Solid-State Battery Materials Market Size, Share & Industry Analysis, By Type (Cathode Active Materials & Conductive Additives, Solid Electrolytes, Anode Materials, and Others), By End-use (Electric Vehicles, Consumer Electronics & Wearables, Stationary Energy Storage, Aerospace & Defense, and Others), and Regional Forecast, 2026-2034

Solid-State Battery Materials Market Size and Future Outlook

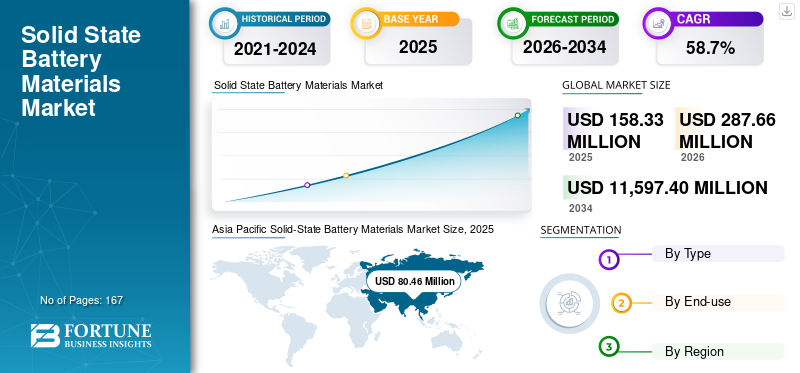

The global solid-state battery materials market size was valued at USD 158.33 million in 2025. The market is projected to grow from USD 287.66 million in 2026 to USD 11,597.40 million by 2034, exhibiting a CAGR of 58.7% during the forecast period. Asia Pacific dominated the solid-state battery materials market with a market share of 50.81% in 2025.

Solid-state battery materials are specialized inputs used in developing and manufacturing next-generation solid-state lithium batteries, including solid electrolytes, cathode active materials & conductive additives, anode materials, and other supporting interface and structural materials. These materials are designed to replace or reduce reliance on flammable liquid electrolytes used in conventional cells. They are increasingly being evaluated for applications that require improved safety, high performance, and longer cycle life. Compared to traditional lithium-ion batteries, solid-state battery systems offer the potential for enhanced thermal stability, higher energy density, and lower safety risk, making them attractive for electric mobility, compact electronics, aerospace systems, and advanced energy storage solutions.

A significant driver within the market is the global shift toward electrification and the development of safer battery technologies. The International Energy Agency has observed that worldwide electric vehicle sales surpassed 17 million units in 2024, accounting for over 20% of total car sales. This trend underscores the sustained long-term demand for advanced battery materials and innovative chemistries. Concurrently, industry activity related to commercialization continues to accelerate, with entities such as Mercedes-Benz and Factorial initiating solid-state road testing in 2025, Toyota advancing all-solid-state battery initiatives under METI-approved programs, and Idemitsu increasing solid-electrolyte production capacity. These advancements collectively enhance the positive outlook for the global market.

The market is still in an early phase of commercialization. Yet, it is being influenced by several prominent participants, including BASF SE, Ampcera, Solid Power, Idemitsu Kosan, NEI Corporation, ProLogium, and Sumitomo Metal Mining Co., Ltd. Plans for scaling up, investments in pilot lines, technology validation initiatives, and strategic alliances are underpinning the market positioning of these organizations and assisting in shaping the future trajectory of solid-state battery materials commercialization.

Download Free sample to learn more about this report.

Solid State Battery Materials Market Key Takeaways

- 2025 Market Size: USD 158.33 million

- 2026 Market Size: USD 287.66 million

- 2034 Forecast Market Size: USD 11,597.40 million

- CAGR: 58.7% from 2026–2034

- Asia Pacific dominated the market with a 50.81% share in 2025.

- The Cathode Active Materials & Conductive Additives segment held the largest market share in 2025.

- The Electric Vehicles segment accounted for the largest market share in 2025.

Asia Pacific

Asia Pacific reached USD 80.46 million in 2025, maintaining its leadership with strong EV manufacturing and battery R&D.

North America

The region is projected to emerge as the second-largest market, supported by strong battery innovation and advanced supply chain development.

Europe

Europe is projected to reach USD 69.51 million by 2026 and grow at a CAGR of 57.8%.

U.S.

U.S. market is projected to reach USD 47.82 million by 2026.

Japan

Japan market is projected to reach USD 26.46 million by 2026.

