Surface Radar Market Size, Share & Industry Analysis, By Installation Type (Mobile and Fixed), By Technology (Mechanically Scanned Antennas, Passive Electronically Scanned Array (PESA), and Active Electronically Scanned Array (AESA)), By Frequency Band (S Band, X Band, & L Band), By Range (Short Range, Medium Range, and Long Range), By Platform (Ground Based and Naval Based), By Application (Surveillance, Defense, C-UAS, Weapon Detection & Tracking, and Others), By Dimension (2D, 3D, and 4D), By Component (Antenna, Transmitter, Receiver, & Signal Processor), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

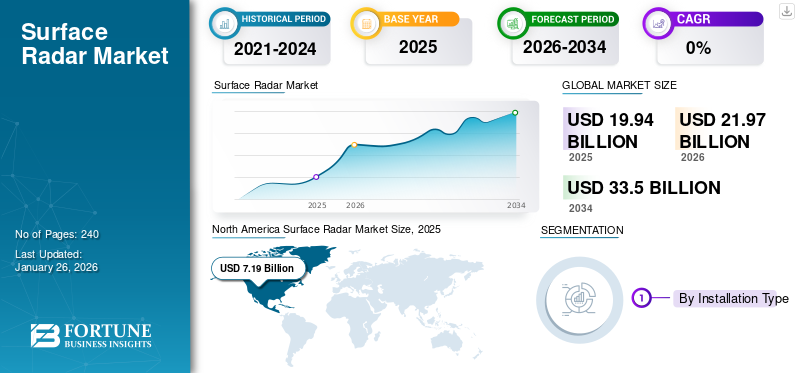

The global surface radar market size was valued at USD 19.94 billion in 2025. The market is projected to grow from USD 21.97 billion in 2026 to USD 33.50 billion by 2034, exhibiting a CAGR of 5.41% during the forecast period. North America dominated the surface radar market with a market share of 36.04% in 2025.

A surface radar is a radar system used to detect, locate, track, and identify various objects. It is mainly classified into naval-based and ground-based radar, depending on the type of platform. It helps to locate objects on the surface and lower atmosphere. Surface radar is a critical system used in the defense industry for various military applications such as air and coastal surveillance, air traffic control, border monitoring, protection of critical assets, and mobile military defense operations.

The market is expected to grow significantly during the forecast period, owing to a rise in defense expenditure and an increase in the need for radars to detect and counter various weaponry and missile systems. The market of surface radars includes key companies such as Lockheed Martin, Raytheon, Thales, Leonardo S.p.A, Saab AB, and others. Military and navy forces of various countries across the globe collaborate with these market players through contracts and agreements to strengthen their surface surveillance and defense capabilities.

Download Free sample to learn more about this report.

GLOBAL SURFACE RADAR MARKET KEY TAKEAWAYS

Market Size & Forecast:

- 2025 Market Size: USD 19.94 billion

- 2026 Market Size: USD 21.97 billion

- 2034 Forecast Market Size: USD 33.50 billion

- CAGR: 5.41% from 2026–2034

Market Share:

- North America dominated the surface radar market with a 36.04% share in 2025, driven by increasing defense spending, missile defense investments, and strong presence of key market players like Lockheed Martin and Raytheon Technologies.

- By technology, Active Electronically Scanned Array (AESA) is expected to retain the largest market share in 2025, supported by its superior multi-target tracking, jamming resistance, and wide operational capabilities across land and naval platforms.

Key Country Highlights:

- United States: Strong demand for advanced radar systems like LTAMDS and AN/SPY-6 due to airspace defense modernization and 360° threat detection capabilities, including against hypersonic weapons.

- Ukraine: Procurement of short-range air defense systems (e.g., Thales Ground Master 200) driven by the Russia-Ukraine conflict, with increased focus on agile, multi-mission radar systems.

- United Kingdom: Government awarded USD 359.23 million to BAE Systems for radar system upgrades on Royal Navy ships, including Artisan and Long Range Radar systems.

- Japan: Received its first AN/SPY-7 radar antenna to enhance maritime and aerial surveillance under the Aegis-equipped vessel program.

