Sports Medicine Market Size, Share & Industry Analysis, By Device Type (Surgery Devices, Bone Reconstruction Devices, Body Support Devices, Others), By Application (Knee, Head & Neck, Shoulder, Ankle & Foot, Wrist & Elbow, Others) By End User (Hospitals, Specialty Clinics), and Regional Forecast, 2026-2034

Sports Medicine Market Size

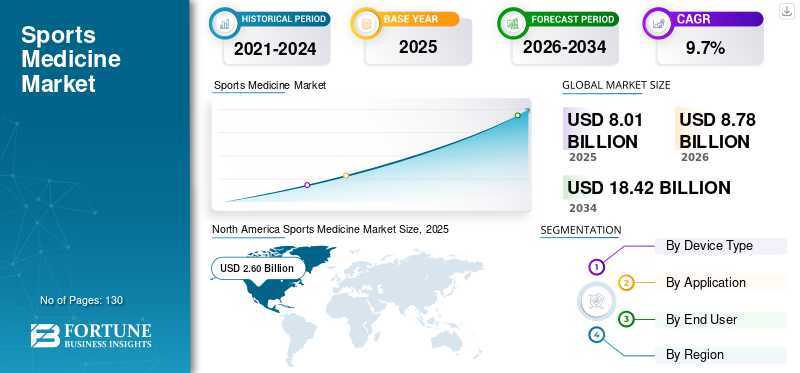

The global sports medicine market size was valued at USD 8.01 billion in 2025. The market is projected to grow from USD 8.78 billion in 2026 to USD 18.42 billion by 2034, exhibiting a CAGR of 9.70% during the forecast period. North America dominated the global market with a share of 41.53% in 2025.

The global sports medicine market gorwth is driven by rising participation in organized sports, fitness programs, and recreational activities. Increasing awareness of injury prevention, performance optimization, and long term musculoskeletal health continues to expand patient volumes across age groups. Technological progress in imaging, minimally invasive surgery, and rehabilitation solutions improves diagnostic accuracy and accelerates recovery. These factors collectively strengthen demand across clinical and nonclinical care settings.

Market expansion is further supported by demographic shifts toward active aging populations and greater emphasis on physical wellness. Professional sports leagues, military organizations, and educational institutions continue to invest in injury management programs. Rising healthcare expenditure and insurance coverage enhance access to advanced treatments, while value based care models encourage efficient recovery pathways.

The sports medicine market size reflects balanced growth across surgical and non surgical segments. Orthopedic procedures, regenerative therapies, and rehabilitation technologies remain central to clinical demand. Hospitals maintain leadership in service delivery, while specialty clinics expand through focused expertise and outpatient efficiency. Digital health integration increasingly supports monitoring, compliance, and outcome measurement.

Regionally, North America leads adoption through strong infrastructure and reimbursement frameworks, while Europe benefits from integrated healthcare systems. Asia Pacific shows the fastest growth driven by population scale and rising healthcare investment. Competitive intensity remains high as manufacturers pursue innovation, partnerships, and geographic expansion to secure long term market positioning.

The industry growth supported by continuous innovation and expanding clinical applications. Stakeholders focusing on evidence based solutions, cost efficiency, and patient outcomes are positioned to capture sustainable value. These dynamics define the strategic foundation for long term growth across the global sports medicine ecosystem. Continued collaboration among manufacturers, clinicians, and policymakers will influence adoption rates, regulatory alignment, and innovation pathways, shaping competitive positioning and long range performance outcomes across global healthcare markets.

Increasing incidence of sports injuries in developed and developing countries is anticipated to drive the growth of the global market during the forecast period of 2019-2026. According to, National Safety Council (NSC) data, exercise and use of exercise equipment in the U.S. resulted in around 526,000 injuries in the year 2017. Rise in athletic career adoption coupled with growing trend towards healthy lifestyle is anticipated to fuel demand for sports medicine. This, in turn will bode well for the sports medicine industry.

Rising prevalence of chronic conditions including cardiovascular diseases and obesity coupled with awareness about healthy lifestyle are some of the major factor escalating participation in athletic activities. According to U.S. Centers for Disease Control (CDC), more than 30 million children and teens in the U.S. participate in organized sports, out of which one third are reported with sporting injuries. Additionally, certain factors that are fuelling the market growth includes consistent innovation of new products in reconstruction and surgery devices, and rising demand for minimally invasive surgeries in developed and developing countries.

