Sustainable Materials Market Size, Share & Industry Analysis, By Product Type (Low Carbon & Recycled Metals, Low Carbon & Green Construction Materials, Recycled & Biobased Pulp & Paper, Recycled & Biobased Plastics & Polymers, Sustainable Textile Fibers, and Others), By End Use (Building & Construction, Packaging, Automotive & Transportation, Consumer Goods, Textiles & Apparel, Electrical & Electronics, and Others), and Regional Forecast, 2026-2034

Sustainable Materials Market Size and Future Outlook

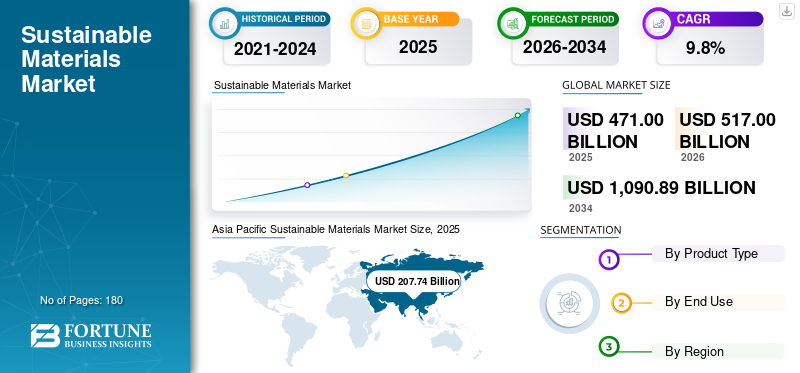

The sustainable materials market size was valued at USD 471.00 billion in 2025. The market is projected to grow from USD 517.00 billion in 2026 to USD 1,090.89 billion by 2034, exhibiting a CAGR of 9.8% during the forecast period. Asia Pacific dominated the sustainable materials market with a market share of 44.% in 2025.

Sustainable materials are engineered or processed material inputs developed to reduce environmental impact across their life cycle while maintaining the functional performance required in industrial applications. These materials are characterized by measurable sustainability attributes such as recycled content, lower carbon footprint, renewable or bio-based origin, responsible sourcing, recyclability, compostability, durability, or reduced dependence on raw fossil-based resources. In commercial use, sustainable materials serve as alternatives to conventional metals, plastics, cementitious materials, paper grades, fibers, composites, and specialty materials, offering buyers lower-carbon, circular, or resource-efficient solutions without compromising performance. The market is being driven by the shift from cost-led material selection toward sustainability-led procurement across major industries. Companies are now considering recycled content, embodied carbon, renewable feedstock use, recyclability, certification, traceability, and end-of-life impact while selecting materials. This shift is supported by stricter regulations on packaging waste, recycling, emissions, and green building practices, as well as corporate targets for carbon reduction and circularity.

The market includes suppliers across metals, polymers, pulp and paper, construction materials, and fibers. Companies are investing in recycling capacity, low-carbon production, bio-based materials, green construction solutions, and recyclable packaging to strengthen their positions. Key players include ArcelorMittal, Holcim, Stora Enso, BASF, and Lenzing. Competitive advantage is increasingly linked to scalable materials with verified sustainability performance and reliable supply.

Download Free sample to learn more about this report.

SUSTAINABLE MATERIALS MARKET TRENDS

Momentum toward Recycled and Low-Carbon Material Inputs across Industrial Value Chains to Fuel Product Adoption

The growing shift toward recycled and low-carbon material inputs is emerging as a key trend in the market. Industries such as construction, packaging, automotive, electronics, and consumer goods are increasingly replacing raw and high-emission materials with recycled metals, plastics, low-carbon cement, green concrete, molded fiber, and certified pulp and paper materials. This transition is supported by corporate sustainability targets, product-level carbon-reduction goals, and increasing pressure to lower Scope 3 emissions across supply chains. Manufacturers are also focusing on materials with traceable recycled content and verified environmental performance to meet procurement requirements. Therefore, the rising integration of recycled and low-carbon inputs across industrial value chains is expected to fuel product adoption.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Regulatory Push for Circular Economy and Rising Consumer Demand for Eco Friendly Products to Drive Market Growth

The market is being driven by stronger regulatory support for circular economy practices and growing consumer preference for eco-friendly products. Governments across major economies are introducing policies to reduce plastic waste, require recycled content, improve packaging recyclability, establish green building standards, and decarbonize industry. These measures are encouraging companies to adopt recycled, bio-based, low-carbon, and recyclable materials across packaging, construction, automotive, textiles, and consumer goods. Similarly, consumers are increasingly favoring products with lower environmental impact, recyclable packaging, and responsibly sourced materials. This is pushing brands to redesign products and packaging with sustainable inputs. Hence, the combined impact of regulation and growing demand for eco-friendly products are expected to drive the sustainable materials market growth during the forecast period.

