AI in Diagnostics Market Size, Share & Industry Analysis, By Component (Solutions/Software and Services), By Technology (Machine Learning, Natural Language Processing (NLP), and Others), By Specialty (Oncology, Neurology, Pathology, and Others), By End-user (Hospitals & Clinics, Diagnostics & Imaging Centers, and Others), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

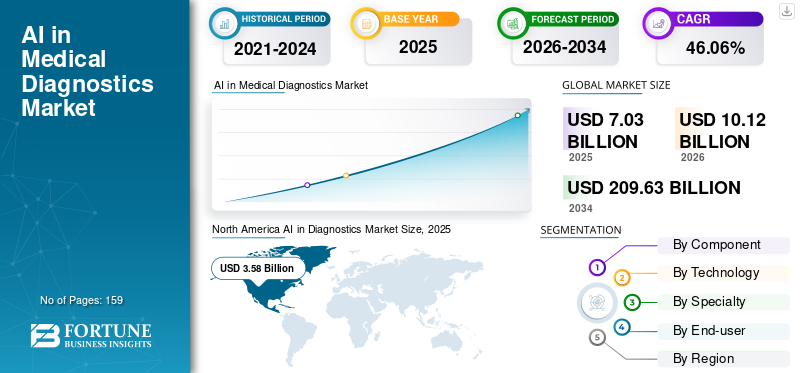

The global AI in diagnostics market size was valued at USD 7.03 billion in 2025. The market is projected to grow from USD 10.12 billion in 2026 to USD 209.63 billion by 2034, exhibiting a CAGR of 46.06% during the forecast period. North America dominated the AI in diagnostics market with a market share of 50.84% in 2025.

The integration of artificial intelligence (AI) in diagnostics is a transformative innovation in the healthcare industry. It utilizes advanced technologies such as machine learning (ML), deep learning, and natural language processing (NLP) to process vast amounts of medical data, including imaging scans, patient histories, laboratory results, and genetic information.

AI processes large data volumes rapidly, significantly reducing the time required for diagnostic procedures. Also, it identifies early signs of diseases such as cancer, heart disease, and neurological conditions, thus enabling timely interventions and better patient outcomes. Such benefits associated with AI in diagnostics applications boost the demand and growth of the market.

Furthermore, the increasing prevalence of chronic diseases and the limited availability of skilled professionals are propelling the demand for artificial intelligence in diagnosis for easier and more accurate detection of disease.

- For instance, in April 2021, according to the Royal College of Radiologists, clinical Radiology UK workforce census report, there was an estimated shortage of 1,939 consultant radiologists, equivalent to 33.0% of the total workforce, and it is estimated that there will be a significant shortage of 3,600 radiologists by 2025. Such a significant demand for skilled professionals increases the adoption of AI in diagnostics.

The global AI in medical diagnostics market has shown robust growth, with projections indicating a continued upward trajectory. Some of the key players operating in the market, including Microsoft Corporation, Google, and Aidoc are offering robust solutions for integrating AI into diagnostics.

Download Free sample to learn more about this report.

Global AI in Diagnostics Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 7.03 billion

- 2026 Market Size: USD 10.12 billion

- 2034 Forecast Market Size: USD 209.64 billion

- CAGR: 46.06% from 2026–2034

Market Share:

- North America dominated the AI in diagnostics market with a 51.46% share in 2024, driven by rapid adoption of AI-based technologies in medical imaging, growing demand for diagnostic accuracy, and strong presence of key players.

- By component, the solutions/software segment is expected to retain its largest market share, supported by continuous advancements in AI-enabled diagnostic platforms and collaborations between technology giants and healthcare providers.

Key Country Highlights:

- United States: Growth is driven by strong collaborations between AI technology providers and healthcare institutions aiming to enhance diagnostic efficiency and streamline clinician workflows.

- Europe: Increasing government funding to deploy AI imaging and decision-support tools in hospitals for chronic disease diagnosis is propelling market adoption.

- China: Rising focus on AI-powered healthcare solutions to address the shortage of skilled professionals and improve early-stage disease detection across major hospitals.

- Japan: Advancements in AI integration for precision diagnostics, particularly in radiology and oncology, are contributing to improved patient care and boosting market demand.

MARKET DYNAMICS

MARKET DRIVERS

Rising Prevalence of Chronic Diseases and Shortage of Healthcare Professionals to Drive the Market Growth

The rising prevalence of chronic diseases, such as cancer, neurological diseases, and cardiovascular conditions, is a prominent driver of AI in the diagnostics market. These diseases require early and accurate detection for effective treatment, which AI-powered diagnostic tools can provide by analyzing complex data with precision.