- India: Investing in indigenous 3D surface radars for border surveillance and missile detection as regional tensions increase.

Impact of Russia-Ukraine War

The Russia-Ukraine conflict has significantly accelerated global demand for advanced surface radar systems, driven by heightened security concerns and the urgent need to counter evolving aerial threats. European countries have rapidly increased procurement of air defense and early warning radars, such as the U.S.-supplied Patriot systems, to bolster national security and deter aerial threats.

For instance, in June 2024, Thales signed a contract to deliver a second complete short-range air defense system to Ukraine, following the proven battlefield effectiveness of the first system supplied in 2023. The new system includes the ControlMaster 200 (CM200) with the Ground Master 200 air surveillance radar, ControlView command-and-control center, radio communications, and portable weapon allocation terminals, enabling detection and engagement of threats from low to high altitudes in diverse environments. The conflict has highlighted the need for high-tech, agile radars capable of detecting drones, missiles, and low-flying aircraft, leading to contracts such as Ukraine’s acquisition of Thales Ground Master 200 and British Blighter A422 radars for anti-UAS operations.

Nations globally are prioritizing radar modernization to address vulnerabilities exposed by the war, particularly against drones, low-altitude aircraft, and missile systems. Defense budgets are being reallocated to enhance air defense networks, with a focus on multi-mission radars capable of detecting and tracking diverse threats across land, sea, and air domains. The conflict has highlighted the importance of electronic warfare resilience. This has encouraged huge investments in radar technologies resistant to jamming and spoofing. Geopolitical tensions have also promoted collaborative defense initiatives, such as multinational radar-sharing networks, to improve situational awareness and collective security. The conflict has increased the demand for surface radars and stimulated market growth.

Surface Radar Market Trends

Rapid Integration of GaN and AESA Technologies in Next-Gen Defense Surface Radars is a Key Market Trend

GaN Technology Used in Transmitters of Surface Radars

GaN technology, which stands for Gallium Nitride, is a semiconductor material used in radar systems to enhance performance and efficiency. It offers advantages such as higher power density, wider bandwidth, and better thermal management compared to traditional silicon-based radar components. This enables radars to detect smaller or stealthier targets at longer ranges, operate over wider frequency bands, and better resist electronic jamming.

Key players in the market are increasing their focus on the design and development of GaN radar systems to enhance the performance and efficiency of the radar systems. For instance, in August 2024, Raytheon announced that it had commenced the production of the LTAMDS gallium nitride (GaN) missile-defense radar system. The LTAMDS GhostEye radar has gallium nitride (GaN) components. Moreover, there is a rise in the replacement of radar systems with advanced GaN surface radars to meet the evolving air and missile defense needs.

Defense forces of various countries are collaborating with surface radar manufacturers for the development of surface radars equipped with GaN technology for improved weapon detection and tracking. For instance, in January 2024, the U.S. Air Force awarded Lockheed Martin USD 65 million to build three additional 3DELRR radar systems (total contract now ~USD 471.6 million), replacing aging AN/TPS-75 radars with advanced GaN-based AESA technology for long-range detection of missiles, aircraft, and drones.

Adoption of Active Electronically Scanned Array (AESA) Antenna Technology in Surface Radars

AESA antenna technology is increasingly utilized in modern surface defense radars due to its significant performance and operational advantages. AESA (Active Electronically Scanned Array) antennas, which consist of hundreds or thousands of individual transmit/receive modules (often GaN-based), allow radars to steer beams electronically without moving parts. This enables rapid tracking of multiple targets, high spatial resolution, and robust operation even if some modules fail.

Numerous surface radar manufacturers integrate AESA technology in radars to achieve high resolution, quick response, and high energy efficiency. Major defense contractors are investing heavily in maturing and deploying these technologies, with Raytheon, for example, demonstrating and fielding GaN-based AESA radars for both domestic and international customers. In addition, the defense forces aim to transform the air defense with advanced technology radar systems, which is expected to push market expansion. For instance, in September 2023, the U.S. defense force awarded a contract worth USD 585 million to Northrop Grumman for the development of GaN-based AESA surface radars to enhance air defense and electronic warfare capabilities. Such a rise in the integration of AESA technology in radar is anticipated to drive market growth during the forecast period.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increase in Defense Spending to Propel Market Growth

