Therapeutic Albumin Market Size, Share & Industry Analysis, By Source (Human and Others), By Indication (Hypovolemia, Hypoalbuminemia, Burn, and Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

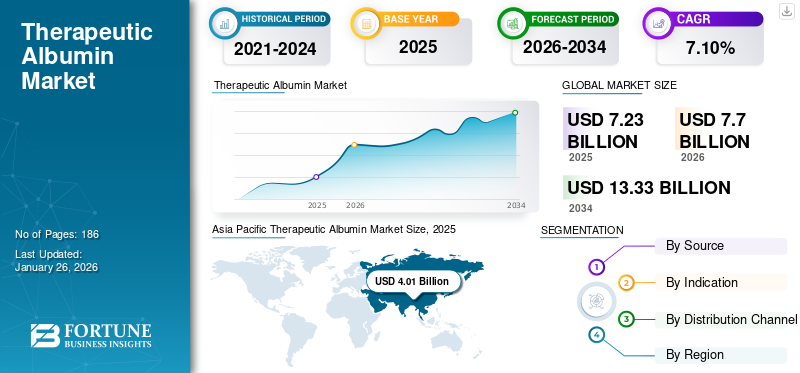

The global therapeutic albumin market size was valued at USD 7.23 billion in 2025. The market is projected to grow from USD 7.70 billion in 2026 to USD 13.33 billion in 2034 at a CAGR of 7.10% during the forecast period. Asia Pacific dominated the therapeutic albumin market with a market share of 55.49% in 2025.

Therapeutic albumin is a sterile, purified protein primarily derived from human blood plasma. It is widely used in the treatment of hypovolemia, burns, hypoalbuminemia, acute liver failure, and shock. Its functions include maintaining oncotic pressure and transporting hormones, enzymes, and drugs. Albumin is a naturally occurring protein that plays a crucial role in maintaining oncotic pressure and transporting various substances in the bloodstream.

The global therapeutic albumin market is witnessing significant growth due to the increasing incidence of trauma and life-threatening critical illnesses, which has led to the higher demand for these products in emergency care settings.

- For instance, in April 2024, as per the data published by the Centers for Disease Control and Prevention, an estimated 6.0 million people in the U.S. were diagnosed with kidney diseases, and 4.5 million people were diagnosed with chronic liver diseases. Such a large population affected by these chronic conditions increases the demand for therapeutic albumin products and thus propels market growth.

However, the market faces challenges due to its reliance on human-derived albumin, such as limited supply, risk of pathogen transmission, and batch variability. Consequently, there is a growing demand for recombinant or advanced albumin products that offer enhanced safety, consistency, and scalability. Additionally, advancements in albumin production and purification technologies are likely to improve its availability and efficacy, thereby supporting market expansion.

Key players in the market, such as Grifols, S.A., Kedrion S.p.A., and Octapharma AG, offer a range of products in multiple concentrations, tailored to meet the needs of patients with various chronic conditions. Additionally, the increasing development of technologically advanced albumin formations are further boosting the company's share in the market.

Download Free sample to learn more about this report.

Global Therapeutic Albumin Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 7.23 billion

- 2026 Market Size: USD 7.70 billion

- 2034 Forecast Market Size: USD 13.33 billion

- CAGR: 7.10% from 2026–2034

Market Share:

- Region: Asia Pacific dominated the market with a 55.49% share in 2025. The region's growth is driven by the rising incidence of burn cases and the high prevalence of chronic diseases, which are boosting the demand for therapeutic albumin products.

- By Indication: The Burn segment is expected to hold a dominant market share. This is attributed to the high number of burn cases globally and the increasing demand for albumin to manage fluid loss in these critical patients.

Key Country Highlights:

- Japan: As a key country in the dominant Asia Pacific region, Japan's market is propelled by a rising prevalence of chronic diseases and an increasing number of burn cases, which drives the demand for therapeutic albumin.

- United States: The market is fueled by a large patient population with chronic conditions, with an estimated 6.0 million people diagnosed with kidney disease and 4.5 million with chronic liver disease. The country also sees a significant number of severe burn injuries, with 32,540 cases requiring inpatient hospitalization in 2023.

- China: Growth is supported by a large and growing patient population with chronic illnesses. The market is also benefiting from increased product availability, as exemplified by the National Institutes for Food and Drug Control's (NIFDC) approval for the commercial release of new human albumin products.

