Smart Cars Market Size, Share & Industry Analysis, By Level of Automation (Level 0–1, Level 2, Level 3, Level 4 & Above), By Connectivity Type (Embedded Connectivity, Tethered Connectivity, and Integrated Connectivity), By Propulsion Type (ICE, Hybrid, and BEV), By Vehicle Type (Hatchback, Sedan, SUV, and LCVs), By Feature Integration Category (Advanced Driver Assistance Systems (ADAS), Infotainment & Digital Cockpit, Telematics & Remote Diagnostics, and Autonomous Driving Compute Platforms), and Regional Forecast, 2026–2034

Smart Cars Market Size and Future Outlook

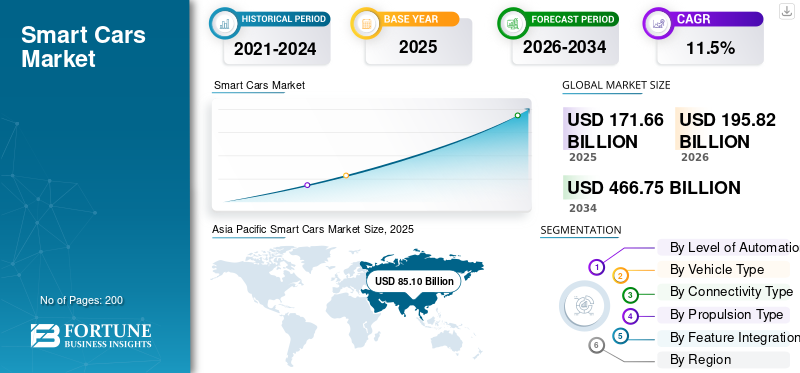

The global smart cars market size was valued at USD 171.66 billion in 2025. The market is projected to grow from USD 195.82 billion in 2026 to USD 466.75 billion by 2034, exhibiting a CAGR of 11.5% during the forecast period. Asia Pacific dominated the smart cars market with a market share of 49.57% in 2025.

Smart cars are technologically advanced vehicles equipped with connectivity, automation, sensors, and intelligent control systems that enhance safety, efficiency, and driving comfort, and enable features such as driver assistance and autonomous driving.Market drivers, including rising consumer demand, technological advancements, supportive government regulations, increasing investments, urbanization, and evolving industry trends, accelerate product adoption and expansion.

Major players in the smart cars market include Tesla, BMW Group, Mercedes-Benz Group, Volkswagen AG, Toyota Motor Corporation, General Motors, and BYD, competing through advanced autonomous technologies, connected vehicle platforms, AI-driven systems, electrification strategies, and continuous innovation in safety and mobility solutions.

Download Free sample to learn more about this report.

SMART CARS MARKET TRENDS

Advancements in Connected and Autonomous Technologies Shaping Market Trends

The integration of advanced connectivity, artificial intelligence (AI), and autonomous driving technologies is a prominent trend in the smart cars market. Automakers are increasingly embedding over-the-air updates, real-time navigation, vehicle-to-everything V2X communication, and advanced driver assistance systems into new models. Consumers are demanding seamless digital experiences comparable to those on smartphones, pushing manufacturers toward software-defined vehicle architectures. Strategic collaborations between automotive OEMs and technology firms are accelerating innovation, redefining mobility ecosystems, and transforming how vehicles interact with drivers, infrastructure, and surrounding environments.

- In February 2026, Visteon and TomTom launched the world’s first in-car local AI navigation system, integrating embedded large language models, on-device processing, real-time map rendering, and cloud fallback, enabling low-latency and offline-capable intelligent route guidance.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Consumer Demand for Safer and More Efficient Mobility Driving Market Growth

Increasing awareness regarding road safety, fuel efficiency, and driving comfort is significantly driving the smart cars market growth. Consumers are prioritizing vehicles equipped with advanced driver assistance systems, adaptive cruise control, collision avoidance, and intelligent parking solutions. Urban congestion and rising accident rates are further encouraging the adoption of intelligent mobility technologies. Additionally, the supportive government regulations mandating safety features and emission reductions are strengthening market demand. Automakers are responding by expanding smart feature integration across mid-range and premium vehicle segments globally.