Various countries across the globe are increasing their defense budgets with the aim of modernizing armed forces and enhancing surveillance capabilities. The defense expenditure has witnessed a significant increase in recent years. For instance, the defense budget reached USD 2.46 trillion in 2024, up from 2.24 trillion in 2023. The growth rate was 7.4% globally in 2024 compared to 2023. Countries in the region, such as Asia, the Middle East & North Africa, and Europe, witnessed major budget increases in response to heightened geopolitical tensions and security threats. The surge in conflicts, territorial disputes, and cross-border tensions occurring across the world has encouraged governments to start making huge investments in advanced technologies to strengthen national security and surveillance infrastructure.

Surface radars are critical for detecting and tracking land, sea, and air targets, making them essential for modern defense systems. Therefore, such a defense budget expansion pushes the demand for surface radar systems that offer real-time threat detection, real-time surveillance, and situational awareness. High defense spending has allowed the government and defense forces of various countries to invest in procurement and research & development of advanced radar technologies such as phased array radars. Moreover, the increased defense budget also enables for integration of advanced technology such as GaN, AESA radar systems, and the development of long-range radars based on evolving mission scenarios. These advancements make surface radar systems more reliable, accurate, and efficient, further boosting their adoption.

Rise in Integration of Surface Radar with Defense Systems to Accelerate Market Growth

Surface radars are essential components of integrated defense systems, including missile defense, air defense, naval surveillance, and battlefield management. The radar system is used in applications such as detection, tracking, locating, and providing accurate data of the target to the weapon systems. Surface radars are integrated with command and control systems to enable real-time situational awareness, faster threat detection, and coordinated response. This integration increases the operational effectiveness of defense forces. Such advantages promote the investment in radar systems that can be integrated with other defense assets.

The rapid evolution of missile capabilities is driving nations to prioritize surface-based missile defense systems for protecting critical assets and urban centers. Their adaptable design against modern threats ensures these solutions remain indispensable to global security and future defense planning. Surface radar manufacturers focus on designing innovative radar systems that integrate with different critical infrastructures. For instance, in April 2024, Hensoldt, a German-based defense electronic solution provider, received an order worth approximately USD 113 million to supply TRML-4D radars, including a maintenance and training package, to Latvia and Slovenia as part of the European Sky Shield Initiative (ESSI). The radar is procured to be integrated into the IRIS-T SLM (Surface Launched Medium Range) air defense systems.

In addition, other defense systems such as THAAD, Patriot, Aegis, and others use surface radars as a critical component of the system for detecting, tracking, and intercepting ballistic, cruise, and hypersonic missiles to safeguard national and territorial security. Thus, the shift toward multi-function radar systems that combine surveillance, tracking, and missile guidance in a single platform is expected to accelerate the surface radar market growth in the coming years.

Market Restraints

High Development and Deployment Costs to Hinder Market Growth

The high development and deployment costs of advanced surface radar systems act as a critical restraint on market growth. The manufacturing of Active Electronically Scanned Array (AESA) systems requires substantial R&D investments. Thus, advanced radar systems, particularly military-grade phased array radars, require substantial investments in R&D, precision manufacturing, and maintenance. The components required for the development of radars, such as gallium nitride (GaN)-based transmitters and high-performance cooling systems, drive up production costs.

Moreover, integrating these radars with existing defense networks demands software customization and interoperability trials, further inflating budgets. Ongoing expenses, such as maintenance, technician training, and frequent hardware or software upgrades, add to the total cost of ownership. All such factors are expected to hamper the growth of the surface radars industry during the forecast period.

Market Opportunities

Growing Demand for Surface Radars to Counter Unmanned Aerial Vehicle Threats to Drive Market Growth Opportunities

Unmanned Aerial Vehicles (UAVs) have evolved into critical assets for modern military activities, particularly in intelligence, surveillance, and reconnaissance (ISR) roles. There is a growing trend of UAVs being weaponized, which poses a direct threat to both military and civilian targets. Therefore, as UAVs become more prevalent, they encourage evolving risks ranging from surveillance and reconnaissance to potential armed attacks. Such factors have increased the demand for counter-UAV (C-UAV) technologies focused on identifying and countering such aerial threats.

