Soft Drink Concentrates Market Size, Share & Industry Analysis, By Product Type (Carbonated Drinks and Non-Carbonated Drinks), By Form (Liquid and Powder), By Flavor (Orange, Mango, Apple, Cola, Berry, Mixed Fruit, Grape, Grapefruit, Pineapple, and Others), By End-Use (Beverage Manufacturers, Foodservice, and Household), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

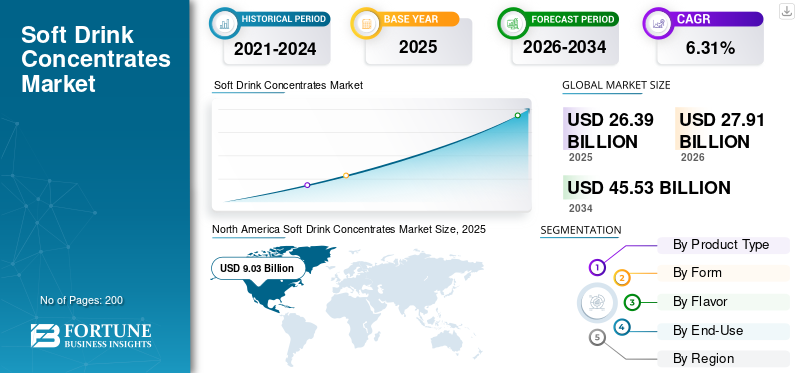

Soft Drink Concentrates Market Size and Future Outlook

The global soft drink concentrates market size was valued at USD 26.39 billion in 2025. The market is projected to grow from USD 27.91 billion in 2026 to USD 45.53 billion by 2034, exhibiting a CAGR of 6.31% during the forecast period. North America dominated the soft drink concentrates market with a market share of 34.22% in 2025.

Soft drink concentrates are flavoring and base solutions used by beverage manufacturers, foodservice providers, and households to prepare carbonated and non-carbonated drinks. These concentrates play a critical role in enabling scalable beverage production, ensuring consistency in taste, and reducing logistics costs compared to ready-to-drink beverages.

Market growth is primarily driven by increasing global consumption of soft beverages, the expansion of Quick-Service Restaurants (QSRs), and the rising demand for customized beverage solutions. Additionally, advancements in flavor innovation, sugar reduction technologies, and functional beverage formulations are further supporting market expansion.

Leading companies such as The Coca-Cola Company, PepsiCo Inc., Kerry Group plc, Döhler Group, and ADM are focusing on product innovation, strategic partnerships, and expansion of beverage concentrate portfolios to strengthen their global presence.

Download Free sample to learn more about this report.

Soft Drink Concentrates Market Key Takeaways

- 2025 Market Size: USD 26.39 billion

- 2026 Market Size: USD 27.91 billion

- 2034 Forecast Market Size: USD 45.53 billion

- CAGR: 6.31% from 2026–2034

- North America dominated the soft drink concentrates market with a 34.22% share in 2025.

- The non-carbonated segment is projected to grow at the fastest CAGR of 7.43% during the forecast period.

- The powder segment is expected to register the fastest CAGR of 8.25% over the forecast period.

North America

North America was valued at USD 9.03 billion in 2025 and is projected to reach USD 15.90 billion by 2034.

Europe

Europe reached USD 6.25 billion in 2025 and is projected to grow to USD 10.27 billion by 2034.

Asia Pacific

Asia Pacific was valued at USD 7.78 billion in 2025 and is expected to reach USD 14.16 billion by 2034, registering the fastest regional growth.

U.S.

The U.S. soft drink concentrates market was valued at approximately USD 7.48 billion in 2025.

Japan

Rising demand for healthier beverage concentrates is supporting market growth in Japan.

Read More

Soft Drink Concentrates Market Trends

Shift Toward Low-Sugar, Clean-Label, and Functional Beverage Concentrates to Shape Industry Trends

The global soft drink concentrates market growth is undergoing a structural shift toward healthier and more transparent product formulations. Consumers are increasingly prioritizing beverages that are low in sugar, free from artificial additives, and enriched with functional ingredients such as vitamins, minerals, and plant-based extracts. This is prompting manufacturers to reformulate traditional concentrates with natural sweeteners such as stevia and monk fruit, as well as to incorporate fruit-derived and botanical ingredients.

This trend is particularly strong in developed markets such as North America and Europe, where regulatory pressure and consumer awareness around sugar consumption are high. At the same time, emerging markets are witnessing rising demand for fruit-based and regional flavors, driving innovation in concentrate formulations.

- For instance, in August 2025, MONIN launched its PURE range in India as a no-added-sugar syrup line made from 100% natural fruit and plant-based extracts. This product targets health-conscious consumers such as chefs, bartenders, and baristas amid rising demand for low-sugar beverages.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Innovation in Flavor Systems and Product Formulation to Strengthen Market Growth

Continuous innovation in flavor systems and beverage formulation is emerging as a key growth driver in the soft drinks concentrates industry, as manufacturers respond to evolving consumer preferences for taste variety, health, and premium experiences. Companies are increasingly investing in advanced flavor technologies, including natural extraction methods, encapsulation techniques, and precision blending, to enhance flavor stability, shelf life, and sensory appeal in concentrate formats.

