Swarm Drone Market Size, Share & Industry Analysis, By Control/Coordination (Leader-Follower Swarm, Centralized Control Swarm, Decentralized AI Swarm, and Hybrid Swarm), By Platform (Fixed-Wing Swarm, Rotary Wing Swarm, and Hybrid VTOL Swarm), By Mission Type (Surveillance & Reconnaissance, Combat/Offensive, Electronic Warfare (EW), Logistics & Supply, and Entertainment, Agriculture, and Inspection), By Operation Mode (Pre-Programmed, Adaptive/AI-Driven, and Fully Autonomous Collaborative), By Payload (Electronic Warfare, Kinetic/Strike, & Others), By End User, and Regional Forecast, 2026-2034

Swarm Drone Market Size

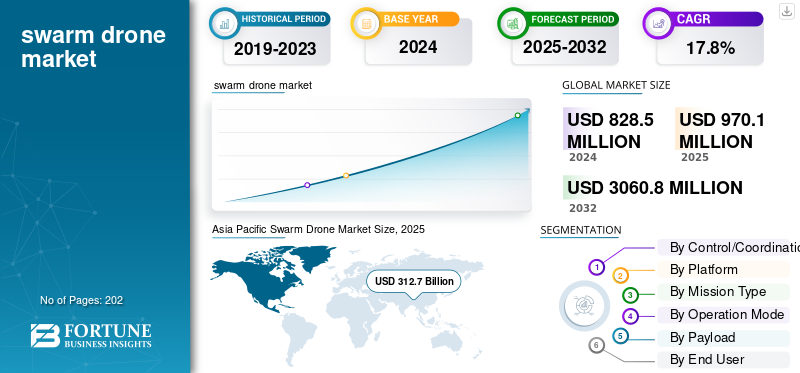

The global swarm drone market size was valued at USD 970.1 million in 2025 an is projected to grow from USD 1148.2 million in 2026 to USD 3,898.40 million by 2034, exhibiting a CAGR of 16.50% during the forecast period. Asia Pacific dominated the swarm drone market with a market share of 38.10% in 2025.

Swarm drones are groups of unmanned aerial vehicles (UAVs) that work together using artificial intelligence, machine learning, autonomous control, and real-time communication to carry out complex tasks such as surveillance, combat, and logistics efficiently. The market includes the global development and use of these multi-drone systems in both defense and commercial sectors. Market growth is driven by improvements in artificial intelligence, machine learning, and autonomy, defense modernization programs, cost-effective scalability, and the increasing use of drones in areas such as infrastructure monitoring, agriculture, and disaster response. Growing geopolitical tensions and government funding for autonomous technologies are speeding up market growth through 2032.

Furthermore, the market encompasses several key market players with General Atomics Aeronautical Systems, Northrop Grumman, Elbit Systems, and Israel Aerospace Industries (IAI) at the forefront. These companies are investing in AI-powered autonomy, communication networks, and improved payload integration to boost swarm coordination and mission flexibility.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rapid Advances in Autonomous AI and Decision-Making Capability Fueling Market Growth

Increasing development and use of autonomous artificial intelligence (AI) and onboard decision-making abilities in drone technology are driving the market growth. These advancements allow drones to work together, adjust, and complete missions with minimum human interaction. This shift encourages defense and commercial users to choose swarm systems over traditional single-vehicle or remote-controlled designs. Better AI makes swarms more resilient, enabling them to cope with communication loss or countermeasures. It also makes them scalable and cost-effective, which opens up more use cases and speeds up investment.

- For example, in January 2025, Firestorm Labs secured a USD 100 million Indefinite Delivery/Indefinite Quantity (IDIQ) contract from the U.S. Air Force to develop and integrate small unmanned aerial systems (UAS) with advanced autonomy features, including swarm capabilities.