- Europe: The market is advanced by a strong focus on research and clinical trials from major players. Positive results from studies such as Grifols' PRECIOSA Phase 3 trial, which demonstrated improved survival in patients with decompensated cirrhosis, are boosting the clinical applications and demand for albumin.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Incidence of Chronic Diseases and Burns to propel Market Growth

The rising incidence of chronic diseases such as liver disorders, kidney diseases, and cancer that often require albumin for effective treatment and management is a key factor driving significant growth in the therapeutic albumin market. Additionally, an increase in burn cases has heightened the demand for albumin, particularly for fluid resuscitation and wound healing. As healthcare systems globally focus on improving patient outcomes and managing complex conditions, the therapeutic applications of albumin become increasingly vital.

Overall, the growing burden of chronic illnesses and acute injuries underscores the critical role of therapeutic albumin in modern medicine.

- For instance, in 2024, according to the American Burn Association Annual Burn Injury Summary Report, 32,540 burn cases injuries in 2023 required inpatient hospitalization at specialized burn centers, including 7,674 burns cases involving additional trauma injuries. Such a large number of patients affected with severe burn injuries increases the demand for therapeutic albumin for fluid restoration, thus driving the global therapeutic albumin market growth.

MARKET RESTRAINTS

Production and Supply Chain Disruption to Hamper Market Growth

The complex nature of producing human-derived albumin involves several complex steps, beginning with blood donation from voluntary donors. This step is inherently limited by the availability of donors, leading to potential supply shortages. After collection, the blood must undergo rigorous purification and sterilization to ensure the safety and efficacy of the albumin produced. Moreover, any decline in donor numbers further hinders the availability of blood plasma needed for albumin extraction, thus limiting the growth of the market.

- For instance, in January 2024, the American Red Cross declared an emergency blood shortage, reporting around a 40.0% fall in blood donations. These factors combined lead to complexities in the supply chain for human-derived albumin, affecting its availability for medical use.

MARKET OPPORTUNITIES

Rising Application of Albumin in Regenerative Medicine and Cell Therapy to Promote Market Growth

Rising research and development activities focused on incorporating albumin into regenerative medicine and cell therapy are creating significant growth opportunities for the therapeutic albumin market. Albumin's unique properties, including its biocompatibility, ability to stabilize proteins, and role as a carrier for various therapeutic agents, make it an invaluable component in tissue engineering and cell culture systems. It enhances the viability and efficacy of stem cells and other cellular therapies.

Furthermore, strategic activities by key market players to expand their research capabilities in developing innovative regenerative medicine using therapeutic albumin are further contributing to market growth.

- For instance, in March 2023, Albumedix Ltd, in collaboration with Heartseed Inc, announced the use of Recombumin, a high-quality, animal and human-origin-free recombinant human albumin as an important component of Heartseed's HS-001. HS-001 is an investigational cardiac remuscularization cell therapy. Such research activities for the expanded application of albumin are expected to propel market growth during the forecast period.

MARKET CHALLENGES

Regulatory Hurdles and Cost Constraints to Challenge Market Growth

The therapeutic albumin market faces significant challenges due to regulatory hurdles. Stringent approval processes from agencies such as the U.S. FDA, EMA, and NMPA slow down product launches and require strict adherence to good manufacturing practices and pharmacopeia standards.

Additionally, the high costs associated with manufacturing and sourcing plasma proteins make production expensive, posing barriers for companies. Developing economies particularly struggle to access affordable therapeutic albumin, further limiting its widespread availability.

THERAPEUTIC ALBUMIN MARKET TRENDS

Increasing Clinical Studies to Develop Recombinant Albumin for Therapeutic Applications

The rising demand for albumin to treat various medical conditions, including accidents, serious burn injuries, and others requiring blood volume restoration and fluid replacement, has led to increased pressure for frequent albumin production. However, the limited supply of human serum albumin due to reliance on whole blood or donated human plasma, along with contamination risks associated with plasma-derived Human Serum Albumin (HAS), limiting efforts to fulfill the growing demand.

To combat these situations, several biotechnology companies are continuously involved in research activities to develop recombinant albumin using recombinant DNA technology. This is aimed to overcome the limitations of plasma-derived HSA, such as supply and quality inconsistencies, which are swiftly shifting the global therapeutic albumin market trends.