- For instance, in March 2025, Rasna launched “Rasna Rich,” a new powder‑concentrate soft‑drink line positioned as a thicker, richer, and more flavor‑forward version of its classic instant drink. Rasna Rich is marketed as a “richer, thicker, and tastier” powder concentrate, leveraging Rasna’s nostalgia‑driven brand equity while targeting a more premium taste experience at mass‑market pricing.

Market Restraints

Rising Health Concerns and Stringent Sugar Regulations to Restrict Market Growth

Growing consumer awareness regarding the adverse health effects of excessive sugar consumption, including obesity and diabetes, is limiting the demand for traditional soft drink concentrates. Governments across several regions are implementing sugar taxes, stricter labeling requirements, and reformulation mandates, which are impacting product demand and pricing structures.

- The World Health Organization (WHO) recommends reducing free sugar intake to less than 10% of total daily energy intake, influencing consumer purchasing behavior.

In addition, fluctuations in raw material costs, including sugar, fruit concentrates, and flavoring agents, can impact production margins and pricing strategies for manufacturers.

Market Opportunities

Rising Demand for Low-Sugar, Functional, and Natural Beverage Concentrates to Expand Market Potential

The shift toward healthier lifestyles are creating significant opportunities for manufacturers to develop innovative beverage concentrates with reduced sugar, natural ingredients, and functional benefits. Consumers are increasingly seeking beverages enriched with vitamins, minerals, electrolytes, and botanical extracts.

- For instance, in November 2025, Lipton expanded beyond traditional black tea by launching new fruit‑and‑herbal teas and a line of ready‑to‑dilute tea concentrates, both aimed squarely at “function plus flavor” and modern, convenience‑driven lifestyles.

SEGMENTATION ANALYSIS

By Product Type

Carbonated Drinks Segment Dominated the Market Due to Strong Global Consumption

Based on product type, the market is segmented into carbonated drinks and non-carbonated drinks.

The carbonated drinks segment held the dominant global soft drink concentrates market share, valued at USD 15.90 billion in 2025, driven by its widespread consumption and strong presence of global beverage brands. Carbonated beverages continue to remain a staple across both developed and emerging markets due to aggressive marketing, strong distribution networks, and consumer familiarity with cola-based drinks.

The non-carbonated segment is projected to grow at the fastest CAGR of 7.43% over the forecast period, supported by increasing demand for healthier alternatives such as fruit juices, flavored water, and low-sugar beverages.

To know how our report can help streamline your business, Speak to Analyst

By Form

Liquid Segment Dominated the Market Due to Ease of Integration in Beverage Production

Based on form, the market is segmented into liquid and powder.

The liquid concentrates segment dominated the market, valued at USD 25.18 billion in 2025, owing to its extensive use in large-scale beverage manufacturing and foodservice applications. Liquid formats ensure better solubility, uniformity, and process efficiency.

The powder segment is expected to grow at the fastest CAGR of 8.25% over the forecast period, driven by its longer shelf life, ease of storage, and increasing adoption in household and institutional applications.

By Flavor

Cola Segment Dominated the Market Due to Its Strong Global Demand

Based on flavor, the market is segmented into orange, mango, apple, cola, berry, mixed fruit, grape, grapefruit, pineapple, and others.

The cola segment led the market, valued at USD 7.98 billion in 2025, reflecting its dominance in carbonated beverage formulations and consistent consumer demand globally. Cola concentrates excel through enhanced flavor consistency, customizable sweetener levels, and reduced logistics costs, making them ideal for bottlers worldwide. Iconic brands such as Coca-Cola and PepsiCo reinforce this via global marketing and brand loyalty, sustaining high volumes despite health trends favoring low-sugar options.

Mango and mixed fruit segments are projected to grow at the fastest CAGRs of 9.02% and 8.44%, respectively, over the forecast period, respectively, driven by strong demand in the Asia Pacific and Latin America, where fruit-based beverages are gaining popularity.

By End-Use

Beverage Manufacturers Segment Dominated the Market Due to High Volume Industrial Demand

Based on end-use, the market is segmented into beverage manufacturers, foodservice, and household.

The beverage manufacturers segment dominated the market, valued at USD 18.86 billion in 2025, supported by large-scale production requirements and strong demand from global beverage companies.

The household segment is projected to grow at the fastest CAGR of 7.61% over the forecast period, driven by rising adoption of at-home beverage preparation and increasing availability of small-pack concentrate formats.

Soft Drink Concentrates Market Regional Outlook

Regionally, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Soft Drink Concentrates Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominates the global market, valued at USD 9.03 billion in 2025 and is projected to reach USD 15.90 billion by 2034, growing at a CAGR of 6.54% over the forecast period. Growth is driven by high per capita soft drink consumption, strong presence of leading beverage companies, and increasing demand for low-sugar and functional concentrates.

U.S. Soft Drink Concentrates Market

The U.S. dominates the North American market, valued at approximately USD 7.48 billion in 2025, supported by high consumption of carbonated beverages and strong foodservice demand. The market is expected to grow steadily, driven by reformulation toward low-calorie beverages.

