Slip Additives Market Size, Share & Industry Analysis, By Type (Fatty Amides, Waxes, Silicone-based, and Others), By Application (Packaging Films, Non Packaging Films, Plastic Compounding & Processing, Coatings & Inks, and Others), and Regional Forecast, 2026-2034

Slip Additives Market Size and Future Outlook

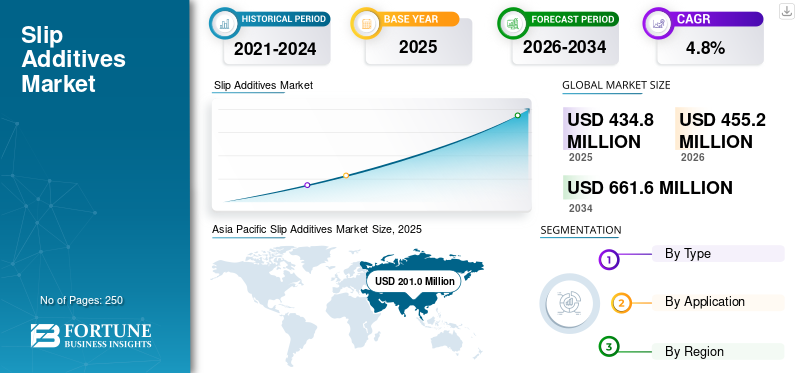

The global slip additives market size was valued at USD 434.8 million in 2025. The market is projected to grow from USD 455.2 million in 2026 to USD 661.6 million by 2034, exhibiting a CAGR of 4.8% during the forecast period. Asia Pacific dominated the slip additives market with a market share of 46.23% in 2025.

Slip additives are specialty polymers used to reduce friction between plastic film layers, between films and processing equipment, and across coated or molded plastic surfaces. These additives are commonly incorporated into polyolefin films, plastic compounds, masterbatches, coatings, and inks to improve film unwinding, bag opening, machinability, scratch resistance, rub resistance, and surface smoothness. Fatty amides such as erucamide, oleamide, stearamide, and behenamide remain the most widely used slip additives, while waxes, silicone-based additives, and specialty permanent slip systems are gaining relevance in higher-performance applications. Applications such as food, consumer goods, healthcare, and industrial packaging as well as engineered plastics, require additives that support process efficiency without compromising sealing, printing, lamination, or regulatory compliance. Therefore, the rising production of flexible packaging films, BOPP and CPP films, multilayer packaging structures, agricultural films, and plastic compounds will drive the product demand over the analysis period.

A mix of oleochemical suppliers, specialty additive manufacturers, and silicone additive producers with capabilities in fatty amide chemistry, polymer additive formulation, and surface-modification technologies shapes the global market. Key players include Cargill, BASF, Clariant, Evonik, Dow, and Momentive. Continuous investments in food-contact compliant additives, permanent slip technologies, silicone-based surface modifiers, bio-based oleochemical routes, and application-focused masterbatch formulations continue to strengthen competitive positioning.

Download Free sample to learn more about this report.

Slip Additives Market Key Takeaways

- 2025 Market Size: USD 434.8 million

- 2026 Market Size: USD 455.2 million

- 2034 Forecast Market Size: USD 661.6 million

- CAGR: 4.8% from 2026–2034

- Asia Pacific dominated the market with a 46.23% share in 2025.

- Fatty amides segment held the largest market share in 2025.

- Packaging films segment held the largest market share in 2025.

North America

The market reached USD 88.2 million in 2025, driven by flexible packaging and specialty films.

Asia Pacific

The market reached USD 201.0 million in 2025, driven by plastic film production and flexible packaging demand.

Europe

The market reached USD 101.8 million in 2025, supported by sustainable packaging and low-migration additives.

U.S.

The market is projected to reach USD 82.5 million by 2026, driven by flexible packaging and specialty films.

Japan

The market is expected to grow steadily, supported by strong plastic processing and demand for high-performance packaging additives.

Read More

SLIP ADDITIVES MARKET TRENDS

Shift toward Bio-based and Low-migration Additives to Accelerate Adoption in Sustainable Plastic Packaging

The growing shift toward sustainable plastic packaging is accelerating the adoption of bio-based, low-migration slip additives worldwide. Packaging converters and brand owners are increasingly focusing on materials that offer improved surface performance while supporting regulatory compliance, food-contact safety, and sustainability targets. The development of bio-based additives derived from renewable feedstocks are gaining attention as manufacturers seek to reduce their dependence on conventional petrochemical additives and eco-friendly solutions. At the same time, low-migration additives are preferred for food packaging, pharmaceutical packaging, hygiene films, and premium flexible packaging, where additive transfer, odor, and surface contamination remain key concerns. As packaging producers continue to balance performance with sustainability, the demand for advanced slip additive formulations is expected to increase steadily, thereby accelerating the product adoption across high-value plastic packaging applications.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Plastic Film Production for Flexible Packaging to Drive Market Growth

