Thin Wall Packaging Market Size, Share & Industry Analysis, By Material (Polypropylene (PP), Polyethylene (PE), Polyethylene terephthalate (PET), and Others), By Product Type (Tubs & Cups, Trays & Clamshells, Lids, and Others), By Application (Food, Beverages, Electricals & Electronics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

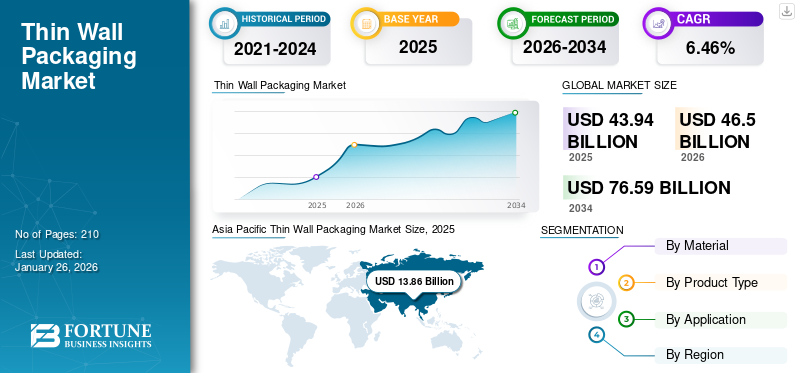

The global thin wall packaging market size was valued at USD 43.94 billion in 2025 and is projected to be worth USD 46.5 billion in 2026 and reach USD 76.59 billion by 2034, exhibiting a CAGR of 6.46% during the forecast period. Asia Pacific dominated the thin wall packaging market with a market share of 31.53% in 2025.

Thin wall packaging is a packaging solution that is utilized as a replacement for glass & cans for packaging several items, including meat, food preserves, and others. The rapidly growing demand for such packaging, as they protect food from physical damage & contamination during transportation, is the major factor driving the market growth. There is a significant push toward eco-friendly packaging solutions, with businesses adopting materials that are recyclable or biodegradable to meet consumer preferences and regulatory requirements.

Berry Global Inc. and Dahl-Tech, Inc. are the leading manufacturers, accounting for the largest market share.

Download Free sample to learn more about this report.

THIN WALL PACKAGING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 43.94 Billion

- 2026 Market Size: USD 46.50 Billion

- 2034 Forecast Market Size: USD 76.59 Billion

- CAGR: 6.46% from 2026–2034

- Asia Pacific dominated the thin wall packaging market with a 31.53% share in 2025.

- The polypropylene (PP) segment is projected to account for 50.52% of the market in 2026.

- The food segment is expected to hold 43.38% of the market in 2026.

Asia Pacific

Asia Pacific reached USD 13.86 billion in 2025, accounting for 31.53% of global market revenue.

North America

North America was valued at USD 10.80 billion in 2025, representing 24.58% of the global market.

Europe

Europe generated USD 8.80 billion in 2025, contributing 20.02% of global revenue.

U.S.

The market is projected to reach USD 9.22 billion by 2026.

Japan

The market is projected to reach USD 2.80 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Significant Benefits Offered by Thin Wall Packaging Drives Market Growth

Thin wall packaging uses less material, which not only reduces production costs but also minimizes environmental impact by lowering the amount of plastic or other materials needed for packaging. As less material is required and the packaging is lighter, manufacturers can benefit from lower raw material costs and reduced energy consumption during production. The packaging allows for better visibility of the product inside, as the material is usually more transparent. It can thus be appealing to consumers who want to see the product before purchasing.

Modern thin wall packages have higher material strength and durability through advanced material science. Some thin wall designs are enhanced with features, such as ribbing or reinforcing structures, making them durable despite their lightweight nature. Lightweight and ergonomic packaging can make it easier for consumers to handle and use products. For instance, thinner plastic bottles are easier to carry, and thinner containers often stack more efficiently.

Increasing Adoption of Thin-Wall Packages from the Food and Beverages Sector Enhances the Market Growth

Thin-wall packages significantly reduces the overall weight of food products, lowering transportation costs and facilitating easier handling. Thin walled cups, trays, and containers are commonly used for yogurt, puddings, and cheese. These materials help preserve freshness and extend shelf life. Pre-packaged meals often utilize thin wall containers for cost-effective, efficient, and lightweight packaging. These containers are lightweight and are designed for both microwave reheating and preservation.

Thin walled trays are used for packaging fresh fruits and vegetables, providing protection while minimizing the weight and environmental impact. Thin wall bottles and cups, particularly used for juices, milk, and smoothies, are both convenient and cost-effective. Thin packaging is essential in maintaining adequate protection against physical damage, contamination, and environmental factors, extending shelf life. Henceforth, the increasing demand for packaging from the food and beverage sector drives market growth.