Europe

Europe is valued at USD 6.25 billion in 2025, and is projected to reach USD 10.27 billion by 2034, registering a CAGR of 5.73% over the forecast period. Growth is supported by rising demand for natural ingredients and regulatory pressure to reduce sugar.

Germany Soft Drink Concentrates Market

Germany is a leading market in Europe, valued at approximately USD 1.35 billion in 2025, driven by strong beverage manufacturing and consumption trends.

U.K. Soft Drink Concentrates Market

The U.K. market was valued at approximately USD 1.20 billion in 2025, supported by sugar tax regulations and rising demand for healthier beverage alternatives.

Asia Pacific

Asia Pacific was valued at USD 7.78 billion in 2025 and is projected to reach USD 14.16 billion by 2034, growing at the fastest CAGR of 6.95% over the forecast period. Growth is driven by rapid urbanization, increasing disposable income, and expanding beverage consumption.

China Soft Drink Concentrates Market

China represents the largest market in the region, valued at approximately USD 2.59 billion in 2025, supported by growing demand for flavored beverages and expanding retail distribution.

South America and the Middle East & Africa

South America was valued at USD 2.45 billion in 2025 and is projected to reach USD 3.87 billion by 2034, registering a CAGR of 5.28% over the forecast period. Growth is driven by increasing soft drink consumption and improving distribution networks.

The Middle East & Africa market was valued at USD 0.88 billion in 2025 and is projected to reach USD 1.32 billion by 2034, expanding at a CAGR of 4.69% during the forecast period, supported by urbanization and rising demand for affordable beverage solutions.

Brazil Soft Drink Concentrates Market

Brazil dominates the regional market, valued at approximately USD 1.31 billion in 2025, driven by strong demand for carbonated beverages and local production capabilities.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Reformulation, Flavor Innovation, and Global Expansion to Gain Market Advantage

The global soft drinks concentrates market is moderately consolidated, with leading players competing through strong brand portfolios, advanced formulation capabilities, and extensive global distribution networks. Companies are increasingly investing in low-sugar formulations, natural flavor systems, and functional beverage solutions to align with evolving consumer preferences.

Key Players in the Soft Drink Concentrates Market

|

Rank |

Company Name |

|

1 |

The Coca-Cola Company |

|

2 |

PepsiCo Inc. |

|

3 |

Kerry Group plc |

|

4 |

Döhler Group |

|

5 |

Archer Daniels Midland Company (ADM) |

List of Key Soft Drink Concentrates Companies Profiled

- The Coca-Cola Company (U.S.)

- PepsiCo Inc. (U.S.)

- Kerry Group plc (Ireland)

- Döhler Group (Germany)

- Archer Daniels Midland Company (U.S.)

- Givaudan SA (Switzerland)

- International Flavors & Fragrances Inc. (U.S.)

- Symrise AG (Germany)

- Sensient Technologies Corporation (U.S.)

- Tate & Lyle PLC (U.K.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Rasna recently launched Nutri+, a nutritional beverage concentrate fortified with vitamins and minerals, aimed at summer refreshment. Nutri+ blends Rasna's classic fruit flavors with added nutrition such as zinc, positioning it against non-nutritional competitors in India's concentrate market.

- October 2025: MONIN launched an Indian Rasa Range for Diwali 2025, a curated portfolio of Indian‑inspired flavors designed to help cafes, bars, hotels, and home creators build festive drinks and desserts around quintessential Indian tastes.

- March 2025: Luxmi Tea Estates launched a premium line of non-alcoholic, tea-based concentrates, Zero Proof, to meet the growing demand for healthier cold tea beverages in India.

- May 2024: Nescafé introduced its premium Espresso Concentrate, targeting cold coffee trends with customizable iced lattes, Americanos, and flavored mixes, available in bottles or pods. Expansions include mocha and decaf variants in the U.K., plus Sweet Vanilla and Espresso Black flavors launched in Australia and China.

- October 2023: iTi Tropicals launched acerola puree and concentrate, derived from the acerola fruit, also known as Barbados cherry or West Indian cherry, which is renowned for its exceptionally high natural vitamin C content. Suitable for jams, jellies, health shots, smoothies, juice blends, gummies, fruit snacks, sorbets, sauces, marinades, and dressings.

REPORT COVERAGE

The global soft drink concentrates market industry report analyzes the market in depth and highlights crucial aspects such as global market overview, trends, market dynamics, marketing strategies, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.31% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Form

|

|

|

By Flavor

|

|

|

By End-Use

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 26.39 billion in 2025 and is anticipated to reach USD 45.53 billion by 2034.

At a CAGR of 6.31%, the global market will exhibit steady growth over the forecast period.

By form, the liquid segment led the market in 2025.

North America held the largest market share in 2025.

Innovation in flavor systems and product formulation is the crucial factor driving the global market.

Coca-Cola Company, PepsiCo Inc., Kerry Group plc, Döhler Group, and ADM are the leading players in the market.

Shift toward low-sugar, clean-label, and functional beverage concentrates is the key market trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us