Download Free sample to learn more about this report.

Sports Medicine Market Key Takeaways

- 2025 Market Size: USD 8.01 billion

- 2026 Market Size: USD 8.78 billion

- 2034 Forecast Market Size: USD 18.42 billion

- CAGR: 9.70% from 2026–2034

- North America dominated the sports medicine market with a 41.53% share in 2025.

- The Knee segment accounted for a significant market share of 36.8%.

- Surgical devices held a leading revenue share due to their critical role in sports injury treatment and minimally invasive procedures.

North America

North America generated USD 2.60 billion in revenue and continues to benefit from strong sports participation, expanding orthopedic centers, and growing investments in sports medicine technologies.

Europe

Europe maintains steady market growth supported by universal healthcare systems, increasing adoption of advanced surgical procedures, and rising demand for rehabilitation solutions.

Asia Pacific

Asia Pacific is expected to register the fastest growth during the forecast period, driven by increasing awareness, expanding healthcare infrastructure, and rising demand across developing economies.

U.S.

The market is supported by high procedure volumes, rapid adoption of innovative technologies, favorable reimbursement policies, and a strong professional sports ecosystem.

Japan

Market growth is driven by an aging yet active population, advanced healthcare technologies, and increasing focus on preventive and rehabilitative care.

Read More

Key Market Dynamics (Sports Medicine Industry)

Market Drivers

Download Free sample to learn more about this report.

“Rising Prevalence of Athletic Injuries to Fuel the Demand for Sports Medicine”

Sports injuries include spondylolysis, fractures, strains and sprains, stingers, disc injury, and Scheuermann's disease. According to the sports injury statistics, published by STANFORD CHILDREN'S HEALTH, in the United States, about 30 million kids and teenagers participate in various organized athletics . Almost one-third of all injuries incurred in childhood are games-related injuries. Additionally, according to National Health Statistics Reports published by the CDC in 2016, an average of 8.6 million sports and recreation-related injuries were reported in the U.S. Anatomical locations of the injuries reported during sports and recreation activities included the high percentage of injuries in lower extremity followed by upper extremity and head and neck.

- North America witnessed a growth from USD 2.46 Billion in 2017 to USD 2060 Billion in 2018.

According to EU IDB catalog of sports, about 4.5 million people, aged 15 and above, are treated in a hospital for injuries each year. Team ball, a major segment of sporting category in Europe, account for approximately 40.0% of all hospital-treated athletic injuries. Additionally, according to Youth Sports Injury Statistics, 2016, about 40.0% of all sports-related injuries treated in hospitals are for children in the age group of 5-14 years.

Higher adoption of athletics and physical activities are some of the major factors increasing such injuries in the developing and developed countries. Moreover, this is one of the major factors anticipated to propel the demand for the sports medicine during the forecast period.

“Increasing Participation in Sports to Spur Growth Opportunities”

Introduction of new games in Olympics and other international games is one of the major factors encouraging people to choose this as a career. For instance, kitesurfing was introduced in 2016 Rio Olympics. In addition, the International Olympic Committee announced the addition of five new sporting activities in the Tokyo 2020 games which, includes skateboard, surfing, baseball/softball, sport climbing, and karate. These addition of athletics in the international sports events is anticipated to increase the participation and hence expected to increase demand for this medicine.

Furthermore, perquisites associated with a sporting career are expected to upsurge the number of youths pursuing professional athletics . Some of these pluses comprise celebrity status and fame, high remuneration, availability of other sources of income such as endorsements, and access to the best medical care.

Rising global participation in organized sports, fitness programs, and recreational activities continues to drive sustained demand within the sports medicine industry. Increased awareness of musculoskeletal health and injury prevention has expanded the patient base beyond professional athletes to include amateur participants, aging populations, and occupational users. Growth in youth sports and fitness culture further accelerates injury incidence, reinforcing long-term demand for diagnostic, surgical, and rehabilitative solutions.

Technological advancement remains a primary catalyst. Innovations in arthroscopy, imaging, and minimally invasive surgical tools enable faster recovery and improved clinical outcomes. These advancements reduce hospital stays and support outpatient treatment models, making care more accessible and cost efficient. The rising adoption of biologics, including platelet-rich plasma and regenerative therapies, is also enhancing treatment effectiveness.