The rising plastic film production for flexible packaging is driving strong product demand worldwide. Flexible packaging is widely used in food and beverage, personal care, pharmaceuticals, household products, e-commerce, and industrial packaging due to its lightweight structure, cost efficiency, durability, and ease of handling. As film production volumes increase, manufacturers are placing greater emphasis on improving film processability, surface smoothness, roll handling, and packaging line efficiency. Slip additives play a critical role in reducing friction between film layers and processing equipment, enabling smoother winding, cutting, sealing, filling, and converting operations. They also help reduce blocking issues during storage and transportation, which is important for high-speed packaging environments. Therefore, the continued expansion of polyethylene and polypropylene films, especially in emerging economies, is set to drive the global slip additives market growth during the forecast period.

MARKET RESTRAINTS

Regulatory Scrutiny over Additive Migration May Limit Adoption in Food-contact and Sensitive Packaging Applications

Regulatory scrutiny over additive migration is limiting the adoption of certain slip additives in food-contact and sensitive packaging applications. The additives can migrate to the surface of plastic films to deliver friction-reducing performance. However, excessive or uncontrolled migration may raise concerns related to food safety, odor, taste transfer, packaging contamination, print adhesion, lamination performance, and sealing efficiency. Regulatory authorities and packaging buyers are increasingly evaluating additive behavior in consumer-sensitive applications such as food and pharmaceutical packaging. As a result, it is creating challenges for conventional slip additive formulations, especially where compliance with food-contact regulations and low-migration requirements is essential. Therefore, stricter migration-related expectations may limit the broader adoption of traditional slip additives in highly regulated, quality-sensitive plastic packaging segments.

MARKET OPPORTUNITIES

Expanding Product Use Cases in New Plastic Applications to Create Lucrative Opportunities for Market Players

The expanding use cases of slip additives in new plastic applications are creating lucrative opportunities for market players. Traditionally, the additives have been widely used in packaging films. However, their role is now extending into molded plastics, caps and closures, automotive components, agricultural films, industrial liners, consumer goods, masterbatches, sheets, and technical polymer applications. Manufacturers are increasingly using slip additives to improve surface smoothness, reduce friction, enhance demolding, minimize scratching, support easier handling, and improve processing efficiency across different plastic formats. This broadening application scope allows additive producers to move beyond conventional film-based demand and develop customized formulations for specific polymers, processing conditions, and performance requirements. Market players can benefit by offering specialty slip additive grades compatible with polyethylene, polypropylene, engineering plastics, recycled plastics, and bio-based polymers.

Segmentation Analysis

By Type

Fatty Amides Segment Dominated the Market Owing to Extensive Use in Packaging Films and Polyolefin Processing

Based on type, the market is segmented into fatty amides, waxes, silicone-based, and others.

The fatty amides segment accounted for the largest slip additives market share in 2025. Its dominance is supported by its wide use in polyethylene and polypropylene films, where it reduces the coefficient of friction, improves film handling, minimizes blocking, and supports smooth converting operations. Oleamide, erucamide, and stearamide-based additives are widely preferred in flexible packaging, agricultural films, consumer goods packaging, and industrial films due to their cost-effectiveness and reliable slip performance. Their compatibility with high-volume packaging film production and established use across polyolefin applications continues to support the segment’s leading position.

The waxes segment is expected to grow at a CAGR of 4.2% from 2026 to 2034, driven by their use as cost-effective additives to improve surface smoothness, dispersion, mold release, and processing efficiency. Their ability to enhance lubrication, reduce friction during processing, and support better pigment or filler dispersion makes them suitable for several industrial plastic applications. As processors continue to prioritize cost efficiency and stable processing behavior, wax-based slip additives will maintain steady demand across value-driven formulations.

The silicone-based segment is projected to expand at a CAGR of 5.4% over 2026 to 2034, driven by their superior durability, low coefficient of friction, scratch resistance, and long-lasting surface modification performance. Unlike conventional migrating slip agents, silicone-based additives can deliver more stable and persistent slip properties in demanding applications. Their adoption is increasing across specialty films, automotive plastics, consumer goods, engineering plastics, and high-performance molded components. The increasing demand for premium surface performance and better functional durability will assist the stronger adoption of silicone-based slip additives across high-value plastic applications.

