Solar Encapsulation Market Size, Share & Industry Analysis, By Material Type (Ethylene Vinyl Acetate {EVA}, Polyolefin Elastomer {POE}, and Others), By Application (Crystalline Silicon PV and Thin Film PV), By End User (Utility-Scale Power Plants, Commercial & Industrial, and Residential), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

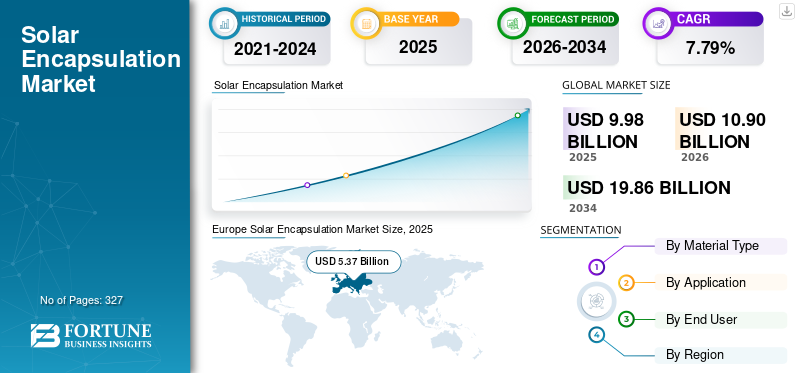

The global solar encapsulation market size was valued at USD 9.98 billion in 2025. It is projected to grow from USD 10.90 billion in 2026 to USD 19.86 billion by 2034, exhibiting a CAGR of 7.79% during the forecast period. Europe dominated the global solar encapsulation market with a market share of 53.81% in 2025.

Solar encapsulation refers to the use of specialized polymer materials to protect and electrically insulate Solar Photovoltaic (PV) cells within a solar module. These materials are laminated above and below the solar cells to shield them from moisture, dust, UV radiation, and mechanical stress. Common encapsulants include Ethylene Vinyl Acetate (EVA), Polyolefin Elastomer (POE), and other specialty polymers. Solar encapsulation plays a critical role in ensuring the durability, safety, and long-term performance of solar modules. The quality of encapsulation directly impacts module efficiency, reliability, and operating lifetime.

Hangzhou First PV Material Co., Ltd. is widely regarded as the global market leader in solar encapsulation materials. The company plays a pivotal role by supplying high-volume EVA and POE encapsulant films to the world’s largest solar module manufacturers, particularly in China, Europe, and emerging markets. The company has been a technology leader in POE and advanced co-extruded encapsulants, which are increasingly used in high-efficiency, bifacial, TOPCon, and HJT solar modules. Its large-scale manufacturing capacity enables cost leadership, while continuous R&D helps improve durability, PID resistance, and moisture protection of PV modules. By aligning closely with leading module OEMs, Hangzhou First has a significant influence on material standards, adoption trends, and cost structures across the global solar encapsulation industry.

Download Free sample to learn more about this report.

SOLAR ENCAPSULATION MARKET Key Takeaways

- 2025 Market Size: USD 9.98 billion

- 2026 Market Size: USD 10.90 billion

- 2034 Forecast Market Size: USD 19.86 billion

- CAGR: 7.79% from 2026–2034

- Europe dominated the global solar encapsulation market with a market share of 53.81% in 2025.

- Ethylene Vinyl Acetate (EVA) segment commands the largest revenue share of 55.35% in 2025.

- Crystalline silicon PV overwhelmingly dominates the market, accounting for the 87.47% encapsulant demand.

Asia Pacific

Asia Pacific is the dominating region in the market, valued at USD 5.37 billion in 2025, driven by growing demand for renewable energy and the presence of huge PV module manufacturing & installations.

North America

North America is expected to reach USD 2.01 billion in 2026, driven by expanding solar deployment and growing domestic PV manufacturing activities.

Europe

Europe is projected to attain USD 1.65 billion in 2026, supported by strong policy initiatives, local PV production, and demand for high-performance solar modules.

U.S.

The market is anticipated to reach USD 1.77 billion in 2026, fueled by federal incentives, new solar manufacturing facilities, and continued growth in solar installations.

Japan

The market is expected to reach USD 0.93 billion in 2026, supported by ongoing adoption of advanced solar technologies and investments in clean energy infrastructure.

