Ultra High Strength Steel (UHSS) Market Size, Share & Industry Analysis, By Type (Dual Phase, Complex Phase, Martensitic Steels, Press Hardened Steels and Others), By End Use (Automotive & Transportation, Machinery & Heavy Equipment, Construction & Infrastructure, Aerospace & Defense, and Others), and Regional Forecast, 2025-2032

Ultra High Strength Steel Market Size and Future Outlook

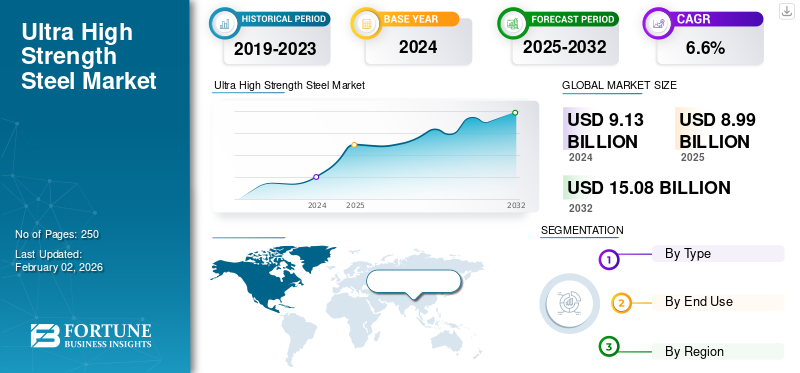

The global ultra high strength steel market size was valued at USD 9.13 billion in 2024. The market is projected to grow from USD 8.99 billion in 2025 to USD 15.08 billion by 2032, exhibiting a CAGR of 6.6% during the forecast period. North America dominated the global ultra high strength steel (UHSS) market with a market share of 49.07% in 2024.

Ultra High Strength Steels (UHSS) refer to a family of advanced steel grades with tensile strengths typically above 980 MPa, engineered to deliver exceptional strength-to-weight ratio, enhanced crash resistance, and superior structural integrity. UHSS is widely used in automotive body structures, chassis components, safety reinforcements, electric vehicle (EV) battery protection systems, industrial machinery, construction equipment, and defense armor applications. Compared with conventional carbon steels and standard high-strength steels (HSS), UHSS offers significantly higher load-bearing capability, improved energy absorption, and superior fatigue resistance. As OEMs push for lighter vehicles, stricter crash standards, and more durable structures, UHSS continues to gain preference across industries, driving steady demand globally.

The ultra high strength steel landscape is shaped by several leading global steelmakers, including ArcelorMittal, SSAB, POSCO, Nippon Steel, JFE Steel, Baowu Group, Hyundai Steel, and U.S. Steel. These companies maintain extensive product portfolios, spanning dual-phase, complex-phase, martensitic, and press-hardened steel grades. Their continuous investments in hot-stamping lines, coating technologies, and low-carbon steelmaking innovations further reinforce their competitive positioning in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Increasing Use of UHSS in Construction, Mining, and Heavy Machinery to Drive Market Growth

The expanding use of ultra high strength steel products across construction, mining, and heavy machinery is emerging as a strong catalyst for global market growth. As infrastructure spending accelerates across Asia, the Middle East, and Latin America, demand for high-strength steel with superior load-bearing capacity, corrosion resistance, and fatigue life has increased sharply. UHSS grades, especially martensitic, quenched-and-tempered (Q&T), and ferrite-bainite variants, offer exceptional strength-to-weight performance, enabling lighter, more durable structural components in cranes, earthmovers, mining trucks, drilling rigs, and high-stress construction beams. These attributes translate into higher equipment uptime, improved fuel efficiency, and extended component life.

The global construction equipment market is expanding, driving up the consumption for UHSS-intensive categories such as cranes and mining machinery. The mining sector is also projected to add a significant number of new heavy-duty haul trucks by 2030, many of which utilize UHSS for dump bodies, chassis frames, and structural reinforcements. As OEMs prioritize durability and lifecycle cost reduction, the adoption of UHSS continues to rise. Thus, the increasing usage across construction, mining, and heavy machinery is expected to drive the global ultra high strength steel (UHSS) market growth during the forecast period.

MARKET RESTRAINTS:

Higher Production Costs and Formability and Joining Issues May Restrain Market Growth

Despite its strong performance advantages, UHSS adoption is often constrained by its significantly higher production and processing costs compared to conventional carbon steels and even standard high-strength steels (HSS). UHSS grades require advanced alloying compositions, controlled thermomechanical rolling, continuous annealing, and specialized heat treatment routes, such as hot stamping or quenching and tempering. These processes add substantial energy, equipment, and operational costs. As a result, UHSS can cost two to three times more per ton than traditional structural steels.

Additionally, UHSS materials also present inherent challenges in formability, welding, and joining, which continue to hinder their wider industrial adoption. As tensile strength increases, ductility tends to decrease, making UHSS more difficult to shape into complex geometries without cracking, edge failure, or springback. Advanced forming techniques such as hot stamping, tailored blank welding, roll forming, or multi-stage forming are often required, each of which demands specialized tooling, process expertise, and higher capital investment. These combined economic and processability challenges limit UHSS penetration in highly cost-constrained segments and delay adoption among smaller manufacturers lacking economies of scale.

MARKET OPPORTUNITIES:

Increasing Demand for High-Strength Materials in Military & Defense to Create Lucrative Opportunity

The growing demand for advanced high-strength materials in defense, national security, and critical infrastructure is creating significant opportunities for UHSS manufacturers. Modern armored vehicles, military transport systems, and ballistic-resistant structures require steels with superior hardness, strength-to-weight ratios, and impact resistance. UHSS, especially quenched-and-tempered (Q&T) grades, offers tensile strength of 1400 MPa, providing essential protection against blast loads, ballistic threats, and extreme operating conditions. According to the United Nations, the global defense spending worldwide surpassed USD 2.7 trillion in 2024. Such massive investments would position UHSS as a strategic material for high-performance applications in defense, creating lucrative opportunities in the market.

