Trailer Telematics Market Size, Share & Industry Analysis, By Trailer Type (Dry Van Trailers, Refrigerated (Reefer) Trailers, Flatbed Trailers, and Tanker Trailers), By Component (Hardware, Software, and Services), By Application (Trailer Tracking & Location Monitoring, Cargo & Condition Monitoring, Asset Utilization & Fleet Management, and Security & Theft Prevention), By Connectivity Technology (Cellular (4G/5G, LTE-M, NB-IoT), Satellite, LPWAN (LoRa, Sigfox), and RFID & Short-Range Communication), and Regional Forecast, 2026-2034

Trailer Telematics Market Size and Future Outlook

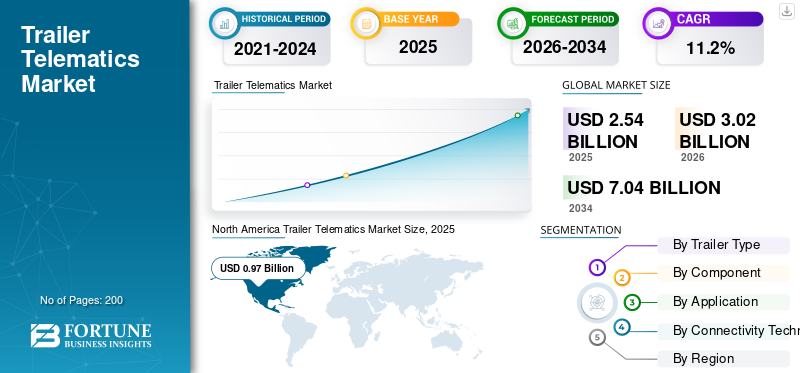

The global trailer telematics market size was valued at USD 2.54 billion in 2025. The market is projected to grow from USD 3.02 billion in 2026 to USD 7.04 billion by 2034, with a CAGR of 11.2% over the forecast period. North America dominated the trailer telematics market with a market share of 38.19% in 2025.

Trailer telematics tags are identification and sensing devices attached to trailers or trailer assets to enable tracking, monitoring, and data capture. These tags may include RFID tags, Bluetooth beacons, GPS-linked identifiers, or sensor-enabled smart tags that help fleet operators monitor trailer location, cargo status, movement, and asset utilization across logistics and transportation operations. The market is driven by rising demand for real-time trailer visibility, better fleet utilization, cargo security, and predictive maintenance. Growth in cold-chain logistics, stricter compliance requirements, and increasing adoption of connected fleet technologies also support demand. Fleet operators are investing in telematics to reduce downtime, optimize routing, improve trailer turnaround, and enhance operational efficiency across long-haul and regional transportation networks.

Major players in the market include Samsara, Geotab, ORBCOMM, Verizon Connect, Trimble, Phillips Connect, Schmitz Cargobull, ZF, and CalAmp. The current trend among these companies is toward integrated smart-trailer platforms, OEM-installed telematics, cloud-based fleet analytics, reefer and cargo monitoring, and subscription-led service models with advanced connectivity features.

Download Free sample to learn more about this report.

Trailer Telematics Market Key Takeaways

- 2025 Market Size: USD 2.54 billion

- 2026 Market Size: USD 3.02 billion

- 2034 Forecast Market Size: USD 7.04 billion

- CAGR: 11.2% from 2026–2034

- North America dominated the trailer telematics market with a 38.19% share in 2025.

- The LPWAN (LoRa, Sigfox) segment is projected to grow at the fastest CAGR of 16.6% during the forecast period.

- The software segment is anticipated to expand at a CAGR of 14.3% over the study period.

North America

North America led the global market in 2025, supported by advanced logistics infrastructure, extensive trucking networks, and increasing deployment of connected fleet technologies.