MARKET RESTRAINTS

Material Performance and High Manufacturing Costs to Impede Market Growth

Thin-wall packaging is more prone to cracking, puncturing, and deformation than thicker alternatives, especially during transportation and handling. Thin materials may not withstand high pressure or external forces, leading to damage that compromises product safety. Moreover, the packaging materials may offer less protection against moisture, air, light, and other environmental factors, which can affect the shelf life of the product. The materials used for thin-wall packaging, such as advanced polymers, may be more expensive than traditional packaging materials, which can increase production costs, thus hindering thin wall packaging market growth.

MARKET OPPORTUNITIES

Growing Demand for Convenient and Sustainable Packaging Will Generate Growth Opportunities

Thin-wall packaging is often associated with lightweight, easy-to-handle products, which appeals to consumers looking for convenience in packaging, especially for single-serve or on-the-go products. As online shopping continues to rise, manufacturers are looking for packaging solutions that protect products while minimizing weight and bulk for shipping. Thin-wall packaging fits this need well, offering secure, space-efficient solutions.

In addition, the packaging uses less material, which directly reduces the environmental footprint by minimizing plastic consumption, waste, and the carbon footprint of production. Many thin wall materials, such as plastics and polymers, are recyclable, aligning with the growing demand for eco-friendly packaging solutions in response to stricter environmental regulations and consumer preferences, offering potential growth opportunities.

MARKET CHALLENGES

Regulatory and Compliance Issues Challenges Market Growth

Stringent environmental regulations regarding plastic usage and disposal pose challenges for the thin-wall packaging industry, necessitating compliance and adaptation to sustainable practices. Thinner packaging materials must meet stringent regulations for food-grade packaging, which can be more challenging to achieve.

Moreover, rising pressure on manufacturers to comply with sustainability-focused regulations may require redesigning thin wall solutions and incorporating recyclable and biodegradable materials. Henceforth, the regulatory and compliance issues challenge market growth.

Download Free sample to learn more about this report.

THIN WALL PACKAGING MARKET TRENDS

Advancements in Material Science and Innovations in Packaging Design a Prominent Trend

Ongoing innovations in material science have led to the development of high-performance, lightweight materials with improved barrier properties, enhancing product protection and extending shelf life. Companies are investing in the development of new materials, such as biodegradable plastics and enhanced barrier polymers, to meet sustainability goals and improve product performance. These advanced materials allow for thinner walls while maintaining the required strength and barrier properties, opening new markets for thin-wall packaging in more sensitive sectors, such as pharmaceuticals, food, and electronics.

- Asia Pacific witnessed a thin wall packaging market growth from USD 12.18 billion in 2023 to USD 12.99 billion in 2024.

The use of bioplastics, compostable polymers, and bio-based resins is gaining momentum, aligning with global sustainability. Additionally, the integration of features such as easy-to-open lids, tamper-proof seals, or child-resistant designs is increasing. It allows manufacturers to cater the needs of safety, convenience, and product integrity. These factors are emerging as a key trend to the market growth.

IMPACT OF COVID-19

The COVID-19 pandemic positively impacted the supply chain, thus boosting the market. However, the massive growth of online food delivery services had a positive impact on the market growth. The rising demand for ready-to-eat meals and food items lead to rapid market growth during the pandemic.

SEGMENTATION ANALYSIS

By Material

Increasing Demand from the Food Sector Drives the Polypropylene (PP) Segment Growth

Based on the material, the market is segmented into polypropylene (PP), polyethylene (PE), polyethylene terephthalate (PET), and others.

The Polypropylene (PP) segment led the market accounting for 50.52% market share in 2026 as it is widely used in thin wall packages due to its lightweight and cost-effective properties. The material is an ideal food-safe plastic for production processes that need high heat. Polypropylene is recyclable, which contributes to the eco-friendly nature of thin walled packaging. Thin walled packaging is lightweight and portable, making it ideal for storing and transporting food, and as PP is a strong, durable material, it is safe for microwave use. The rising utilization of polypropylene for food packaging boosts segmental growth.

Polyethylene terephthalate will experience steady growth in the forthcoming years. The material is easy to separate and is widely recyclable. Products packed with such materials are lightweight but durable and are perfect for several dairy packaging products, further leading to segmental growth.

By Product Type

Tubs & Cups Lead the Market as They are Lightweight and Easy to Handle & Transport

Based on product type, the market is categorized into tubs & cups, trays & clamshells, lids, and others.

