AI in Oncology Market Size, Share & Industry Analysis, By Component (Hardware/Devices and Software & Services), By Deployment (Cloud-based, On-Premise & Hybrid), By Technology (Machine Learning & Deep Learning, Natural Language Processing & Others), By Indication (Breast Cancer, Lung Cancer, Prostate Cancer, Colorectal Cancer, Brain Tumor & Others), By Application (Screening & Diagnosis, Pathology, Radiation Oncology, Clinical Decision Support & Therapy Selection, & Others), By End User (Pharmaceutical & Biotechnology Companies, Healthcare Providers, & Others), and Regional Forecast, 2026-2034

AI in Oncology Market Overview

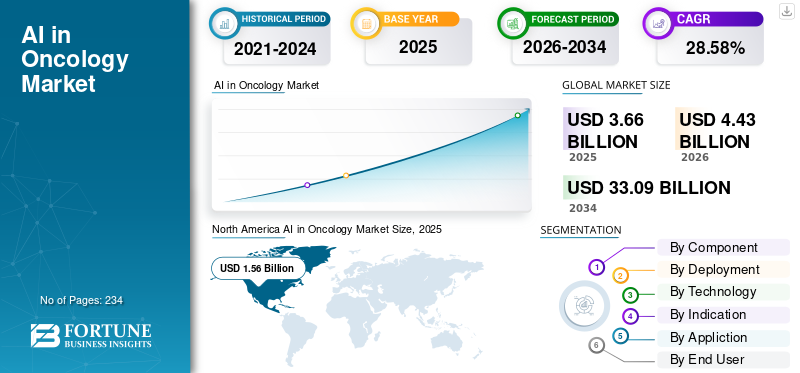

The AI in oncology market size was valued at USD 3.66 billion in 2025. The market is projected to grow from USD 4.43 billion in 2026 to USD 33.09 billion by 2034, exhibiting a CAGR of 28.58% during the forecast period. North America dominated the AI in oncology market with a market share of 42.62% in 2025.

AI in oncology involves employing artificial intelligence, primarily machine learning/deep learning and natural language processing to enhance cancer treatment and research. This assists healthcare professionals and life-science groups in identifying cancer sooner, accurately classifying tumors, selecting personalized treatments, and tracking results. Key factors driving this market growth include increasing prevalence of cancer and screening programs increasing demand for scalable diagnostic tools, improved accuracy and throughput from AI‑assisted radiology and others.

Major companies such as SOPHiA GENETICS, PathAI, Inc., Siemens Healthineers AG, and Insilico Medicine are emphasizing on advancements in their offerings with an aim to gain market share.

Download Free sample to learn more about this report.

AI in Oncology Market Key Takeaways

- 2025 Market Size: USD 3.66 billion

- 2026 Market Size: USD 4.43 billion

- 2034 Forecast Market Size: USD 33.09 billion

- CAGR: 28.58% from 2026-2034

- North America dominated the AI in oncology market with a 42.62% share in 2025.

- The hardware/devices segment is projected to grow at a CAGR of 24.16% during the forecast period.

- The cloud-based segment is anticipated to expand at a CAGR of 37.10% during the forecast period.

North America

North America reached USD 1.56 billion in 2025 and maintained its leading position in the global market.

Europe

Europe is projected to be the second-largest regional market, growing at a CAGR of 21.15% during the forecast period.

Asia Pacific

Asia Pacific is expected to reach USD 0.80 billion by 2026, making it the third-largest regional market.

U.S.

The market is estimated to reach USD 1.73 billion in 2026, accounting for around 39.1% of global revenue.

Japan

The market is estimated at USD 0.18 billion in 2026, representing approximately 4.0% of global revenue.