Read More

SOLAR ENCAPSULATION MARKET TRENDS

Advancement in High-throughput Encapsulation Materials to Drive Market Growth

An emerging trend in the solar encapsulation industry is the development and adoption of thinner and lightweight encapsulant films designed for high-throughput module manufacturing. As solar module producers focus on reducing material consumption and improving factory productivity, encapsulant suppliers are engineering films that maintain mechanical strength, optical performance, and durability while using less material per module. Thinner encapsulants help lower overall module weight, which is particularly important for large-format modules, rooftop installations, and transportation efficiency. At the same time, these materials are optimized for faster lamination cycles, supporting higher production line speeds and lower per-unit manufacturing costs. This trend aligns with the broader industry objective of reducing Levelized Cost of Electricity (LCOE) and improving supply-chain efficiency, while still meeting long-term reliability and warranty requirements for modern PV systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Global Solar PV Installations to Drive Market Growth

Solar power has become one of the fastest-growing energy technologies worldwide, driven by declining module costs, supportive government policies aimed at reducing carbon emissions, and corporate commitments to decarbonization. Annual global solar installations have risen from well below 150 GW a few years ago to several hundred gigawatts annually in the mid-2020s, with large-scale deployment across the Asia Pacific, North America, and Europe. Every solar module manufactured, regardless of technology or geography, requires encapsulation layers to protect cells from moisture ingress, UV radiation, mechanical stress, and electrical degradation over a 25–30-year lifespan. For example, China’s large-scale solar manufacturing expansion alone consumes millions of square meters of encapsulant films annually. As countries accelerate renewable capacity additions to meet net-zero targets, rising module production volumes directly and proportionally increase demand for encapsulation materials, making installation growth a powerful structural driver for solar encapsulation market growth.

Technological Evolution Toward High-Efficiency and Advanced Solar Modules to Propel Market Growth

The industry is rapidly transitioning from conventional multicrystalline modules to advanced technologies such as mono-PERC, TOPCon, Heterojunction (HJT), and bifacial modules, all of which impose stricter performance requirements on encapsulant materials. Bifacial modules, for instance, require encapsulants with superior optical transparency and long-term resistance to moisture and potential-induced degradation, accelerating the shift from traditional EVA to higher-performance POE-based encapsulants. Similarly, larger wafer sizes and higher operating temperatures increase stress on lamination materials, raising the need for more durable encapsulation solutions. Leading module manufacturers are increasingly specifying POE or co-extruded encapsulants for their premium product lines, even at higher cost, to reduce the risk of field failure. This technological upgrading increases the value per module spent on encapsulation and drives faster growth in advanced materials compared with overall module volumes.

MARKET RESTRAINTS

Ensuring Long-Term Performance Amid Rapidly Evolving Module Technologies to Constrain Market Growth

A major restraint facing the solar encapsulation industry is the need to ensure long-term material performance while solar module technologies continue to evolve at a rapid pace. New cell architectures, such as TOPCon, heterojunction, and bifacial designs, operate under higher temperatures, electrical loads, and increased moisture sensitivity, placing greater demands on encapsulant performance. However, these technologies are commercialized much faster than the time required to generate long-term field reliability data. Encapsulation manufacturers must rely on accelerated aging tests and predictive modeling, which increases technical uncertainty and development costs. At the same time, frequent changes in cell design, module size, and lamination processes require continuous product adaptation. Balancing innovation speed with reliability assurance remains a complex and resource-intensive challenge for the industry.

MARKET OPPORTUNITIES

Growth of Domestic Solar Manufacturing and Localization Initiatives to Offer Lucrative Market Opportunities

A key opportunity for the solar encapsulation market lies in the rapid expansion of domestic solar module manufacturing outside China, due to growing emphasis on energy security concerns and government-led localization programs. Policies such as manufacturing-linked incentives, local content requirements, and tax credits in regions, including North America, India, and parts of Europe, are encouraging the establishment of new PV module factories. Each new manufacturing line creates recurring demand for encapsulation films, often with preferences for locally sourced materials to comply with policy rules and reduce supply-chain risk. This opens up opportunities for encapsulant producers to establish regional manufacturing, form strategic partnerships with module OEMs, and supply customized formulations tailored to local climate conditions. As manufacturing footprints diversify geographically, encapsulation suppliers that can scale quickly and meet regional quality standards are well positioned to capture incremental market share.

