Third Generation Energy Sources Market Size, Share & Industry Analysis, By Technology Type (Hydrogen Energy Systems, Advanced Nuclear Energy, Advanced Renewable Technologies, Third-Generation Bioenergy, Ocean Energy Technologies, and Others), By Application (Power Generation, Industrial Energy Use, Transportation, and Others), By End User (Utilities & Power Generation Companies, Industrial Sector, Oil & Gas, Transportation & Logistics, and Others), Regional Forecast, 2026-2034

Third Generation Energy Sources Market Size and Future Outlook

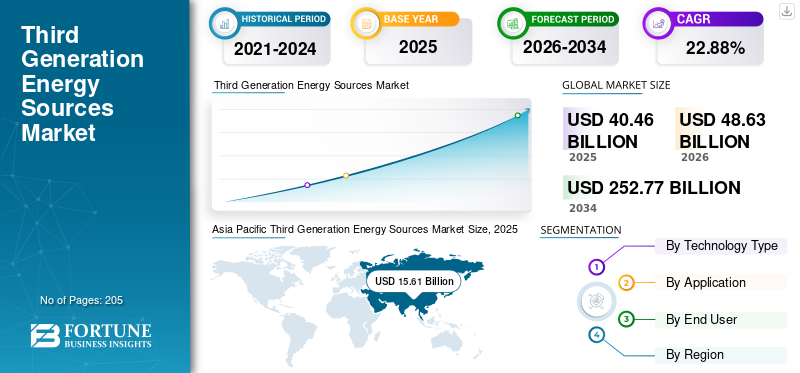

The global third generation energy sources market size was valued at USD 40.46 billion in 2025. The market is projected to grow from USD 48.63 billion in 2026 to USD 252.77 billion by 2034, exhibiting a CAGR of 22.88% during the forecast period. Asia Pacific dominated the third generation energy sources market with a market share of 38.58% in 2025.

Third generation energy sources represent the next wave of clean energy technologies designed to deliver high efficiency, low emissions, and long-term sustainability beyond conventional fossil fuels and earlier renewable systems. These include green hydrogen, advanced nuclear technologies such as small modular reactors (SMRs), advanced solar materials such as perovskites, enhanced geothermal systems, and emerging solutions such as ocean energy and synthetic fuels. According to the International Energy Agency (IEA), the International Renewable Energy Agency (IRENA), and the European Union (EU), these technologies are critical to achieving global net-zero targets, particularly in hard-to-abate sectors such as heavy industry, aviation, and shipping. Wind energy supports third-generation energy systems by providing renewable electricity for green hydrogen production and integration with advanced energy technologies.

A major factor driving the market is the accelerating push for decarbonization and energy security, supported by government policies, innovation funding, and cross-sector collaborations. Initiatives such as the Hydrogen Council’s global roadmap and Generation IV International Forum (GIF) highlight growing investments in scalable, low-carbon solutions. Additionally, increasing electrification, rising energy demand, and the need for resilient energy systems are further driving the adoption of these advanced energy technologies worldwide, particularly among utility-scale solutions.

- For instance, in November 2023, the Generation IV International Forum (GIF) announced progress in advancing next-generation nuclear reactor technologies, including molten salt and fast neutron reactors, aimed at improving safety, efficiency, and waste reduction. The initiative, supported by multiple member countries, focuses on accelerating commercialization timelines for advanced nuclear systems. This development reflects the growing global commitment toward deploying third-generation and beyond energy technologies to support long-term decarbonization and reliable baseload power generation.

Some of the leading companies operating in the industry include Air Liquide, Linde plc, Siemens Energy AG, and Plug Power Inc. Air Liquide is a global leader in industrial gases and a key player in the market, with a strong focus on hydrogen production, storage, and distribution technologies. The company is actively advancing low-carbon and green hydrogen solutions to support energy transition, particularly across industrial decarbonization and clean mobility applications.

Download Free sample to learn more about this report.

THIRD GENERATION ENERGY SOURCES MARKET TRENDS

Rising Integration of Hydrogen with Advanced Energy Systems Across Various Sectors is the Key Market Trend

A key trend shaping the third generation energy sources market is the increasing integration of hydrogen with advanced energy systems across power, industry, and transportation sectors. Organizations such as the International Energy Agency (IEA) and the Hydrogen Council highlight that hydrogen is emerging as a central energy carrier, particularly for decarbonizing hard-to-abate industries such as steel, chemicals, and heavy transport. This is driving the development of large-scale hydrogen hubs, electrolyzer deployments, and cross-border supply chains.