- For instance, in August 2024, Shilpa Medicare Limited announced the successful completion of Phase 1 clinical trial for sRbumin, a recombinant human albumin 20% (rHA). sRbumin is derived from yeast and is a highly purified, structurally and functionally equivalent alternative to human serum albumin. Such advancements underscore the potential of recombinant human albumin as a viable alternative to plasma-derived has, addressing critical gaps in healthcare.

Download Free sample to learn more about this report.

IMPACT of COVID-19

The COVID-19 pandemic negatively impacted the global market. Disruption in the supply chain and interruption in plasma collection centers due to stringent guidelines hampered market growth during this period. Moreover, limited patient visits to hospitals and a shift of healthcare focus toward the COVID-19 patients eventually impeded the adoption of the products in the market.

SEGMENTATION ANALYSIS

By Source

New Product Launches and Product Approvals to Boost Human Segment's Growth

Based on source, the market is divided into human and others. The human segment is expected to hold the dominant global therapeutic albumin market share of 65.17%% in 2026. The dominance of the segment is due to the rising prevalence of chronic diseases and the presence of key players in the market with robust product offerings of human albumin. Additionally, increasing number of regulatory approvals for new human albumin products in different concentrations further boost growth in the segment.

- For instance, in November 2021, Grifols, S.A. launched ALBUTEIN FlexBag (Albumin [Human] USP) in 5.0% and 25.0% concentrations. This product is indicated for hypovolemia, cardiopulmonary bypass procedures, neonatal hyperbilirubinemia, acute nephrosis, hypoalbuminemia, ovarian hyperstimulation syndrome, the segment's Adult Respiratory Distress Syndrome (ARDS).

The others segment is expected to grow with a moderate CAGR during the forecast period. The growth of the segment is due to a shortage of human blood for producing albumin and increasing risk of blood transfusion-related diseases. Such challenges have increased the demand for albumin derived from other sources. Additionally, increasing research and development activities by key biotechnology companies to launch albumin products is expected to propel the segment's growth during the forecast period.

- For instance, in April 2025, Healthgen Biotechnology developed a technology to synthesize Human Serum Albumin (HSA) from rice, offering a potential solution to the ongoing supply shortage of this critical blood protein. Such advancements are expected to increase the supply and support continued market growth.

By Indication

Rising Burn Incidences to Boost Segment Growth

Based on indication, this market is classified into hypovolemia, hypoalbuminemia, burn, and others.

The burn segment is expected to hold a dominant portion of the market due to the rising number of burn cases and increasing demand for albumin to maintain fluid loss in such conditions, contributing market share 89.66% globally in 2026

- For instance, in October 2023, according to the World Health Organization (WHO), an estimated 6.6 million thermal burn injuries were recorded each year worldwide.

- In addition to this, in November 2024, according to the data published by the Directorate General of Health Services, India, under the National Program for Prevention & Management of Trauma and Burn, the annual burn incidence in India is estimated to be 6.0 to 7.0 million per year.

- The high incidence is attributed to factors such as illiteracy, poverty, and low-level safety consciousness among the population.

The large number of burn and trauma injuries significantly increases the demand for therapeutic albumin to maintain and restore the fluid volume of the body and thus boost the segment's growth in the market.

The hypovolemia segment is expected to grow at a substantial CAGR during the forecast period, driven by the rising number of cases leading to low extracellular fluid volume, which can result from conditions such as extreme perspiration, vomiting, diarrhea, and chronic conditions such as congestive heart failure or kidney failure. These conditions increase the demand for therapeutic albumin in fluid resuscitation in patients and thus are expected to boost the segment growth in the market.

The hypoalbuminemia and others segment is expected to grow with a moderate CAGR during the forecast period. The rising number of acute and chronic conditions such as nephrotic syndrome, hepatic cirrhosis, heart failure, and malnutrition leading to hypoalbuminemia are key drivers. Additionally, increasing approvals and product launches of albumin solutions for therapeutic uses in turn, boost the segment's growth during the forecast period.

- For instance, in May 2020, Bio Products Laboratory (BPL) launched ALBUMINEX 5% (human albumin) and ALBUMINEX 25% (human albumin) solutions for injection in the U.S., which are used for the treatment of hypovolemia, ascites, hypoalbuminemia (including cases resulting from burns), acute nephrosis, Acute Respiratory Distress Syndrome (ARDS), and cardiopulmonary bypass.

