Transparent Barrier Packaging Films Market Size, Share & Industry Analysis, By Material (Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Ethylene Vinyl Alcohol (EVOH), Polyamide (PA), Polyvinylidene Chloride (PVDC), and Others), By End-use Industry (Food & Beverages, Healthcare, Personal Care & Cosmetics, Home Care, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

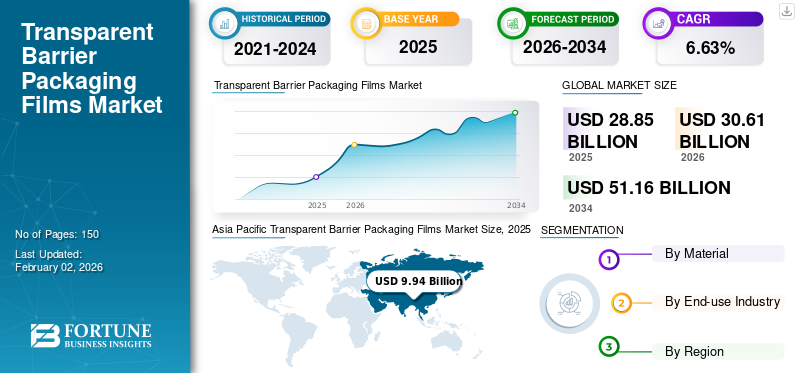

The global transparent barrier packaging films market size was valued at USD 28.85 billion in 2025 and is projected to grow from USD 30.61 billion in 2026 to USD 51.16 billion by 2034, exhibiting a CAGR of 6.63% during the forecast period. Asia Pacific dominated the transparent barrier packaging films market with a market share of 34.45% in 2025.

Transparent barrier packaging films are advanced multilayer or coated plastic films engineered to offer both visibility and protection for packaged goods. These films merge transparency, enabling consumers to see the contents, with excellent barrier characteristics that inhibit the passage of gases such as oxygen, carbon dioxide, and water vapor.

Furthermore, the market includes several key players, with Smurfit Kappa, Sealed Air, and Pregis Corporation, at the forefront. A broad portfolio, innovative product launches, and strong steps aimed at expanding geographical presence have supported the leading position of these players in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand from the Food and Beverage Industry to Fuel Market Expansion

The primary driver for the global market for transparent barrier packaging films is the increasing demand from the food and beverage industry for prolonged shelf life and enhanced product visibility. These films offer superior barriers against oxygen, moisture, and aroma, rendering them suitable for packaging perishable items such as meat, dairy products, snacks, and ready-to-eat meals. The rising trend of convenience foods, combined with consumers' preference for visually attractive and sustainable packaging, is driving adoption. Additionally, innovations in multilayer film technologies and the growing shift from rigid formats to flexible packaging are further propelling the global transparent barrier packaging films market growth.

MARKET RESTRAINTS

Environmental Impact Concerns and Recycling Challenges to Hinder Market Growth

Despite the advantages they offer, the market encounters limitations stemming from environmental issues associated with plastic use and the challenges involved in recycling multilayer barrier films. The majority of transparent barrier films are composed of materials such as PET, EVOH, and PVDC, which complicate the recycling process and add to the accumulation of plastic waste. Stringent government regulations targeting single-use plastics, along with growing consumer awareness regarding sustainability, are driving manufacturers to transition toward recyclable or bio-based alternatives. This shift may lead to increased production costs and restrict the market expansion.

MARKET OPPORTUNITIES

Rising Focus on Sustainable and Bio-Based Barrier Films Creates Profitable Growth Opportunities

The current shift toward environmentally sustainable packaging options presents profitable opportunities for market participants. Advancements in bio-based materials, including Polylactic Acid (PLA) and cellulose-based barrier films, are gaining traction as industries strive to achieve their sustainability objectives. Moreover, the increasing use of these packaging materials in pharmaceuticals, pet food, and personal care packaging, where both product protection and visibility are crucial, is anticipated to create new opportunities for market growth. Strategic partnerships between resin manufacturers and packaging converters aimed at creating recyclable or compostable transparent films also offer considerable commercial prospects.

TRANSPARENT BARRIER PACKAGING FILMS MARKET TRENDS

Rising Shift toward High-Performance, Recyclable, and Multi-Functional Films Emerges as a Market Trend

The market is experiencing a significant transition toward recyclable and high-performance transparent barrier films, which are intended to fulfill both functional and environmental criteria. Innovations in coating and nanocomposite barriers are improving the durability, heat resistance, and recyclability of these films. Additionally, the rising use of transparent packaging in e-commerce, along with the increasing impact of premium branding and clean-label packaging, is influencing future demand. Furthermore, companies are investing in mono-material structures to facilitate recycling while maintaining oxygen and moisture barrier characteristics.

