures of Online Payments to Drive Non-cash Segment Growth

Based on payment, the market is split into cash and non-cash.

Non-cash segment is projected to reach 90.12% of the market share in 2026. With the ongoing concerns about physical cash handling, digital payment methods offer strong security features, such as encryption and fraud protection, which are appealing to users. Many mobility services are integrating advanced technologies, such as mobile apps and contactless payment systems, which streamline the user experience and encourage more people to utilize these services. The availability of multiple payment methods (credit/debit cards, digital wallets, cryptocurrencies, and others) caters to a broader audience, enhancing user satisfaction and encouraging use. These trends will accelerate the growth of the non-cash segment in the future.

The cash segment will witness slower growth during the forecast period. While cash payments were once a staple in the market, their prevalence has significantly declined in recent years. The industry has undergone a transformation driven by factors such as technological advancements, changing consumer preferences, and regulatory shifts. Cash handling is time-consuming for both riders and operators, leading to wait times and operational bottlenecks longer.

Regulatory initiatives promoting digital transactions and cashless economies in various regions are pushing shared mobility operators to phase out cash-based payments, further boosting the adoption of non-cash alternatives.

By Location Analysis

Diverse Range of Customer Needs to Propel Adoption of Shared Mobility in Non-airport Locations

Based on location, the market is segmented into airport and non-airport.

The non-airport segment is projected to reach 87.36% of the global market share in 2026. The market has expanded rapidly beyond airport terminals, catering to a diverse range of user needs and preferences across various urban and suburban locations. These include bustling business districts, residential neighborhoods, educational institutions, healthcare facilities, public transportation hubs, shopping centers, and industrial parks. While these locations offer significant growth opportunities, operators must navigate challenges such as fluctuating demand, infrastructure limitations, and complex regulations.

Airport segment will capture considerably lesser market share than non-airport segment and will grow at a steady pace within the forecast period. Airports have been a cornerstone of the shared mobility market growth. Their high foot traffic concentration of travelers with transportation options creates a prime environment for shared services. These services, such as ride-hailing, car-sharing, and bike-sharing, provide convenient and efficient transportation solutions for airport passengers, reducing reliance on traditional taxis and shuttles.

By Vehicle Analysis

Increasing Demand of Micromobility Services to Drive Demand of Scooters & Bikes

Based on vehicle, the market is divided into passenger vehicles and scooters & bikes.

The scooters & bikes segment is expected to attain rapid growth over the forecast period. Compact size, environmental friendliness, and affordability have made them attractive options for short-distance travel, especially in urban areas. As cities grapple with traffic congestion, these micromobility solutions offer a viable alternative to personal vehicles. This growing demand has led to the proliferation of bike and scooter-sharing services, transforming the urban transportation landscape. Furthermore, advancements in battery technology and increased investment in charging infrastructure are enhancing the reliability of electric scooters and bikes, making them a more viable option for urban mobility.

The passenger vehicles segment is projected to reach 97.98% of the global market share in 2026. The demand for cars within the shared mobility market is steadily increasing. While micromobility options such as electric scooters and bikes have gained significant traction, there remains a substantial need for larger vehicles to accommodate longer distances, group travel, and the transportation of goods. Car-sharing platforms and ride-hailing services are expanding their fleets to meet this growing demand, offering users convenient and flexible transportation alternatives to personal car ownership. The shift towards electric and hybrid vehicles within shared mobility fleets is expected to significantly reduce emissions and operational costs, further propelling market growth.

REGIONAL INSIGHTS

Geographically, the market is segmented into North America, Asia Pacific, Europe, and the rest of the world.

Asia Pacific Shared Mobility Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific contributed 40.51% to the global market in 2025, with a valuation of USD 34.69 billion, and is projected to reach USD 39.48 billion in 2026. Factors such as rapid urbanization, increasing traffic congestion, rising fuel costs, and a growing young, tech-savvy population are driving this growth. China and India, with their large populations and developing infrastructure, have become the hotspots for shared transportation platforms. This trend is expected to continue as more cities in the region adopt suitable transportation solutions and individuals opt for convenient and cost-effective mobility solutions. The Japan market is projected to reach USD 5.57 billion by 2026, the China market is projected to reach USD 23.16 billion by 2026, and the India market is projected to reach USD 3.91 billion by 2026.

Government initiatives in Asia Pacific, like China’s smart city projects and India’s Smart Cities Mission, are giving a major push to shared mobility solutions. With governments also investing heavily in 5G and IoT, the region is shaping up to be a global leader in smart mobility, and this momentum is expected to continue well into the next decade.