Healthcare system evolution contributes significantly to market expansion. Increased insurance coverage, employer-sponsored wellness programs, and government initiatives promoting physical activity support broader access to sports medicine services. Additionally, growing investments by sports organizations and educational institutions in injury management infrastructure further strengthen demand. Collectively, these factors create a favorable environment for sustained market growth.

Market Restraints

Despite strong growth fundamentals, the sports medicine market faces several structural and economic constraints. High treatment and equipment costs remain a major barrier, particularly for advanced surgical systems and regenerative therapies. Limited reimbursement coverage in certain regions restricts patient access and discourages healthcare providers from adopting high-cost technologies.

Regulatory complexity also constrains market expansion. Approval processes for medical devices and biologics vary significantly across regions, extending time to market and increasing development expenditures. Compliance with evolving safety, efficacy, and data requirements adds operational burden, particularly for smaller manufacturers.

Workforce limitations present additional challenges. A shortage of trained orthopedic surgeons, sports medicine specialists, and rehabilitation professionals restricts service capacity in many regions. This imbalance affects patient throughput and limits the scalability of advanced treatment models.

Economic volatility further impacts demand, as sports medicine procedures are often elective and sensitive to disposable income fluctuations. Price competition among vendors places pressure on margins, reducing investment flexibility. These combined restraints necessitate strategic planning, cost optimization, and focused innovation to maintain competitiveness.

Market Trends

The sports medicine industry is experiencing structural transformation driven by technological convergence and evolving care delivery models. Minimally invasive and arthroscopic procedures continue to replace traditional open surgeries, offering faster recovery times and improved patient satisfaction. This shift supports the growing preference for outpatient and ambulatory care settings.

Digital health integration is accelerating, with wearable devices, remote monitoring tools, and data analytics enhancing injury tracking and rehabilitation adherence. Artificial intelligence applications are increasingly used for imaging analysis, risk assessment, and personalized treatment planning. These capabilities improve clinical precision while supporting scalable care delivery.

Regenerative medicine represents a key trend, with expanding use of biologics such as platelet-rich plasma and stem cell therapies. These approaches aim to restore tissue function and reduce reliance on surgical intervention. Sustainability considerations are also shaping procurement strategies, encouraging the use of durable materials and efficient manufacturing processes.

Together, these trends are redefining clinical pathways, shifting value toward outcome-based care models and reinforcing long-term demand for advanced sports medicine solutions.

Market Opportunities

The sports medicine market presents significant growth opportunities across emerging and developed economies. Rapid urbanization, expanding middle-class populations, and increasing health awareness in developing regions create substantial untapped demand. Governments investing in sports infrastructure and public health initiatives further enhance market accessibility.

Technological innovation offers substantial opportunity for differentiation. Digital rehabilitation platforms, telemedicine integration, and data-driven performance analytics enable scalable care models and improved patient engagement. Companies that leverage interoperable systems and remote monitoring capabilities can extend reach beyond traditional clinical environments.

Strategic partnerships represent another avenue for expansion. Collaborations between device manufacturers, healthcare providers, and sports organizations accelerate innovation and market penetration. Joint research initiatives support product development while reducing financial risk.

Preventive care and injury risk reduction programs also present growth potential. As healthcare systems emphasize cost containment, solutions that reduce injury incidence and recovery time gain strategic relevance. Organizations that align product portfolios with value-based care objectives are well positioned to capture long-term growth within the evolving sports medicine landscape.

SEGMENTATION

By Device Type Analysis

“Bone Reconstruction Devices Segment is anticipated to grow at a Faster Pace during the forecast period.”

Based on type, the global market can be segmented into surgery devices, bone reconstruction devices, body support devices, and others.

Surgery Devices

Surgical devices represent a core revenue segment due to their essential role in treating complex sports injuries. Arthroscopy systems, fixation devices, and minimally invasive surgical tools dominate this category. Continuous improvements in visualization, precision, and ergonomic design have enhanced procedural outcomes and reduced complication rates.

Hospitals and high-volume orthopedic centers remain primary adopters, supported by rising procedure volumes and expanding indications. Technological convergence with robotics and navigation systems further strengthens demand for advanced surgical solutions.

