Surgical AI Assistance Software Market Size, Share & Industry Analysis, By Component (Software & Services), By Technology (Machine Learning & Deep Learning, Natural Language Processing (NLP), & Others), By Deployment (Cloud-Based, On-Premise, & Hybrid), By Application (Pre-operative Surgical Planning, Intra-operative Guidance & Navigation, Robotic Surgery Assistance, Surgical Video Analytics & Performance, Clinical Decision Support, & Others), By Workflow (Pre-operative, Intraoperative, & Postoperative) By End User (Hospitals & ASCs, Specialty Clinics, & Others), & Regional Forecast, 2026-2034

Surgical AI Assistance Software Market Size and Future Outlook

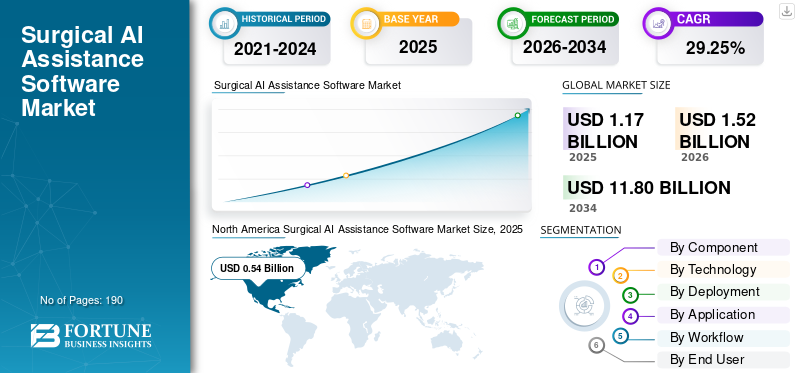

The global surgical AI assistance software market size was valued at USD 1.17 billion in 2025. The market is projected to grow from USD 1.52 billion in 2026 to USD 11.80 billion by 2034, exhibiting a CAGR of 29.25% during the forecast period. North America dominated the surgical AI assistance software market with a market share of 46.15% in 2025.

The global surgical AI-assistance software market is expected to grow rapidly in the coming years. The market growth is driven by the rising demand for minimally invasive and robotic-assisted procedures and by the growing focus on surgical efficiency and precision. These software platforms help healthcare providers improve patient care. As hospitals continue to invest in digital surgery infrastructure, AI-enabled software is becoming increasingly crucial for converting surgical data into actionable insights and supporting better clinical and operational outcomes. Furthermore, continued product innovation by leading companies is expected to strengthen market expansion across hospitals, ambulatory surgical centers, and specialty surgical practices.

Strategic collaborations among key companies and new product launches by these companies to incorporate AI capabilities into their surgical-assistance software solutions reinforce the market's growth potential.

- For instance, in April 2024, Medtronic launched a new AI analysis capability for laparoscopic and robotic-assisted procedures through its Touch Surgery Ecosystem, including 14 new Performance Insights algorithms and Touch Surgery Live Stream. These launches were designed to expand AI-powered surgical insights, simplify workflow, and improve performance review. Such product advancements are expected to support the wider adoption of surgical AI-assistance software and contribute to the overall global market growth.

Furthermore, leading players in the industry, such as Intuitive Surgical, Inc., Medtronic plc, Brainlab SE., and Proximie Limited, are focusing on expanding their offerings and strengthening their market positions.

Download Free sample to learn more about this report.

SURGICAL AI ASSISTANCE SOFTWARE MARKET TRENDS

Shift Toward Data-Driven Surgical Performance Optimization is a Significant Market Trend Observed

A prominent global trend in the market is the shift toward data-driven surgical performance optimization. Hospitals and surgical teams are placing greater focus on measurable outcomes, procedural consistency, and operating room efficiency. This AI-enabled software analyzes surgical videos, instrument movements, workflow patterns, and case-level data to identify performance variations and convert them into actionable insights. As a result, healthcare providers are increasingly using these tools not only to support surgeons during procedures but also to improve training, standardization, and post-case review. Such factors are strengthening the role of surgical AI assistance software as a long-term performance improvement tool rather than only a procedural support solution.