Read More

SOLID-STATE BATTERY MATERIALS MARKET TRENDS

Commercialization is Shifting from Cell-Level Innovation toward Scalable Materials and Manufacturing Readiness

A significant trend within the market is the transition from laboratory-scale chemistry validation to industrial-scale material and process readiness. Previously, industry focus was primarily on demonstrating the feasibility of solid-state battery architectures. Nonetheless, the market is increasingly focused on scalable production of solid electrolytes, separator technologies, interface-engineered cathodes, and lithium-compatible anode systems capable of supporting pilot and commercial deployment. This shift is of considerable importance, as the commercial success of solid-state batteries relies not only on cell design but also on the ability to produce upstream materials consistently, safely, and cost-effectively.

This trend is increasingly evident throughout the entire value chain. Idemitsu has advanced with its plans to expand production capacity for lithium sulfide and solid electrolytes. In contrast, QuantumScape has reported progress in its Cobra separator process and has consequently announced the shipment of B1 samples scheduled for 2025. Additionally, Solid Power has continued to refine its pilot line for continuous electrolyte production, highlighting the industry’s broader shift toward manufacturable materials rather than solely conceptual innovations. These developments indicate that the industry is transitioning into a phase focused on implementation, where supply chains, processing methodologies, and qualification processes are becoming as critical as electrochemical performance.

A second noteworthy trend is the expansion of the application narrative. While the primary commercial driver remains the increased demand for electric vehicles, the market is also attracting increased interest from sectors such as consumer electronics, stationary energy storage, and aerospace and defense. This development highlights the growing recognition that solid-state systems can support a wider array of energy storage solutions, particularly in scenarios where safety, compactness, and high performance are prioritized over immediate cost parity with traditional batteries. As commercialization progresses, this broader application spectrum is expected to bolster long-term market resilience and diversify demand beyond a single end-use industry.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Electric Vehicles and Safer High-Energy Batteries is Accelerating Market Growth

The primary catalyst for the solid-state battery materials market growth is the global transition toward vehicle electrification and the adoption of safer battery technologies. The electric vehicle (EV) industry continues to expand rapidly, prompting automakers to increasingly evaluate solid-state systems as a promising platform to achieve higher energy density, lower fire risk, and greater durability. As solid-state battery designs can offer superior safety and improved electrochemical performance compared with conventional lithium-ion batteries, the materials used in these systems are increasingly attracting the attention of original equipment manufacturers (OEMs), battery developers, and upstream material suppliers.

This demand outlook is supported by broader momentum in the electric vehicle (EV) market. The International Energy Agency (IEA) reported that global EV sales exceeded 17 million units in 2024 and noted continued strength into 2025, which is encouraging investment in battery localization, next-generation chemistries, and supporting supply chains. In parallel, commercialization milestones, including Mercedes-Benz and Factorial’s solid-state test vehicle, Toyota’s Ministry of Economy, Trade and Industry (METI)-backed all-solid-state battery plans, and Samsung SDI’s roadmap toward mass production of all-solid-state batteries by 2027, are reinforcing confidence in future material demand. Consequently, the market is benefiting from both rising end-use expectations and increased material development activity.

The market is increasingly supported by demand for high-performance battery systems across sectors beyond mainstream mobility. Premium electronics, defense platforms, and specialized equipment consistently require batteries that combine compactness, thermal stability, and extended cycle life. This trend is driving additional demand for advanced solid electrolytes, cathode systems, and anode-compatible materials, even before the widespread adoption of batteries in large-scale automotive applications.

MARKET RESTRAINTS

High Material Costs and Delayed Commercial Scale-Up are Limiting Near-Term Volume Expansion

A notable constraint for the market is the gradual progression of large-scale commercialization rather than rapid development. While the technological prospects are optimistic, many solid-state battery initiatives are still in pilot, sampling, testing, or validation stages. This suggests that the current direct consumption of solid-state battery materials remains relatively limited when compared to traditional battery materials markets. Practically speaking, the industry has not yet achieved widespread mass deployment, especially in the automotive sector, where qualification processes are lengthy, and performance consistency standards are highly demanding.

Another significant constraint is the complexity and expense of materials processing. Solid electrolytes, lithium-metal-compatible interlayers, and interface-engineered cathodes often require specialized synthesis methods, controlled environments, and more expensive precursors. Sulfide-based materials, in particular, are highly sensitive to moisture, whereas oxide and polymer systems present their own interfacial and processing challenges. These technical limitations raise production costs and may hinder broader adoption in price-sensitive applications.