MARKET RESTRAINTS

Communication, Coordination, and Reliability Challenges Hinder Swarm Deployment

Achieving strong, low-latency, secure communication, and coordination between drones in real-world, contested environments is hindering the swarm drone market growth. For a swarm to operate well, each drone technology must continuously share sensor data, positional information, and mission commands with others. However, issues such as signal interference, limited bandwidth, latency delays, packet loss, and network congestion can cause drones to fall out of sync or struggle to respond to changing conditions. Additionally, the complex algorithms for formation control, collision avoidance, fault tolerance, and task allocation must work reliably even when individual drones malfunction or lose connection; these constraints push current communication and control systems to their limits.

- For instance, in May 2024, during “The Sound of Blooming Flowers” drone light show at the Sky Theatre in Shanghai, hundreds of drones malfunctioned mid-performance due to technical synchronization errors. Several drones fell from the sky, caught fire, and caused panic among spectators, highlighting the critical need for more reliable communication links and fail-safe systems in swarm operations.

MARKET OPPORTUNITIES:

Rising Demand for Spectacular Public Events and Eco-Friendly Entertainment Creates New Revenue Streams

The growing demand for large drone light shows and aerial performances as alternatives to traditional fireworks and large LED screens. Cities, event planners, and brands want safer, environmentally friendly, and visually appealing displays. Swarm drone systems can provide synchronized, 3D visual experiences over land and water that draw large crowds and create excitement. This trend opens up new revenue channels in entertainment, tourism, advertising, cultural festivals, and civic celebrations, especially in urban areas with strict emissions or noise rules.

- For example, in April 2025, Ho Chi Minh City in Vietnam hosted a record-breaking drone light show with 10,518 synchronized drones, organized by DAMODA, to celebrate the 50th anniversary of the Liberation of the South. This event showed how large drone swarms can be scaled for major celebrations and highlighted the strong commercial potential for providers of swarm based aerial entertainment.

SWARM DRONE MARKET TRENDS:

Growing Use of Containerized and Rapid-Deployment Swarm Launch Systems are Market Trends

A major trend in the swarm drone area is the development of containerized launch platforms. These platforms can deploy large numbers of drones quickly and with minimal infrastructure. The “drone in a box” systems cut down on setup time and simplify logistics. They also make swarm shows or tactical drone operations more scalable and flexible.

- For example, in October 2025, the Chinese company DAMODA unveiled a containerized system capable of launching and recovering hundreds of quadcopter drones within minutes, with synchronized takeoff and landing. This platform was initially designed for entertainment light shows, but it has military applications.

MARKET CHALLENGES:

Authentication, Handover & Scalability in Communication Networks Poses Challenges in Market Growth

The technical challenge limiting swarm deployment is ensuring secure, low-latency authentication, and smooth handover of drones in mobile networks. This is important for large or dynamic swarms. Traditional cellular or 5G authentication protocols do not work well when dozens or hundreds of drones need to join, leave, or move between communication nodes. We need swarm based or swarm-level authentication schemes, but these are still being developed and face issues with security, latency, and synchronization.

Impact of Russia Ukraine War

Russia-Ukraine War Significantly Speed up Development and Use of Swarm Drone Technologies

The conflict has shown the tactical benefits of coordinated UAV operations for reconnaissance, electronic warfare, and precision strikes. It highlights how low-cost, semi-autonomous groups of drones can overwhelm traditional defenses. Both sides have increasingly tried coordinated drone attacks and loitering munitions. This has pushed militaries globally to invest in AI-driven swarm capabilities, counter-swarm defense systems, and software for planning missions. This real-world testing has pushed defense agencies and manufacturers around the globe to prioritize swarm drone research and development, making the war a key market driver of rapid market growth and technological innovation.

- For instance, in June 2025, Ukraine carried out Operation Spiderweb, in which 117 drones were launched deep inside Russian territory from mobile containers and struck five Russian air bases, reportedly damaging over 20 military aircraft.

Download Free sample to learn more about this report.

Segmentation Analysis

By Platform

Rotary-Wing Swarm Segment Dominated in 2024 Due to Operational Flexibility and Vertical Mobility

In terms of platform, the market is categorized into fixed-wing swarm, rotary wing swarm, and hybrid VTOL swarm.