Bone Reconstruction Devices

Bone reconstruction devices are increasingly utilized in trauma management, ligament repair, and degenerative conditions. Growth in this segment is driven by rising incidences of fractures, ligament tears, and age-related musculoskeletal deterioration. Innovations in biomaterials, bioresorbable implants, and patient-specific implants improve healing outcomes and reduce revision rates. Adoption is particularly strong in sports involving high-impact injuries, including football, basketball, and skiing.

Body Support Devices

Body support devices, including braces, compression garments, and orthotic supports, represent a stable and expanding segment. These products are widely used across injury prevention, post-operative recovery, and rehabilitation phases. Their non-invasive nature and accessibility support high adoption among amateur athletes and general consumers. Demand is reinforced by growing awareness of injury prevention and increased participation in fitness activities.

Others

This category includes rehabilitation equipment, monitoring devices, and adjunctive technologies. Digital rehabilitation platforms, sensor-based monitoring tools, and therapeutic accessories are gaining prominence. These products support data-driven recovery programs and align with the broader shift toward personalized care models.

Technological advancements in implants coupled with increasing application of arthroscopy, ligament repair products and fracture products are some of the factors anticipated to aid growth of the body reconstruction devices segment. For instance, nearly 120,000 to 200,000 anterior cruciate ligament (ACL) reconstructions are performed every year in the U.S.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

“Knee Segment is expected to hold the Highest Share among Application”

On the basis of application, the market can be segmented into knees, head & neck, shoulder, ankle & foot, wrist and elbow and others.

Knee segment dominated the market share in 2018 and is expected to grow at significant CAGR during the forecast period. Increasing number of knee injuries coupled with rising demand for minimally invasive surgeries are some of the major factors anticipated to propel the segment growth. Knee applications account for the largest share of the sports medicine market due to the high prevalence of ligament injuries, meniscal tears, and degenerative conditions. Sports involving running, jumping, and sudden directional changes contribute significantly to injury incidence. Advanced arthroscopic techniques, biologic therapies, and post-surgical rehabilitation protocols continue to drive segment growth.

- The Knee segment is expected to hold a 36.8% share in 2018.

Head and neck applications primarily involve concussion management, cervical spine injuries, and trauma-related conditions. Growing awareness of long-term neurological risks has increased demand for diagnostic tools and protective solutions. Sports organizations are investing heavily in injury prevention and monitoring technologies to mitigate long-term health consequences.

Shoulder injuries, including rotator cuff tears and dislocations, are common across contact and overhead sports. Surgical innovation and improved implant design have enhanced recovery outcomes. The segment benefits from increasing participation in sports such as swimming, baseball, and tennis.

Ankle & foot segment is anticipated to grow at a higher pace during the forecast period of 2019-2026. Increased participation in physical activities leading to several injuries such as foot and ankle injuries, stimulating demand for sports medicine in developed and developing countries. According to the American College of Foot and Ankle Surgeons (ACFAS), ankle sprains account for 10.0% of overall injuries registered in emergency departments.

Ankle and foot injuries are prevalent across both recreational and professional sports. Advances in imaging, fixation devices, and rehabilitation protocols have improved treatment effectiveness. This segment benefits from growing awareness of early intervention and functional rehabilitation strategies.

Repetitive strain and impact injuries drive demand in this segment, particularly among athletes involved in racket sports and throwing activities. Minimally invasive techniques and targeted rehabilitation programs support continued adoption of specialized treatment solutions.

Additional applications include hip injuries and spinal conditions, which are gaining attention due to aging populations and increased sports participation among older adults. These areas represent emerging opportunities for device manufacturers and service providers.

By End User Analysis

“Hospitals Segment is expected to hold the Highest Share among End User.”

On the basis of the distribution channel, the market can be segmented into hospitals and specialty clinics.

Hospitals

Hospitals remain the dominant end-user segment due to their comprehensive infrastructure, multidisciplinary expertise, and ability to manage complex surgical cases. Access to advanced imaging, operating facilities, and post-operative care supports high procedural volumes.

Hospitals also serve as primary centers for clinical research and training. Availability of advanced medical equipment, skilled healthcare professionals, and growing number of athletic injuries in the developed and developing nations are some of the factors attributed to the growth of the hospital segment.

Specialty Clinics

Specialty clinics are experiencing rapid growth driven by focused expertise, shorter wait times, and cost-efficient care delivery. These facilities increasingly adopt advanced technologies to compete with hospital systems. Their outpatient orientation aligns with the growing preference for minimally invasive procedures and same-day discharge models.