The Tubs & cups segment is projected to dominate the market with a share of 47.51% in 2026. Their lightweight nature makes them easy to handle and transport. Their durability ensures they withstand the rigors of daily usage, and their versatility enhances their functionality. Tubs & cups also offer excellent clarity for better appearance & product recognition, which, in turn, thrives the segment’s growth.

Trays & clamshells are the second-leading product type segment and are estimated to witness significant growth over the forecast period. Rising demand for lightweight packaging solutions is a key factor influencing the segment’s growth. Moreover, its increasing usage in food, beverages, and other industries also propels rapid growth.

By Application

To know how our report can help streamline your business, Speak to Analyst

Versatile and Durable Properties Boost the Demand for Thin Walled Packaging in the Food Sector

Based on application, the market is classified into food, beverages, electricals & electronics, and others.

The food segment held the largest thin wall packaging market share in 2026. Thin wall packages comes in many shapes and sizes and can be used for a variety of foods, including dairy, frozen, fruits, vegetables, bakery items, frozen foods, ready meals, juices, soups, and meats. Thin packaging is strong and tough to impact and can be microwave-safe. The rising consumer demand for pre-packaged food items or food products that are easy to carry is a major factor boosting the segment’s growth. Moreover, the online food delivery trend is also a prime factor studied to bolster the growth of food applications. The food segment is expected to account for 43.38% of the market in 2026.

The beverages segment is a rapidly growing application in the market. Thin walled packaging is a lightweight, cost-effective, and sustainable packaging solution that is becoming increasingly popular in the beverage industry as it uses less material, decreases transportation costs, and minimizes carbon emissions, thus contributing to the segment’s growth.

THIN WALL PACKAGING MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific Thin Wall Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Well-established Consumer Electronic, Food and Beverages, and E-Commerce Industries Boost Market Growth in Asia Pacific

Asia Pacific

In 2025, the Asia Pacific market stood at USD 13.86 billion, representing 31.53% of global demand, and is projected to grow to USD 14.8 billion in 2026. Asia Pacific is the dominating region of the global market due to the expansion of the food and beverage industry and increasing consumer demand for packaged goods. Rapid growth in the e-commerce sector, food & beverage industries, and consumer electronic sectors enhance the demand for thin wall trays, lids, and containers, further aiding regional growth. The Japan market is valued at USD 2.8 billion by 2026, the China market is valued at USD 4.85 billion by 2026, and the India market is valued at USD 4.01 billion by 2026.

- According to the Ministry of Industry and Information Technology, China ranks first worldwide in the production and sales of consumer electronics owing to the country's enhanced innovation and brand-building capacity. The user penetration in China's consumer electronics market is estimated to be 56.6% in 2024.

Increasing Food Delivery Trends Drive the North American Market Growth

North America

The market in North America reached USD 10.8 billion in 2025, representing 24.58% of total market revenue, and is expected to reach USD 11.44 billion in 2026. North America is the second-dominating region and holds a significant market share. The ongoing food delivery and rising demand for ready-to-eat meals in the region majorly contribute to regional growth. The U.S. market is valued at USD 9.22 billion by 2026.

- According to a recent report on food delivery and online ordering statistics, 60% of consumers in America order takeout and delivery at least once a week, with online ordering increasing 300% faster than dining. DoorDash has boomed as the most popular food delivery app in the U.S., with a 67% market share. Uber Eats is the second-most popular food delivery app, with a 23% market share.

Growing Pharmaceutical Exports Enhances Europe’s Market Growth

Europe

Europe contributed approximately USD 8.8 billion to the global market in 2025, accounting for 20.02% share, and is expected to reach USD 9.28 billion in 2026. Europe is the third-largest contributor to the market. Rising demand for cost-effective, sustainable, and customized products in the region contributes to market growth. The usage of thin walled packaging products in the pharmaceutical industries and the growing export of pharmaceutical products enhance regional growth. The UK market is valued at USD 1.7 billion by 2026, while the Germany market is valued at USD 2.01 billion by 2026.

- According to the Observatory of Economic Complexity, in 2023, the world exports of pharmaceutical products exceeded USD 805 billion. The major exporters of pharmaceutical products were Germany (USD 125 Billion) and Switzerland (USD 93.8 Billion).

Rising Demand from Food and Beverages Sector Drives Market Growth in Latin America

Latin America

The Latin America market accounted for USD 6.12 billion in 2025, representing 13.92% of the global industry, and is expected to reach USD 6.42 billion in 2026. The Latin America region will experience steady growth in the projected period. As more people live in urban areas and seek convenience, the demand for ready-to-eat meals, snack foods, and other packaged products has increased, further fueling the need for thin-wall packaging.

- According to the National Library of Medicine, Brazil witnessed a significant increase in the group of alcoholic beverages (29%), flavored juices (11%), caloric soft drinks (8%), milk and milk substitutes (6%), and fruit juices (5%).