- The European Commission is expected to adopt the Circular Economy Act by the end of 2026, which is intended to create a single EU market for secondary raw materials, improve the availability of high-quality recycled materials, and strengthen demand for these materials across the region. The Act will support the EU’s Competitiveness Compass objective of positioning the bloc as a global leader in the circular economy by 2030.

MARKET RESTRAINTS

High Production Costs and Performance Limitations Compared to Conventional Materials Restrains Market Growth

High production costs and performance limitations remain major restraints for the market. Many recycled, bio-based, biodegradable, and low-carbon materials are more expensive than conventional alternatives due to limited feedstock availability, complex processing requirements, certification costs, and smaller production scale. In some applications, sustainable materials may also face challenges related to durability, heat resistance, mechanical strength, barrier performance, processability, or consistency of quality. These issues are especially important in packaging, automotive, construction, electronics, and industrial applications where material performance is critical. Price-sensitive customers may delay adoption when cost premiums are high or when product performance requires additional testing and validation. Thus, cost and technical barriers continue to limit wider market penetration.

MARKET OPPORTUNITIES

Innovations in Biodegradable Materials and Green Manufacturing Processes to Create Lucrative Opportunities

Innovations in biodegradable materials and green manufacturing processes are creating strong opportunities in the market. Companies are investing in advanced recycling, closed-loop material recovery, bio-based polymers, compostable packaging, low-carbon cement, green steel, sustainable fibers, and recyclable paper-based materials. These innovations are helping improve material performance, reduce production costs, and expand the use of sustainable alternatives across high-volume applications. Green manufacturing processes using renewable energy, lower-emission production routes, and certified feedstock are also improving the commercial attractiveness of sustainable materials. As brands and industrial buyers seek scalable solutions with measurable environmental benefits, innovation-led product developments are expected to unlock new growth opportunities across packaging, construction, automotive, textiles, and consumer goods.

Segmentation Analysis

By Product Type

Low Carbon & Recycled Metals Dominate Owing to Their Large-Scale Use across Construction and Industrial Applications

Based on product type, the market is segmented into low carbon & recycled metals, low carbon & green construction materials, recycled & biobased pulp & paper, recycled & biobased plastics & polymers, sustainable textile fibers, and others.

Low carbon and recycled metals account for the largest sustainable materials market share due to their extensive use in construction, automotive, electronics, packaging, and industrial manufacturing. Recycled steel, aluminum, and copper help reduce reliance on raw metal production while lowering energy use and embodied carbon. Their strong performance characteristics, established recycling infrastructure, and compatibility with existing manufacturing processes support widespread adoption. The segment’s dominance is also driven by increasing demand for low-carbon building materials, circular metal inputs, and sustainable procurement across heavy industries.

Low carbon and green construction materials are gaining strong traction as builders, developers, and infrastructure owners focus on reducing emissions from buildings and civil projects. The segment includes low-carbon cement, green concrete, recycled aggregates, engineered wood, mass timber, and sustainable insulation materials. Green building standards, public infrastructure decarbonization, and corporate net-zero targets also support demand. As sustainability becomes a key criterion in construction procurement, the segment is expected to expand at a CAGR of 9.8% during 2026–2034.

Recycled and biobased plastics and polymers are becoming important sustainable alternatives across packaging, consumer goods, automotive, agriculture, and industrial applications. Recycled-content mandates, plastic waste reduction targets, and brand-level commitments to recyclable or lower-carbon packaging are driving demand. These materials are also being implemented in durable goods and mobility applications where light weighting and circularity are important. With innovation in advanced recycling and biopolymer performance, the segment is expected to grow at a CAGR of 10.6% during 2026–2034.

By End Use

Building & Construction Dominates Market Due to High Material Consumption and Rising Green Building Adoption

Based on end use, the market is segmented into building & construction, packaging, automotive & transportation, consumer goods, textiles & apparel, electrical & electronics, and others.