- For instance, according to the data published in August 2024 by the National Breast Cancer Foundation, Inc. 2024, an estimated 310,720 women and 2,800 men to be diagnosed with invasive breast cancer. Also 1 in 8 women in the U.S. is expected to get diagnosed with breast cancer in her lifetime. Such a large number of patients suffering from chronic diseases requires efficient early diagnosis to improve their quality of life.

Simultaneously, the global shortage of healthcare professionals, including radiologists and pathologists, has increased the reliance on AI to manage workloads efficiently.

- For instance, in 2022, according to the Clinical Radiology UK workforce census report U.K. has a 29.0% shortfall of clinical radiologists that is expected to rise to 40% by 2027 if any actions are not taken. Such a shortfall of radiologists increases the demand for advanced radiological solutions to reduce the workload and increase patient outcomes. Thus drives the global AI in diagnostics market growth.

MARKET RESTRAINTS

Reluctance among Medical Practitioners to Adopt AI is Hampering the Growth of the Market

The hesitance among healthcare professionals to adopt AI technologies is a significant factor restraining the growth of global AI in the diagnostics market. This reluctance often arises from a lack of understanding, fears of job displacement, and distrust regarding the accuracy and reliability of AI-driven tools. Concerns about AI making clinical decisions that have traditionally been the responsibility of human practitioners further exacerbate this issue. To address these obstacles, comprehensive education, training, and demonstrations of AI's advantages are crucial for the building of the healthcare practitioners' trust and confidence in these technologies.

MARKET OPPORTUNITIES

Increasing adoption of AI for Various Untapped Specialty Areas is a Prominent Opportunity for the Market

The increasing adoption of AI in untapped specialty areas, such as ophthalmology, autoimmune disorders, and infectious diseases, remain underexplored. This has created a lucrative growth opportunity for the operating players to increase the launch of new platforms for the untapped specialties.

- In May 2024, Lumibird Medical introduced C.DIAG, an advanced dry eye diagnostic aid platform integrated with AI algorithms. This platform is part of the C.SUITE offering, designed to assist healthcare providers in diagnosing, treating, and educating patients with dry eye disease. Such launches promote market growth during the forecasted timeframe.

MARKET CHALLENGES

Regulatory Compliance and Data Privacy Concerns to Pose a Critical Challenge to Market Growth

The integration of AI in clinical practices has to undergo critical ethical and regulatory concerns. AI’s contribution in healthcare requires adherence to stringent regulations such as HIPAA, which demand transparency, accountability, and robust data protection measures. These frameworks aim to ensure the safety, accuracy, and ethical use of AI diagnostic tools.

Additionally, managing sensitive patient data raises privacy risks, demanding secure handling and compliance. Also, increasing cybercrimes and data leaks are leading to reputational damage and loss of trust, hindering market expansion.

AI IN DIAGNOSTICS MARKET TRENDS

Rising Funding Activities for the Adoption of AI in Precision Diagnostics is a Prominent Trend

Increasing investments from venture capitalists, government programs, and private organizations to expand the development of advanced AI-powered diagnostic tools for precision diagnostics is a prominent trend in the market.

For instance, in October 2024, Ataraxis AI secured USD 4.0 million in seed funding co-led by Giant Ventures and Obvious Ventures. The funding was used for the development of innovative AI-powered diagnostic tools to improve patient outcome predictions and personalize treatments. Such factors drive the adoption of this trend in the market.

Other Trends

Rising Government Initiatives for Boosting the Adoption of AI in Diagnosis

The governments across the globe are prioritizing AI investments in healthcare to expand their services with AI and reduce the increasing workload on the radiologist and the healthcare expenditure for chronic diseases. This is due to increasing prevalence of key diseases and rising demand for accurate and efficient diagnosis for better patient comfort.

- For instance, in June 2023, the UK's National Health Service (NHS) allocated USD 26.8 million to expedite the deployment of AI imaging and decision-support tools. These technologies aimed to enhance rapid diagnosis of conditions such as cancer, strokes, and heart disease, revolutionizing patient care and treatment outcomes.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Strategic Activities to Launch Advanced Solutions/Software to Propel Segment’s Growth

Based on the component, the market is divided into solutions/software and services.

The solutions/ software segment accounted for the largest market share in 2024. The increasing collaboration amongst the key players of the market to develop advanced AI-based diagnostic solutions to boost the segment’s growth.