Trauma centers and specialty clinics is expected to witness lucrative growth during the forecast period of 2019-2026. The increasing number of orthopedic clinics and trauma centers coupled with a growing preference to orthopedic specialist in case of sports injury is anticipated to propel segment growth.

Overall, segmentation trends reflect a market increasingly shaped by technological integration, specialization, and patient-centric care models. Vendors that align product development with evolving clinical workflows and end-user expectations are positioned to achieve sustainable competitive advantage.

REGIONAL ANALYSIS

North America Sports Medicine Market Analysis:

North America generated a revenue of USD 2.60 billion in 2018 and is anticipated to grow at a moderate CAGR during the forecast period. The increasing number of orthopedic centers, increasing participation in athletics and physical activity along with growing investment in the development of sports-related medicine treatment devices is anticipated to boost the growth of the regional market during the forecast period followed by Europe.

North America dominates the sports medicine market due to advanced healthcare infrastructure, high sports participation, and strong reimbursement systems. Continuous innovation, widespread adoption of minimally invasive procedures, and significant investment in research and development reinforce regional leadership. The presence of major manufacturers further supports consistent technological advancement.

North America Sports Medicine Market Size, 2025

To get more information on the regional analysis of this market, Download Free sample

United States Sports Medicine Market:

The United States accounts for the largest share of regional revenue, driven by high procedure volumes and rapid technology adoption. Strong professional sports culture, favorable reimbursement policies, and extensive outpatient care networks support sustained demand. Continuous innovation and clinical research reinforce the country’s leadership in sports medicine solutions.

Europe Sports Medicine Market Analysis:

Europe demonstrates stable growth supported by universal healthcare access and increasing focus on preventive care. Adoption of advanced surgical techniques and rehabilitation technologies is widespread. Regulatory harmonization across member states facilitates product commercialization, while aging populations and active lifestyles continue to support market expansion.

Germany Sports Medicine Market:

Germany remains a key European market due to strong healthcare infrastructure and advanced orthopedic expertise. High investment in medical technology and research supports innovation. The country’s emphasis on sports science and rehabilitation drives consistent demand for advanced sports medicine solutions.

United Kingdom Sports Medicine Market:

The United Kingdom market benefits from structured healthcare delivery and growing private sector participation. Increased focus on injury prevention and rehabilitation supports demand for modern sports medicine technologies. National initiatives promoting physical activity further contribute to market stability and long-term growth.

Asia-Pacific Sports Medicine Market Analysis:

Asia Pacific is anticipated to grow at a higher CAGR during the forecast period. Rising demand for these medicines from developing countries such as China, India, and Japan is anticipated to boost the growth of the market in the region. Furthermore, Asia Pacific Knee, Arthroscopy and Sports Medicine Society (APKASS) conducts annual conferences to educate healthcare professionals with an aim to update knowledge, nourish education and to create awareness about the recent research & development in this type of medicine. These factors are anticipated to increase the adoption of athletic career and demand for sports medicine devices hence boosting the market revenue.

Asia-Pacific represents the fastest-growing regional market, supported by rising disposable incomes, expanding healthcare access, and growing sports participation. Government investment in infrastructure and increased awareness of injury management accelerate adoption of advanced sports medicine solutions across the region.

Japan sports medicine Market:

Japan’s market growth is driven by an aging yet active population and strong emphasis on preventive healthcare. Advanced medical technologies, combined with high standards of clinical practice, support adoption of innovative sports medicine solutions across professional and recreational settings.

China sports medicine Market:

China’s sports medicine market is expanding rapidly due to increasing health awareness, government investment in sports development, and modernization of healthcare facilities. Growing participation in organized sports and domestic manufacturing capabilities support sustained market growth.

Latin America sports medicine Market Analysis:

Latin America shows moderate but steady growth driven by expanding private healthcare systems and rising sports participation. Brazil and Mexico lead regional demand, supported by improving infrastructure and greater access to orthopedic and rehabilitation services.

Middle East & Africa sports medicine Market Analysis

The Middle East and Africa region demonstrates emerging growth potential, supported by healthcare modernization and investment in sports infrastructure. Gulf countries lead adoption of advanced technologies, while broader regional growth remains constrained by uneven access to specialized medical services.