The market's economic landscape remains predominantly influenced by pilot-scale manufacturing rather than by achieving full industrial efficiencies. Until production yields and supply chain development improve, many solid-state battery materials are expected to retain premium pricing. This circumstance restricts adoption in lower-margin applications and perpetuates market concentration within segments where safety, size, and performance considerations justify elevated material costs.

MARKET OPPORTUNITIES

Broader Adoption across Consumer Electronics, Stationary Energy Storage, and Strategic Supply Chains Creates Long-Term Upside

A significant opportunity for the market lies in expanding beyond passenger electric vehicles. Although electric vehicles are anticipated to remain the predominant long-term demand segment, there is increasing potential in consumer electronics and wearables, stationary energy storage, and the aerospace and defense sectors. In these areas, considerations such as battery safety, operational stability, and energy density are likely to command higher value premiums, thereby making solid-state material systems commercially attractive even before reaching full automotive cost competitiveness.

Another significant opportunity lies in developing regional and localized supply chains. Governments and manufacturers across Asia Pacific, North America, and Europe are increasingly prioritizing the resilience of the battery ecosystem and the advancement of next-generation energy technologies. This trend creates opportunities for material suppliers capable of providing scalable electrolyte production, interface optimization materials, and sophisticated cathode or anode systems. Idemitsu’s decision to build a lithium sulfide facility and the Ministry of Economy, Trade and Industry (METI)-supported plans for solid electrolyte development exemplify how upstream material investments are becoming a strategic element in the industrialization of all-solid-state batteries.

The market further exhibits considerable potential for expansion through targeted research and development efforts. Suppliers capable of overcoming challenges related to interfacial resistance, manufacturability, moisture sensitivity, and cycling stability are positioned to achieve superior market standing. As the industry progresses, demand is expected to shift from generic next-generation battery materials to more specialized, application-specific material platforms designed for electric vehicles (EVs), compact electronic devices, and systems requiring high reliability.

MARKET CHALLENGES

Interface Stability, Manufacturing Yield, and Supply-Chain Readiness Continue to Create Execution Risk

One of the primary challenges in the market is translating promising laboratory and pilot results into consistent commercial output. Solid-state batteries rely heavily on material interfaces, and even minor inconsistencies in electrolyte quality, cathode contact, densification, or anode compatibility can degrade performance. This makes scale-up particularly demanding for material suppliers, as success depends on chemical innovation and manufacturing reliability and repeatability.

An additional challenge involves enhancing the broader supply-chain readiness. The industry continues to require increased availability of precursor materials, improved pilot-to-commercial production infrastructure, and more standardized qualification pathways. Although numerous market participants are making rapid progress, the overall ecosystem remains less mature compared to traditional lithium-ion batteries. This situation can result in bottlenecks in scaling up, customer qualification, and commercialization timelines, particularly for automotive-grade projects.

Ultimately, the timing of commercialization remains a challenge. While the market exhibits robust momentum, actual offtake remains contingent on the timely achievement of announced technological milestones. Delays in pilot-line commissioning, cell qualification, or vehicle integration may defer upstream materials demand. Consequently, organizations operating in this market must reconcile long-term investment strategies with meticulous execution and diversified application exposure.

Segmentation Analysis

By Type

Cathode Active Materials & Conductive Additives Segment Led Market as It Offers Enhanced Power

Based on type, the market is segmented into cathode active materials & conductive additives, solid electrolytes, anode materials, and others.

The cathode active materials & conductive additives segment accounted for the largest solid-state battery materials market share in 2025, driven by the need to improve electrochemical performance, interface stability, and conductivity in solid-state cell architectures. In solid-state systems, cathode engineering is particularly important due to differences in material compatibility and ionic transport behavior compared to traditional liquid-electrolyte cells. Accordingly, there is an increasing demand for sophisticated cathode formulations capable of supporting dense architectures, ensuring stable cycling, and delivering enhanced power. Furthermore, this segment is projected to exhibit a CAGR of 64.5% throughout the study period.