Modern surface radars, especially those utilizing technologies such as Frequency Modulated Continuous Wave (FMCW) and Active Electronically Scanned Array (AESA), are being increasingly used to counter-drone operations. These radars help to detect, track, and support the neutralization of UAVs, even in challenging environments. This increased focus on counter-UAV measures has led to a surge in demand for short-range radar systems. This increase in demand is fueling the production of surface radars with counter-UAS capabilities and flexible deployment options.

For instance, in March 2025, Saab and the Swedish Air Force developed and evaluated the “Loke” counter-drone system in just 84 days. The radar was manufactured to rapidly address the urgent threat posed by drones on the modern battlefield. Loke integrates the Giraffe 1X radar for drone detection, a lightweight command-and-control system, and the Trackfire remote weapon station for neutralization, providing a modular and scalable solution that covers the entire engagement process.

Therefore, the defense agencies are prioritizing the deployment and upgrade of surface radar systems to safeguard national assets and maintain airspace security. These developments are expected to present growth opportunities for the market.

Segmentation Analysis

By Installation Type

Fixed Segment Held Largest Market Share Due to Its Extended Range, Expanded Coverage, and Fast Response Time

On the basis of installation type, the market is classified into mobile and fixed.

The fixed segment is likely to lead the largest surface radar market, holding 58.38% share in 2026, owing to several advantages, including long-range surveillance, early threat detection, and the ability to track multiple targets simultaneously. Moreover, there is a rise in the demand for fixed surface radars for building a reliable, accurate, up-to-date Recognized Air Picture (RAP). For instance, in July 2023, Thales signed an agreement with the Swedish Defence Materiel Administration (FMV) for the delivery and installation of SMART-L Multi Mission Fixed (MM/F) long-range radars. These radars are expected to be used for detecting and tracking various targets at long ranges to achieve and maintain airspace sovereignty. Such increased demand for fixed surface radars for air and coastal surveillance is expected to drive segment growth.

The mobile segment is expected to grow at the highest CAGR during the forecast period. There is increased adoption of mobile surface radars due to their portability and quick deployment properties. The governments of various countries are investing in mobile radars to provide real-time information on targets, enemy troops, and potential threats. Moreover, the defense forces collaborate with surface radar manufacturers to procure mobile surface radars to support their ground-based air defense systems. For instance, in August 2024, Saab was awarded a contract worth USD 73.02 million by the Swedish Defence Materiel Administration (FMV) to supply Giraffe 1X radar for one of Sweden’s Ground Based Air Defence (GBAD) solutions. The radar will be deployed on the Sisu GTP armored vehicle. Such developments are anticipated to promote the adoption of mobile surface radars in defense operations, which drives the growth of the segment.

By Technology

Active Electronically Scanned Array (AESA) Segment to Lead Due to Its Enhanced Performance and Electronic Warfare Capabilities

On the basis of technology, the market is classified into Mechanically Scanned Antennas, Passive Electronically Scanned Array (PESA), and Active Electronically Scanned Array (AESA).

The Active Electronically Scanned Array (AESA) segment is projected to remain the dominant technology in the global market with a share of 60.79% in 2026. The segment is also projected to grow at the highest CAGR during the forecast period. AESA technology is increasingly favored in surface radars for defense due to its superior performance and capabilities compared to traditional radar systems. AESA radar antennas use a beam steering technique without physical movement, faster scanning rates, enhanced resolution, multi-target tracking, and greater resistance to jamming. Defense forces of multiple countries are using AESA radars to solidify air surveillance and air defense capabilities. For instance, in December 2023, Thales signed a letter of award for the supply of the new GM400α long-range radar delivered with a complete station infrastructure to the Royal Malaysia Air Force (RMAF). GM400α is a fully digital active electronically scanned array long-range air defense 3D radar.

The Passive Electronically Scanned Array (PESA) segment is expected to grow steadily during the forecast period. Surface radars integrated with passive electronically scanned arrays are employed for various defense applications such as military surveillance, border monitoring, and tracking UAVs. For instance, the AN/SPY-1 Aegis Combat System surface combat system uses an AN/SPY-1 passive electronically scanned array (PESA) 3D radar system manufactured by Lockheed Martin.