- For instance, in September 2025, Intuitive Surgical launched Real-Time Surgical Insights for da Vinci 5, including new software capabilities such as Force Gauge, In-Console Video Replay, and Network CCM. These solutions were designed to enhance surgeon and hospital efficiency. Such developments show how companies are moving toward data-led surgical assessment and workflow optimization, which is expected to accelerate the adoption of surgical AI assistance software across advanced operating environments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Minimally Invasive and Robotic-Assisted Surgeries is Accelerating Adoption of AI Tools for Surgical Assistance

The rising adoption of minimally invasive and robotic-assisted surgeries is a key driver of global surgical AI assistance software market growth. These procedures require greater precision, visualization, coordination, and data support during surgery. As hospitals and surgeons shift toward minimally invasive techniques, the need for software that improves navigation, enhances intraoperative decision-making, and standardizes surgical performance is growing. These factors are driving strong demand for AI-assistance platforms that help reduce variability, improve efficiency, and support better clinical outcomes. As a result, the wider use of robotic and minimally invasive procedures is directly supporting the expansion of surgical AI-assistance software across advanced operating room settings.

- For instance, in July 2025, Medtronic plc received CE Mark for LigaSure technology on the Hugo robotic-assisted surgery system, expanding the system’s capabilities for gynecologic, general, and urologic procedures in Europe. The development showcases how companies are broadening the applications of robotic-assisted surgery, increasing the need for intelligent software layers that support workflow, visualization, and surgical performance in minimally invasive settings.

MARKET RESTRAINTS

Cybersecurity and Data Privacy Risks to Limit Adoption of Surgical AI Assistance Software to Restrain Market Growth

A restraint in the global market is the risk of cybersecurity breaches and data privacy concerns. These platforms rely heavily on connected devices, surgical video, cloud infrastructure, and continuous data exchange across the operating room. As connectivity increases, the risk of unauthorized access, data leakage, workflow disruption, and system manipulation also rises. This creates hesitation among hospitals and surgical centers, especially when the software is integrated with imaging, robotic, and OR systems that directly affect clinical workflows. As a result, healthcare providers often move more cautiously with deployment, which slows wider adoption of surgical AI assistance software despite its clinical potential.

- For instance, in July 2025, an article titled ‘Enhancing reliability and security in cloud-based telesurgery systems leveraging swarm-evoked distributed federated learning framework to mitigate multiple attacks’ stated that practical deployment remains constrained by increasing cybersecurity threats, which create challenges for patient safety and system reliability. Such factors support the view that cybersecurity is a commercial barrier, as providers delay investment until platforms demonstrate stronger resilience, privacy protection, and secure real-time performance.

MARKET OPPORTUNITIES

Expansion of AI-Powered Preoperative Planning to Create New Growth Opportunities

The global market is expected to offer robust growth opportunities as AI-powered preoperative planning continues to expand. Surgeons are increasingly demanding tools that improve case preparation before the procedure begins. AI-based planning software can analyze patient-specific imaging, support anatomical assessment, recommend procedural approaches, and help surgeons plan with greater accuracy. As a result, these tools can improve confidence in complex procedures, reduce variability in surgical planning, and support better workflow alignment between preoperative and intraoperative stages. This is creating new commercial opportunities for vendors, as hospitals and surgical teams are increasingly interested in software that can make surgery more personalized, efficient, and data-driven.

- For instance, in July 2025, Johnson & Johnson MedTech launched VIRTUGUIDE, an AI-powered patient-matched Lapidus system for bunion surgery in the U.S. The innovative system uses preoperative planning software developed with PeekMed to assess each patient’s bunion and generate personalized recommendations for the intended correction. The development is expected to expand adoption opportunities for surgical AI assistance software across more specialties.

MARKET CHALLENGES

High Implementation and Ownership Cost to Challenge Market Expansion

The global market is facing challenges due to high implementation and ownership costs. Adopting these platforms often requires significant investment. Hospitals invest in compatible hardware, IT infrastructure, system integration, staff training, validation, maintenance, and long-term technical support. As these costs increase, healthcare providers become more cautious about large-scale deployment. This slows adoption across budget-sensitive hospitals and surgical centers, in turn limiting the pace of market expansion even as the clinical value of AI-assisted surgery continues to improve.

- For instance, a 2025 Frontiers in Public Health article on the cost-effectiveness of robotic surgery stated that although robotic surgery shows clinical and economic potential in some settings, the high initial investment remains a significant barrier to adoption. This directly highlights how large upfront spending can delay purchasing decisions and restrict broader implementation, particularly in healthcare systems that require stronger financial justification before adopting advanced surgical technologies.