Europe

Europe remains a mature and technologically advanced market driven by strong semitrailer freight operations, regulatory compliance requirements, and rising digital fleet management adoption.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region due to expanding freight transportation, booming e-commerce logistics, and increasing investments in smart supply chain infrastructure.

U.S.

The U.S. trailer telematics market is expected to reach approximately USD 0.91 billion in 2026, supported by strong adoption of connected-trailer platforms and growing demand for predictive fleet management solutions.

Japan

Japan’s market is projected to reach around USD 0.11 billion in 2026, driven by advanced transportation infrastructure and increasing use of telematics for supply chain visibility and temperature-controlled logistics.

Read More

Trailer Telematics Market KeyTakeaways

- 2025 Market Size: USD 2.54 billion

- 2026 Market Size: USD 3.02 billion

- 2034 Forecast Market Size: USD 7.04 billion

- CAGR: 11.2% from 2026–2034

- North America dominated the trailer telematics market with a 38.19% share in 2025.

- The LPWAN (LoRa, Sigfox) segment is projected to grow at the fastest CAGR of 16.6% during the forecast period.

- The software segment is anticipated to expand at a CAGR of 14.3% over the study period.

North America

North America led the global market in 2025, supported by advanced logistics infrastructure, extensive trucking networks, and high adoption of connected fleet technologies.

Europe

Europe remains a technologically advanced market driven by strong semitrailer freight transport systems, strict transportation regulations, and rising adoption of digital fleet management solutions.

Asia Pacific

Asia Pacific is projected to witness the fastest growth due to rapid expansion of e-commerce logistics, growing cross-border trade, and increasing investments in smart transportation infrastructure.

U.S.

The U.S. trailer telematics market is projected to reach approximately USD 0.91 billion in 2026, driven by strong demand for real-time fleet visibility and predictive maintenance solutions.

Japan

Japan’s market is estimated to reach around USD 0.11 billion in 2026, supported by advanced transportation infrastructure and increasing deployment of connected logistics technologies.

Read More

TRAILER TELEMATICS MARKET TRENDS

Rising Integration of Smart Trailer and IoT Technologies Drives Market Evolution

Smart trailer technologies are increasingly transforming logistics operations by turning trailers into connected assets that transmit real-time operational data. Fleet operators are adopting these systems to gain better operational visibility and improve asset productivity across long-haul and regional logistics networks. Smart trailers enable predictive maintenance, automated alerts, and optimized trailer allocation, which helps reduce idle time and operational inefficiencies. As digital freight management and connected fleet ecosystems expand globally, trailer telematics is becoming a core technology within supply chain digitalization strategies, particularly among large logistics providers and refrigerated transport operators.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for Real-Time Fleet Visibility and Operational Efficiency Fuels Market Expansion

Logistics operators are prioritizing technologies that provide real-time visibility into fleet assets, cargo conditions, and trailer utilization, which is significantly driving the global trailer telematics market growth. These systems allow fleet managers to track trailer movements, monitor cargo temperature, detect door openings, and optimize route decisions through centralized fleet management platforms. Reducing empty miles, preventing cargo loss, and improving asset utilization directly improve profitability in large-scale freight operations. Additionally, regulatory requirements for cargo safety and compliance further encourage fleets to adopt connected trailer technologies. As freight volumes continue to grow and supply chains become more complex, transportation companies increasingly rely on telematics solutions to improve operational control and ensure reliable delivery performance.

- In April 2021, ORBCOMM announced that IWX Motor Freight had adopted its cold-chain telematics solution to monitor refrigerator trailers, enabling real-time tracking and temperature monitoring for high-value cargo shipments.

MARKET RESTRAINTS

High Initial Implementation Costs and Integration Complexity Limit Market Adoption

Despite the benefits of trailer telematics, the high upfront cost of hardware installation and system integration remains a major restraint for many fleet operators, particularly small and medium-sized trucking companies. Deploying telematics systems across large trailer fleets requires investment in sensors, telematics control units, connectivity services, and fleet management solutions software platforms. In addition, integrating telematics solutions with existing transportation management systems and enterprise resource planning platforms can be technically complex and time-consuming. Smaller fleets with limited capital budgets may hesitate to adopt these technologies because the return on investment may take several years to realize. These financial and operational barriers slow adoption rates in cost-sensitive transportation markets and in regions where digital fleet infrastructure is still developing.