To know how our report can help streamline your business, Speak to Analyst

By Frequency Band

S Band Segment Holds Largest Market Share Due to Its Increased Demand for Wide Area Surveillance

On the basis of frequency band, the market is classified into S band, X band, L band, and others.

S band segment dominates by holding the largest share of 40.95% in 2026. Surface radars that operate on S-band frequency are increasingly utilized in defense for their ability to provide long-range and wide-area surveillance. These radars are a critical system for tracking missiles, aircraft, and drones over large territories. An increase in government investments and procurement contracts is further driving the adoption of S-band surface radars in both fixed and mobile platforms. For instance, in December 2024, Saab signed a contract worth USD 48 million with BAE Systems in support of the U.S. Air Forces in Europe for multiple Giraffe 4A radar systems. Sea Giraffe 4A is a naval long-range AESA S-band multifunction radar. Thus, the increase in demand for S band surface radars for long-range surveillance and surface defense applications is expected to drive the growth of the segment.

The X-band segment is estimated to be the fastest-growing segment owing to its accurate target discrimination and high-resolution imaging capabilities. X band surface radars are increasingly being used for precise tracking and fire control operations. As border security and anti-drone operations become more critical, military organizations are prioritizing X band radar deployments.

By Range

Long Range Holds Largest Share Due to Growing Demand for Rapid Threat Detection, Missile Defense, and Wide-Area Surveillance

On the basis of range, the market is classified into short range, medium range, and long range.

The long-range segment dominates with a share of 43.98% in 2026, and includes surface radars that can detect targets at a distance of over 200 km. The segment is growing as long-range surface radars are extensively used for air surveillance, target detection and tracking, and missile locating. There is a rise in the need for long range radar systems to monitor the airspace, identify potential threats, and provide target data to regulate air sovereignty. Moreover, the long range radar is also popularly used to track and detect air and naval targets. For instance, in February 2025, the U.S. Defense approved the USD 304 million sale of AN/TPS-78 long-range radar to Egypt. The S-band air surveillance radar system includes an advanced small target drone and maritime tracking subsystem with integrated automatic detection and tracking.

The short range segment is estimated to be the fastest-growing segment owing to the rising need for counter-drone operations and rapid threat response. Short-range surface radars are experiencing rapid growth due to their effectiveness in detecting and tracking nearby threats. The surge in asymmetric threats, such as small UAVs and low-flying projectiles, has increased the need for short-range detection systems. Moreover, the short-range surface radars are extensively used to tackle a wide variety of airborne threats, which is expected to propel the segment growth. For instance, in November 2024, Thales and the NATO Support and Procurement Agency (NSPA) signed a contract with the Portuguese Army for the supply of a ForceShield system. The ForceShield solution includes a short range Ground Master 200 air surveillance radar designed to strengthen the short-range air defence (VSHORAD) capabilities.

By Platform

Ground Based Segment Holds Largest Share Due to Surge in Need for Air Defense, Border Security, and Counter-Drone Operations

The market by platform includes ground based and naval based.

Ground based radars segment holds the largest share of the market. Ground based surface radars are in high demand due to increasing aerial threats, including drones and missiles, which require robust detection and response capabilities. The radars are installed at ground level, either on land, high mobility vehicles, containers, trailers, and others. They are used in various applications such as border surveillance, monitoring troop movements, and maintaining situational awareness. For instance, in January 2024, the Ministry of National Defence of Lithuania and the Ministry of Defence of the Netherlands signed an agreement with Thales regarding the procurement of the Thales Ground Master 200 Multi-Mission Compact (GM200 MM/C) radars. GM200 MM/C is a ground based radar that is expected to be used by both countries for supporting airspace surveillance tasks or integrating with air defense systems.

