Sodium Sulfate Market Size, Share & Industry Analysis, By Source (Natural and Synthetic), By Application (Detergents & Cleaning, Pulp & Paper, Textile & Dyeing, Glass, and Others), and Regional Forecast, 2026-2034

Sodium Sulfate Market Overview

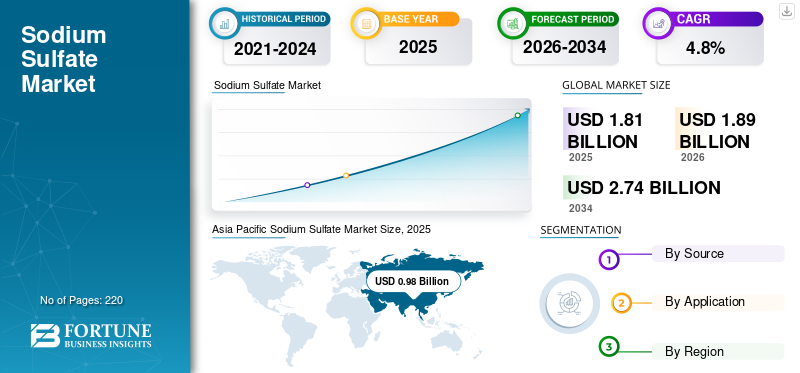

The sodium sulfate market size was valued at USD 1.81 billion in 2025. The market is projected to grow from USD 1.89 billion in 2026 to USD 2.74 billion by 2034 at a CAGR of 4.8% during the forecast period. Asia Pacific dominated the sodium sulfate market with a market share of 54.14% in 2025.

Sodium sulfate (Na2SO4) is an inorganic salt with the chemical formula Na₂SO₄, produced either from naturally occurring sodium-sulfate-bearing brines and evaporite deposits or recovered as a by-product of chemical processes such as cellulose, rayon, lithium carbonate, silica pigment, and related production routes. In commercial terms, the market covers both natural and synthetic types sold into bulk industrial applications, including detergents, glass, pulp and paper, textiles, and certain chemical processes.

The main driver for the market growth is its structural demand across large-volume, recurring industrial applications, especially detergents, followed by kraft pulp, textiles, and glass. Broad and recurring demand from detergent formulations, along with continued use in kraft pulp, textiles, and glass manufacturing, remains the key factor supporting the market growth. Key players operating in the market include Alkim Alkali Kimya A.Ş., Compañía Minera Río Tirón, Grupo SAMCA, Adisseo, and Saskatchewan Mining and Minerals Inc.

Download Free sample to learn more about this report.

SODIUM SULFATE MARKET TRENDS

Shift Toward Application-Specific Positioning and Differentiated End-Use Targeting are Evolving as Prominent Market Trends

A major trend in the market is its shift away from treating the material as a purely undifferentiated bulk salt and toward more application-specific positioning around purity, consistency, and end-use fit. Lenzing positions its Na2SO4 as a co-product of viscose and modal fiber production, with stable year-round availability and higher purity than unrefined sodium sulfate. Additionally, Crimidesa markets Na2SO4 explicitly for detergents and glass, based on performance needs such as flow, consistency, and clarification. This shows that the market is increasingly shaped by application suitability rather than tonnage availability.

Another trend is the gradual pressure on traditional filler-heavy detergent demand in regions shifting toward more compact formats. A.I.S.E. states that detergent compaction has been enabled by removing water and fillers from formulations, and its compaction factsheet also notes that liquid laundry detergents overtook powders in consumer preference in Europe. This pushes suppliers to diversify more actively into glass, pulp, chemicals, feed, and quality-differentiated industrial grades.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Recurring Demand Across Powder Detergents, Kraft Pulp, Textiles, and Glass Supports Market Expansion

One of the strongest drivers of the sodium sulfate market growth is its broad, recurring consumption across essential industrial applications. The product demand is growing as sodium sulfate serves practical process roles rather than only minor additive functions. TAPPI notes that kraft pulp mills require sulfur makeup, and Pulp & Paper Canada explains that Na2SO4, or salt cake, is used as a make-up chemical in kraft pulping to generate sodium sulfide in the recovery cycle. Crimidesa states that Na2SO4 functions as a clarifying agent in glass manufacturing, helping maintain a homogeneous melt and reducing imperfections. These end uses strengthen demand as they are tied to operating chemistry and manufacturing performance, not just optional formulation choices.