By Application

Packaging Films Segment Dominated the Market Owing to High Slip Additive Consumption in Flexible Packaging

Based on application, the market is segmented into packaging films, non-packaging films, plastic compounding & processing, coatings & inks, and others.

To know how our report can help streamline your business, Speak to Analyst

The packaging films segment accounted for the largest market share in 2025, driven by high additive consumption across food packaging, personal care packaging, pharmaceutical packaging, household packaging, and industrial flexible packaging. The additives are essential in packaging films as they reduce friction, improve roll handling, prevent blocking, and enable smoother sealing, cutting, filling, and converting. Their strong use in the production of polyethylene and polypropylene films continues to reinforce segment demand. As flexible packaging remains the primary application area for high-volume plastic films, packaging films will continue to drive the global slip additive consumption during the forecast period.

The plastic compounding and processing segment is projected to grow at a CAGR of 4.9% over 2026 to 2034, as processors increasingly use slip additives to improve material flow, reduce friction, support demolding, and enhance surface finish. These additives are incorporated into masterbatches, molded plastics, sheets, profiles, and compounded polymer formulations to improve throughput and reduce processing-related defects. The product demand is particularly strong for automotive components, consumer products, industrial plastics, and packaging-related compounds, where better surface feel and smoother processing are important.

The others segment is expected to grow at a CAGR of 4.5% from 2026 to 2034, supported by the expanding product use in specialty consumer products, technical polymers, industrial components, liners, sheets, and selected engineered plastic applications. These applications use slip additives to enhance surface performance, reduce friction, improve release properties, and support smoother handling across non-conventional plastic formats. Although the segment accounts for a comparatively smaller share, it is gaining relevance as manufacturers explore new application areas beyond traditional film-based demand.

Slip Additives Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Slip Additives Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching USD 201.0 million, and is expected to remain the leading regional market. This is due to strong plastic film production, expanding flexible packaging consumption, and the presence of large-scale polymer processing industries across China, India, Japan, South Korea, and Southeast Asia. The increasing investments in packaging conversion capacity, rapid growth of e-commerce, and higher consumption of consumer goods are further strengthening the need for additives that improve film handling, reduce blocking, and enhance processing efficiency.

China Slip Additives Market

The China market accounted for approximately USD 88.3 million in 2026, representing around 19.4% of the global demand. The country remains one of the largest product consumers due to its extensive plastic film manufacturing base, strong flexible packaging output, and great downstream demand from food, consumer goods, industrial packaging, and e-commerce sectors. The continuous expansion of polyethylene and polypropylene film production is supporting consistent additive consumption.

To know how our report can help streamline your business, Speak to Analyst

India Slip Additives Market

The India market is poised to reach USD 34.1 million in 2026, accounting for nearly 7.5% of the global market. The market growth in the country is supported by the rapid expansion of flexible packaging, rising packaged food consumption, increasing organized retail penetration, and strong demand from FMCG, personal care, and pharmaceutical packaging. Domestic plastic processors are increasingly using slip additives to improve packaging line performance, film unwinding, and surface handling efficiency.

North America

The North America market reached USD 88.2 million in 2025 and is estimated to grow at a CAGR of 4.4% over 2026 to 2034. The region represents a mature yet technologically advanced market, supported by the strong demand for flexible packaging, specialty films, consumer goods packaging, and industrial plastic products. The presence of established packaging converters, carrier resin producers, and additive suppliers continues to support steady demand. In addition, the shift toward recyclable packaging structures and high-performance film formulations is encouraging the adoption of more advanced slip additive solutions.

U.S. Slip Additives Market

The U.S. market is anticipated to reach a value of USD 82.5 million in 2026, accounting for around 18.1% of global revenues. The product demand is driven by the country’s large flexible packaging industry, strong food and beverage packaging demand, and the growing use of specialty films in healthcare, personal care, and industrial applications. The U.S. also remains an important market for high-performance and low-migration slip additive formulations.

Europe

The Europe market recorded a value of USD 101.8 million in 2025, with the market expanding at a CAGR of 4.2% over 2026 to 2034. High regulatory scrutiny, strong sustainability commitments, and growing demand for premium packaging materials characterize the region. European converters are increasingly focusing on low-migration, bio-based, and recyclable packaging-compatible additives to meet food-safety, circular-economy, and brand-owner requirements. Although growth is comparatively moderate due to market maturity, the shift toward sustainable, high-performance film formulations continues to drive the demand for advanced slip additive technologies.

Germany Slip Additives Market

The Germany market is estimated to account for approximately USD 26.8 million in 2026, representing around 5.9% of the global demand. The market is supported by its strong packaging, automotive plastics, industrial film, and polymer processing industries. German converters and compounders place strong emphasis on performance consistency, regulatory compliance, and sustainable material design, which supports the demand for low-migration and specialty additives.