By Distribution Channel

Increasing Number of Surgical Procedures to Boost the Hospital Pharmacies Segment

Based on distribution channel, the global market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies.

The hospital pharmacies segment is expected to dominate the distribution channel segment with a share of 54.56% in 2026. The increasing shift of patients with chronic conditions and burn cases toward hospital-based treatment is expected to boost the distribution of these products through hospital pharmacies. Additionally, the growing number of surgical procedures in hospital settings contributes to a growing demand for albumin and thus promotes the growth of the segment.

- For instance, in November 2024, according to the data published in the Journal of Cardiothoracic and Vascular Anesthesia, a study examining the use of albumin among adults undergoing thoracic surgery in the U.S. from 2011-2017 found that albumin was used in 170 of 342 hospitals. Among the patients studied, 13.0% and 7.0% of 14,672 and 22,532 patients, respectively, underwent open and minimally invasive thoracic surgery. Such a large number of hospitals adopting albumin during surgeries is expected to boost its distribution through these channels.

The retail pharmacy segment is expected to hold a considerable share of the market owing to the widespread accessibility of retail locations and proper storage facilities. This convenience enables patients to obtain the product closer to home.

The online pharmacies segment is expected to grow with the highest CAGR during the forecast period. This growth is fueled by increasing adoption of digital platforms, the convenience of home delivery, and expanding internet penetration.

THERAPEUTIC ALBUMIN MARKET REGIONAL OUTLOOK

On the basis of region, the global market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Therapeutic Albumin Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific represented USD 4.01 billion, accounting for 55.49% of the worldwide market, and is projected to grow to USD 4.33 billion in 2026. The rising incidence of burn cases and the prevalence of chronic diseases in the region are the prominent factors boosting the demand for these products. Additionally, the presence of major players in the market, with a focus on expanding its product offerings, is promoting market growth in the region. The Japan market is projected to reach USD 0.85 billion by 2026, the China market is projected to reach USD 1.86 billion by 2026, and the India market is projected to reach USD 0.46 billion by 2026.

- For instance, in July 2023, Kedrion S.p.A announced that China's National Institutes for Food and Drug Control (NIFDC) approved BPL's human Albumin product for commercial release in the Chinese market.

North America

The North America market accounted for USD 1.57 billion in 2025, representing 21.71% of the global industry, and is expected to reach USD 1.66 billion in 2026. The rising prevalence of chronic diseases, strong presence of plasma donation centers, and well-established presence of key players with advanced production facilities to manufacture plasma based products such as therapeutic albumin to propel market growth in the region. The U.S. market is projected to reach USD 1.52 billion by 2026.

- For instance, in January 2022, Grifols, S.A. acquired Prometic Plasma Resources Inc. (PPR) from Kedrion in Canada with an aim to expand the availability of lifesaving plasma medicines in the country.

U.S.

The U.S. dominated the North American region owing to the increasing demand for plasma-based products and the presence of key biopharmaceutical companies with advanced facilities in the country.

- For instance, in February 2025, Octapharma AG inaugurated a new manufacturing site in Vienna to meet the rising demand for human plasma-based medicine.

Europe

Europe recorded a market size of USD 1.03 billion in 2025, capturing 14.22% of the global market share, and is projected to reach USD 1.08 billion in 2026. Europe held the second-largest share of the market due to the presence of key players in the market and their increased research and development activities and clinical trials to launch new products. The UK market is projected to reach USD 0.18 billion by 2026, while the Germany market is projected to reach USD 0.28 billion by 2026.

- In December 2024, Grifols, S.A. announced positive topline results from its PRECIOSA Phase 3 trial, which investigated long-term use of Albutein (human albumin USP) in patients with decompensated cirrhosis and ascites. The study found that patients receiving Albutein 20% alongside standard medical treatment experienced improved transplant-free survival, reduced mortality, and fewer disease-related complications.

Latin America and the Middle East & Africa

Middle East & Africa contributed 2.73% to the global market in 2025, with a valuation of USD 0.2 billion, and is projected to reach USD 0.2 billion in 2026. The Latin America market was valued at USD 0.42 billion in 2025, capturing 5.85% of global revenue, and is estimated to reach USD 0.44 billion in 2026. Latin America and the Middle East & Africa are projected to hold the smaller market share during the forecast period. The rising prevalence of chronic diseases and increasing demand for albumin products are expected to boost the region's growth in the market.