- In February 2026, Wayve secured a major investment round from leading automakers to accelerate development of its AI-driven autonomous driving software, leveraging end-to-end deep learning models, real-world data training, and scalable ADAS-to-Level-4 architecture deployment.

MARKET RESTRAINTS

High Development and Integration Costs Restraining Market Expansion

The substantial costs associated with research, development, and integration of advanced sensors, semiconductors, and software platforms pose a key restraint in the smart car market. Developing autonomous and connected technologies requires continuous investment in cybersecurity, testing, and system validation. Smaller manufacturers often face financial and technical barriers to large-scale deployment. Moreover, fluctuating semiconductor supply chains and high component prices can increase vehicle costs, limiting affordability for price-sensitive consumers and slowing widespread adoption in emerging markets.

MARKET OPPORTUNITIES

Rapid Expansion of Smart City Projects Present New Market Opportunities

The rapid expansion of smart city projects worldwide presents significant opportunities for the smart cars market. Governments are investing in intelligent transportation systems, digital infrastructure, and connected road networks to improve urban mobility efficiency. Smart vehicles capable of vehicle-to-infrastructure communication can seamlessly integrate into these ecosystems. As cities modernize traffic management and prioritize sustainable mobility, demand for connected and semi-autonomous vehicles is expected to rise. Partnerships between automotive manufacturers, telecom providers, and municipalities will further unlock long-term growth potential.

- In January 2025, Toyota announced the completion of Phase 1 construction of Woven City, a fully connected mobility test course integrating hydrogen energy systems, autonomous e-Palette vehicles, smart infrastructure sensors, and real-time data exchange platforms.

MARKET CHALLENGES

Cybersecurity and Data Privacy Concerns Challenging Market Adoption

As smart cars rely heavily on vehicle connectivity and data exchange, cybersecurity risks remain a critical challenge. Connected vehicles generate and transmit vast amounts of user and operational data, making them potential targets for hacking and data breaches. Ensuring secure communication channels, software integrity, and regulatory compliance requires continuous technological upgrades and monitoring. Consumer concerns regarding data privacy and system reliability may impact purchase decisions. Addressing these risks through robust encryption, secure architectures, and global standards is essential for sustained market confidence.

Segmentation Analysis

By Level of Automation

Widespread Conventional Vehicle Production and Regulatory Safety Mandates to Sustain Level 0–1 Segment Dominance

Based on the level of automation, the market is segmented into level 0–1, level 2, level 3, and level 4 & above.

The level 0–1 segment dominates the smart cars market share due to its extensive penetration across mass-market vehicles globally. Most vehicles currently in operation incorporate basic driver assistance features such as lane departure warning and automatic emergency braking. Cost-effective integration, regulatory safety mandates, and large-scale production volumes ensure steady market share and consistent technology adoption across emerging and developed markets.

The Level 3 segment is projected to expand at a CAGR of 34% over the forecast period. Increasing approvals for conditional autonomous driving, premium vehicle launches, and advancements in AI-powered perception systems are accelerating Level 3 deployment, particularly in technologically advanced automotive markets.

- In November 2025, General Motors unveiled next-generation software-defined vehicle advancements at its GM Forward event in NYC, highlighting centralized compute architecture, Ultifi software platform upgrades, enhanced advanced driver assistance systems ADAS capabilities, and scalable over-the-air update integration.

By Vehicle Type

Rising Consumer Preference for Versatile and Feature-Rich Vehicles to Accelerate SUV Segment Leadership

Based on vehicle type, the market is segmented into hatchback, sedan, SUV, and LCVs.

The SUV segment dominates the smart cars market and is also the fastest growing, driven by rising consumer preference for spacious, technologically advanced, and premium-feature vehicles. Higher integration of ADAS, connectivity systems, and semi-autonomous functionalities in SUVs enhances their market share. Growing urbanization, improving disposable incomes, and strong OEM focus on SUV electrification and smart platform integration further accelerate segmental expansion globally.

- In February 2026, Volkswagen announced that the 2026 Taigun and Virtus facelifts will launch within six months, featuring upgraded infotainment systems, enhancing user experience with digital cockpit interfaces, Level 2 ADAS integration, and improved connected car technologies.