U.K. Slip Additives Market

The U.K. market is poised to reach a value of USD 12.9 million in 2026, contributing nearly 2.8% of global revenues. Flexible packaging, food-contact films, personal care packaging, and specialty plastic applications mainly support demand. The country’s continued focus on recyclable packaging formats and packaging waste reduction is encouraging the use of additive solutions that maintain film performance while supporting evolving sustainability requirements.

Latin America

The Latin America market reached USD 26.0 million in 2025 and is projected to grow at a CAGR of 4.8% during 2026–2034. The regional market is supported by the rising demand for flexible packaging across food, beverages, household products, agriculture, and consumer goods. Brazil and Mexico remain important contributors due to their large plastic processing bases and expanding packaged goods industries. While the region remains smaller than Asia Pacific, Europe, and North America, growth in packaged food consumption, retail modernization, and industrial packaging is expected to support steady additive demand.

Brazil Slip Additives Market

The Brazil market is poised to record a value of USD 12.0 million in 2026, accounting for about 2.6% of the global market. The country’s demand is supported by flexible packaging production for food, agriculture, personal care, and household products. Growth in plastic film processing, coupled with the need for better film handling and anti-blocking performance in tropical storage and transportation conditions, continues to support slip additive consumption.

Middle East & Africa

The Middle East & Africa market stood at USD 17.7 million in 2025 and is projected to expand at a CAGR of 5.0% over 2026 to 2034. The product demand is supported by the growing plastic packaging production, expanding petrochemical-based polymer processing capacity, and increasing consumption of flexible packaging across food, retail, hygiene, and industrial applications. The Middle East benefits from strong resin production and downstream plastics conversion, while African markets are gradually seeing higher demand for packaged consumer goods and agricultural films.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Additive Manufacturers Strengthen Competitive Edge through Specialty Formulations and Application-specific Slip Solutions

The global slip additives market is moderately consolidated, with competition shaped by product performance, polymer compatibility, regulatory compliance, and technical formulation expertise. Key players such as Cargill, BASF, Clariant, Evonik, Dow, and Momentive compete through fatty amide additives, wax-based solutions, silicone-based additives, and customized masterbatch formulations. Companies are increasingly focusing on low-migration, food-contact-approved, bio-based, and permanent slip solutions to address evolving packaging and polymer-processing requirements. Competitive strategies include product launches, capacity expansion, strengthening regional supply, acquisitions, and collaborations with film converters and compounders. As demand rises across flexible packaging, coatings, inks, molded plastics, and recycled polymer applications, manufacturers are expected to prioritize application-specific innovation and sustainable additive portfolios to strengthen their market positions.

LIST OF KEY SLIP ADDITIVES COMPANIES PROFILED

- Cargill (U.S.)

- BASF (Germany)

- Clariant (Switzerland)

- Evonik (Germany)

- Kao Chemicals (Japan)

- KLK OLEO (Malaysia)

- Fine Organics (India)

- Dow (U.S.)

- BYK (Germany)

- Momentive (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Avient Corporation launched Hiformer Slip + Antistatic for BOPP Films in Latin America. The additive combines slip and antistatic performance in one formulation, helping BOPP film producers improve COF control, film clarity, and extrusion cleanliness.

- May 2025: Ampacet introduced SLIP SCAVENGER 1540 for flexible packaging with recycled polyethylene content. The solution will enable the management of inconsistent slip behavior in PCR-based films, thereby improving processing reliability.

- February 2024: Tosaf completed North American investments that increased its additive and color masterbatch production capacity by 40%. The expansion strengthened the company’s regional supply of packaging film and polymer-processing customers.

- October 2023: Ampacet introduced PERMSLIP 1409, a permanent slip masterbatch for flexible packaging. The product will offer consistent, low COF performance and help reduce additive transfer during film conversion.

REPORT COVERAGE

The global slip additives market analysis provides an in-depth study of market size and forecast across all market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.8% from 2026-2034 |

| Unit | Value (USD Million), Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 434.8 million in 2025 and is projected to reach USD 661.6 million by 2034.

In 2025, the Asia Pacific market value stood at USD 201.0 million.

The market is slated to exhibit steady growth at a CAGR of 4.8% during the forecast period of 2026-2034.

The packaging films application segment led the market in 2025.

The continued expansion of polyethylene and polypropylene films, especially in emerging economies, is a key factor set to drive market growth.

Cargill, BASF, Clariant, Evonik, Dow, and Momentive are the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Shift toward bio-based and low-migration slip additives are the key factors anticipated to accelerate product adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us