MARKET OPPORTUNITIES

Expansion of Cold Chain Logistics and Temperature-Sensitive Freight Creates Significant Growth Opportunities

The rapid expansion of global cold-chain logistics presents a major opportunity for trailer telematics providers. Transportation of temperature-sensitive goods such as food, pharmaceuticals, and biotechnology products requires precise monitoring of cargo conditions throughout the supply chain. Trailer telematics systems equipped with temperature, humidity, and door sensors allow logistics operators to monitor cargo environments in real time and receive alerts when conditions deviate from acceptable thresholds. This capability reduces spoilage risks, ensures regulatory compliance, and enhances supply chain transparency. As international trade in perishable products increases and pharmaceutical distribution networks expand, telematics-enabled refrigerated trailers are expected to experience strong demand. Companies offering integrated cold-chain monitoring platforms are therefore positioned to benefit significantly from this market shift.

MARKET CHALLENGES

Data Security Risks and Connectivity Reliability Challenges Affect System Performance

As trailer telematics systems increasingly rely on wireless networks and cloud-based data platforms, concerns about data security, system reliability, and network coverage are becoming major challenges for enabling fleet operators. Large fleets generate significant volumes of operational data that must be transmitted securely between trailers, vehicles, and centralized fleet management systems. Any vulnerabilities in communication networks or telematics platforms could expose logistics operations to cyber risks or data breaches. Additionally, connectivity gaps in remote or rural transport corridors may limit the reliability of real-time monitoring systems. Maintaining secure data transmission and ensuring uninterrupted connectivity across diverse geographic regions, therefore, remains a critical challenge for telematics solution providers and logistics companies deploying connected trailer technologies.

Segmentation Analysis

By Component

Hardware Component Lead the Market Due to Significant Investment by Large Fleet Operators

Based on component, the market is segmented into hardware, software, and services.

The hardware dominates the market because telematics deployment begins with physical devices such as telematics control units, sensors, GPS devices, and RFID tags installed directly on trailers. These hardware components capture operational data such as location, cargo status, and trailer conditions, enabling communication with fleet management platforms. Large fleet operators invest significantly in hardware infrastructure during the early stages of telematics implementation, which supports the segment’s leading market share. As connected-trailer fleets expand, demand for reliable sensing and communication devices continues to grow.

The software segment is projected to grow at a CAGR of 14.3% over the forecast period.

- In June 2022, ZF announced the expansion of its SCALAR fleet orchestration platform to integrate trailer telematics data for fleet analytics and asset monitoring.

By Application

Trailer Tracking & Location Monitoring Dominates the Market Owing to Real-Time Trailer Visibility for Fleet Operators

Based on application, the market is segmented into trailer tracking & location monitoring, cargo & condition monitoring, asset utilization & fleet management, and security & theft prevention.

The trailer tracking & location monitoring dominates the global trailer telematics market share because real-time trailer visibility is the primary use case for fleet operators adopting telematics solutions. Tracking technologies enable logistics companies to monitor trailer location, movement, and route history, improving dispatch planning, enabling faster response to delays, and enhancing supply chain transparency. As fleets seek to optimize trailer utilization and reduce idle equipment time, GPS-based tracking systems remain the most widely implemented telematics function across commercial trailers globally.

The cargo & condition monitoring segment is projected to grow at a 13.0% CAGR over the forecast period.

- In October 2023, ORBCOMM introduced its next-generation smart-trailer telematics solution, designed to provide real-time tracking and monitoring of trailers and cargo conditions.