Solid electrolytes are expected to grow at a CAGR of 53.2% over the forecast period. These materials replace traditional liquid electrolytes and are integral to enhancing safety, thermal stability, and long-term electrochemical performance. The segment encompasses sulfide-, oxide, and polymer-based electrolyte systems, each exhibiting distinct trade-offs in conductivity, stability, and manufacturability. Industry demand is supported by ongoing efforts to commercialize all-solid-state batteries, particularly in electric vehicle platforms and high-value battery applications. Moreover, Idemitsu’s 2025 announcements regarding lithium sulfide and the expansion of solid-electrolyte development capacity further underscore the strategic significance of this segment.

By End-use

To know how our report can help streamline your business, Speak to Analyst

Growing Focus on Advancing Battery Safety Boosted Electric Vehicles Segment Growth

In terms of end-use, the market is categorized into electric vehicles, consumer electronics & wearables, stationary energy storage, aerospace & defense, and others.

Electric vehicles held the largest market share and are expected to be the fastest-growing segment during the forecast period. This expansion is primarily driven by escalating demand for electric vehicles, a focus on advancing battery safety, and the need for increased energy density and prolonged cycle life. Solid-state material systems are increasingly gaining prominence in the development of EV batteries due to their enhanced safety attributes and superior thermal stability relative to traditional lithium-ion batteries. As automotive manufacturers and battery developers continue to invest in solid-state lithium platforms for future mobility solutions, this segment is expected to remain the primary catalyst for market growth. The 2025 road testing by Mercedes-Benz in collaboration with Factorial, alongside Toyota's ongoing development of all-solid-state batteries, corroborates this optimistic projection. Moreover, this segment is projected to grow at a 64.9% compound annual growth rate over the study period.

The consumer electronics & wearables segment presents a significant opportunity, driven by demand for compact, lightweight, and high-performance batteries in devices such as smartphones, smartwatches, earbuds, laptops, and other portable electronics. The evaluation of solid-state battery materials for these applications has increased, owing to their potential to enable slimmer designs, enhanced safety, and improved energy density. As demand for advanced portable devices continues to grow, particularly across the Asia Pacific region, this segment is projected to grow throughout the forecast period. Furthermore, robust electronics manufacturing ecosystems and evolving supply chains continue to foster long-term adoption of materials within this category. Furthermore, this segment is projected to grow at a 48.0% compound annual growth rate over the study period.

The stationary energy storage segment is expected to sustain long-term growth as the market for solid-state batteries expands beyond mobility applications. Utilities, grid operators, and commercial energy consumers are increasingly seeking safer and more durable renewable energy storage and grid-support systems. Although commercialization in this segment is still in its early stages compared to electric vehicles, the need for stable cycling, operational safety, and extended asset lifespan makes it promising.

Solid-State Battery Materials Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Solid-State Battery Materials Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the largest market share at USD 42.17 million and maintained its leadership in 2025, at USD 80.46 million. This region benefits from robust battery manufacturing ecosystems, comprehensive electronics and automotive supply chains, and numerous prominent developers of solid-state technologies and materials. China, Japan, and South Korea are integral to electric vehicle (EV) production, advanced battery research and development, and the development of next-generation materials, thereby establishing the region as both the primary source of demand and innovation for solid-state battery materials.

China Solid-State Battery Materials Market

By 2026, the Chinese market is projected to attain a valuation of USD 74.15 million. China is expected to remain the leading country-level demand center in Asia Pacific, driven by its substantial capabilities in electric vehicle manufacturing, battery production, and localized supply chains. The country's leadership in electric vehicle output and the advancement of the battery ecosystem create a favorable environment for the future integration of solid-state materials.

To know how our report can help streamline your business, Speak to Analyst

Japan Solid-State Battery Materials Market

The Japan market in 2026 is estimated to be around USD 26.46 million, accounting for roughly 9.2% of the global revenues.

India Solid-State Battery Materials Market

The India market in 2026 is estimated at around USD 10.05 million, accounting for roughly 3.5% of global revenues.

Europe

Europe is expected to experience substantial market growth in the coming years. Over the forecast period, the region is projected to grow at an annual rate of 57.8%, reaching a market valuation of USD 69.51 million by 2026. The region combines strong momentum in automotive electrification with rising interest in localized battery manufacturing, strategic sourcing of materials, and the qualification of next-generation batteries. Europe’s demand forecast is primarily driven by electric vehicle programs, high-reliability industrial applications, and select aerospace-related battery developments. Furthermore, the region is supported by notable milestones in commercialization. The 2025 road-testing initiative by Mercedes-Benz in partnership with Factorial, along with ProLogium’s 2025 announcement concerning its European mass-production roadmap, exemplify Europe's rise as an important market for the validation and deployment of future solid-state batteries.