Segmentation Analysis

By Component

Software Segment Led Market as It Offers the Core Value of Surgical AI Assistance

Based on the component, the market is categorized into software and services.

The software segment accounted for the largest share of the market. Software dominated the market as it offers the core value of surgical AI assistance. It provides an intelligence layer that supports planning, visualization, navigation, analytics, and decision-making during surgery. These software generates the clinical insights, workflow support, and performance intelligence that hospitals are actually buying to improve surgical care. As healthcare providers continue to focus on smarter operating rooms and data-driven surgery, demand remains strongest for software platforms that can be scaled across procedures and sites. These factors have led to high demand for software, encouraging key companies to make strategic product launches.

- For instance, in March 2025, Caresyntax partnered with Pristine Surgical to enhance surgical intelligence for Pristine’s Summit 4K single-use digital arthroscope and Pristine Connect digital platform. Such development highlights how software is differentiating layers in surgical intelligence, which supports the dominance of the software segment in the market.

The services segment is expected to grow at a CAGR of 25.46% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Complex Functionalities of Surgical Assistance Software Utilize Machine Learning and Deep Learning Technologies at Scale, Boosted Segment Growth

Based on technology, the market is segmented into machine learning and deep learning, natural language processing (NLP), and others.

In 2025, machine learning and deep learning accounted for the largest revenue share. Most surgical AI assistance functions depend on image recognition, pattern detection, workflow prediction, and real-time interpretation of surgical data. Such high utilization leads to dominance of machine learning and deep learning in the market. These technologies are used in navigation, video analytics, robotic support, and intraoperative visualization, making them more commercially relevant than narrower technologies in this market. As surgical platforms generate more video and procedural data, machine learning-based models become increasingly valuable, as they continue to improve and can support greater precision and standardization.

- For instance, in July 2024, Stryker received FDA 510(k) clearance for its Q Guidance System with Spine Guidance 5 Software featuring Copilot. The technology integrated smart-powered surgical instruments into its growing ecosystem, demonstrating how machine-learning-driven capabilities are increasingly central to advanced surgical assistance platforms.

The others segment is projected to grow at a CAGR of 29.85% during the forecast period.

By Deployment

Increasing Preference for Cloud-based Deployment by Healthcare Providers Boosted Segment Growth

Based on deployment, the market is segmented into cloud-based, on-premise, and hybrid.

In 2025, the cloud-based segment dominated the market. Surgical AI software increasingly depends on connected workflows, remote collaboration, centralized analytics, software updates, and multi-site data access. Hospitals and health systems are increasingly interested in platforms that enable real-time sharing of surgical content and scalable intelligence across locations, favoring cloud-based models over fully local installations. As digital surgery becomes more networked, cloud deployment becomes more practical, supporting interoperability, easier expansion, and faster feature upgrades.

- For instance, in October 2024, Olympus partnered with Proximie to offer a cloud-based platform for digitizing operating rooms with real-time video, audio, and imagery sharing. Such developments indicate that cloud-connected platforms are becoming the preferred model for scaling surgical intelligence, which supports the leadership of the cloud-based segment.

In addition, the hybrid segment is projected to grow at a CAGR of 26.26% during the study period.

By Application

Real-Time Visualization Support for Intra-Operative Guidance & Navigation Fueled Segment Growth

Based on application, the market is segmented into pre-operative surgical planning, intra-operative guidance & navigation, robotic surgery assistance, surgical video analytics & performance, clinical decision support, and others.

The intra-operative guidance & navigation segment dominated the largest surgical AI assistance software market share. Intraoperative guidance and navigation have the most direct and immediate value during the procedure. Surgeons need real-time support for visualization, anatomical orientation, precision, and instrument guidance, especially in minimally invasive and robotic-assisted surgery. As a result, hospitals often prioritize technologies that improve decision-making in the operating room, keeping intra-operative guidance and navigation at the center of commercial adoption.

- For instance, in September 2025, Brainlab announced FDA 510(k) clearance and U.S. launch of Spine Mixed Reality Navigation. The release focused on advanced visualization support for pedicle screw placement during minimally invasive spine surgery, showing strong market momentum behind intra-operative guidance and navigation solutions.