MARKET CHALLENGES

Fluctuating Raw Material Prices and High Production Costs to Raise Challenges for Market Development

One of the primary challenges faced in this market is the instability of raw material prices, especially for petroleum-derived resins such as polyethylene and polypropylene. These fluctuations have a direct impact on profit margins and the stability of the supply chain. Furthermore, the manufacturing of high-barrier multilayer films requires advanced technology and considerable capital investment, which can pose as barriers to entry for small and medium-sized producers. Striking a balance between performance characteristics, cost-effectiveness, and sustainability remains a significant technical challenge for industry players.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Outstanding Benefits Offered by Polyethylene Material to Drive Segment Growth

In terms of material, the market is categorized into Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Ethylene Vinyl Alcohol (EVOH), Polyamide (PA), Polyvinylidene Chloride (PVDC), and others.

The polyethylene (PE) material segment is expected to lead the market, contributing 28.84% globally in 2026. Polyethylene (PE) is a prominent material in the market for transparent barrier packaging films, attributed to its exceptional versatility, affordability, and functional benefits. PE films provide outstanding moisture barrier characteristics, superior sealability, and robust mechanical strength, rendering them suitable for diverse packaging applications in food, personal care, and pharmaceutical packaging. Their adaptability and compatibility with different co-extrusion and lamination techniques allow manufacturers to produce multilayer structures that improve oxygen and aroma resistance while preserving optical clarity.

The polypropylene (PP) material segment is projected to register a CAGR of 6.84% over the forecast period.

By End-use Industry

Rising Utilization of Transparent Barrier Films in the Food & Beverages Sector to Drive Segmental Growth

Based on end-use industry, the market is classified into food & beverages, healthcare, personal care & cosmetics, home care, and others.

The food and beverage segment will hold the largest share of the market, driven by demand for packaging materials that ensure extended shelf life, product safety, and freshness, accounting for a 33.45% market share in 2026. Moreover, the demand for such packaging films has accelerated due to the rising consumer preference for convenience and on-the-go packaged foods combined with the growth of e-commerce food delivery and increasing consumption of processed and frozen food items.

To know how our report can help streamline your business, Speak to Analyst

In addition, the healthcare end-use industry segment is likely to showcase a CAGR of 6.72% during the study period.

Transparent Barrier Packaging Films Market Regional Outlook

By geography, the market is classified into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Transparent Barrier Packaging Films Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 34.45% to the global market in 2025, with a valuation of USD 9.94 billion, and is projected to reach USD 10.65 billion in 2026. An increase in packaged food consumption, the growth of retail and e-commerce, and a rise in pharmaceutical manufacturing in China and India drives the Asia Pacific transparent barrier packaging films industry. This area significantly influences global film demand, as both converters and brands in the region quickly embrace flexible packaging and prefer cost-efficient film solutions.

In the region, India and China are estimated to reach USD 2.89 and USD 3.5 billion respectively in 2026.

North America

In 2025, North America represented USD 7.24 billion, accounting for 25.09% of the worldwide market, and is projected to grow to USD 7.68 billion in 2026. The growth of the market in North America is propelled by robust demand from the food and beverage sector, e-commerce packaging, and pharmaceuticals, where clarity and barrier performance are essential. Brand owners seek transparent films that extend shelf life and highlight the product. The rising investments in flexible packaging lines are increasing film consumption. In 2026, the U.S. market accounts for a value of USD 6.2 billion.

Europe

The Europe market generated USD 5.3 billion in 2025, representing 18.36% of the global market landscape, and is expected to reach USD 5.59 billion in 2026. The dynamics of Europe are significantly influenced by assertive circular-economy policies, such as the EU Packaging & Packaging Waste Regulation and the Extended Producer Responsibility (EPR) schemes implemented by member states. This regulatory impetus serves as both a limitation, particularly for multilayer transparent films that pose recycling challenges, and a substantial market influencer given that manufacturers are required to either redesign films to enhance recyclability or to offer verified end-of-life solutions. Backed by these factors, the U.K. is expected to reach a valuation of USD 1.02 billion, Germany to record USD 1.21 billion in 2026, and France to hit USD 0.84 billion in 2025.

Latin America

Over the forecast period, the Middle East & Africa and Latin America regions would witness moderate growth in this market. The market in Latin America reached USD 3.58 billion in 2025, representing 12.40% of total market revenue, and is projected to reach USD 3.76 billion in 2026. Latin America exhibits consistent growth in demand, primarily driven by packaged foods, beverages, and pharmaceutical (smaller yet expanding) sectors. The key factors further contributing to this growth are urbanization and an increasing penetration of packaged foods.