The rotary wing swarm segment led the market accounting for 44.53% market share in 2026. This is due to its more maneuverability, ability to take off and land vertically, capability to hover, and suitability for dense urban, ISR, and tactical missions. This makes them ideal for tasks such as surveillance, infrastructure inspection, disaster response, urban reconnaissance, and military operations close to the ground resulting in dominance of rotary-wing swarm drones.

- For example, in April 2024, Kraus Hamdani Aerospace won a contract to provide the U.S. Navy’s first solar-electric VTOL unmanned aerial system, the K1000ULE, within the Group-2 VTOL category. This system allows a single operator to control a swarm of rotary or VTOL craft across different missions.

The hybrid segment market is expected to grow at a fastest CAGR of 20.0% over the forecast period.

By Control/Coordination

On the basis of the market segmentation of by control/coordination, the market is classified into leader-follower swarm, centralized control swarm, decentralized AI swarm, and hybrid swarm.

The decentralized AI swarm segment is projecteed to dominate the markt with a share of 32.08% in 2026. Dominance is attributed to its better scalability, autonomy, and resilience in changing or contested environments. The rising focus on AI-driven autonomy, multi-agent reinforcement learning, and self-organizing systems has made decentralized setups popular for defense and large-scale commercial uses.

- For instance, in November 2024, the U.S. Defense Advanced Research Projects Agency (DARPA) successfully carried out a field demonstration under its OFFSET (Offensive Swarm-Enabled Tactics) program. This event showcased more than 125 autonomous drones working under decentralized AI control for complex urban reconnaissance and target engagement missions.

To know how our report can help streamline your business, Speak to Analyst

By Mission Type

Surveillance & Reconnaissance Segment Dominates Market Due to Rising Demand for Real-Time Intelligence and Battlefield Awareness

Based on mission type, the market is segmented into surveillance & reconnaissance, combat/offensive, electronic warfare (EW), logistics & supply, and entertainment, agriculture, and inspection.

The Surveillance and Reconnaissance (S&R) segment will account for 44.21% market share in 2026. This growth is fueled by the ongoing need for continuous intelligence, target tracking, battlefield awareness, and maritime monitoring. Swarm-enabled surveillance systems can efficiently cover large areas compared to single drones. The necessity of real-time situational awareness in today’s conflicts and security operations means that S&R missions are important for drone investments resulting in dominance of S&R segment under mission type.

For example, in November 2024, Poland signed a contract worth USD 24.5 million with WB Electronics to buy 52 FlyEye surveillance drones, aiming to enhance its reconnaissance and imagery intelligence capabilities along its borders.

The segment of combat/offensive is growing at a CAGR of 19.5% across the forecast period.

By Operation Mode

Pre-Programmed Segment Dominated Market Due to Operational Maturity and Regulatory Acceptance

Based on operation mode, the market is segmented into pre-programmed, adaptive/AI-driven,

and fully autonomous collaborative.

The pre-programmed autonomy segment is anticipated to hold a dominant market share of 59.48% in 2026. This dominance is attributed to its proven reliability, easier certification, and lower operational risk compared to adaptive or fully autonomous systems. Most deployed swarm systems, especially those used for entertainment, basic surveillance, and training missions, rely on pre-defined flight paths and mission scripts instead of AI-based decision-making. Defense forces and commercial operators still prefer pre-programmed systems as they make mission planning easier and reduce the risk of unpredictable autonomous behavior.

The segment of adaptive/AI-driven is set to flourish with a growth rate of 20.4% across the forecast period.

By Payload

ISR Payload Segment Dominates Market Due to Growing Demand for Real-Time Surveillance and Intelligence Collection

Based on payload, the market is segmented into kinetic/strike, electronic warfare, ISR, logistics, and sensor/environmental.