To know how our report can help streamline your business, Speak to Analyst

Building & construction accounted for the largest market share in 2025, driven by high demand for low-carbon metals, green construction materials, recycled aggregates, engineered wood, sustainable insulation, and low-carbon cementitious systems. The sector is under increasing pressure to reduce embodied carbon in buildings and infrastructure, making the adoption of sustainable materials a key priority. Green building standards, infrastructure modernization, public procurement policies, and net-zero construction targets are further driving demand. As a result, building and construction remain the leading end-use segment in the market.

Packaging is another active end-use area for sustainable materials, supported by the transition away from raw plastic and non-recyclable formats. Recycled and biobased pulp and paper, molded fiber, recycled plastics, compostable polymers, kraft paper, and biobased packaging materials are increasingly used across food, beverage, personal care, e-commerce, and industrial packaging. With strong adoption across consumer-facing industries, the packaging segment is expected to grow at a CAGR of 10.3% during 2026–2034.

Textiles and apparel are witnessing steady growth in the adoption of sustainable materials as brands shift toward recycled, certified, and lower-impact fiber inputs. Sustainable textile fibers, such as recycled polyester, recycled nylon, organic cotton, lyocell, hemp, flax, and recycled wool, are used in apparel, footwear, sportswear, home textiles, and technical textiles. The segment is supported by brand-level sourcing targets, traceability requirements, and rising consumer interest in responsible fashion, driving growth at a CAGR of 8.9%.

Sustainable Materials Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

Asia Pacific

Asia Pacific Sustainable Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market in 2025, reaching USD 207.24 billion, and is expected to expand at a CAGR of 10.2% over the forecast period. The region’s leadership is supported by large-scale consumption of low carbon and recycled metals, green construction materials, recycled and biobased plastics, pulp and paper materials, and sustainable textile fibers. China, India, Japan, South Korea, and Southeast Asia continue to drive demand through construction activity, packaging growth, automotive manufacturing, electronics production, and textile supply chains. Strong industrial output, rising sustainability regulations, and increasing corporate adoption of recycled and lower-carbon material inputs are expected to keep the Asia Pacific at the forefront of market growth.

China Sustainable Materials Market

China will account for approximately USD 113.99 billion in 2026, representing around 22.0% of global revenues. The country remains the largest single market due to its strong base in construction, metals, plastics, packaging, electronics, automotive manufacturing, and textile production. Demand is supported by rising use of recycled metals, low-carbon construction materials, recycled plastics, and fiber-based packaging across industrial and consumer applications.

To know how our report can help streamline your business, Speak to Analyst

India Sustainable Materials Market

India will reach USD 27.72 billion in 2026, accounting for nearly 5.4% of global sales. The market is gaining momentum due to rapid infrastructure development, packaging growth, textile manufacturing, and the rising adoption of sustainable construction and polymer materials. Increasing regulatory attention on plastic waste, recycling, and green buildings is also supporting demand for recycled, biobased, and lower-carbon material inputs.

North America

North America was at USD 108.33 billion in 2025, growing at a CAGR of 9.1% over the forecast period. The region is supported by strong demand from green construction, sustainable packaging, recycled metals, automotive manufacturing, consumer goods, and electronics. Corporate decarbonization targets and recycled-content commitments are encouraging greater use of low carbon metals, recycled polymers, fiber-based packaging, and green building materials.

U.S. Sustainable Materials Market

The U.S. market will be valued at USD 101.69 billion in 2026, accounting for approximately 19.7% of global revenues. Green building activity, recycled metals, sustainable packaging, low-carbon cementitious materials, recycled plastics, and corporate sustainability procurement drive product demand.

Europe

Europe reached USD 122.46 billion in 2025, expanding at a CAGR of 9.8% through 2034. The region is one of the most regulation-driven markets for sustainable materials, supported by circular economy policies, packaging waste rules, recycled-content targets, green procurement, and low-carbon construction initiatives. Demand is especially strong across recycled and low carbon metals, fiber-based packaging, sustainable construction materials, and recycled or biobased polymers.

Germany Sustainable Materials Market

Germany will stand at USD 29.73 billion in 2026, representing around 5.8% of global revenues. The country’s strong automotive, industrial manufacturing, construction, packaging, and engineering base supports demand for low carbon metals, recycled polymers, green construction materials, and sustainable packaging inputs.

U.K. Sustainable Materials Market

The U.K. market will reach USD 20.20 billion in 2026, accounting for nearly 3.9% of global revenues. Growth is supported by sustainable packaging adoption, green building practices, recycled-content procurement, and consumer goods companies shifting toward lower-impact materials.