- For example, in January 2024, Rad AI partnered with Google to utilize its cloud and AI innovations to develop an AI-enabled reporting platform to save radiologists' time, reduce burnout, and improve patient care. Such activities promote the segment’s growth in the market.

The services segment is projected to grow with a moderate CAGR during the forecast period. The growth of the segment is driven by strategic activities amongst the key players who are engaged in developing and launching new services to assist healthcare providers and patients in propelling the segment’s growth.

- For instance, in April 2024, Bayer partnered with Google Cloud to develop AI solutions that support radiologists and enhance patient services. This collaboration aimed to improve the development and deployment of AI-powered healthcare applications, to offer scalable, secure, medical imaging applications, to boost the segment’s growth in the market.

By Technology

Increasing Adoption and Launch of Innovative tools with AI-Machine Learning to Expand Segment’s Growth

Based on technology, the market is divided into machine learning, natural language processing (NLP), and others.

The machine learning segment is expected to hold a maximum portion of the technology segment in the market. Machine learning can analyze vast amounts of healthcare data, identify patterns and make predictions. Thus, ML algorithms help to improve diagnostic accuracy and efficiency, enabling healthcare professionals to make better-informed decisions quickly.

Additionally, the increasing demand and adoption of AI-ML tools for diagnosis by healthcare providers is boosting the segment’s growth in the market.

- For instance, in May 2024, iHridAI launched HarmonyCVI, an artificial intelligence (AI)/ machine learning (ML)-based rapid diagnostics and insights tool. This tool assists cardiologists and radiologists in performing enhanced analyses of cardiac MRI scans. Such launches promote the segment’s growth in the market.

The Natural Language Processing (NLP) segment is expected to grow with a significant CAGR during the forecast period. NLP processes and interprets unstructured clinical data, such as patient notes, medical literature, and electronic health records, to create comprehensive patient profiles. It enables healthcare providers to deliver care with better and faster results by analyzing the medical history of a patient thus making a crucial component in the AI diagnostic landscape.

The others segment, which includes computer vision, robotics, and others is anticipated to grow at a considerable rate in the near future.

By Specialty

Rising Prevalence of Cancer Likely to Propel the Growth of Oncology Segment in the Market

On the basis of specialty, the market is segmented into oncology, neurology, pathology, and others.

The oncology segment held a maximum portion of the global AI in diagnostics market share in 2024. This growth of the segment is driven by the rising prevalence of cancer and increasing research and development activities to launch new drugs for treatment.

Thus, such factors increase the demand for accurate and predictive diagnosis of cancer and propel the demand for AI in oncology diagnosis.

- For instance, in February 2025, Onc.AI received U.S. FDA Breakthrough Device Designation for its Serial CT Response Score (Serial CTRS) model. This deep-learning tool analyzes CT scans to classify patients with metastatic non-small cell lung cancer into high- or low-mortality risk categories. Serial CTRS has shown superior accuracy compared to traditional imaging methods, and this innovation is expected to enhance personalized cancer care and support oncology drug development. Such development promotes the growth of the segment in the market.

On the other hand, the neurology segment is expected to hold a considerable share of the market. This is augmented by the rising prevalence of neurological diseases and increasing demand for early and accurate diagnosis of them.

- For instance, in November 2024, Royal Philips partnered with icometrix with an aim to deploy an advanced solution for MRI brain scans to enhance the diagnosis and treatment monitoring of neurological conditions such as Alzheimer’s and multiple sclerosis. Such advancements boost the growth of the segment during the forecast period.

The pathology segment is expected to grow with a moderate CAGR during the forecast period. AI assists in digitally analyzing tissue images, identifying abnormal cells or patterns, automating routine tasks, and ultimately improving diagnostic accuracy and efficiency, allowing pathologists to focus on more complex cases. Such advantages boost the segment’s growth in the market.

- In August 2024, PathAI, Inc. introduced its AIM-MASH product on the AISight Image Management System (IMS). This advanced AI-based measurement tool is designed to assist in analyzing the Metabolic Dysfunction-Associated Steatotic Liver Disease (MASLD) Activity Score (MAS) component grades and fibrosis staging within the MASH Clinical Research Network (CRN). This advancement aimed to increase the reproducibility and scalability of pathologists' assessments and management for metabolic dysfunction-associated steatohepatitis cases. Thus, such scenarios promote the growth of the segment in the market.

By End-user

Rise in the Number of Chronic Diseases to Drive Segment Growth of Diagnostics & Imaging Centers

On the basis of end-users, the market is segmented into hospitals & clinics, diagnostics & imaging centers, and others.