At the same time, there is a growing convergence between advanced nuclear, renewable energy, and hydrogen production, where technologies such as small modular reactors (SMRs) and renewable-powered electrolysis are being combined to ensure a stable and continuous clean energy supply. Additionally, innovations in energy storage, synthetic fuels, and power-to-X solutions are enhancing system flexibility and enabling better grid balancing.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Strong Policy Support and Decarbonization Mandates to Drive Industry Growth

The third generation energy sources market growth is primarily driven by stringent decarbonization targets and strong policy support from governments and global organizations. Agencies such as the International Energy Agency (IEA) and International Renewable Energy Agency (IRENA) emphasize that advanced technologies such as hydrogen, advanced nuclear, and next-generation renewables are essential to achieve net-zero emissions. Governments are actively introducing funding programs, regulatory frameworks, and national strategies to accelerate deployment. Additionally, the residential and commercial segments contribute to third-generation energy adoption through distributed clean energy systems, hydrogen-based heating, and advanced decentralized power solutions.

For instance, in August 2022, the U.S. Department of Energy (DOE) launched major funding initiatives for clean hydrogen hubs to scale production and infrastructure. Similarly, in July 2020, the European Commission introduced its Hydrogen Strategy for a Climate-Neutral Europe, targeting large-scale hydrogen adoption across industries. In addition, the Generation IV International Forum (GIF) has been promoting advanced nuclear development through international collaboration, with ongoing technological updates reported in 2023.

MARKET RESTRAINTS

High Capital Costs and Varying Levels of Technology Maturity to Hamper Market Demand

The adoption of third generation energy sources is restrained by high capital investment requirements and varying levels of technological maturity, which limit large-scale commercialization. Advanced technologies such as green hydrogen, SMRs, and ocean energy systems require significant upfront investment in infrastructure, R&D, and deployment.

According to the International Energy Agency (IEA), in September 2023, the cost of electrolyzers and hydrogen infrastructure remains a key barrier to scaling clean hydrogen projects globally. Similarly, the International Atomic Energy Agency (IAEA) highlighted in June 2022 that advanced nuclear technologies, including SMRs, face challenges related to licensing, regulatory approvals, and long development timelines.

MARKET OPPORTUNITIES

Expansion of the Hydrogen Economy and Cross-Sector Integration to Create Market Opportunities

The third generation energy sources market presents significant opportunities through the rapid expansion of the global hydrogen economy and increasing cross-sector integration of clean energy systems. For instance, in January 2023, the Hydrogen Council emphasized the growing pipeline of large-scale hydrogen projects, including export-oriented hubs in regions such as the Middle East, Australia, and Latin America.

In addition, the integration of advanced nuclear with hydrogen production and renewable energy systems is creating new business models, particularly for continuous clean power supply and grid stability. In June 2023, the International Energy Agency (IEA) noted that combining nuclear and renewables with hydrogen production can significantly enhance energy system flexibility and efficiency. These developments are opening up opportunities across industrial decarbonization, synthetic fuels, and long-duration energy storage.

MARKET CHALLENGES

Infrastructure Gaps and Supply Chain Limitations

A major challenge in the market is the lack of adequate infrastructure and underdeveloped supply chains, which hinder large-scale deployment and commercialization. Technologies such as hydrogen and advanced fuels require extensive infrastructure for production, storage, transportation, and distribution, which is still in early stages globally. In October 2023, the International Energy Agency (IEA) noted that limited hydrogen pipeline networks and storage facilities remain critical bottlenecks for market expansion.

Similarly, advanced nuclear and emerging technologies face challenges related to component manufacturing, skilled workforce availability, and regulatory standardization. In April 2022, the International Atomic Energy Agency (IAEA) emphasized that supply chain readiness and licensing frameworks are key barriers to faster deployment of advanced reactors.

Segmentation Analysis

By Technology Type

Hydrogen Energy Systems Segment Led, Driven by their Ability to Decarbonize Multiple Sectors

Based on technology type, the market is classified into hydrogen energy systems, advanced nuclear energy, advanced renewable technologies, third-generation bioenergy, ocean energy technologies, and others.