By Trailer Type

Widespread General Freight Transportation Sustains Dry Van Trailer Segmental Leadership

Based on trailer type, the market is segmented into dry van trailers, refrigerated (reefer) trailers, flatbed trailers, and tanker trailers.

Dry van trailers dominate the market because they account for the largest share of general freight transportation worldwide, including retail goods, packaged products, and consumer shipments. Fleet operators widely deploy telematics in dry van trailers to improve real-time tracking, enhance asset utilization, and reduce empty trailer movements across logistics networks. Since dry vans are the most common trailer type in long-haul freight operations, telematics solutions for location monitoring and utilization management are most widely installed in this segment.

The refrigerated (Reefer) trailers segment is projected to grow at a CAGR of 12.4% over the forecast period.

- In September 2023, Utility Trailer Manufacturing Company announced expanded deployment of TrailerConnect telematics systems across its refrigerated and dry van trailers to improve real-time fleet visibility and asset monitoring.

To know how our report can help streamline your business, Speak to Analyst

By Connectivity Technology

Cellular Connectivity Leads the Market Due to Reliability, Cost-Efficiency, and Real-Time Communication Between Platforms

Based on connectivity technology, the market is segmented into cellular (4G/5G, LTE-M, NB-IoT), satellite, LPWAN (LoRa, Sigfox), and RFID & short-range communication.

The cellular connectivity dominates because it provides reliable, cost-effective, and real-time communication between telematics devices and cloud-based fleet management platforms. Cellular networks support continuous data transmission for location tracking, cargo monitoring, and predictive maintenance applications across long-haul transportation routes. The widespread availability of 4G and emerging 5G networks further strengthens the adoption of cellular connectivity for telematics systems across commercial trailer fleets worldwide.

The LPWAN (LoRa, Sigfox) segment is projected to grow at a 16.6% CAGR over the forecast period.

- In February 2024, Semtech announced expanded adoption of LoRa-enabled asset tracking solutions for logistics and transportation applications to improve long-range, low-power monitoring of mobile assets.

TRAILER TELEMATICS MARKET REGIONAL OUTLOOK

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

NORTH AMERICA

North America Trailer Telematics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North American market holds a dominant share due to the region’s highly developed logistics industry, extensive long-haul trucking networks, and strong adoption of connected fleet technologies. Large commercial trailer fleets in the U.S. and Canada increasingly deploy telematics to improve trailer utilization, cargo security, and fleet efficiency. The presence of major telematics solution providers and OEM-integrated smart trailer platforms further supports regional growth. The increasing demand for cold-chain monitoring and real-time asset visibility across cross-border freight corridors between the U.S., Canada, and Mexico is also accelerating the adoption of advanced trailer telematics systems among logistics operators.

U.S. TRAILER TELEMATICS MARKET

The U.S. market is expected to reach USD 0.91 billion in 2026, driven by its massive tractor-trailer freight ecosystem and high telematics adoption among logistics companies. Large fleet operators are increasingly investing in connected-trailer solutions to improve real-time fleet visibility, optimize trailer utilization, and support predictive maintenance. Growth is further supported by strong demand for cold-chain logistics and the rapid adoption of integrated fleet management platforms across trucking and logistics companies.

EUROPE

Europe is a mature, technologically advanced market for trailer telematics, driven by the region’s strong logistics infrastructure and widespread use of semitrailer-based freight transport. European logistics companies increasingly deploy telematics solutions to improve operational efficiency, regulatory compliance, and cargo visibility across cross-border transportation networks. The region also benefits from strong trailer manufacturing capabilities and OEM-integrated telematics platforms offered by leading trailer manufacturers. Rising demand for refrigerated logistics, stricter transportation regulations, and the increasing adoption of digital fleet management systems are driving telematics adoption across commercial trailer fleets in Europe.