Read More

AI IN ONCOLOGY MARKET TRENDS

Rising Investment from Pharma and Biotech for AI-enabled Drug Discovery is Emerging Market Trend

Increasing investments in AI by pharma and biotech are establishing a noticeable trend of AI in oncology. Oncology research and development face growing limitations due to high failure rates, costly trials, and sluggish patient enrollment. With biomarker-defined subpopulations dividing patient groups, sponsors are leveraging AI to more rapidly pinpoint the target cancer patients by analyzing multimodal data and aligning them with eligibility requirements on a large scale. Simultaneously, AI is being utilized earlier in the discovery phase to prioritize targets and hypotheses, minimizing wet-lab cycles and concentrating resources on candidates with a greater likelihood of success. This reallocates funds from single-use analytics to scalable AI systems that can assist various programs, regions and study designs. The outcome is an increase in data partnerships, licensing agreements and multi-sponsor platforms where AI enhances both the feasibility of trials and subsequent commercial standing. Eventually, these investments evolve from initial pilot projects into comprehensive R&D processes across the enterprise, fostering continuous market growth in software, services, and data resources. These factors are supporting the overall global AI in oncology market growth.

- For instance, in May 2024, Precision Cancer Consortium (PCC) and Massive Bio announced results from a large multi-sponsor (pharma) clinical trial matching study, highlighting AI used to improve oncology trial matching and supporting drug development workflows.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Cancer Incidence & Screening Programs Propels Market Growth

Growing cancer incidence and wider screening coverage are pushing health systems to adopt scalable diagnostic tools as traditional radiology/pathology capacity cannot expand at the same pace as patient volumes. Global cancer burden is already high and is projected to rise sharply, which increases the number of people entering screening, diagnosis and follow-up pathways. As screening programs expand, providers face larger imaging backlogs and variability in interpretation across sites, hence they look for AI that can triage, standardize reads and flag high-risk cases without adding proportional headcount. Moreover, AI enabled workflows also help deliver more consistent care in community settings by embedding clinical decision support into routine diagnostic steps. All these factors cumulatively drive the market growth.

- For instance, in July 2025, Geisinger announced it launched an AI-enabled breast cancer screening program that uses an AI model to evaluate EHR data monthly, flagging highest-risk patients who are overdue for mammograms and routing them for appropriate screening and follow-up.

MARKET RESTRAINTS

Regulatory Complexity and Variable Reimbursement Pathways to Hamper Market Growth

Regulatory intricacy and inconsistent reimbursement serve as significant restraints in AI for oncology, as vendors need to navigate various approval pathways while demonstrating both clinical and economic value to secure payment. This delays product launches and compels companies to tailor compliance packages for each market, raising expenses and extending time-to-revenue. On the buyer side, hospitals are reluctant to expand implementations when reimbursement lacks clarity, causing AI tools to remain in pilot phases or receive funding solely as departmental innovation expenses. The issue is sensitive for AI in oncology imaging/pathology, as its adoption relies on being embedded in regulated workflows and reimbursement can differ by payer, country, or even the interpretation of codes. This results in limiting the market growth to certain extent.

- For instance, in Jane 2025, the European Commission’s Medical Device Coordination Group and AI Board issued guidance on the interplay between the EU AI Act and the EU Medical Device Regulation (MDR), highlighting that AI medical products may need to comply with two overlapping regimes, which adds documentation and conformity complexity for AI vendors entering/operating in Europe.

MARKET OPPORTUNITIES

Integration with Cloud Computing and Edge Devices Offers Market Growth Opportunities

Combining cloud computing with edge devices presents a significant market opportunity in AI driven oncology. It addresses the two main obstacles to deployment simultaneously: scalability and clinical feasibility. Cloud platforms facilitate the deployment of AI across multi-site hospital networks and imaging chains by offering centralized model management, orchestration, and quicker updates without extensive on-site IT labor. Simultaneously, edge devices facilitate low-latency inference near scanners (CT/MRI/mammography) and assist in maintaining sensitive images locally when required, minimizing bandwidth limitations and alleviating data governance issues. This edge-to-cloud approach enhances reliability for high-volume imaging facilities, as AI can continue operating even with unstable connectivity. With the increase in oncology screening and follow-up imaging volumes, providers are leaning toward SaaS and edge solutions to standardize triage and reporting across multiple locations while managing expenses. All these factors would drive the market growth in the coming years.

- For instance, in March 2025, GE HealthCare announced Genesis solutions, a cloud enterprise imaging SaaS portfolio that explicitly includes an “edge” capability (along with storage, VNA, and data migration) to support deployment across healthcare organizations and streamline imaging workflows.