The diagnostics & imaging centers segment dominated the market. The significant share of the segment is due to increased demand for skilled professionals and increasing workload on the providers. Additionally, the rising prevalence of chronic diseases and increasing demand for faster and more accurate disease diagnosis are expected to raise the adoption of AI tools in these settings, thus propelling the segment’s growth in the market.

- For instance, in July 2024, iCAD, Inc. partnered with Windsong Radiology Group, part of U.S. Radiology Specialists, Inc., with an aim to introduce iCAD’s ProFound AI Breast Health technology at Windsong Radiology Center locations. Such activities to increase AI adoption in radiology centers to promote the segment’s growth.

The hospitals & clinics segment is expected to grow substantially during the forecast period. The increase in the adoption of new technologies in these settings and the increase in collaborations of major players in the market are contributing to the growth of this segment.

Additionally, increasing product launches by the key players to improve physician workflows is propelling the segment’s growth in the market.

- In July 2024, Microsoft collaborated with Mass General Brigham and the University of Wisconsin School of Medicine and Public Health with an aim to advance AI foundation models for medical imaging to drive clinician efficiency and enable better health outcomes. Such collaboration and launches promote the growth of these settings in the market.

The other segment comprises research centers and academic institutes that are anticipated to grow with a moderate CAGR during 2025-2032.

AI IN DIAGNOSTICS MARKET REGIONAL OUTLOOK

By region, this market is divided into North America, Europe, Asia Pacific, and Latin America.

North America

North America AI in Diagnostics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region captured 50.84% of the global market in 2025, generating USD 3.58 billion in revenue, and is projected to reach USD 5.16 billion in 2026. and is anticipated to continue to dominate the global market during the forecast period. Increasing technological advancements and emphasis on utilizing advanced tools for maintaining tedious workflows are augmenting the market’s growth in the region.

U.S.

The U.S. is dominating the market in the North America region. Owing to the increasing adoption of AI-based technologies in medical imaging and diagnostics and the presence of key market players with advanced solutions in AI for diagnostics, the U.S. market is anticipated to witness a strong growth in the coming years.

- In July 2024, GE HealthCare collaborated with Amazon Web Services, Inc. to develop foundational models and generative artificial intelligence (AI) applications with the goal of enhancing medical diagnostics and patient care.

Europe

Europe maintained a strong presence in the global market, reaching USD 1.39 billion in 2025, accounting for 19.78% share, and is expected to reach USD 1.99 billion in 2026. Europe is anticipated to hold the second-largest position in terms of revenue share. The rising funding activities to deploy AI tools in hospitals for speedy diagnosis of chronic diseases to propel the market’s growth in the region.

- For instance, in October 2023, 64 NHS trusts across England secured USD 26.8 million from the Government of the U.K. to deploy AI tools that analyze X-rays and CT scans to speed up diagnosis and treatments for patients and support clinicians in their work with the quicker, more accurate diagnosis of conditions. Such activities boost the market growth in the Europe region.

Asia Pacific

In 2025, Asia Pacific generated USD 1.59 billion, contributing 22.55% to global market revenue, and is projected to grow to USD 2.3 billion in 2026. The Asia Pacific market is projected to witness the highest CAGR, especially in developing countries such as China, Japan, and India. The rising prevalence of chronic diseases and the shortage of radiologists are fostering research and development in AI and machine learning applications in radiology, which is the key factor driving the market growth in the region.

Moreover, the hospitals and diagnostics centers of the region are actively adopting AI for disease detection is one of the prominent regions for the region’s growth during 2025-2032.

- For instance, in March 2025, Continental Hospitals, Hyderabad, India, announced the integration of artificial intelligence (AI) into cancer detection that focuses on detecting breast, lung, and pancreatic cancers at early stages. Such activities promote the growth of the market in the region.

Latin America

The Latin America market generated USD 0.3 billion in 2025, representing 4.28% of the global market landscape, and is expected to reach USD 0.43 billion in 2026. Latin America accounted for moderate market revenue during the forecast period. The region’s growth is expected to be supported by the rising demand for remote patient monitoring and increasing collaborations among companies to expand their healthcare offerings in the market.

Middle East & Africa

Middle East & Africa recorded a market size of USD 0.18 billion in 2025, capturing 2.56% of the global market share, and is projected to reach USD 0.25 billion in 2026. The Middle East & Africa also recorded moderate market revenue during the forecast period. The market growth in this region is supported by increasing technological advancements and healthcare initiatives.