U.K. TRAILER TELEMATICS MARKET

The U.K. is a key contributor to Europe’s market due to its highly developed logistics and retail distribution networks. Fleet operators in the country are increasingly deploying telematics solutions to optimize fleet performance, monitor cargo conditions, and reduce operational costs. The growth of e-commerce logistics and cold-chain transportation further supports the growing adoption of connected-trailer technologies. The U.K. market is set to be valued at USD 0.14 billion by 2026.

GERMANY TRAILER TELEMATICS MARKET

Germany holds a strong position in the European market due to its central role in freight transportation and its advanced logistics infrastructure. The country’s large commercial vehicle fleet and strong trailer manufacturing ecosystem encourage the adoption of telematics-enabled trailers. Logistics companies in Germany increasingly rely on connected fleet solutions to improve asset utilization, supply chain transparency, and regulatory compliance. Germany’s market is expected to reach a growth rate of 10.2% during the forecast period.

ASIA PACIFIC

Asia Pacific is the fastest-growing region in the global market, driven by rapid growth in freight transportation, expanding e-commerce logistics, and increasing investments in digital supply chain infrastructure. Countries across the region are modernizing logistics operations through connected fleet technologies and smart transportation systems. Rising demand for cold-chain logistics, growing industrial production, and increasing cross-border trade are encouraging logistics companies to deploy trailer telematics solutions. As large commercial fleets seek improved operational visibility and efficiency, telematics adoption across trailers is expected to expand significantly across major Asia Pacific economies.

CHINA TRAILER TELEMATICS MARKET

China is expected to be the largest market, with a 44.1% share in 2026, in the Asia Pacific, due to its vast logistics industry and rapidly expanding freight transportation sector. Logistics companies are increasingly implementing telematics technologies to enhance fleet monitoring, improve cargo visibility, and optimize transportation efficiency. Growth is also supported by large-scale commercial vehicle fleets and expanding digital logistics platforms across the country.

JAPAN TRAILER TELEMATICS MARKET

Japan’s market benefits from the country’s advanced transportation infrastructure and strong adoption of connected mobility technologies. Logistics operators increasingly deploy telematics solutions to improve supply chain visibility, manage fleet operations more efficiently, and support temperature-controlled logistics. The country’s emphasis on technological innovation and operational efficiency reduces costs and continues to support the adoption of telematics across commercial vehicle fleets. Japan is projected to reach a valuation of USD 0.11 billion in 2026.

INDIA TRAILER TELEMATICS MARKET

India is expected to experience a rapid growth with a 15.8% CAGR during the forecast period, as the country’s logistics sector expands and digital fleet management technologies gain traction. Increasing freight movement, growing organized logistics networks, and rising adoption of GPS-based fleet monitoring solutions are supporting demand. The government’s focus on digital transportation infrastructure and improved supply chain efficiency is further encouraging the deployment of telematics across commercial trailers.

REST OF THE WORLD

The Rest of the World region, including Latin America, the Middle East, and Africa, represents a developing market for trailer telematics solutions. Although telematics adoption is still at an early stage compared with North America and Europe, logistics operators in these regions are gradually implementing connected fleet technologies to improve operational efficiency and cargo security. Increasing international trade, expansion of regional logistics networks, and rising investments in digital transportation infrastructure are supporting the gradual adoption of trailer telematics systems across freight fleets in emerging economies.

COMPETITIVE LANDSCAPE

Key Industry Players

Connected Fleet Platforms and Strategic Partnerships Strengthen Key Players’ Competitiveness

Rapid growth in connected fleet platforms, sensor-enabled monitoring systems, and strategic collaborations among telematics providers, trailer OEMs, and logistics companies is shaping the global trailer telematics market trends. Major players such as ORBCOMM, Samsara, Geotab, Verizon Connect, Trimble, ZF Group, Phillips Connect, and Schmitz Cargobull compete by offering integrated smart-trailer solutions that combine GPS tracking, cargo monitoring, predictive maintenance analytics, and cloud-based fleet management software. Companies increasingly focus on scalable software platforms, multi-sensor telematics hardware, and subscription-based service models to enhance fleet visibility and operational efficiency. Partnerships between telematics providers and trailer manufacturers are also expanding OEM-installed solutions that enable factory-integrated connectivity. Additionally, investments in IoT connectivity, AI-driven fleet analytics, and cybersecurity capabilities are strengthening competitive differentiation.