The LCV segment holds the third-largest market share and is projected to grow at a CAGR of 11.6% during the forecast period. Expanding e-commerce, fleet digitization, and adoption of telematics-enabled commercial vehicles are driving smart feature integration in light commercial vehicle fleets.

To know how our report can help streamline your business, Speak to Analyst

By Connectivity Type

Cost-Effective Smartphone Integration and Mass-Market Adoption to Strengthen Tethered Connectivity Dominance

Based on connectivity type, the market is segmented into tethered connectivity, embedded connectivity, and integrated connectivity.

The tethered connectivity segment dominates the smart cars market due to its affordability and widespread compatibility with smartphones. Consumers prefer leveraging mobile-based applications for navigation, infotainment, and real-time updates without significantly increasing vehicle costs. Automakers increasingly offer tethered systems in entry- and mid-level vehicles, ensuring high-volume adoption and sustained market share across price-sensitive and emerging automotive markets.

The integrated connectivity segment is the fastest-growing, projected to expand at a CAGR of 12.2% over the forecast period. Rising demand for seamless cloud-based services, over-the-air updates, advanced telematics, and vehicle-to-everything (V2X) communication is accelerating adoption in premium and next-generation smart vehicles.

- In February 2026, Uber unveiled Uber Autonomous Solutions, introducing a scalable platform integrating fleet management APIs, real-time telematics, autonomous vehicle dispatch algorithms, and delivery optimization tools to accelerate global autonomous mobility and logistics deployment.

By Propulsion Type

Extensive Global Vehicle Base and Established Infrastructure to Sustain ICE Segment Dominance

Based on propulsion type, the market is segmented into ICE, hybrid, and BEV.

The ICE segment dominates the smart cars market due to its vast global vehicle parc, established fueling infrastructure, and affordability across developing economies. Automakers continue integrating advanced connectivity and driver assistance technologies into ICE vehicles to enhance competitiveness. Strong production volumes, widespread consumer familiarity, and gradual electrification transition timelines collectively support sustained market share for ICE-powered smart vehicles.

The BEV segment is the fastest-growing, with a CAGR of 18.3% over the forecast period. Accelerating electrification policies, battery cost reductions, expanding charging infrastructure, and rising consumer preference for zero-emission mobility are driving the rapid integration of smart features in battery-electric vehicles globally.

- In November 2025, Mercedes-Benz and Momenta announced co-development of next-generation ADAS, integrating end-to-end deep learning algorithms, high-performance computer platforms, multi-sensor fusion, and scalable Level 2+ to Level 3 autonomous driving capabilities.

By Feature Integration Category

Rising Demand for Connected User Experience to Strengthen Infotainment & Digital Cockpit Leadership

Based on the feature integration category, the market is segmented into advanced driver assistance systems (ADAS), infotainment & digital cockpit, telematics & remote diagnostics, and autonomous driving compute platforms.

The infotainment & digital cockpit segment holds the largest market share due to growing consumer preference for connected, personalized, and immersive in-vehicle experiences and driving experience. High adoption of touchscreens, voice assistants, digital instrument clusters, and smartphone integration across vehicle segments significantly supports sustained demand and widespread feature standardization.

The autonomous driving compute platforms segment is the fastest growing, projected to expand at a CAGR of 16.4% over the forecast period. Increasing investments in high-performance processors, AI-enabled perception systems, and centralized vehicle computing architectures are accelerating adoption in next-generation smart and semi-autonomous vehicles.

- In February 2026, Wayve raised USD 1.2 billion from NVIDIA, Uber, and three automakers to advance its end-to-end AI autonomous driving stack, utilizing an in-vehicle compute autonomous vehicle development kit, GPU-accelerated training infrastructure, and scalable Level 2–4 software deployment architecture.

Smart Cars Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Smart Cars Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is projected to register rapid growth over the forecast period. Strong vehicle production hubs in China, Japan, and South Korea, coupled with rapid electrification and autonomous technology investments, are accelerating market growth. Government incentives for connected mobility, expanding 5G infrastructure, and rising consumer demand for advanced in-vehicle technologies further strengthen regional leadership. Increasing smart city initiatives and growing middle-class vehicle ownership continue to elevate overall smart cars market demand across the region.