U.K. Solid-State Battery Materials Market

The U.K. market in 2026 is estimated at around USD 10.78 million, accounting for roughly 3.7% of global revenues.

Germany Solid-State Battery Materials Market

The German market in 2026 is estimated at around USD 20.07 million, accounting for roughly 7.0% of global revenues.

North America

North America is projected to emerge as the second-largest regional market during the forecast period. The region benefits from a significant early presence of battery innovators, electric vehicle technology developers, and ongoing initiatives to develop advanced battery supply chains. Entities such as QuantumScape and Solid Power are particularly influential in shaping the region’s role in separator technology, sulfide electrolyte development, and the commercialization of solid-state cells.

U.S. Solid-State Battery Materials Market

Given the U.S. dominance in the region, the U.S. market is estimated at around USD 47.82 million in 2026, accounting for roughly 16.6% of global sales.

Latin America and Middle East & Africa

Throughout the forecast period, Latin America and the Middle East & Africa are expected to experience relatively moderate growth within this market. Currently, these regions account for smaller demand bases owing to the concentration of solid-state battery deployment in more established battery manufacturing areas. In Latin America, prospective opportunities are likely to emerge through electric vehicle (EV) adoption, connections to battery raw materials, and specific industrial assembly activities. In the Middle East & Africa, potential growth is more closely linked to energy transition strategies, long-term storage needs, and specialized battery applications for infrastructure. Although both regions are projected to remain smaller than Asia Pacific, Europe, and North America, they continue to contribute to the expanding long-term prospects for solid-state battery materials. The Latin America market is projected to reach USD 8.14 million in 2026.

GCC Solid-State Battery Materials Market

The GCC market in 2026 is estimated at USD 5.35 million, accounting for approximately 1.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Scale-Up Capability, Materials Engineering, and Commercial Validation are Core Differentiators

The market operates within an innovation-driven, competitive framework, prioritizing technological advances, commercial viability, and pilot-scale implementation over extensive incumbent production capacity. Competitive advantage is built on proprietary electrolyte chemistry, manufacturable separator or interface technology, lithium-metal compatibility, and the ability to support customer qualification through reliable material performance.

Given the nascent stage of the market, leadership is presently characterized more by credible commercialization pathways than by volume. Organizations capable of integrating advanced material engineering with scalable manufacturing and robust strategic alliances are anticipated to attain the most prominent positions. Presently, BASF SE, Ampcera, Solid Power, Idemitsu Kosan, NEI Corporation, ProLogium, and Sumitomo Metal Mining Co., Ltd. are among the most prominent entities operating within this domain.

LIST OF KEY SOLID-STATE BATTERY MATERIAL COMPANIES PROFILED

- BASF SE (Germany)

- Ampcera (U.S.)

- Solid Power, Inc. (U.S.)

- Idemitsu Kosan Co., Ltd. (Japan)

- NEI Corporation (U.S.)

- Umicore (Belgium)

- Sumitomo Metal Mining Co., Ltd. (Japan)

- Nichia Corporation (Japan)

- Mitsubishi Chemical Corporation (Japan)

- Tokyo Chemical Industry Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Solid Power announced a joint evaluation agreement with BASF SE and BMW to advance all-solid-state battery technology for a future demonstration vehicle, reinforcing the commercial relevance of its sulfide electrolyte platform.

- October 2025: Sumitomo Metal Mining and Toyota entered a joint development agreement for the mass production of cathode materials for all-solid-state batteries for BEVs. The companies said they had developed a highly durable cathode material suitable for ASSBs.

- April 2025: Idemitsu completed construction work to increase the capacity of its pilot facilities for mass production technology related to solid electrolytes, supporting its scale-up roadmap.

- October 2024: NEI introduced Li₃InCl₆ halide solid electrolyte powder for solid-state battery R&D applications, expanding its SSE materials portfolio.

REPORT COVERAGE

The global solid-state battery materials market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market shares and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 58.7% from 2026 to 2034 |

| Unit | Value (USD Million) Volume (Kiloton) |

| Segmentation | By Type, End-use, and Region |

| By Type |

|

| By End-use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 158.33 million in 2025 and is projected to reach USD 11,597.40 million by 2034.

Recording a CAGR of 58.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The electric vehicles end-use segment led in 2025.

Asia Pacific held the highest market share in 2025.

Rising demand for electric vehicles and safer high-energy batteries is accelerating market growth.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us