MARKET CHALLENGES

Cost Pressure Driven by Solar Module Price Volatility to Hinder Market Growth

A significant challenge for the solar encapsulation market is the intense cost pressure arising from fluctuations in solar module prices and manufacturing margins. The solar industry is highly competitive, and module prices frequently decline due to oversupply, technological transitions, or fluctuations in raw material prices. During such periods, module manufacturers prioritize aggressive cost reductions across the bill of materials, including encapsulation films, despite their critical role in module reliability. Even small reductions in encapsulant pricing can have a material impact on supplier margins, as encapsulation is already a cost-optimized product. In price-sensitive utility-scale projects, manufacturers may delay the adoption of higher-performance encapsulants and opt for standard materials to maintain competitiveness. This dynamic limits value growth for encapsulation suppliers and makes revenue highly sensitive to short-term market cycles, even when long-term solar deployment fundamentals remain strong.

IMPACT OF TARIFF ON THE MARKET

Tariffs on solar modules, cells, and related components can have a notable indirect impact on the market. Import duties and trade restrictions often alter global manufacturing flows, prompting module producers to relocate or localize production to avoid tariff exposure. While this can create new demand for encapsulation materials in emerging manufacturing regions, it may also lead to short-term disruptions and uneven capacity utilization. Tariffs can increase overall module production costs, intensifying pressure on encapsulation suppliers to reduce prices or localize sourcing. At the same time, localized manufacturing incentives linked to tariffs may encourage regional encapsulant production, reshaping supply chains rather than reducing long-term demand.

SEGMENTATION ANALYSIS

By Material Type

Lower Cost of Ethylene Vinyl Acetate to Play a Key Role in Leading Market Share

By material type, the market is segmented into Ethylene Vinyl Acetate (EVA), Polyolefin Elastomer (POE), and others.

Ethylene Vinyl Acetate (EVA) segment commands the largest revenue share of 55.35% in 2025, driven by its long track record, cost-effectiveness, and well-established processing characteristics. EVA continues to account for the largest share of encapsulation consumption, particularly in conventional monofacial crystalline silicon modules and price-sensitive markets. Its strong adhesion, good optical transparency, and compatibility with high-volume lamination processes make it the preferred choice for many manufacturers. However, EVA’s market share is gradually declining as advanced module designs expose its limitations in moisture resistance and potential-induced degradation under demanding operating conditions.

Polyolefin Elastomer is the fastest-growing segment with a CAGR of 8.47% in the solar encapsulation market, driven by the rapid adoption of bifacial and high-efficiency module technologies. POE offers superior resistance to moisture ingress, lower degradation risk, and better electrical insulation compared to EVA, making it increasingly preferred for premium and utility-scale projects. Although POE currently holds a smaller share than EVA, its share is expanding steadily as module manufacturers prioritize long-term durability and performance over upfront material cost.

By Application

Continued Shift Toward High-Efficiency Crystalline Technologies Boosted the Crystalline Silicon PV Segment's Growth

Based on application, the market is divided into Crystalline Silicon PV, and Thin Film PV.

Crystalline silicon PV overwhelmingly dominates the market, accounting for the 87.47% encapsulant demand. This is due to mono- and multicrystalline silicon technologies that represent the primary choice for utility-scale, commercial, and residential solar installations worldwide. Crystalline silicon modules require encapsulation on both sides of the solar cells, typically using EVA or POE films, which directly drives large-volume consumption of encapsulation materials. The continued shift toward high-efficiency crystalline technologies such as mono-PERC, TOPCon, heterojunction, and bifacial modules further reinforces this dominance, as these designs often require higher-performance and, in some cases, higher-value encapsulants. As a result, crystalline silicon PV accounts for the largest share of both volume and value in the solar encapsulation market.

Thin Film PV is the second leading segment in the market, expected to grow at a CAGR of 9.13% during the forecast period. Technologies such as CdTe, CIGS, and amorphous silicon employ different module architectures, which often require specialized encapsulation solutions tailored to their respective manufacturing processes. While thin film solar technologies may use less encapsulant per watt compared to crystalline silicon, they still rely on encapsulation for moisture protection, mechanical stability, and long-term durability. The market share of thin film encapsulation remains limited due to the comparatively low deployment of thin film PV globally. However, it maintains relevance in niche applications, such as large-scale utility projects and specific climatic conditions.

By End User

To know how our report can help streamline your business, Speak to Analyst

Significant Deployment in Large Scale Solar Projects to Lead Utility-Scale Power Plants Market Growth

Based on end user, the market is broadly segmented into utility-scale power plants, commercial & industrial, and residential.