The naval is estimated to be the fastest-growing segment. This segment is expected to witness high growth as there is an increased focus on maintaining maritime security during the rising geopolitical tensions. Naval radars are utilized for detecting and tracking surface vessels, aircraft, and low-flying threats. Modern naval radars utilize technologies such as Active Electronically Scanned Array (AESA) and FMCW for enhanced detection, target discrimination, and all-weather performance. The naval forces are collaborating with various surface radar manufacturers to produce and supply radars that can be installed on ships and vessels for air surveillance and defense applications. For instance, in June 2024, Raytheon awarded a USD 677 million contract to continue to produce AN/SPY-6(V) radars for the U.S. Navy. Moreover, it is expected to be installed on more than 65 U.S. Navy ships over the next 10 years to defend against air, surface, and ballistic threats. Thus, such an increase in demand for naval-based radars for surveillance and target interception in the future is expected to drive the growth of the segment.

By Application

Surveillance Segment Holds Largest Market Share Due to Rise in Demand for Airspace Monitoring and Surveillance Solutions

On the basis of application, the market is classified into surveillance, defense, C-UAS, weapon detection & tracking, and others.

The surveillance segment will sustain the leading position during the forecast period. The demand for surface radars in surveillance applications is increasing due to escalating geopolitical tensions. These radars provide real-time detection and tracking of potential threats, enabling early warning and rapid response to hostile activities. Defense modernization programs and increased military budgets worldwide are fueling investments in state-of-the-art surveillance radar systems. Collaborative defense initiatives, such as NATO programs, are also driving the adoption of advanced surveillance radars among member countries.

The C-UAS segment is estimated to be the fastest-growing segment. The increasing use of Unmanned Aerial Vehicles (UAVs) and drones has led to a surge in the need for counter-UAS solutions. Surface radars equipped with advanced detection and tracking capabilities are essential for identifying and neutralizing small, low-flying, and agile UAV threats. The rise in asymmetric warfare, terrorism, and the use of drones for reconnaissance and attacks has surged the demand for precise, real-time anti-drone radar technologies. For instance, in January 2025, Elbit Systems Ltd. received a contract worth approximately USD 60 million to supply its multi-layered Counter Unmanned Aerial Systems (C-UAS) to a NATO European country. The solution includes DAiR Radar, which is utilized for rapid detection and location of multiple drones, and neutralizing them.

By Dimension

3D Range Holds Largest Market Share Due to Its Ability to Offer Accurate Range and Data

On the basis of dimension, the market is classified into 2D, 3D, and 4D.

The 3D segment will sustain its dominance during the forecast period due to 3D surface radars being increasingly adopted in defense due to their ability to provide precise range, azimuth, and elevation data, which is essential for tracking aerial threats such as aircraft, missiles, and drones. For example, the AN/MPQ-64 Sentinel is a widely used X-band 3D radar system deployed for short-range air defense, offering early warning and cueing for weapon systems. The AN/TPY-4 and TPS-77 MRR manufactured by Lockheed Martin are some of the 3D surface radars used to detect and track a wider range of threats.

The 4D segment is estimated to be the fastest-growing segment, owing to its advantages, such as accurate target discrimination, movement analysis, and classification of objects. Modern 4D radars are increasingly getting popular for tracking the position, speed, and direction of multiple objects simultaneously, which is essential for countering complex, fast-evolving threats. For instance, in April 2025, the Swedish Defence Materiel Administration (FMV) signed an agreement with Thales for the supply of the 4D Thales Ground Master 200 Multi-Mission Compact radar (GM200 MM/C). The radar is deployed to provide time-on-target across a wide spectrum of threats during surveillance.

By Component

Signal Processor Holds Largest Share Due to Increase in Demand for Advanced Signal Processors to Counter Stealthy and Rapid Threats/Attacks

On the basis of component, the market is classified into antenna, transmitter, receiver, signal processor, and others.

Signal processors is the dominating segment in the market due to their critical role in enhancing detection accuracy, clutter suppression, and real-time target identification. The complexity of modern warfare is increasing with the manufacturing of more stealthy and agile targets. This has led to a rise in demand for processors capable of handling high data volumes and sophisticated analytics.