Latin America

Latin America recorded USD 18.84 billion in 2025, with the region expected to grow at a CAGR of 8.9% over the forecast period. Demand remains concentrated in packaging, pulp and paper, construction, consumer goods, and selected bio-based material applications. Brazil and Mexico are the major contributors, supported by paper and pulp production, food and beverage packaging, automotive manufacturing, and the gradual adoption of recycled and lower-carbon materials.

Brazil Sustainable Materials Market

Brazil will reach USD 9.87 billion in 2026, contributing around 1.9% of global revenues. The country benefits from its strong pulp and paper base, bio-based feedstock availability, packaging demand, and construction activity. Sustainable material adoption is mainly driven by recycled and biobased pulp and paper, packaging materials, selected green construction inputs, and growing interest in renewable material alternatives.

Middle East & Africa

The Middle East & Africa market reached USD 14.13 billion in 2025, growing at a CAGR of 9.4% during the forecast period. Demand is led by green construction, infrastructure development, low-carbon cement, recycled metals, and sustainable packaging, particularly across GCC countries and South Africa. However, green building programs, infrastructure investments, and corporate sustainability initiatives are expected to gradually increase the use of sustainable material inputs across construction, packaging, industrial, and consumer applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Material Innovation, Circularity, and Low-Carbon Manufacturing Shape Market Positioning

The sustainable materials market is moderately fragmented, with competition shaped by material innovation, recycling capabilities, low-carbon manufacturing routes, feedstock access, certification strength, and application-specific performance. Leading players globally include ArcelorMittal, Holcim, Stora Enso, BASF, and Lenzing, supported by several regional and emerging suppliers focusing on recycled metals, green construction materials, bio-based polymers, molded fiber packaging, and sustainable textile fibers. Companies are increasingly adopting strategies such as low-carbon product launches, expansion of recycling capacity, development of bio-based materials, partnerships with packaging and construction customers, and investments in circular material platforms. As regulatory pressure and corporate sustainability commitments increase, investments in low-carbon metals and recycled plastics are reshaping competitive positioning and accelerating adoption across construction, packaging, automotive, consumer goods, textiles, and industrial applications.

LIST OF KEY SUSTAINABLE MATERIALS COMPANIES PROFILED

- ArcelorMittal (Luxembourg)

- SSAB (Sweden)

- Hydro (Norway)

- Holcim (Switzerland)

- Heidelberg Materials (Germany)

- Stora Enso (Finland)

- Mondi (U.K.)

- Smurfit Westrock (Ireland)

- International Paper (U.S.)

- BASF (Germany)

KEY INDUSTRY DEVELOPMENTS

- November 2025: SSAB entered into a partnership with EAB to supply fossil-free steel, including SSAB Zero, for use in warehouse fittings, doors, and steel buildings. The partnership supports wider industrial adoption of low-emission steel in building and infrastructure-related applications.

- October 2025: Heidelberg Materials started delivering evoZero, its carbon-captured near-zero cement, to customers across Europe. The product is based on carbon capture technology at the company’s Brevik CCS facility in Norway and is targeted at construction projects seeking verified low-carbon cement solutions.

- September 2025: Hydro expanded its Hydro CIRCAL recycled aluminum portfolio to include foundry alloys. The product maintains a minimum of 75% post-consumer scrap content and enables automotive customers to use recycled aluminum in wheels, battery boxes, structural parts, and engine components.

- July 2025: CRH announced an agreement to acquire Eco Material Technologies for approximately USD 2.10 billion. Eco Material is a leading North American supplier of supplementary cementitious materials, including fly ash, pozzolans, synthetic gypsum, and green cement. The acquisition is intended to strengthen CRH’s position in low-carbon cementitious materials and support rising demand for sustainable infrastructure and concrete solutions.

- April 2025: Stora Enso launched Performa Nova, a next-generation high-yield folding boxboard for consumer packaging. The product is designed for renewable, recyclable, and resource-efficient packaging applications across dry, frozen, chilled food, chocolate, and confectionery segments, following the start-up of the company’s consumer board line in Oulu, Finland.

REPORT COVERAGE

The global sustainable materials market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Market Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, End Use, and Region |

| By Product Type |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 471.00 billion in 2025 and is projected to reach USD 1,090.89 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 207.24 billion.

Recording a CAGR of 9.8%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The building & construction end use segment led the market.

Regulatory push for circular economy and rising consumer demand for eco-friendly products are expected to drive market growth.

ArcelorMittal, Holcim, Stora Enso, BASF, and Lenzing are the top players in the market.

Asia Pacific held the highest market share.

Momentum towards recycled and low-carbon material inputs across industrial value chains is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us