MARKET RESTRAINTS

Detergent Compaction, Format Shifts, and Weakness in Energy-Intensive Downstream Industries Can Limit Growth

A major restraint for the market is that detergent demand growth does not automatically translate into proportional growth in sodium sulfate intensity. A.I.S.E. states that detergent compaction has been achieved by taking water and fillers out of products, and it also highlights the longer-term market shift from powders toward liquids. Since Na2SO4 is highly important in powdered detergents as a bulking and flow-supporting component, this shift can reduce consumption per unit of cleaning performance even when the broader cleaning products market remains healthy.

This restraint is compounded by cyclical weakness in energy-intensive industrial sectors, especially glass. Glass Alliance Europe’s 2024–2025 statistical report says the European glass market remained under pressure in 2024 and early 2025, citing high energy costs, geopolitical spillovers, import pressure, plant closures, and a weak economic environment. As glass is one of sodium sulfate’s major industrial applications, weak furnace utilization and cautious capacity planning in glassmaking can soften sodium sulfate offtake in mature regions even when the product remains technically necessary.

MARKET OPPORTUNITIES

Circular By-product Recovery, Higher-Purity Grades, and Import-Reliant Markets Create Growth Opportunities

One of the clearest opportunities in the market is converting by-product streams into a stable, higher-value commercial supply. U.S. Geological Survey (USGS) states that Na2SO4 is recovered as a by-product from a wide range of chemical processes, including cellulose, rayon, lithium carbonate, and silica pigments. Lenzing’s Na2SO4 offer directly reflects this opportunity, positioning the product as a consistent-quality co-product from fiber production with higher purity than unrefined sodium sulfate. This creates space for suppliers to market sodium sulfate not merely as a low-cost commodity, but as a cleaner, more reliable circular raw material.

Another opportunity lies in expanding sales into specialized applications and import-dependent regions. Adisseo markets AdiSodium as a sodium sulfate feed material for poultry, swine, and ruminants, which shows that the addressable market extends beyond detergents and heavy industry. Similarly, World Integrated Trade Solution (WITS) data show substantial 2024 import demand in Brazil, Colombia, Indonesia, Mexico, and Tanzania, while Grupo SAMCA states that Minera de Santa Marta exports 80% of its 625,000-ton annual capacity to more than 40 countries. That combination points to continued opportunity in export-led supply models and in differentiated grades for feed and industrial niches.

MARKET CHALLENGES

Low-Value Bulk Economics, Freight Sensitivity, and Dual Supply Structure Challenges Market Development

A major challenge for the market is that it remains a relatively low-value bulk chemical whose economics are highly sensitive to transport and supply-chain execution. WITS data show that large import demand is spread across Latin America, Asia, and Africa rather than concentrated only near producing hubs. Similarly, export supply is led heavily by China and, to a lesser extent, Spain, the U.S., and India. This makes freight, container, or bulk logistics, and delivered reliability especially important in commercial competition similar to production costs.

The market also faces a structural balancing challenge as supply comes from two very different models. USGS states that Na2SO4 can come from natural brines and evaporite deposits or as a by-product from unrelated chemical processes. That depicts supply can tighten or expand for reasons outside product demand itself, such as mining conditions, upstream chemical operating rates, or broader shifts in cellulose, rayon, or lithium-linked production. This makes the market harder to balance than a simple standalone mineral sector and increases volatility in regional supply availability.

IMPACT OF TRADE PROTECTIONISM AND GEOPOLITICAL

Trade protectionism and geopolitical tensions can affect the market by increasing uncertainty around export availability, delivered costs, and industrial competitiveness in downstream sectors such as detergents, glass, and pulp. The OECD’s 2024 Inventory of Export Restrictions on Industrial Raw Materials says export restrictions are becoming increasingly prevalent and more prohibitive, with negative spillovers across global supply chains. Sodium sulfate is not usually framed as a critical mineral headline story, but it remains part of a trade-exposed industrial raw-material system that can still be affected by freight disruption, regional policy shifts, and tighter export conditions.