The intelligence, surveillance, and reconnaissance (ISR) payload segment leads the global market. This growth is driven by the increasing need for ongoing situational awareness, border monitoring, and battlefield intelligence. ISR payloads, such as electro-optical/infrared (EO/IR) sensors, high-resolution cameras, and synthetic aperture radar (SAR), are crucial. They enable swarm drones to collect, process, and transmit important data in real time. As defense agencies and security forces focus on data-driven operations, ISR-equipped swarms serve as the foundation for most active swarm deployments globally.

The segment of kinetic/strike is set to flourish with a growth rate of 19.6% across the swarm drone market forecast period

By End User

Military Segment Dominates Market Due to Expanding Defense Modernization and Tactical Deployment of Swarm Systems

In terms of end user, the market is segmented into military and commercial.

Military segment leads the global swarm drone market in 2024. This is due to the fast integration of autonomous and semi-autonomous swarm systems in defense strategies around the globe. These drones can overpower defenses, improve situational awareness, and lower human risk. Defense modernization programs in the U.S., China, India, Turkey, and Europe prioritize swarm-capable UAVs for tactical and strategic advantages. The growing demand for low-cost, scalable, and smart systems has made swarm drones a key part of modern warfare concepts.

For example, in September 2024, the U.S. Air Force awarded Kratos Defense & Security Solutions a contract to expand its Collaborative Combat Aircraft initiative. This initiative focuses on swarm-enabled autonomous systems that can function alongside manned fighters.

The segment of commercial is set to grow at a CAGR of 19.4% across the forecast period.

Swarm Drone Market Regional Outlook

Asia Pacific Swarm Drone Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific Dominates Global Market Due to Rapid Defense Modernization and Indigenous Development Initiatives

By region, the market is categorized into Europe, North America, Asia Pacific, Middle East, and the rest of the world.

Asia Pacific

Asia Pacific accounted for USD 369.73 Million in 2025, representing 38.11% of the global market share, and is projected to reach USD 441.91 Million in 2026. This is due to extensive government-supported research and development programs, increasing defense budgets, and a greater focus on autonomous and AI-enabled warfare systems. Countries such as China, India, and South Korea are at the forefront of swarm drone innovation. They use local manufacturing resources and AI expertise to create affordable and scalable systems for surveillance, combat, and electronic warfare.

North America

Other regions such as North America, Europe, and the Middle East are expected to witness significant growth in the market in the coming years. The North America market generated USD 290.1 Million in 2025, representing 29.90% of the global market landscape, and is expected to reach USD 343.13 Million in 2026. This growth is mainly due to increased investment in Unmanned Aerial Vehicles for military use. Based on these factors, countries such as the U.S. expect to reach a valuation of USD 302.48 million, and Canada is set to reach USD 33.8 million by 2025.

Europe

Europe contributed 24.85% to the global market in 2025, with a valuation of USD 241.04 Million, and is projected to reach USD 283.1 Million in 2026, making it the third-largest region in the market. In this region, both the U.K. and France are expected to reach USD 49.5 million and USD 46.0 million, respectively, in 2025.

Rest of the World

In 2025, the Rest of the World market stood at USD 69.23 Million, representing 7.14% of global demand, and is projected to grow to USD 80.09 Million in 2026. Over the forecast period, the rest of the world (Middle East & Africa and Latin America) are expected to experience moderate market growth. Especially the UAE and Turkey, is becoming a significant adopter. They are integrating swarm drones for border surveillance and unique operations through companies such as EDGE Group and Baykar.

COMPETITIVE LANDSCAPE

Key Industry Players:

Asia Pacific Companies Strengthen Dominance While Global Defense Giants Drive Technological Leadership

The competitive landscape of the market structures strong involvement from Asia Pacific defense manufacturers and Western technology companies, each offering unique strengths to the ecosystem. This region’s leadership is driven by rapid innovation, local production, and large defense programs, especially from China, India, and South Korea.