In 2025, the hydrogen energy systems dominated the market, accounting for 40.59% share. This growth is due to their ability to decarbonize multiple sectors simultaneously, including industry, transportation, and power generation. Unlike other technologies, hydrogen serves as both an energy carrier and storage medium, enabling integration with renewable and nuclear energy systems.

The advanced renewable technologies segment is expected to grow at a CAGR of 23.52% during the study period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Power Generation Segment Dominated Due to Large-Scale Energy Demand

Based on application, the market is classified into power generation, industrial energy use, transportation, and others.

In 2025, the power generation segment dominated the market, accounting for 45.41% share. This growth is due to its large-scale energy demand and central role in electricity systems. Advanced technologies such as small modular reactors (SMRs), advanced solar, and geothermal systems are primarily deployed for grid-scale power production, ensuring a reliable and continuous energy supply. In addition, integration with hydrogen production and energy storage enhances grid stability and flexibility.

The industrial energy use segment is expected to grow at a CAGR of 24.22% during the study period.

By End User

Utilities & Power Generation Companies Segment Dominated Due to Ownership of Large-Scale Energy Infrastructure

On the basis of end user, the market is classified into utilities & power generation companies, industrial sector, oil & gas, transportation & logistics, and others.

In 2025, the utilities & power generation segment dominated the global market with 36.61% share. The growth is driven by the ownership of large-scale energy infrastructure and strong investment capabilities. These entities are responsible for developing, operating, and maintaining energy assets, enabling them to adopt advanced technologies at scale. Their access to long-term financing, regulatory support, and established grid networks allows faster integration of emerging energy solutions.

The oil & gas segment is expected to grow at a CAGR of 23.57% during the study period.

Third Generation Energy Sources Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Third Generation Energy Sources Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific reached USD 15.61 billion in 2025, securing the largest third generation energy sources market share. In the region, India was valued at USD 1.53 billion in 2025. The region is a major hub for the product, driven by large-scale investments, policy support, and growing demand from the industrial sector. Countries such as China, Japan, South Korea, and India are actively advancing hydrogen production, advanced nuclear technologies, and next-generation renewable systems.

India Third Generation Energy Sources Market

The Indian market in 2025 stood at around USD 1.53 billion, accounting for roughly 3.78% of global revenues. India is rapidly emerging in the market through its National Green Hydrogen Mission, targeting large-scale production and industrial adoption. The country is also exploring advanced energy technologies to reduce import dependence and support long-term decarbonization goals.

China Third Generation Energy Sources Market

China’s market is projected to be significant worldwide, with 2025 revenues standing at around USD 6.66 billion, representing roughly 16.46% of the global market.

Japan Third Generation Energy Sources Market

The Japanese market in 2025 stood at around USD 2.47 billion, accounting for roughly 6.10% of global revenues.

North America

In 2025, the North American market was valued at USD 8.72 billion and continues to maintain a significant share in 2026, reaching USD 10.34 billion. Region’s growth is primarily driven by developed economies, strong federal funding mechanisms, and commercialization-focused programs, particularly in the U.S. The U.S. Department of Energy (DOE) has accelerated deployment through initiatives such as hydrogen hubs and advanced reactor demonstration programs, enabling faster scaling of technologies such as SMRs and clean hydrogen. Additionally, tax incentives and production credits under federal legislation are improving project economics for hydrogen production and advanced energy systems.

U.S. Third Generation Energy Sources Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market stood at around USD 7.14 billion in 2025, accounting for roughly 17.64% of the global market sales.

Europe

Europe is projected to record a growth rate of 22.15% in the coming years, which is the second-highest among all regions. The region reached a valuation of USD 11.31 billion in 2025. Europe’s growth in third generation energy sources is driven by binding decarbonization targets and structured hydrogen deployment frameworks at the regional level. The European Commission’s hydrogen strategy and REPowerEU plan are accelerating investments in electrolyzer capacity, cross-border hydrogen infrastructure, and industrial decarbonization projects. Countries such as Germany and the Netherlands are advancing import-oriented hydrogen corridors and port-based distribution networks, particularly through hubs such as Rotterdam.

Germany Third Generation Energy Sources Market

Germany’s market in 2025 reached around USD 3.46 billion 2025 and is estimated to reach around USD 4.20 billion by 2026, representing roughly 8.55% of the global revenues. Germany is a key leader in the market, driven by its strong focus on green hydrogen adoption and industrial decarbonization. The country is actively developing large-scale hydrogen import networks and domestic electrolyzer capacity to support sectors such as steel and chemicals. Additionally, Germany’s policy framework and funding programs are accelerating the commercialization of advanced energy technologies.