In addition, the surgical video analytics & performance segment is projected to grow at a CAGR of 30.66% during the study period.

By Workflow

High Utilization of Surgical Assistance Solutions in Intraoperative Workflow Fueled Segmental Growth

Based on workflow, the market is segmented into pre-operative, intraoperative, and postoperative.

In 2025, the intraoperative segment accounted for the largest share. The intraoperative workflow dominated the market as the highest-value use cases for surgical AI occur during the procedure. At this stage, visualization, tissue assessment, anatomical guidance, alerts, and real-time decision support can directly influence surgical safety, precision, and efficiency. Since providers are looking for tools that can improve outcomes at the point of care, adoption is strongest for AI solutions embedded within the intraoperative phase rather than only before or after surgery.

- For instance, in January 2024, Activ Surgical completed its first international procedure using ActivSight Intelligent Light at the Abdali Hospital in Jordan. The technology provided enhanced visualization and real-time, on-demand surgical insights in the operating room, which clearly supports the dominance of intraoperative workflow applications in this market.

The pre-operative segment is projected to grow at a CAGR of 28.18% over the study period.

By End User

Increasing Demand in Hospitals & ASCs Due to Large Patient Volumes Propelled Segment Growth

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

Hospitals and ASCs accounted for the largest market share. Hospitals and ASCs handle the highest volume of surgical procedures and are the primary settings where advanced digital surgery platforms are installed and used. These facilities are more likely to invest in AI-assisted navigation, robotic systems, workflow intelligence, and performance analytics to improve throughput, standardization, and surgical outcomes across multiple specialties. As procedural volumes and digital surgery investments rise, hospitals and ASCs continue to account for the largest market share.

- For instance, in May 2025, Medtronic installed its first Hugo robotic-assisted surgery system in Korea at Seoul National University Hospital, where the system was expected to support treatment, research, and education across multiple surgical procedures. This shows how major hospitals remain the leading adopters of advanced surgical AI-enabled platforms, reinforcing the dominance of the hospitals and ASCs segment.

The specialty clinics segment is projected to grow at a CAGR of 32.78% over the study period.

Surgical AI Assistance Software Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Surgical AI Assistance Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 0.42 billion and maintained its leading position in 2025 at USD 0.54 billion. The region has high adoption of robotic-assisted surgery, strong hospital investment in digital surgery infrastructure, and faster commercialization of advanced surgical software. Recent product launches and the U.S. FDA clearances are also expanding the installed base for AI-enabled surgical workflows, driving growth.

U.S. Surgical AI Assistance Software Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 0.64 billion in 2026, accounting for roughly 42.16% of global revenues.

Europe

Europe is projected to grow at a CAGR of 27.90% in the coming years, the second-highest among all regions, and reach a valuation of USD 0.40 billion by 2026. The region is witnessing growth as hospitals expand robotic and minimally invasive surgery programs, while CE-marked innovations are broadening the range of procedures supported by advanced surgical platforms. Additionally, Europe’s evidence-focused health technology assessment environment supports adoption where software can demonstrate clinical and workflow value.

U.K. Surgical AI Assistance Software Market

The U.K. market is estimated at around USD 0.08 billion in 2026, representing roughly 5.15% of the global revenues.

Germany Surgical AI Assistance Software Market

The German market is projected to reach approximately USD 0.09 billion in 2026, equivalent to around 5.72% of the global revenues.

Asia Pacific

Asia Pacific is estimated to reach USD 0.33 billion in 2026 and secure the position of the third-largest region in the market. The market is growing in the region as healthcare providers increase investment in robotics, AI training, and digital surgery capacity, especially across large hospital systems and emerging medical technology hubs. Regional training initiatives and robotics experience centers are helping accelerate surgeon readiness and access to AI-enabled surgical platforms.

Japan Surgical AI Assistance Software Market

The Japanese market in 2026 is estimated at around USD 0.07 billion, accounting for approximately 4.41% of the global revenues.

China Surgical AI Assistance Software Market

The Chinese market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 0.12 billion, representing approximately 7.75% of global sales.

India Surgical AI Assistance Software Market

The Indian market in 2026 is estimated at around USD 0.03 billion, accounting for roughly 1.75% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.04 billion in 2026. The market is growing in Latin America as hospitals are gradually expanding access to minimally invasive and robotic surgery, and broader competition among surgical platform vendors is improving the availability of advanced systems. In the Middle East & Africa, the GCC is set to reach USD 0.02 billion in 2026.