This is especially relevant as the trade structure for product is not evenly distributed. WITS data show China as the top exporter in 2024 and as a major importer in countries such as Brazil, Colombia, Indonesia, Mexico, and Tanzania. In practical terms, that depicts that disruptions in Chinese export flows, shipping costs, or regional industrial policy can ripple quickly into delivered pricing and customer sourcing strategies across multiple importing regions, even when underlying end-use demand remains stable.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is increasingly focused on purity control, application fit, and co-product valorization rather than on radical chemistry change. Lenzing emphasizes higher-purity sodium sulfate produced via a quality-controlled process, while Adisseo positions Na2SO4 as a feed material with defined nutritional functionality. This indicates that product development is moving toward performance within specific end-use systems, whether the goal is consistent detergent behavior, better industrial process compatibility, or a more controlled feed-grade profile.

This makes R&D significant for the product strongly application-led. In detergents, the focus is on particle behavior, flow, and formulation consistency, where Crimidesa explicitly links Na2SO4 to improving fluidity and consistency in powdered detergents. In glass, the focus is on melt clarification and homogeneity. In pulp, the emphasis remains on reliable sulfur makeup in the recovery cycle. Across the market, development priorities are therefore likely to remain centered on quality consistency, impurity control, and better fit within downstream manufacturing systems rather than on creating entirely new Na2SO4 chemistries.

SEGMENTATION ANALYSIS

By Source

Natural Segment Dominates Due to Strong Mineral-Based Supply and Broad Suitability for Bulk Industrial Uses

Based on source, the market is segmented into natural and synthetic.

Among these, natural segment is expected to hold the dominant share as it benefits from large-scale extraction from brines and evaporite deposits and remains strongly represented by major mineral-based producers. USGS identifies natural brines and crystalline evaporite deposits as key supply routes, while natural production has returned to prominence, especially in mainland China. Producers such as Alkim and Minera de Santa Marta also reinforce the importance of mineral-based production in commercial supply.

The synthetic segment also remains commercially important as it is tied to integrated chemical production and circular-economy models. USGS lists multiple by-product sources, and Lenzing shows how co-product sodium sulfate can be marketed in stable quantities and controlled purity. This segment may not lead in tonnage, but it remains important where customers value consistency, purity, and sustainability-linked sourcing.

By Application

To know how our report can help streamline your business, Speak to Analyst

Detergents & Cleaning Leads Due to Product’s Established Role in Powdered Detergent Formulations

Based on application, the market is segmented into detergents & cleaning, pulp & paper, textile & dyeing, glass, and others.

Among these, detergents & cleaning is expected to hold the leading sodium sulphate market share. Sodium sulfate is used as a filler and viscosity regulator in powdered laundry and dish‑washing detergents, helping to standardize bulk density and prevent caking. Increasing ownership of washing machines and dishwashers in households (especially across Asia Pacific and Latin America) is boosting detergent consumption.

The pulp & paper segment also holds a significant position as product remains relevant for sulfur makeup in kraft pulping. In kraft mills, Na2SO4 is converted to sodium sulfide, which helps maintain the alkaline cooking liquor and improves pulp yield and quality.

Textile & dyeing remains important as a long-standing industrial outlet, and glass is commercially relevant as Na2SO4 is used as a clarifying aid in the melt. Large‑scale dyeing and printing operations in China, India, Bangladesh, and Pakistan are major consumers of sodium sulfate–based dye auxiliaries.

The others segment includes chemical uses, such as sodium sulfide production and selected feed applications, broadening the market beyond a traditional detergent-focused view.

SODIUM SULFATE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Sodium Sulfate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the market. The region benefits from deep supply, broad detergent and textile manufacturing activity, and China’s overwhelming trade position. China remains the central market within Asia Pacific as it combines large-scale production with strong export reach and relevance across detergents, glass, chemicals, and textiles. Its dominance in export statistics suggests that China is not only the main supply hub, but also a major benchmark setter for global trade flows and pricing direction.