Meanwhile, the U.S. and European countries maintain their edge in advanced China), Baykar (Turkey), IAI and Elbit Systems (Israel), Kratos Defense & Security Solutions (U.S.), General Atomics (U.S.), and Leonardo (Italy) lead the development of swarm-enabled UAV platforms. AI autonomy and communication technologies. Key players such as AVIC (They focus on AI-driven coordination, combat applications, and cooperation between manned and unmanned systems.

In the commercial and dual-use sectors, companies such as Anduril Industries, Edge Group/ADASI (UAE), BotLab Dynamics (India), TEKEVER (Portugal), Primoco UAV (Czech Republic), and DZYNE Technologies (U.S.) are combining military-grade autonomy with scalable civilian uses. These include surveillance, monitoring infrastructure, and aerial displays.

Strategically, the competitive environment is changing. There is a shift toward collaborative research and development, joint ventures, and open system design. This approach promotes cooperation among allied nations.

LIST OF KEY SWARM DRONES COMPANIES PROFILED:

- Kratos Defense & Security Solutions, Inc. (U.S.)

- General Atomics Aeronautical Systems, Inc. (U.S.)

- Anduril Industries (U.S.)

- AeroVironment, Inc. (U.S.)

- DZYNE Technologies, LLC (U.S.)

- Leonardo S.p.A. (Italy)

- Thales Group (France)

- Airbus Defence and Space (France/Germany)

- TEKEVER Ltd. (Portugal)

- Primoco UAV SE (Czech Republic)

- China Aerospace Science and Technology Corporation (CASC) (China)

- Aviation Industry Corporation of China (AVIC) (China)

- China Electronics Technology Group Corporation (CETC) (China)

- NewSpace Research & Technologies Pvt. Ltd. (India)

- Baykar Technologies (Turkey)

- EDGE Group / ADASI (United Arab Emirates)

- Lentatek Space Aviation and Technology Inc. (Turkey)

- Denel Dynamics (South Africa)

- Sistemas Integrados de Monitoreo (SIMA) (Brazil)

- ZALA Aero (Russia)

KEY INDUSTRY DEVELOPMENTS:

- In July 2024, Baykar Technologies (Turkey) initiated swarm integration testing for its Bayraktar TB3 UAV, focusing on distributed reconnaissance and cooperative target-sharing capabilities across multiple platforms.

- In May 2024, EDGE Group/ADASI (UAE) unveiled its REACH-S UAV, a modular medium-altitude platform engineered for networked and swarm-enabled operations, enhancing the UAE’s indigenous defense technology portfolio.

- In April 2024, China Electronics Technology Group Corporation (CETC) conducted a swarm flight of more than 200 UAVs, testing AI-based cooperative algorithms for intelligence, surveillance, and electronic warfare applications.

- In February 2024, India’s Defence Research and Development Organization (DRDO) and NewSpace Research & Technologies conducted a large-scale 75-drone swarm demonstration capable of coordinated surveillance and precision strikes, marking a major milestone in India’s indigenous swarming technology program.

- In January 2024, the U.S. Air Force Research Laboratory (AFRL) advanced its “Golden Horde” networked weapon program, which successfully demonstrated collaborative communication between multiple unmanned munitions during live-fire testing.

REPORT COVERAGE:

The global swarm drone market analysis provides an in-depth study of market size; company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation:

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forcast Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.50% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation

|

By Control/Coordination

By Platform

By Mission Type

By Operation Mode

By Payload

By End User

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 970.1 million in 2025 and is projected to reach USD 3,898.4 million by 2034.

In 2025, the market value stood at USD 970.1 million.

The market is expected to exhibit a CAGR of 16.5% during the forecast period (2026–2034).

The rotary wing swarm segment led the market by platform.

Rapid advances in autonomous AI and decision-making capability fueling growth.

Kratos Defense & Security Solutions, Inc., AeroVironment, Inc., General Atomics Aeronautical Systems, Baykar Teknoloji, Leonardo S.p.A, Aviation Industry Corporation of China, EDGE Group/ADASI, and China Aerospace Science and Technology Corporation are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 202

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us