North America

In 2025, North America represented USD 16.98 billion, accounting for 19.83% of the worldwide market, and is projected to grow to USD 18.83 billion in 2026. North America will account for a considerable share over the forecast period. A rising awareness of climate change and air pollution is driving a shift toward sustainable transportation options. Shared mobility services often have a smaller environmental footprint compared to personal car ownership. Furthermore, shared transportation can reduce traffic congestion by encouraging carpooling and reducing the number of vehicles on the road. The U.S. market is projected to reach USD 16.88 billion by 2026.

In North America, companies are increasingly adopting Mobility-as-a-Service (MaaS) to streamline employee commuting and logistics. This shift is creating fresh opportunities for service providers to develop customized solutions for businesses, helping them integrate shared mobility into daily operations. As more corporations embrace this approach, North America is set to maintain a strong market presence in the years ahead.

Europe

The Europe market generated USD 31.24 billion in 2025, representing 36.49% of the global market landscape, and is expected to reach USD 34.96 billion in 2026. Many European cities have well-developed public transportation systems, making shared mobility a complementary mode of transport for first and last-mile connections. Compact city layouts, pedestrian-friendly zones, and cycling infrastructure create a favorable environment for shared services. Owning a car can be expensive in many European cities, making shared approach an attractive alternative for cost-conscious consumers. The France market is projected to reach USD 8.80 billion by 2026 and the Germany market is projected to reach USD 7.18 billion by 2026.

Europe, on the other hand, benefits from well-defined policies, particularly the EU’s Sustainable and Smart Mobility Strategy. These regulations encourage cities to incorporate shared mobility into their public transport networks, making urban transit more seamless. With local governments pushing for cleaner, more efficient mobility solutions, businesses have a strong incentive to collaborate on innovative transportation models. This regulatory clarity provides a stable foundation for growth across the region.

Rest of the world

The market in the rest of the world including Latin America and the Middle East & Africa will grow at the highest CAGR during the forecast period. Rest of the World contributed approximately USD 2.72 billion to the global market in 2025, accounting for 3.17% share, and is expected to reach USD 3.08 billion in 2026. Ongoing investments in transportation infrastructure, such as roads and public transportation, are creating a more favorable environment for shared mobility services. Large-scale events and conferences often generate significant demand for transportation, creating opportunities for service providers.

KEY INDUSTRY PLAYERS

Strategic Partnerships and Collaborations to Help Industry Players Gain Competitive Advantages

Leading players in the market are adopting various strategies such as mergers & acquisitions, expansion of sales and distribution networks, and collaborations to gain a strong foothold in the market. For instance, in May 2023, Uber Technologies Inc. entered into a partnership with Waymo to integrate Waymo’s autonomous driving technology with Uber’s ridesharing network.

List of Top Shared Mobility Companies:

- Uber Technologies Inc. (U.S.)

- Lyft (U.S.)

- Didi Chuxing Technology Company (China)

- Grab Holdings Inc. (Singapore)

- Cabify (Spain)

- Ola Cabs (India)

- Car2go NA, LLC (U.S.)

- Deutsche Bahn Connect GmbH (Germany)

- Bolt (Estonia)

- Gojek (Indonesia)

KEY INDUSTRY DEVELOPMENTS:

- June 2023 – Lyft entered into an agreement with Electrify America to provide discounted charging across charging locations across the country.

- March 2023 – Uber Technologies Inc. and bp pulse announced a new mobility agreement to accelerate the company’s plans to become a zero emissions mobility platform across the globe.

- December 2022 – Lyft announced that it is working with partners to add thousands of electric vehicles from Hyundai, Ford, Kia, Polestar, and others to the Express Drive rental program in the future.

- June 2019 – Grab received an investment of USD 300 million from Invesco Ltd. to accelerate Grab’s expansion in Asia.

- June 2019 – Grab announced a partnership with Splyt to provide convenient access to customers for ride-hailing services.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies, product types, end-users, designs, and technologies. Besides this, it offers an in-depth analysis and insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 21.00% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Payment

By Location

By Vehicle

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 85.63 billion in 2025 and is projected to grow from USD 96.34 billion in 2026 to USD 441.48 billion by 2034.

The market is expected to record a CAGR of 21.00% during the forecast period of 2026-2034.

The benefit of cost savings is anticipated to drive the growth of the market.

Asia Pacific is projected to hold a dominating market share during the forecast period.

Shared micromobility includes the use of shared bikes and scooters for individuals seeking first- and last-mile connections to public transportation

- 2021-2034

- 2025

- 2021-2024

- 250

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us