Latin America

The Latin American market reached a valuation of USD 2.61 billion in 2025 and is expected to witness moderate growth in this market during the forecast period. The growth is driven by abundant renewable resources and strong potential for low-cost green hydrogen production and exports.

Brazil Third Generation Energy Sources Market

Brazil's market reached around USD 1.12 billion in 2025, representing roughly 2.76% of the global market.

Middle East & Africa

The Middle East & Africa region is expected to witness significant growth in this market during the forecast period. The Middle East & Africa market reached a valuation of USD 2.21 billion in 2025, driven by large-scale green hydrogen and ammonia projects, particularly in the GCC region.

GCC Third Generation Energy Sources Market

The GCC market reached around USD 1.26 billion in 2025, representing roughly 3.11% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Major players are Focusing on Strengthening their Partnerships to Increase Their Global Market Share

The global third generation energy sources market holds a consolidated market structure, constituting prominent players such as Air Liquide, Linde plc, Siemens Energy AG, and Plug Power Inc. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in March 2024, Air Liquide announced the development of a large-scale renewable hydrogen production facility in Normandy, France, aimed at supporting industrial decarbonization. The project integrates electrolyzer technology powered by renewable electricity to supply low-carbon hydrogen to nearby industrial clusters. This initiative reflects the company’s strategy to scale hydrogen infrastructure and accelerate the transition toward sustainable energy systems across Europe.

Other key players in the global market include Nel ASA, Bloom Energy Corporation, and NuScale Power Corporation. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY THIRD GENERATION ENERGY SOURCES COMPANIES PROFILED

- Air Liquide (France)

- Linde plc (Ireland)

- Siemens Energy AG (Germany)

- Plug Power Inc. (U.S.)

- Nel ASA (Norway)

- Bloom Energy Corporation (U.S.)

- NuScale Power Corporation (U.S.)

- Rolls-Royce SMR Ltd. (U.K.)

- First Solar, Inc. (U.S.)

- Enel S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS

- January 2024: Plug Power commissioned a green hydrogen production plant in Georgia, U.S., utilizing renewable energy-powered electrolysis. The facility is part of the company’s broader plan to establish a nationwide hydrogen network for mobility and industrial use. This development reinforces Plug Power’s commitment to scaling hydrogen infrastructure and advancing clean energy adoption.

- October 2023: Linde plc signed an agreement to build and operate a clean hydrogen production facility in Texas, U.S., utilizing advanced technologies for low-carbon hydrogen supply. The project is designed to serve industrial customers while supporting broader energy transition goals. Linde’s involvement highlights its role in expanding hydrogen infrastructure and enabling large-scale adoption of next-generation energy solutions.

- September 2023: Nel ASA received an order to supply alkaline electrolyzer equipment for a large-scale hydrogen project in Europe, supporting renewable hydrogen production. The project focuses on decarbonizing industrial processes by integrating hydrogen as a clean energy carrier. This contract highlights Nel’s role in enabling the expansion of hydrogen production capacity globally.

- June 2023: Siemens Energy partnered with Air Products to develop a gigawatt-scale electrolyzer manufacturing facility in Berlin, Germany. The facility aims to accelerate the production of electrolyzers required for green hydrogen projects across Europe. This initiative strengthens Siemens Energy’s position in hydrogen technology and supports the scaling of advanced energy systems for industrial and energy applications.

- May 2023: Bloom Energy deployed its solid oxide electrolyzer technology for a hydrogen project in the U.S., aimed at producing efficient green hydrogen for industrial applications. The technology offers higher efficiency compared to conventional electrolysis, supporting cost-effective hydrogen production. This initiative underscores Bloom Energy’s innovation in advanced energy systems.

REPORT COVERAGE

The global third generation energy sources market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.88% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology Type, Application, End User, and Region |

| By Technology Type |

|

| By Application |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 40.46 billion in 2025 and is projected to reach USD 252.77 billion by 2034.

In 2025, the market value stood at USD 15.61 billion.

The market is expected to exhibit a CAGR of 22.88% during the forecast period.

The hydrogen energy systems segment led the market by technology type.

Strong policy support is the key factor driving the market.

Air Liquide, Linde plc, and Siemens Energy AG are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us