The transmitter segment is estimated to be the fastest-growing segment owing to the demand for higher power, frequency agility, and reliability in modern surface radar systems. The push for miniaturized, energy-efficient transmitters has also facilitated the deployment of mobile and unmanned radar platforms for rapid response scenarios. Modern transmitters support multi-band and multi-mode operations, allowing a single radar system to adapt to diverse mission profiles, from maritime surveillance to urban counter-UAV tasks. Moreover, there is growing emphasis on the development of radars with transmitters that can seamlessly integrate with other defense systems. For instance, in October 2024, the Norwegian Ministry of Defense announced plans to develop a radar with Raytheon and Kongsberg Defense & Aerospace for supporting the National Advanced Surface-to-Air Missile System (NASAMS) against high-value targets. The features of the radar include an electronically scanned array and gallium nitride (GaN) technology for providing high power handling capabilities, efficiency, and high-frequency operations.

Surface Radar Market Regional Outlook

On the basis of region, the surface radar market is studied across North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Surface Radar Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 7.19 billion, accounting for 36.04% of the worldwide market, and is projected to grow to USD 7.95 billion in 2026. North America dominated the market due to the increasing defense spending and huge investment in the missile defense system. Numerous key players in the market, such as Lockheed Martin Corporation, Raytheon Technologies, and Northrop Grumman Corporation, are headquartered in the U.S. The focus of the U.S. government on strengthening border security, airspace surveillance, and missile defense has resulted in continuous procurement and upgrading of advanced radar systems. There is a surge in the procurement and deployment of new ground-based and shipborne radars for various military operations. For instance, in April 2025, the U.S. Army selected Raytheon’s Lower Tier Air and Missile Defense Sensor (LTAMDS) to replace the aging Patriot radar, rapidly moving the program from prototype to production using special contracting authority. LTAMDS delivers advanced 360-degree threat detection and tracking, including against hypersonic weapons. The U.S. market is projected to reach USD 7.28 billion by 2026.

Europe

The European market generated USD 5.87 billion in 2025, representing 29.45% of the global market landscape, and is expected to reach USD 6.43 billion in 2026. Europe is the key region in the market due to the presence of major surface radar manufacturers such as Hensoldt, Saab AB, and others. Increase in defense spending, cross-border security concerns, and the modernization of military assets are driving the growth of the market in the region. The region benefits from strong collaboration through NATO, which drives joint procurement and deployment of radar systems for air and missile defense across member states. Ongoing conflicts and geopolitical tensions, particularly in Eastern Europe, have led to accelerated investments in early warning and surveillance radars. Moreover, there is a rise in the development of the next generation of radar technology to counter emerging threats.

For instance, in June 2023, the UK Defense Ministry awarded a contract to BAE Systems worth USD 359.23 million to support the Royal Navy’s three main radar systems: Artisan, Sampson, and Long Range Radar (LRR). Through this contract, BAE Systems is expected to provide maintenance support and upgrade existing radars, including offering technology upgrades to systems already in use as well as those being installed on the Royal Navy’s new Type 26 frigates. The UK market is projected to reach USD 1.5 billion by 2026, while the German market is projected to reach USD 1.24 billion by 2026.

Asia Pacific

Asia Pacific contributed 25.42% to the global market in 2025, with a valuation of USD 5.07 billion, and is projected to reach USD 5.64 billion in 2026. The market in the Asia Pacific is experiencing significant growth due to an increase in defense budgets. Regional disputes in the region have prompted large-scale investments in surveillance, air defense, and coastal monitoring radars. For instance, India’s deployment of indigenous 3D surveillance radars and China’s expansion of maritime radar networks underscore the strategic importance of radar technology in the region. For instance, countries in the Asia Pacific region are also investing in advanced radar platforms for missile defense and counter-UAV operations. For instance, in January 2025, the Japan Ministry of Defense received its first AN/SPY-7(V)1 radar antenna for the Aegis System Equipped Vessel (ASEV) to support the national security goals of the country.

The Japan market is projected to reach USD 0.95 billion by 2026, the China market is projected to reach USD 2.08 billion by 2026, and the India market is projected to reach USD 1.63 billion by 2026.