- In October 2025, Huawei powered smart EV ambitions, delivering advanced MDC in-vehicle compute platforms, HarmonyOS cockpit systems, high-resolution LiDAR integration, and end-to-end ADAS solutions supporting Level 2+ autonomous capabilities.

China Smart Cars Market

The China market in 2026 is estimated at around USD 60.50 billion, accounting for roughly 30.9% of global revenues. Strong domestic OEM presence, EV leadership, autonomous pilots, and policy-backed intelligent mobility ecosystems drive dominance.

Japan Smart Cars Market

The Japanese market in 2026 is estimated at around USD 16.99 billion, accounting for roughly 8.7% of global revenues. Advanced R&D, hybrid leadership, an aging-driver safety focus, and premium connected-car technology integration support steady expansion.

India Smart Cars Market

The India market in 2026 is estimated at around USD 6.85 billion, accounting for roughly 3.5% of global revenues. Rapid urbanization, rising disposable income, digital adoption, and regulatory safety mandates accelerate the fastest-growing demand.

Europe

Europe holds the second-largest market share and is projected to grow at a CAGR of 11.3% during the forecast period. Stringent vehicle safety regulations, strong premium vehicle presence, and aggressive electrification targets drive the integration of smart features. Leading automotive OEMs are heavily investing in software-defined vehicles and advanced driver assistance systems. Additionally, cross-border regulatory harmonization and strong R&D capabilities in autonomous technologies contribute to sustained market growth across Western and Northern Europe.

- In December 2025, Smart confirmed development of the compact electric SUV, featuring a dedicated EV platform, advanced digital cockpit system, Level 2 ADAS suite, over-the-air software updates, and enhanced connected vehicle capabilities.

Germany Smart Cars Market

The Germany market in 2026 is estimated at around USD 13.24 billion, accounting for roughly 6.8% of global revenues. Strong premium OEM base, Industry 4.0 capabilities, electrification targets, and autonomous testing frameworks drive growth.

U.K. Smart Cars Market

The U.K. market in 2026 is estimated at around USD 2.76 billion, accounting for roughly 1.4% of global revenues. Government-backed EV transition, connected vehicle trials, and advanced engineering capabilities support gradual market expansion.

North America

North America represents the third-largest market, supported by early technology adoption and a strong innovation ecosystem. The presence of leading technology companies and automotive manufacturers accelerates advancements in autonomous driving, AI-enabled platforms, and connected vehicle solutions. Consumer preference for SUVs and premium vehicles promotes higher penetration of advanced features. Favorable regulatory developments for autonomous vehicle testing and expanding EV infrastructure further support long-term market growth across the U.S. and Canada.

- In October 2025, Locomobi announced the relocation of all hardware manufacturing to Canada, strengthening production of its AI-enabled parking management systems featuring IoT sensors, cloud-based analytics, real-time vehicle recognition, and integrated smart mobility software platforms.

U.S. Smart Cars Market

The U.S. market in 2026 is estimated at around USD 31.37 billion, accounting for roughly 16.0% of global revenues. Strong technology ecosystem, autonomous innovation leadership, high SUV penetration, and expanding EV infrastructure sustain robust growth.

Rest of the World

The Rest of the World market is witnessing gradual growth as urbanization, digital transformation, and infrastructure development accelerate across Latin America, the Middle East, and Africa. Increasing smartphone penetration and expanding telematics adoption are encouraging connected vehicle integration. While cost sensitivity remains a constraint, improving economic conditions and government-led smart mobility initiatives are supporting incremental market demand. The growing investments in transportation modernization and fleet digitalization contribute to steady regional expansion.

- In February 2026, smart launched the smart car in the UAE, featuring a long-range battery pack, dual-motor AWD configuration, Level 2 ADAS suite, panoramic digital cockpit, and advanced connected vehicle technologies with over-the-air updates.