Sports medicine Industry Competitive Landscape

“Arthrex. Inc., Smith & Nephew and Stryker Account for Highest Market Share in Terms of Revenue”

Arthrex. Inc. is a leading player in the global market, owing to its strong portfolio and strong distribution network globally. In order to strengthen the market position, key market players are focusing on the introduction of minimally invasive reconstruction and surgery devices and mergers and acquisitions with other key market players with an aim to establish strong brand presence. Arthrex. Inc., Smith & Nephew and Stryker, dominated the market in 2018. Other players operating in the market are CONMED Corporation, Zimmer Biomet, KARL STORZ SE & Co. KG, Johnson & Johnson Services, Inc. and others.

The sports medicine industry features a dynamic competitive environment characterized by the presence of multinational corporations, specialized medical device manufacturers, and emerging technology-driven firms. Leading companies maintain diversified portfolios encompassing surgical instruments, implants, biologics, and rehabilitation solutions. Competitive positioning is reinforced through continuous innovation, regulatory expertise, and global distribution networks.

Market leaders focus on research and development to introduce next-generation products that enhance clinical outcomes and procedural efficiency. Strategic acquisitions enable portfolio expansion and entry into adjacent therapeutic areas. Partnerships with hospitals, sports organizations, and academic institutions strengthen clinical validation and market reach.

Emerging players differentiate through niche specialization, digital health integration, and cost-efficient solutions tailored to outpatient and ambulatory settings. Many leverage data analytics, remote monitoring, and personalized treatment platforms to address evolving clinical needs. Pricing strategies and localized manufacturing further support competitiveness in cost-sensitive markets.

Overall, competition is intensifying as companies seek to balance innovation, scalability, and regulatory compliance. Long-term success increasingly depends on the ability to deliver integrated solutions that align with evolving healthcare delivery models and value-based care frameworks.

List Of Key Companies Profiled:

- Arthrex, Inc.

- Smith & Nephew

- Stryker

- CONMED Corporation

- Zimmer Biomet

- Johnson & Johnson Services, Inc.

- KARL STORZ SE & Co. KG

- Other players

Latest Sports medicine Industry Developments (2024–2025)

- February 12, 2024: Smith+Nephew unveiled an expanded sports medicine portfolio to enable biological healing, including the REGENETEN® Bioinductive Implant and the AGILI-C® Cartilage Repair Implant.

- April 19, 2024: Arthrex received both Gold and Silver Medals at the 2024 Edison Awards. The Gold award was for the MIS FiberTak® Achilles SpeedBridge™ Repair Implant System with Knotless Rip-Stop, and the Silver award was for the SutureLoc™ implant, the first knotless, all-suture retensionable anchor designed specifically for arthroscopic meniscal root repair.

- March 2024: Stryker Corporation Completed the acquisition of a digital rehabilitation technology firm to expand post-operative care capabilities and strengthen data-driven patient monitoring solutions.

- June 2024: Zimmer Biomet Introduced a next-generation sports medicine implant portfolio designed to improve biomechanical performance and support faster patient recovery timelines.

- September 2024: Arthrex Expanded biologics manufacturing operations to meet rising demand for regenerative therapies used in sports injury treatment and recovery optimization.

- February 2025: DJO Global Launched an AI-enabled rehabilitation ecosystem integrating wearable sensors and analytics to enhance outcome tracking and personalized therapy planning.

REPORT COVERAGE

The report provides detailed information regarding various insights of the market. Some of them are growth drivers, restraints, competitive landscape, regional analysis, and challenges. It further offers an analytical depiction of the sports medicine market trends and estimations to illustrate the forthcoming investment pockets. The market is quantitatively analyzed to provide the financial competency of the market. The information gathered in the report has been taken from several primary and secondary sources.

Report Scope & Segmentation

Request for Customization to gain extensive market insights.

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Device Type

|

|

By Application

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 8.01 billion in 2025 and is projected to reach USD 18.42 billion by 2034.

In 2026, the market was valued at USD 8.78 billion.

The market is likely to exhibit a CAGR of 9.7% during the forecast period.

Knee segment is expected to be the leading segment in this market during the forecast period.

Rising prevalence of sports injuries is one of the key factor driving the growth of the market

Arthrex. Inc., Smith & Nephew, and Stryker are among the top players in the market.

North America is expected to hold the highest market share in the market.

- 2021-2034

- 2025

- 2021-2024

- 130

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us