- For instance, in March 2025, Emirates Health Services announced the implementation of advanced AI technology in Medical Examination Centers for Residency to identify pulmonary tuberculosis through standard chest imaging tests. Such developments are expected to bolster market growth across the region.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Expanded Product Launches by Key Players to Propel Market Progress

The global AI in medical diagnostics market holds a semi-consolidated market structure featuring prominent players such as Microsoft Corporation, Google, and NVIDIA Corporation. The substantial share of these companies in the market is due to the strategic activities with the medical devices companies and robust product and service offerings with expanded research and development to enhance user experience is expected to enhance their market positions.

- For instance, in March 2024, Microsoft collaborated with NIVIDA Corporation to leverage generative AI, cloud computing, and advanced technology in healthcare. Combining Microsoft Azure's global scale and security with NVIDIA DGX Cloud and the Clara suite aimed to enhance clinical research, drug discovery, medical imaging, and precision medicine, ultimately improving patient care. Such activities bolster the company’s share in the market.

Other notable players in the global market include Aidoc, Siemens Healthcare Private Limited, PathAI, Inc., and Digital Diagnostics Inc. These companies are anticipated to prioritize new product launches and collaborations to boost their AI in medical diagnostics market share during the forecast period.

LIST OF KEY AI IN DIAGNOSTICS COMPANIES PROFILED

- Amazon.com, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Google (U.S.)

- Siemens Healthcare Private Limited (Germany)

- Aidoc (Israel)

- PathAI, Inc. (U.S.)

- Digital Diagnostics Inc.(U.S.)

- Tempus AI (U.S.)

- Qure.ai (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2024: Siemens Healthineers AG and DeepHealth, Inc. announced a strategic partnership to enhance ultrasound operations by integrating AI-powered health informatics into workflows and imaging hardware.

- December 2024- deepc partnered with Somamed. This partnership aimed to expand deepcOS, an advanced AI platform for radiological diagnostics across Italy.

- November 2024- GE HealthCare collaborated with DeepHealth, Inc. with an aim to develop SmartTechnology solutions for expanding innovation, commercialization and adoption of AI in imaging.

- July 2024- WELL Health Technologies Corp. launched an AI-powered co-pilot for cardiologists designed to identify patients at high risk for cardiovascular disease.

- June 2024- AliveCor, Inc. received U.S. FDA clearance for KAI 12L AI technology and the Kardia 12L ECG System. This technology uses AI for detecting critical cardiac issues, including heart attacks.

- March 2022- Tempus AI launched a multi-center study called "Electrocardiogram-based Artificial Intelligence-Assisted Detection of Heart Disease" (ECG-AID). The study aimed to assess the effectiveness of the company's AI-driven predictive tests in cardiology, focusing on identifying patients at high risk for atrial fibrillation (AFib) and seven types of structural heart diseases (SHD) affecting the mitral, aortic, and tricuspid valves, as well as overall heart function and thickness.

- October 2024: RADPAIR unveiled RADPAIR 2.0, with Groq LPU AI inference technology. This advancement revolutionizes radiology workflows, delivering unparalleled speed, accuracy, and intelligence to radiologists globally.

- November 2024: Koninklijke Philips N.V. partnered with Synthetic MR, a Swedish company specializing in MRI software, to launch Smart Quant Neuro 3D. This innovative solution enhances objective decision-making for diagnosing and assessing treatments for brain disorders such as multiple sclerosis, traumatic brain injury, and dementia.

REPORT COVERAGE

The global AI in diagnostics market report comprises of total global market analysis that emphasizes key aspects such as an overview of cutting-edge technologies, the regulatory environment in major countries, and the challenges faced in adopting and implementing AI driven diagnostics solutions. The report also examines the applications of AI in hospitals and clinics alongside notable industry developments, including mergers, partnerships, and acquisitions. Furthermore, it detailed regional analysis of various segments and the impact of COVID-19 on the market is covered in the report.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 46.06% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Component

|

|

By Technology

|

|

|

By Specialty

|

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 7.03 billion in 2025 and is projected to reach USD 209.64 billion by 2034.

In 2025, North America stood at USD 3.58 billion.

Registering a CAGR of 46.06%, the market will exhibit rapid growth over the forecast period (2026-2034).

The solutions/software segment leads the market.

The rising prevalence of chronic diseases and the shortage of healthcare professionals are driving the market.

Microsoft Corporation, NVIDIA Corporation, and Google are major players in the global market.

North America dominated the market in terms of share in 2025.

Reduction in healthcare workload and accurate diagnostics results are the factors expected to drive the adoption of the products.

- 2021-2034

- 2025

- 2021-2024

- 159

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us