COMPETITIVE LANDSCAPE

Key Industry Players

Software-Defined Architectures, AI Integration, and Strategic Alliances Intensify Competitive Rivalry

The market is shaped with global automotive OEMs and technology leaders competing through software-defined platforms, AI-enabled driver assistance, and advanced connectivity ecosystems. Key players such as Tesla, BMW Group, Mercedes-Benz Group, Volkswagen AG, Toyota Motor Corporation, General Motors, and BYD focus on autonomous development, electrification, and over-the-air update capabilities. Strategic technology partnerships, semiconductor collaborations, and mobility platform investments strengthen competitive positioning. Continuous innovation in centralized computing, cybersecurity frameworks, and smart cockpit integration defines competitive intensity across developed and emerging automotive markets.

- In November 2024, BYD showcased its Intelligence Advancement at Dream Day 2024, unveiling DiPilot ADAS upgrades, advanced vehicle domain controllers, high-precision sensors, and enhanced intelligent cockpit systems supporting connected and semi-autonomous driving capabilities.

LIST OF KEY SMART CARS COMPANIES PROFILED

- Tesla, Inc. (U.S.)

- Toyota Motor Corporation (Japan)

- Volkswagen AG (Germany)

- Mercedes-Benz Group AG (Germany)

- BMW Group (Germany)

- General Motors Company (U.S.)

- BYD Company Ltd. (China)

- Hyundai Motor Company (South Korea)

- Stellantis N.V. (Netherlands)

- Honda Motor Co., Ltd. (Japan)

- Ford Motor Company (U.S.)

- Nissan Motor Co., Ltd. (Japan)

- SAIC Motor Corporation Limited (China)

- Volvo Car AB (Sweden)

- Geely Automobile Holdings Limited (China)

KEY INDUSTRY DEVELOPMENTS

- September 2025: smart confirmed the reinvention of its iconic city car, introducing a next-generation electric platform featuring advanced ADAS integration, over-the-air software updates, digital cockpit interfaces, and enhanced urban-range battery optimization.

- March 2025: Mercedes-Benz partnered with China’s Hesai to integrate high-resolution automotive LiDAR sensors into next-generation smart vehicles, enhancing long-range object detection accuracy, multi-sensor fusion performance, and scalable Level 3 autonomous driving capabilities for global markets.

- April 2024: Neusoft launched OneCoreGo 5.0 at Auto China 2024, a global smart mobility solution integrating centralized vehicle computing, cross-domain software architecture, AI-powered cockpit systems, and scalable connected vehicle services.

- January 2024: Huawei announced plans to establish a new smart car company in China, focusing on intelligent driving systems, HarmonyOS cockpit integration, MDC computing platforms, and advanced ADAS technologies for software-defined electric vehicles.

- January 2024: BYD announced a USD 14 billion investment to advance smart car development, strengthening intelligent driving algorithms, proprietary vehicle domain controllers, high-performance battery integration, and next-generation connected EV platforms.

- January 2024: Samsung partnered with Hyundai Motor Group to connect smart homes with vehicles, integrating the SmartThings IoT platform, in-vehicle infotainment systems, remote vehicle control, and seamless data synchronization across digital ecosystems.

- August 2023: Geely launched a new smart EV co-developed with Baidu, integrating Apollo autonomous driving software, high-performance in-vehicle compute systems, advanced voice AI, and over-the-air update-enabled connected vehicle architecture.

- March 2022: VinFast selected North Carolina for its electric vehicle assembly plant, featuring advanced manufacturing automation, integrated battery production, smart factory systems, and scalable EV platform development capabilities.

REPORT COVERAGE

The global smart cars market analysis provides an in-depth study of the market size & forecast by all the market segments included in the vehicle security components market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key car industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| By Level of Automation |

|

| By Vehicle Type |

|

| By Connectivity Type |

|

| By Propulsion Type |

|

| By Feature Integration Category |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 171.66 billion in 2025 and is projected to reach USD 466.75 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 85.10 billion.

The market is expected to exhibit a CAGR of 11.5% during the forecast period.

The SUV segment leads the market in terms of vehicle type.

Technological advancements in tire compounds are enhancing competitive performance.

Major players in the market include Tesla, BMW Group, Mercedes-Benz Group, Volkswagen AG, Toyota Motor Corporation, General Motors, and BYD, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us