Utility-scale solar power plants account for the largest share of the solar encapsulation market at 75.57%. This growth is driven by the sheer scale of module procurement and deployment in large scale solar ground-mounted projects. These installations prioritize long-term reliability, high power output, and durability over extended operating lifetimes, often exceeding 30 years. As a result, utility-scale projects are increasingly specifying advanced encapsulation materials, particularly for bifacial and glass–glass modules, to mitigate degradation risks and enhance energy yield. The dominance of this segment is further reinforced by large solar parks and government-led renewable programs in the Asia Pacific, the Middle East, and the Americas, making utility-scale applications the primary driver of encapsulation volume and value.

The commercial & industrial segment is set to grow at a CAGR of 8.85%. It is the fastest growing segment among the end users. Rooftop and on-site installations for factories, warehouses, offices, and data centers demand reliable modules with strong performance under diverse operating conditions. While cost sensitivity remains important, C&I customers increasingly value module longevity and warranty assurance, supporting the adoption of higher-quality encapsulation materials. Growth in this segment is supported by corporate sustainability targets, rising electricity costs, and supportive net-metering and incentive policies across developed and emerging markets.

SOLAR ENCAPSULATION MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Europe Solar Encapsulation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the dominating region in the market, valued at USD 5.37 billion in 2025. The region holds the largest share of the market, driven by growing demand for renewable energy and the presence of huge PV module manufacturing & installations. China accounts for more than 40% of the global installed solar capacity and houses the bulk of large-scale module fabrication facilities, which directly consume encapsulation materials. India’s ambitious renewable targets (e.g., 500 GW of installed solar by 2030) further strengthen regional demand. Advanced module formats such as bifacial and high-efficiency cells, widely adopted in the region, result in higher encapsulant usage per module, reinforcing Asia Pacific’s leadership. Leading countries such as China, Japan, and India markets are expected to reach USD 2.67 billion, USD 0.93 billion, and USD 0.75 billion, respectively, in 2026.

North America

North America also holds a considerable position in the market, set to reach USD 2.01 billion in 2026, primarily driven by the U.S. The U.S. has become one of the world’s top three annual solar installation markets, with tens of gigawatts of new capacity added each year. Federal incentives and manufacturing incentives aimed at reducing carbon emissions have spurred several new PV assembly facilities, increasing demand for domestically sourced encapsulation films. The U.S. market is set to reach a valuation of USD 1.77 billion in 2026.

Europe

Europe represents a significant and quality‐focused share, with a market value of USD 1.65 billion in 2026. This growth is driven by strong policy support for the deployment of PV and domestic manufacturing. For example, Germany added over 10 GW of solar capacity in 2024, underscoring continued expansion. European preferences for long-lasting, higher-performance modules elevate demand for advanced encapsulation materials. Simultaneously, EU efforts to strengthen local PV supply chains contribute to localized encapsulant consumption. Leading countries such as the U.K., Germany, and France are expected to have market values of USD 0.07 billion, USD 0.54 billion, and USD 0.16 billion respectively, by 2026.

Latin America

Latin America accounts for a modest solar encapsulation market share, largely driven by the expansion of utility solar projects. Chile and Brazil alone accounted for over 9 GW of new solar capacity in recent years, driven by competitive power auctions and favorable solar resources. While much of the region’s module supply is imported, the growing demand for C&I and utility deployments is steadily increasing encapsulant demand.

Middle East & Africa

The Middle East & Africa currently represent the smallest share of the market, and are emerging as future growth regions. For instance, the UAE’s Mohammed bin Rashid Al Maktoum Solar Park aims to reach 5 GW by 2030, demonstrating a significant commitment to large-scale solar energy. Harsh desert conditions and a focus on reliability increase the appeal of durable encapsulation solutions, supporting premium material adoption even as overall deployment scales up from a lower base. The region is expected to hold a market value of USD 0.7 billion by 2026, with the GCC countries alone accounting for approximately USD 0.35 billion by 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players’ Increasing Investment in Material Innovation to Lead the Market Share

Hangzhou First plays a leading global role in the solar encapsulation industry. The company has built one of the world’s largest production capacities for EVA and POE encapsulation films, allowing it to support high-volume module manufacturing while maintaining cost competitiveness. Beyond scale, Hangzhou First invested heavily in material innovation, particularly in POE and co-extruded encapsulants designed for bifacial, TOPCon, and heterojunction modules that demand superior moisture resistance and long-term reliability. Its close technical collaboration with leading solar module manufacturers enables rapid customization of encapsulant formulations to match evolving cell designs and lamination processes. By expanding production bases both within China and internationally, Hangzhou First also strengthened supply-chain resilience and helped accelerate the adoption of advanced encapsulation standards across the global solar industry.