- In October 2023, ORBCOMM launched its next-generation smart-trailer solution, designed to provide real-time visibility into trailer location, cargo condition, and asset utilization across global transportation fleets.

LIST OF KEY TRAILERS TELEMATICS COMPANIES PROFILED

- Samsara Inc. (U.S.)

- Verizon Connect (U.S.)

- Geotab Inc. (Canada)

- Trimble Inc. (U.S.)

- ORBCOMM Inc. (U.S.)

- CalAmp Corp. (U.S.)

- Zonar Systems Inc. (U.S.)

- PowerFleet Inc. (U.S.)

- Phillips Connect Technologies (U.S.)

- Spireon Inc. (U.S.)

- Schmitz Cargobull AG (Germany)

- Krone Commercial Vehicle Group (Germany)

- WABCO Holdings Inc. / ZF Group (Germany)

- Continental AG (Germany)

- SkyBitz Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Cartrack partnered with Schmitz Cargobull to integrate TrailerConnect data into Cartrack’s SaaS fleet platform. The agreement allows fleets to access trailer temperature, location, route, and load-condition data via OEM-fitted devices without additional hardware, strengthening interoperability of trailer telematics, compliance monitoring, and operational control for European transport operators.

- January 2026: Phillips Connect and McLeod Software launched a smart-trailer integration that feeds trailer location, tire, light, brake health, and AI-powered cargo intelligence data directly into McLeod’s TMS. The collaboration helps fleets plan loads, cut empty moves, improve trailer turns, and embed trailer telematics into everyday dispatch and planning workflows.

- October 2025: Schmitz Cargobull and AddSecure announced a Europe-wide strategic partnership for a fully integrated truck-and-trailer telematics solution. The platform combines TrailerConnect data, including TPMS information, with AddSecure’s FleetVision portal, enabling automatic integration without extra hardware and lowering IT workload for fleet operators across Europe.

- September 2025: Phillips Connect introduced TechAssist, a mobile app designed to simplify the installation and maintenance of smart-trailer technology. The launch supports trailer OEMs and fleet installers with guided workflows, one-click setup, diagnostics, and enhanced visibility into ABS and PLC connections, helping smart trailers become operational faster and with fewer installation errors.

- March 2025: ORBCOMM announced Hill Bros selected its integrated dry and refrigerated trailer monitoring solutions for fleet-wide management. The deployment combines ORBCOMM hardware with a unified cloud analytics platform, enabling the carrier to monitor trailer location, reefer temperature, load status, utilization, and yard activity through a single consolidated telematics environment.

REPORT COVERAGE

The global trailer telematics market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, strategic partnerships, mergers & acquisitions. The market forecast provides a comprehensive competitive landscape, including the largest market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.2% from 2026 to 2034 |

| Unit | Value (USD billion) |

| Segmentation | By Trailer Type, By Component, By Application, By Connectivity Technology, and By Region |

| By Component |

|

| By Application |

|

| By Connectivity Technology |

|

| By Trailer Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.54 billion in 2025 and is projected to reach USD 7.04 billion by 2034.

In 2025, the market value stood at USD 0.97 billion.

The global market is expected to grow at a CAGR of 11.2% during the forecast period.

The cellular sub-segment led the market share in the connectivity technology segment.

Rising demand for real-time trailer visibility, better fleet utilization, cargo security, and predictive maintenance are driving market momentum.

Key market players include Samsara, Geotab, ORBCOMM, Verizon Connect, Trimble, and Phillips Connect.

North America accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us