MARKET CHALLENGES

High Implementation Costs and Requirement for IT Infrastructure Challenges Market Growth

Significant implementation expenses and IT infrastructure needs pose a major challenge for AI in oncology, particularly in smaller hospitals, as these institutions frequently do not possess the digital infrastructure essential for operating AI effectively on a large scale. Numerous oncology AI solutions rely on robust PACS/LIS/EHR integration, secure data pipelines, sufficient bandwidth/storage, and continuous monitoring, meaning the overall cost encompasses not only the license but also interfaces, cybersecurity, computation, workflow redesign, and training. Moreover, smaller hospitals usually possess streamlined IT teams and limited capital/operational budgets, resulting in extended procurement cycles and compelling them to focus on essential systems rather than AI enhancements. Even when the AI model is effective, implementation can be hindered by outdated systems, data-quality issues, and a lack of governance procedures, resulting in a pilot-to-production block. This delays regional expansions and results in uneven uptake, with large networks advancing more quickly than community sites, constraining total addressable market conversion in the short term. All the factors cumulatively affect the market growth.

- For instance, according to a study published in June 2025 in The Lancet eClinicalMedicine, the procurement and early deployment of AI for chest diagnostics (including lung cancer-related workflows) was harder than expected due to challenges such as harmonizing with older IT systems, governance, and operational rollout complexity across NHS Trusts.

Segmentation Analysis

By Component

Increasing Number of Software Deployments to Propel Segmental Growth

Based on the component, the market is divided into hardware/devices and software & services.

The software & services segment captured the largest global AI in oncology market share. Most buyers including hospitals and imaging centers increasingly buy AI as subscriptions or modular licenses (pathology AI, imaging triage, CDS, trial matching), which scales across multiple sites and produces repeatable annual revenue. Additionally, increasing number of collaborations & partnerships between operating players also supported the segment growth.

- For instance, in March 2025, Philips announced it expanded its partnership with Ibex Medical Analytics and released updates to Philips IntelliSite Pathology Solution to accelerate AI-enabled digital pathology workflows for cancer diagnosis.

The hardware/devices segment is anticipated to rise with a CAGR of 24.16% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Rising Focus on Cloud-based Solutions Supported the Segmental Dominance

Based on the deployment, the market is divided into cloud-based, on-premise, and hybrid.

The on-premise segment is anticipated to capture the largest market share in 2025. This is attributed to the fact that many cancer workflows rely on tight integration with legacy PACS/LIS/EHR systems, which is often simpler when AI runs behind the hospital firewall. On-premise setups help meet strict governance requirements such as audit trails, access controls and give providers more direct control over cybersecurity hardening and change management for regulated clinical workflows. Furthermore, the segment is set to hold 45.0% share in 2026.

- For instance, a study published in European Radiology in October 2024 evaluated an on-premise, privacy-preserving large language model (locally hosted Llama-2) to automatically structure radiology reports.

The cloud-based segment is anticipated to rise with a CAGR of 37.10% over the forecast period.

By Technology

High Usage in Various Applications to Boost Machine Learning & Deep Learning Segmental Growth

In terms of technology, the market is divided into machine learning & deep learning, natural language processing, and others.

The machine learning & deep learning segment dominated the global market in 2025. ML/DL scales well across sites as once integrated into PACS/LIS/TPS, it can run continuously on high case volumes with recurring licensing. Also, the use cases depend on deep neural networks for detection, segmentation, classification, and quantitative scoring, where performance gains translate directly into throughput and consistency improvements. Furthermore, the segment is set to hold 64.9% share in 2026.

- For instance, in April 2025, Paige announced the U.S. FDA granted Breakthrough Device designation to Paige PanCancer Detect, an AI-assisted pathology application designed to help detect suspicious cancer foci across multiple tissue and organ types, showing continued regulatory and commercial momentum for deep-learning-based oncology diagnostics.

The natural language processing segment is anticipated to rise with a CAGR of 32.07% over the forecast period.

By Indication

Increasing Focus on Screening Programs to Boost Breast Cancer Segmental Growth

In terms of indication, the market is divided into breast cancer, lung cancer, prostate cancer, colorectal cancer, brain tumours, and others.