Furthermore, increasing focus of key companies toward receiving approvals for their new blood collection centers is likely to boost the manufacturing and supply of these products in the region.

- For instance, in July 2023, Grifols, S.A. announced that its Egypt-based plasma donation center received quality certification from the Plasma Protein Therapeutics Association (PPTA) International Quality Plasma Program (IQPP). This certification ensures adherence to the highest standards in plasma-protein therapeutics, which are used to treat life-threatening and chronic conditions. Such approvals are expected to boost the production of therapeutic albumin and thus propel market growth in the region.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Major Players Focus on Research Activities to Maintain their Position in the Market

The market exhibits a consolidated structure, with key players such as Grifols, S.A., Octapharma AG, and Kedrion S.p.A., accounting for a substantial share in 2024. These companies maintain their dominant positions through robust product offerings and strategic activities, such as acquisitions and collaborations aimed at strengthening global reach.

- For instance, in October 2022, Grifols, S.A. announced the inauguration of a new albumin purification and filling plant at its Dublin manufacturing hub. The new plant significantly aimed to increase the annual production capacity of ALBUTEIN FlexBag, a flexible container used for storing and administering albumin treatments. This move underscores the company’s commitment to scaling up production and meeting rising global demand.

Other key market contributors include Takeda Pharmaceutical Company Limited, LFB, and China Biologic Products Holdings, Inc. These companies are investing in research and development, with a focus on new product launches to increase their respective market share during the forecast period.

LIST OF KEY THERAPEUTIC ALBUMIN COMPANIES PROFILED

- Takeda Pharmaceutical Company Limited. (Japan)

- CSL (Australia)

- Grifols, S.A. (Spain)

- Octapharma AG (Switzerland)

- Kedrion S.p.A. (Italy)

- Biotest AG (Germany)

- LFB (France)

- China Biologic Products Holdings, Inc. (China)

- Baxter (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Shilpa Medicare Limited announced that its wholly owned subsidiary, Shilpa Pharma Lifesciences, has successfully completed a U.S. Food and Drug Administration (FDA) inspection of its Unit-2 facility in Raichur, India, with no Form 483 observations.

- December 2022: CSL announced the opening of a new plasma fractionation facility in Australia. This plasma fractionation facility can treat immune system problems, hemophilia, burns, and other life-threatening medical conditions.

- December 2022: Kedrion S.p.A. acquired UNICAplasma s.r.o and UNICAplasma Morava s.r.o. with an aim to operate five plasma collection centers in the Czech Republic. This acquisition supports the company’s goal of securing high-quality plasma for our production of plasma-derived therapies targeting rare and debilitating conditions.

- April 2021: CSL collaborated with Terumo Blood and Cell Technologies to deploy a new plasma collection platform across CSL Plasma U.S. collection centers.

- March 2019: Takeda Pharmaceutical Company Limited received U.S. FDA approval for a new plasma manufacturing facility in Georgia. The facility supports the production of FLEXBUMIN 25% [Albumin (Human)], USP, 25% human albumin solution used in critical medical treatments.

REPORT COVERAGE

The global therapeutic albumin market research report provides a detailed industry analysis, focusing on key aspects, such as an overview of advanced products and prevalence of key diseases in key countries. Additionally, the report highlights key industry developments such as mergers, partnerships, acquisitions, and new product launches. Besides these, it also offers insights into regional dynamics, emerging market trends and growth opportunities. Furthermore, the report comprises a detailed pipeline analysis and the impact of COVID-19 on the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.10% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Source

|

|

By Indication

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 7.23 billion in 2025 and is projected to reach USD 13.33 billion by 2034.

In 2025, market value in Asia Pacific stood at USD 4.01billion.

Registering a CAGR of 7.10%, the market will exhibit steady growth during the forecast period (2026-2034).

Based on source, the human segment is expected to lead this market during the forecast period.

The rising prevalence of chronic diseases and burn cases is the major factor driving the growth of the market.

CSL, and Octapharma AG are some of the major players in the global market.

Asia Pacific is expected to dominate the market.

The increasing research and development activities to modify the sources for albumin production to fulfill the rising demand are expected to drive the adoption of product.

- 2021-2034

- 2025

- 2021-2024

- 186

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us