South Africa Surgical AI Assistance Software Market

The South African market is projected to reach approximately USD 0.01 billion by 2026, accounting for roughly 0.45% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations by Key Players to Propel Market Progress

The global surgical AI assistance software market is highly consolidated, with companies such as Intuitive Surgical, Inc., Medtronic plc, Brainlab SE, Proximie Limited, Medivis, Inc., and Caresyntax GmbH. holding a significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in December 2025, Intuitive cleared the da Vinci Single Port (SP) surgical system for use in inguinal hernia repair, cholecystectomy, and appendectomy procedures. The U.S. FDA approved these clearances. These clearances expand da Vinci SP’s capabilities and build on its existing U.S. clearances in urology, colorectal, thoracic, and transoral procedures.

Other notable players in the global market include Activ Surgical, Inc., Augmedics Ltd., and Stryker Corporation. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period for the global AI assistance software market.

LIST OF KEY SURGICAL AI ASSISTANCE SOFTWARE COMPANIES PROFILED

- Intuitive Surgical, Inc. (U.S.)

- Medtronic plc (U.S.)

- Brainlab SE (Germany)

- Proximie Limited (U.K.)

- Medivis, Inc. (U.S.)

- Caresyntax GmbH (Germany)

- Activ Surgical, Inc. (U.S.)

- Augmedics Ltd. (U.S.)

- Stryker Corporation (U.S.)

- Asensus Surgical, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Genesis MedTech Group and the National University Health System (NUHS) partnered to advance artificial intelligence (AI) in surgery and medical device innovation.

- October 2025: Proximie partnered with the Surgical Innovation and Education Center, IRCAD North America, at The Pearl innovation district. The partnership created a data-driven connected ecosystem offering global access to advanced surgical techniques and technologies.

- July 2025: Olympus Corporation announced the conclusion of an agreement with Revival Healthcare Capital (Revival) to advance endoluminal robotics. Olympus and Revival will co-found Swan EndoSurgical, a new company dedicated to developing a novel robotic system designed to revolutionize gastrointestinal (GI) patient care.

- June 2025: Johnson & Johnson launched the PolyphonicTM AI Fund for Surgery to help develop AI solutions that solve challenges before, during, and after surgery. Joined by a coalition of companies, including NVIDIA and Amazon Web Services (AWS), the initiative builds on the company’s work to advance AI that will help redefine modern surgical practices and improve patient outcomes.

- April 2024: Medtronic launched new AI algorithms for post-operative analysis, providing AI surgical insights across laparoscopic and robotic-assisted surgery, along with 14 new Performance Insights algorithms, boosting AI analytics across an expanded range of laparoscopic and robotic-assisted surgical procedures. The development continues to integrate computing power in operating rooms globally.

REPORT COVERAGE

The report provides a comprehensive global surgical AI assistance software market. It evaluates how AI-enabled software is being used across surgical planning, intraoperative guidance, robotic-assisted surgery, surgical video analytics, workflow optimization, and post-surgical performance review. The study also examines the growing role of integrated and standalone platforms. In addition to segment analysis, the report provides a comprehensive assessment of key market dynamics, including drivers, restraints, challenges, trends, and growth opportunities influencing industry expansion. It further covers a competitive landscape analysis, profiling major companies operating in the market and their product offerings, strategic developments, and innovation focus. The report also includes regional market insights, showing how adoption patterns differ across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Along with this, it also considers company market share, recent product launches, partnerships, regulatory progress, and developments shaping the future of the market worldwide.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 29.25% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, Deployment, Application, Workflow, End User, and Region |

| By Component |

|

| By Technology |

|

| By Deployment |

|

| By Application |

|

| By Workflow |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.17 billion in 2025 and is projected to reach USD 11.80 billion by 2034.

In 2025, the market value stood at USD 0.54 billion.

The market is expected to grow at a CAGR of 29.25% over the forecast period of 2026-2034.

By component, the software segment led the market.

Rising adoption of minimally invasive and robotic-assisted procedures is fueling market growth.

Intuitive Surgical, Inc., Medtronic plc, Proximie Limited, and Medivis, Inc. are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us