China Sodium Sulfate Market

China’s market is one of the largest globally, with 2025 revenue at USD 0.49 billion, representing roughly 16.1% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is expected to register steady demand during the forecast period. The region benefits from established industrial use in detergents, pulp and paper, and chemical applications, while the U.S. also remains a significant contributor in global exports. Growth is likely to be moderate rather than volatile, with market performance shaped more by industrial operating conditions than by entirely new product end uses.

U.S. Sodium Sulfate Market

In 2025, the U.S. market was USD 0.21 billion, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 11.7% of global market sales.

Europe

Europe is expected to maintain a significant position in the market due to its established natural sodium sulfate production base, integrated co-product supply, and mature glass and pulp industries. Europe is especially significant where consistency, industrial qualification, and differentiated grades is crucial. The region’s role is less about being the cheapest global source and more about serving customers that value stable quality, application fit, and diversified non-Chinese supply.

Germany Sodium Sulfate Market

The Germany market in 2025 was valued at around USD 0.07 billion, representing roughly 3.9% of global market revenues.

U.K. Sodium Sulfate Market

The U.K. market in 2025 was valued at around USD 0.04 billion, representing roughly 2.0% of global market revenues.

Latin America

Latin America is a smaller but relevant market. Brazil stands out as the most important market in Latin America as it was the one of the largest importer globally. This makes Brazil a major destination market for producers looking to grow through trade-based supply rather than local mineral extraction.

Brazil Sodium Sulfate Market

Brazil market in 2025 was valued at around USD 0.08 billion, representing roughly 4.4% of global market revenues.

Middle East & Africa

The Middle East & Africa market remains comparatively smaller, but it is commercially significant as several countries appear in global import rankings. Growth in the region is likely to depend on industrial development, access to competitively delivered supply, and continued expansion in detergents and basic manufacturing uses.

GCC Sodium Sulfate Market

GCC market in 2025 was valued at around USD 0.07 billion, representing roughly 3.8% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players in the Market Compete through Resource Access and Export Logistics

The market includes large natural sodium sulfate miners and processors such as Crimidesa, Grupo SAMCA’s Minera de Santa Marta, Alkim, Saskatchewan Mining and Minerals, and Searles Valley Minerals, alongside integrated or by-product suppliers such as Lenzing, Adisseo, Atul, Nippon Chemical Industrial, and Cooper Natural Resources. Public company materials show a clear split between mineral-based producers that emphasize deposit quality and bulk scale, and controlled-process suppliers that emphasize purity, steady quality, and application fit.

LIST OF KEY SODIUM SULFATE COMPANIES PROFILED

- Alkim Alkali Kimya A.Ş. (Turkey)

- Compañía Minera Río Tirón (Spain)

- Grupo SAMCA (Spain)

- Lenzing AG (Austria)

- Adisseo (France)

- Saskatchewan Mining and Minerals Inc. (Canada)

- Cooper Natural Resources (U.S.)

- Searles Valley Minerals (U.S.)

- Nippon Chemical Industrial Co. Ltd. (Japan)

- Atul Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Saskatchewan Mining and Minerals acquired Compass Minerals Wynyard Inc., an operating SOP facility in Saskatchewan. SMMI said the plant will operate as part of an integrated sulfate platform supported by sodium sulfate from Chaplin, and it also referenced a planned 50,000-100,000 ton SOP facility at Chaplin.

- May 2024: SMMI announced PrairiesCan funding to diversify production and improve sustainable production practices. The company said sodium sulphate operations would continue indefinitely and increase to 70,000 mt/y in 2025.

REPORT COVERAGE

The market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies and segmentation. In addition, it offers insights into the market and current industry trends, and highlights key developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Growth Rate | CAGR of 4.8% from 2026 to 2034 |

| Segmentation | By Source, By Application, By Region |

| By Source |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1.81 billion in 2025 and is projected to reach USD 2.74 billion by 2034.

Recording a CAGR of 4.8%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The detergents & cleaning segment is expected to lead the market during the forecast period.

Asia Pacific held the highest market share in 2025.

Recurring demand across powder detergents, kraft pulp, textiles, and glass supports market growth.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us