Rest of the World

The rest of the World contributed approximately USD 1.81 billion to the global market in 2025, accounting for 9.08% share, and is expected to reach USD 1.96 billion in 2026. In the Rest of the World, regions such as Latin America and the Middle East, the market is growing at a moderate pace. The Rest of the World, encompassing Latin America, the Middle East & Africa, is witnessing steady growth in the market due to rising security concerns, modernization of armed forces, and increased investments in border and maritime surveillance. Countries in Latin America, such as Brazil, are investing in the procurement of advanced radar systems to counter missile threats and enhance airspace security amid regional instability. For instance, in June 2024, the Brazilian Air Force announced that it had acquired Ground Master 200 Multi-mission All-in-one (GM 200 MM/A) tactical air surveillance radars. The radar is used for air surveillance, as well as ground-based air defense (GBAD) operations.

Competitive Landscape

Key Market Players

Key Players Focus on Production of Advanced Technology Radars and Strategic Collaboration with Defense Forces to Enhance Their Market Presence

The surface radar market is highly competitive, driven by a rise in global defense budgets, technological advancements, and the increasing importance of space-based capabilities in the military sector. Some of the top players in the industry are Lockheed Martin, Raytheon, Thales, Leonardo S.p.A, and Saab AB. Moreover, the key players’ continuous investment in research and development, product innovation, and strategic partnerships strengthens their market position and increases the market share. These key players are actively engaging in collaborations with defense agencies, government organizations, and technology firms to co-develop advanced radar solutions tailored for evolving military needs, including counter-drone, missile defense, and autonomous systems applications.

LIST OF KEY SURFACE RADAR COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Raytheon Technologies Corporation (U.S.)

- Thales (France)

- Leonardo S.p.A (Italy)

- Saab AB (Sweden)

- BAE Systems (U.K.)

- Northrop Grumman Corporation (U.S.)

- IAI (Israel)

- Elbit Systems (Israel)

- L3Harris Technologies, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Thales received a contract from the Swedish Defence Materiel Administration to supply Ground Master 200 Multi-Mission Compact radar, enhancing Sweden’s airspace sovereignty with advanced 4D AESA technology and rapid deployment capability.

- March 2025: The Indian Ministry of Defence signed a USD 340.6 million contract with Bharat Electronics Limited for the Indigenous Low-level Transportable Radar (LLTR) ‘Ashwini’, an active electronically scanned phased array radar designed by DRDO to enhance the Indian Air Force’s ability to detect and track aerial targets, including fighter jets, UAVs, and helicopters, at low altitudes.

- January 2025: Raytheon was awarded a USD 529 million contract to supply the Netherlands with a Patriot air and missile defense system fire unit, including a Lower Tier Air and Missile Defense Sensor (LTAMDS) radar, launchers, and command and control stations, to replace the unit previously donated to Ukraine.

- September 2024: Lockheed Martin secured an additional order from the Norwegian Defence Materiel Agency for three more TPY-4 ground-based multi-mission radars, raising Norway’s total to 11, after the radar completed its Critical Design Review, confirming it meets stringent program requirements.

- March 2024: RTX's Raytheon secured a USD 2.1 billion Army contract (2024) and achieved Milestone C approval (2025) for LTAMDS production after delivering six radars under a 2019 agreement, positioning it as the next-gen 360° AESA radar for global air defense. The company is scaling production to 12 units/year to meet the U.S. and international demand.

REPORT COVERAGE

The report provides a detailed analysis of the sector and focuses on important aspects such as key players, installation type, technology, frequency band, range, platform, application, and component, depending on various regions. Moreover, it offers deep insights into the surface radar market trends, competitive landscape, market competition, and market status and highlights key industry developments. Additionally, it encompasses several direct and indirect factors that have contributed to the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 5.41% from 2026 to 2034 |

|

Segmentation

|

By Installation Type

By Technology

By Frequency Band

By Range

By Platform

By Application

By Dimension

By Component

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 19.94 billion in 2025 and is projected to record a valuation of USD 33.50 billion by 2034.

Registering a CAGR of 5.41%, the market will exhibit significant growth during the forecast period of 2026-2034

By technology, the Active Electronically Scanned Array (AESA) segment is expected to lead the market.

North America dominates the market in terms of share.

In 2025, the market value stood at USD 7.19 billion.

The key factor driving the market is an increase in defense expenditure across the globe.

- 2021-2034

- 2025

- 2021-2024

- 240

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us