The breast cancer segment captured the highest share of the global market in 2025. It has the largest standardized screening footprint (mammography) and therefore the highest routine diagnostic volumes where AI can be scaled quickly. The imaging pathway is also relatively structured (BI-RADS style workflows), making it easier to train, validate and deploy ML models for triage, detection support and risk prediction across hospitals and imaging chains. Breast cancer programs tend to have clearer quality metrics (recall rates, detection rates, interval cancers), so providers can quantify ROI and justify procurement faster than in many other cancers. In addition, breast care pathways commonly combine radiology, pathology, and longitudinal follow-up, creating strong demand for AI that improves end-to-end workflow consistency. Furthermore, the segment is set to hold 23.6% share in 2026.

- For instance, in June 2025, Clairity announced the U.S. FDA De Novo authorization for CLAIRITY BREAST, an AI platform designed to predict a woman’s five-year breast cancer risk from routine screening mammography.

The lung cancer segment is anticipated to rise with a CAGR of 31.04% over the forecast period.

By Application

High Usage in Care Pathways to Boost Screening & Diagnosis Segmental Growth

On the basis of application, the market is divided into screening & diagnosis, pathology, radiation oncology, clinical decision support (CDS) & therapy selection, patient monitoring, drug discovery & development, clinical trial matching & patient stratification and others.

The screening & diagnosis segment captured the highest share of the global market in 2025. These workflows are also highly repeatable such as mammography, LDCT, CT/MRI follow-ups, hence AI tools can be deployed across many scanners and sites and generate recurring, high-throughput usage. It also integrates naturally into existing PACS/radiology workflows, which accelerates adoption across imaging centers. As cancer incidence and screening volumes rise, scalable diagnostic support becomes the quickest lever to expand capacity without adding proportional specialist headcount. Furthermore, the segment is set to hold 18.3% share in 2026.

- For instance, in April 2025, University Hospitals Cleveland Medical Center announced it activated an AI program for early lung cancer identification to support low-dose CT screening workflows.

The patient monitoring segment is anticipated to rise with a CAGR of 35.04% over the forecast period.

By End User

High Utilization of AI by Healthcare Providers to Support Segment’s Leading Position

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, healthcare providers, academic & research institutes, diagnostic laboratories, and others.

In 2025, the healthcare providers segment held the leading position in the global market. They are the primary point of care where AI is used daily to manage high-volume clinical workflows such as screening/diagnosis, pathology review, radiotherapy planning and therapy selection. In addition, hospitals and cancer networks increasingly deploy AI as enterprise platforms integrated with PACS/LIS/EHR, which drives larger contract values and multi-site expansion within health systems. Furthermore, the segment is set to hold 46.6% share in 2026.

- For instance, in October 2024, GE HealthCare announced CareIntellect for Oncology, a cloud-first AI application designed to bring together multi-modal patient data into a single longitudinal view and support care teams (including surfacing potentially suitable clinical trials). Tampa General Hospital and UT Southwestern Medical Center were named as early evaluators.

In addition, pharmaceutical & biotechnology companies are projected to witness a 31.49% growth rate during the forecast period.

AI in Oncology Market Regional Outlook

By geography, the market is divided into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America AI in Oncology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market reached USD 1.30 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position, with USD 1.56 billion. North America is at the forefront due to its concentration of AI providers, imaging networks, and supportive reimbursement policies.

U.S. AI in Oncology Market

The U.S. dominated the North American market and can be analytically approximated at around USD 1.73 billion in 2026, accounting for roughly 39.1% of global market.

Europe

Europe market is anticipated to grow at 21.15% CAGR during the forecast period. The region is anticipated to capture the second leading position among all regions. Europe’s growth is supported by expanding digital pathology and standardization of cancer pathways across public systems, high radiotherapy footprint and increasing focus on data governance and federated models.

U.K. AI in Oncology Market

The U.K. market in 2026 is estimated at around USD 0.25 billion, representing roughly 5.7% of global revenues.