Increasing Utilization in Cosmetics and Pharmaceutical Sector Aids Market Growth in Middle East & Africa

Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 4.37 billion in 2025, accounting for 9.94% share, and is expected to reach USD 4.57 billion in 2026. The Middle East & Africa market is projected to experience moderate growth during the forecast period. Thin-wall packaging is increasingly being used in the pharmaceutical and cosmetics industries for items such as pill bottles, cosmetic containers, and single-dose packaging. The rising imports of generic drugs and the growing pharmaceutical sector also drive market growth.

- The Convention on Pharmaceutical Ingredients states that the Saudi pharmaceutical market is the largest in the region. Currently, Saudi Arabia imports over 81% of the generic drugs consumed locally, creating a large scope for reducing import dependency.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Market Participants to Witness Significant Growth Opportunities with New Product Launches

The market is highly fragmented and competitive. A few significant players are dominating the market by offering innovative packaging solutions in the packaging industry. These major market players constantly focus on expanding their customer base across regions by innovating their existing wide range of products. The major developments by the key manufacturers will flourish the market expansion.

Major players in the industry include Berry Global Inc., Dahl-Tech, Inc., BEWI, Otto Männer GmbH, Mold-Tek Packaging, and Greiner Packaging International. Numerous other companies operating in the market are focused on market scenarios and delivering advanced packaging solutions.

List of Key Thin Wall Packaging Companies Profiled:

- Berry Global Inc. (U.S.)

- Dahl-Tech, Inc. (U.S.)

- BEWI (Norway)

- Otto Männer GmbH (Germany)

- Mold-Tek Packaging (India)

- Greiner Packaging International (Austria)

- PACCOR (Germany)

- Groupe Guillin (France)

- Takween Advanced Industries (Saudi Arabia)

- Plastipak Industries Inc. (U.S.)

- Double H Plastics, Inc. (U.S.)

- Dampack International B.V. (Netherlands)

- Insta Polypack (India)

- Weiss (India)

- Elsepack (China)

KEY INDUSTRY DEVELOPMENTS

- In November 2023, ITC Packaging worked with BMB SPA and Novapet to launch TWI-PET. The new technology develops thin walls and flexible PET packaging in a one-step injection molded process. Containers developed with TWI-PET feature IML decoration with labels designed with PET or PP, which are both recyclable.

- In October 2023, Netstal launched a lightweight ICM thin wall cup designed with 100 % PP at Fakuma. The thin wall packaging is optimized for the circular economy utilizing the injection compression molding process. The packaging is produced in 4 cavities at a cycle time of 2.7 seconds in an Elion 1750 with a hybrid injection unit and is majorly suitable for dairy products.

- In March 2023, Haitian International and Haitian Smart Solutions launched PET thin walled packaging solutions to support the packaging industry in solving the issues of thin walled PET, such as poor fluidity, easy crystallization, molding problems, and white spots.

- In October 2021, Wendy's announced a collaboration with packaging and plastics industry leaders LyondellBasell and Berry Global to help advance the sustainable goal of sourcing 100% of its customer-facing packaging. The collaboration supports Wendy's selection of plastic-lined paper cups with restricted recyclability to single-substrate.

- In May 2021, SABIC, a global leader in the chemical industry, declared the launch of its collaboration with KraussMaffei High Performance AG at the partner’s Thin Wall Packaging Application Center in Näfels, Switzerland. It is the site of KraussMaffei's Swiss subsidiary & producer of high-performance injection molding systems known under the NETSTAL brand.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The market will witness astonishing growth with the growing collaborations, mergers, and investments. These initiatives help in increasing the importance of thin wall product packaging. In August 2023, TC Transcontinental Packaging declared an investment of USD 60 million for the development of cutting-edge, mono-material, and recyclable flexible plastic packaging solutions, offering high-performance polyethylene films with additional heat resistance.

REPORT COVERAGE

The market research report provides a detailed market analysis. The market overview also focuses on key aspects, such as top key players, competitive landscape, product/service types, market segments, Porter’s five forces analysis, and leading segments of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market intelligence & growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope and Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.46% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Product Type

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 43.94 billion in 2025.

The market is likely to grow at a CAGR of 6.46% over the forecast period.

The food application segment is leading in the market.

The market size of Asia Pacific stood at USD 13.86 billion in 2025.

The key market drivers are significant benefits offered by thin wall packaging and increasing utilization from the food and beverages sector.

Some of the top players in the market are Berry Global Inc., Dahl-Tech, Inc., BEWI, Otto Männer GmbH, Mold-Tek Packaging, and Greiner Packaging International.

The global market size is expected to reach USD 76.59 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us