Middle East & Africa

The Middle East & Africa market was valued at USD 2.8 billion in 2025, capturing 9.69% of global revenue, and is estimated to reach USD 2.92 billion in 2026. The Middle East and Africa represents a diverse market. The Gulf regions and South Africa exhibit a heightened demand for high-performance transparent barrier films (such as those used for imported products, premium frozen food, and pharmaceuticals), whereas other nations tend to be more sensitive to pricing. Key factors contributing to this trend include the expansion of the frozen and processed food sectors, rising investments in the transparent barrier packaging films industry, along with a rise in imports that necessitate durable barrier packaging.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players’ Diverse Product Range and Robust Distribution Network to Strengthen Market Leadership

The global transparent barrier packaging films industry displays a semi-concentrated structure with various small- to mid-size companies actively working across the globe. These players are engaged in product innovation, strategic partnerships, and geographic expansion.

Amcor Plc, Mondi, and Klöckner Pentaplast are some of the dominating players in the market. A comprehensive range of unit-dose packaging products, global presence through a robust supply chain, and partnerships with research and academic institutes are a few characteristics of these players that support their dominance.

Apart from this, other key players in the market are Sealed Air, TOPPAN Inc., Glenroy Inc., and others. These companies are executing various strategic initiatives, including investments in R&D and forming partnerships with pharmaceutical companies to increase their market presence.

LIST OF KEY TRANSPARENT BARRIER PACKAGING FILMS COMPANIES PROFILED

- Amcor Plc (Switzerland)

- Mondi (U.K.)

- Klöckner Pentaplast (U.K.)

- Sealed Air (U.S.)

- TOPPAN Inc. (Japan)

- Glenroy Inc. (U.S.)

- Zhejiang Changyu New Materials Co., Ltd. (China)

- Momar Industries (U.S.)

- 3M (U.S.)

- Innovia Films (U.K.)

- Cosmo Films Ltd. (India)

- UFlex Limited (India)

- WINPAK LTD (Canada)

- Qingdao Kingchuan Packaging (China)

- Green Packaging Material (Jiangyin) Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- September 2025: TIPA Compostable Packaging announced an expansion of its product range to incorporate four new high-barrier film and laminate offerings. These new laminates further TIPA’s commitment to providing compostable options without sacrificing performance, barrier, or compatibility with machinery. Significant applications encompass single-serve and sachet uses, chips and various salty snacks, protein and beverage powders, nutraceuticals such as vitamins and gummies, as well as ground coffee and tea.

- July 2025: RKW Group introduced its newest advancement in sustainable advanced packaging solutions by launching films that feature an integrated ethylene-vinyl alcohol (EVOH) barrier. These films, improved with cutting-edge machine-direction orientation (MDO) technology, provide recyclability and sustainability across various packaging formats and sectors, establishing new standards for flexible packaging. The increasing demand from consumers and forthcoming global regulations are propelling the necessity for these innovative solutions.

- December 2023: TOPPAN Packaging Czech s.r.o., a subsidiary of the TOPPAN Group, hosted a ceremonial groundbreaking to initiate the construction of a new facility in Most, located in the Ústí nad Labem Region of the Czech Republic. The facility will produce GL BARRIER, a leading transparent barrier film that is developed and produced by the TOPPAN Group, catering to the growing global demand for environmentally friendly packaging.

- October 2022: Japan-based Toppan enhanced its GL Barrier line of transparent films by introducing a Polyethylene (PE) mono-material barrier packaging specifically for liquids. The company noted that achieving the necessary properties for packaging liquid and high-moisture products with PE mono-material structures has been challenging until then. The newly developed packaging, which is also designed for boiling sterilization, would offer barrier performance that would surpass the then PE mono-material packaging options.

- May 2019: CCL Industries' division Innovia Films broadened its product line with the launch of a series of transparent high-barrier packaging films. Referred to as Propafilm Strata SL, these recyclable films can function as a standalone mono-filmic solution or be incorporated into laminate constructions, making them potentially suitable for the food industry. The transparent high quality of these films, which comply with Food Contact regulations and are free from chlorine, enables customers to see the products that are enclosed within.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.63% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Material · Polyethylene (PE) · Polypropylene (PP) · Polyethylene Terephthalate (PET) · Ethylene Vinyl Alcohol (EVOH) · Polyamide (PA) · Polyvinylidene Chloride (PVDC) · Others By End-use Industry · Food & Beverages · Healthcare · Personal Care & Cosmetics · Home Care · Others By Geography · North America (By Material, End-use Industry, and Country) o U.S. o Canada · Europe (By Material, End-use Industry, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, End-use Industry, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, End-use Industry, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, End-use Industry, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 28.85 billion in 2025 and is projected to reach USD 51.16 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 9.94 billion.

The market is expected to exhibit a CAGR of 6.63% during the forecast period of 2026-2034.

The polyethylene (PE) segment led the market by material in 2026.

The key factor driving the market growth is the rising demand from the food and beverage industry.

Amcor Plc, Mondi, Klockner Pentaplast, Sealed Air, TOPPAN Inc., and Glenroy Inc. are some of the prominent players in the market.

Asia Pacific dominated the transparent barrier packaging films market with a market share of 34.45% in 2025.

Increasing demand from the food and beverage industry is one of the factors that is expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us