Germany AI in Oncology Market

Germany market is projected to reach approximately USD 0.29 billion in 2026, equivalent to around 6.6% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 0.80 billion by 2026, making it the third largest region in the worldwide sector. The region is experiencing substantial increases in cancer cases and diagnostic imaging volumes, a surge in the use of cloud/hybrid hospital IT in developed markets, and heightened regional clinical trial engagement along with biopharma funding.

Japan AI in Oncology Market

The Japan market in 2026 is estimated at around USD 0.18 billion, accounting for roughly 4.0% of global revenues.

China AI in Oncology Market

China’s market is projected to reach revenues of around USD 0.20 million in 2026, representing roughly 4.6% of global sales.

India AI in Oncology Market

The India market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 3.5% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa, and Latin America regions are expected to experience slower growth throughout the forecast period. The market in Latin America is projected to attain a valuation of USD 0.32 billion by 2026. Key elements such as funding for major hospitals, cancer treatment centers, national health reform initiatives, upgrades to oncology facilities in top private hospital networks, and increased imaging and radiotherapy capabilities are anticipated to propel market expansion.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.08 billion by 2026, representing about 1.7% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Scalable AI Workflows and Number of Installed Bases to Strengthen Market Share of Leading Companies

The competitive landscape of the global AI in oncology market is highly fragmented, with large medtech incumbents, precision-oncology data players, and specialist AI software vendors competing across imaging, pathology, radiotherapy, CDS, and trial matching. Prominent players in the market include Siemens Healthineers AG, Elekta, GE HealthCare, Roche, Tempus, Guardant Health, and others. Strong footprint in radiation oncology, ability to embed AI into end-to-end cancer care workflows, and large installed base across radiotherapy sites are some of the factors supporting dominance of these companies.

Other significant players include Azra AI, SOPHiA GENETICS, Insilico Medicine, PathAI, Inc., and others. These players are increasingly focusing on new product launches, AI platform expansion, and partnerships to widen adoption across hospitals and imaging networks.

- For instance, in May 2025, Viz.ai launched the “Viz Oncology Suite,” expanding its AI-powered platform into oncology to accelerate diagnosis and care coordination.

LIST OF KEY AI IN ONCOLOGY COMPANIES PROFILED

- TEMPUS (U.S.)

- Azra AI (U.S.)

- Ibex Medical Analytics (Israel)

- SOPHiA GENETICS (U.S.)

- PathAI, Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Insilico Medicine (U.S.)

- Guardant Health, Inc. (U.S.)

- Hoffmann-La Roche (Switzerland)

- Elekta (Sweden)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Oracle and the Canadian Institute for Cancer Care (Ci4CC) announced a collaboration to advance AI in oncology, interoperability, next-gen clinical trials, and personalized medicine across Ci4CC’s network.

- October 2025: Dana-Farber, Fred Hutch, MSK, and Johns Hopkins launched the Cancer AI Alliance, backed by AWS, Deloitte, Microsoft, and NVIDIA to accelerate applied AI using cancer data.

- September 2025: Labcorp announced a collaboration with Roche to implement FDA-cleared VENTANA DP 600/DP 200 digital pathology slide scanners, supporting pathologists’ digital diagnosis and future AI integration.

- June 2025: PathAI announced it received FDA 510(k) clearance for AISight Dx for primary diagnosis in clinical settings, enabling broader clinical deployment of digital pathology workflows that can integrate AI.

- April 2025: Precision for Medicine and PathAI announced a collaboration to advance AI-powered clinical trial services and biospecimen products, strengthening trial enablement and patient stratification workflows.

REPORT COVERAGE

The global AI in oncology market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global AI in oncology market outlook report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 28.58% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Indication, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Indication |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.66 billion in 2025 and is projected to reach USD 33.09 billion by 2034.

In 2025, the North America market value stood at USD 1.56 billion.

The market is expected to exhibit a CAGR of 28.58% during the forecast period of 2026-2034.

By component, the software & services segment is expected to lead the market.

Growing cancer incidence and screening programs increasing demand for scalable diagnostic tools are primarily driving market expansion.

TEMPUS, Azra AI, Ibex Medical Analytics, and SOPHiA GENETICS are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 234

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us