List of the Key Solar Encapsulation Companies Profiled

- Hangzhou First PV Material Co., Ltd. (China)

- Sinopont (China)

- Hanwha Solutions / Hanwha Chemical (South Korea)

- 3M Company (United States)

- STR Holdings, Inc. (United States)

- HIUV New Materials (China)

- Betterial New Materials (China)

- Cybrid Technologies (China)

- Mitsui Chemicals, Inc. (Japan)

- Sveck (Changzhou Sveck Technology Co., Ltd.) (China)

- RenewSys India Pvt. Ltd. (India)

- DuPont (United States)

- Celanese (United States)

- Vishakha Renewables (India)

- Crown Advanced Material Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, RenewSys entered into a supply agreement with ZNShine Solarworld, a wholly owned subsidiary of Solarworld Energy Solutions, to provide solar encapsulation materials. The contract covers 400 MW of encapsulants scheduled for delivery between November 2025 and February 2026. This agreement reflects the increasing demand for advanced, high-efficiency encapsulation solutions as solar module manufacturers continue to shift toward next-generation cell technologies.

- In July 2025, UbiQD signed an exclusive, multi-year supply agreement with First Solar to provide its proprietary quantum dot technology for use in thin-film bifacial solar modules. The agreement follows a joint development program initiated in 2023 and supports expanded R&D collaboration between the two companies. The partnership is expected to accelerate early adoption of quantum dots in thin-film PV, with UbiQD’s production capacity potentially scaling beyond 100 metric tons per year. The collaboration aligns with broader U.S. efforts to expand domestic power generation capacity to meet rising demand from data centers, AI, and manufacturing.

- In May 2025, Reliance Group entered into a strategic partnership with Chinese equipment supplier GWELL to strengthen its presence in solar encapsulation materials. The collaboration involves the supply of 20 EVA/POE/EPE encapsulation film production lines with a total capacity of 20 GW, aimed at supporting India’s fast-growing photovoltaic market. As part of the rollout, four production lines have already been dispatched and are being installed and commissioned at Reliance’s facilities, marking an important step toward large-scale domestic production of solar encapsulation films.

- In June 2024, At Intersolar 2024, LONGi introduced its Hi-MO X6 Artist Ultra Black solar module, featuring a uniform, deep-black appearance across all sides. This effect is achieved through a specially engineered glass surface and a refined cell selection process using automated optical inspection during production. The dual-glass module incorporates a thicker front glass along with POE encapsulation film, enhancing overall durability, safety, and long-term reliability. With bifacial capability, the module is designed for diverse rooftop applications, including carports and winter garden installations.

- In August 2023, Verde Technologies partnered with Northern Illinois University and the U.S. National Renewable Energy Laboratory (NREL) to advance the commercialization of its perovskite-based thin-film solar cells. Under the collaboration, Verde and NIU will gain exclusive access to a portfolio of NREL’s perovskite solar technologies through a dedicated agreement. NREL will play a central role in bringing jointly owned technologies to the market, supporting the transition of perovskite innovations from research to commercial deployment.

REPORT COVERAGE

The report delivers a detailed insight into the market and focuses on key aspects, such as leading companies. Besides, it offers insights into the market trends and technologies, and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors and challenges that have contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.79% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material Type · Ethylene Vinyl Acetate (EVA) · Polyolefin Elastomer (POE) · Others |

|

By Application · Crystalline Silicon PV · Thin Film PV |

|

|

By End User · Utility-Scale Power Plants · Commercial & Industrial · Residential |

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 9.98 billion in 2025.

The market is likely to record a CAGR of 7.79% over the forecast period (2026-2034).

By end user, the utility-scale power plants segment leads the market.

The Asia Pacific market size was valued at USD 5.37 billion in 2025.

Rapid expansion of global solar PV installations is the key factor driving the market.

Some of the key players in the market are Hangzhou First PV Material, Sinopont, Hanwha Solutions, 3M Company, STR Holdings, Inc., and others.

The global market size is expected to reach a valuation of USD 19.86 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 327

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us