ULTRA HIGH STRENGTH STEEL MARKET TRENDS:

Trend of Automotive Lightweighting and Electrification to Fuel Product Demand

The ongoing transition toward lightweighting and electrification of vehicles is a major trend shaping the UHSS market globally. Automotive OEMs are increasingly designing lighter, stronger body-in-white structures to meet stringent emissions standards, improve fuel efficiency, and extend electric vehicle (EV) driving range. UHSS, grades, particularly dual-phase, complex-phase, martensitic, and press-hardened steels, offer tensile strengths ranging from 980–2000 MPa, enabling up to 30–40% weight reduction compared to conventional steels while maintaining crashworthiness.

Moreover, the average EV uses 20–30% more UHSS than internal-combustion vehicles due to battery protection trays, underbody shields, side-impact reinforcements, and crash-energy management structures. According to the International Energy Agency (IEA), global EV sales surpassed 17 million units in 2024. With EV penetration expected to reach 45–50% of new car sales by 2030, UHSS consumption per vehicle is forecast to increase steadily. As OEMs push for more durable vehicles with lightweight materials, UHSS will remain an integral part of next-generation automotive architecture in the foreseeable period.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Press Hardened Steels Led due to its Excellent Dimensional Accuracy

Based on type, the market is classified into dual phase, complex phase, martensitic steels, press hardened steels, and others.

The press hardened steels (PHS) segment dominated the global ultra high strength steel (UHSS) market share in 2024 due to its excellent dimensional accuracy. PHS has a cornerstone of modern safety cell design, used in A/B pillars, roof rails, door rings, and EV battery protection systems. Its ability to achieve superior crash performance, combined with lightweighting potential, has led to rapid adoption, especially in EVs and 5-star safety platforms. As automakers expand hot-stamping capacity globally, PHS represents the fastest-growing UHSS segment across leading OEMs.

Complex Phase steels exhibit a refined microstructure comprising bainite, martensite, and retained austenite, providing higher strength and improved hole-expansion capability compared to dual-phase grades. With tensile strength levels ranging from 1000 to 1180 MPa, CP steels are optimized for applications that require excellent edge stability and resistance to crack propagation. They are commonly used in structural components, seat frames, crash boxes, anti-intrusion parts, and chassis reinforcements. Their growing adoption by major OEMs is advancing UHSS usage in mainstream vehicle designs.

Martensitic UHSS grades, typically ranging from 1200 to 1700 MPa in tensile strength, provide exceptional hardness, strength, and impact resistance. Produced through rapid quenching, these steels offer one of the highest strength-to-weight ratios within the automotive industry. They are widely used in door intrusion beams, bumper reinforcements, side-impact structures, and energy-absorbing components where maximum rigidity is essential. Their widespread use in SUVs, trucks, and safety-critical components continues to expand as global safety standards rise.

The “Others” category includes ferrite-bainite (FB) and quenched-and-tempered (Q&T) UHSS grades. Ferrite-bainite grades offer a balanced combination of strength and toughness, making them commonly used in suspension components, truck frames, and industrial applications. Q&T steels achieve exceptional hardness and wear resistance, serving mining equipment, defense armor, and heavy structural applications. These specialty grades complement mainstream automotive UHSS by offering tailored performance attributes for specific high-stress, high-durability environments across the machinery, construction, and defense sectors, driving moderate growth in the foreseeable period.

By End Use

Stringent Global Crash Safety Standards Boosted Automotive & Transportation Segment Growth

Based on end use, the market is segmented into automotive & transportation, machinery & heavy equipment, construction & infrastructure, aerospace & defense, and others.

To know how our report can help streamline your business, Speak to Analyst

The automotive & transportation segment held the largest market share in 2024, driven by stringent global crash safety standards, the need for lightweighting, and the rapid expansion of EV platforms. UHSS grades such as DP, CP, martensitic, and PHS enable automakers to reduce vehicle weight by 30–40% while improving structural rigidity and crash performance. Key applications include body-in-white structures, door intrusion beams, bumpers, pillars, battery enclosures, and underbody protection. As global EV sales continue to expand, UHSS consumption per vehicle is rising proportionally, making this segment the backbone of UHSS demand across North America, Europe, China, Korea, and Japan.

Machinery and heavy equipment heavily rely on UHSS for improving durability, load capacity, and lifecycle performance under demanding operating conditions. Mining trucks, cranes, earthmovers, agricultural machinery, and lifting equipment require steels with superior wear resistance, high tensile strength, and fatigue tolerance. UHSS, including Q&T, ferrite-bainite, and martensitic grades, supports lighter yet stronger structural frames, booms, and load-bearing components. With the global construction machinery market projected to grow steadily, the use of UHSS in high-stress industrial applications continues to expand steadily.

UHSS is gaining traction in the construction and infrastructure sectors, where engineers increasingly seek stronger, lighter, and more durable materials for modern structural designs. UHSS enables higher load-bearing capacity, longer spans, and improved fatigue resistance in bridges, transmission towers, high-rise structures, and heavy infrastructure frameworks. Its strength advantage allows for the use of thinner sections and reduced material consumption, improving cost efficiency and structural resilience. As global infrastructure investment surges, UHSS adoption in cranes, steel frameworks, and high-strength structural beams will steadily increase, driving moderate demand for ultra high strength steel in the foreseeable period.

The “Others” segment includes rail, shipbuilding, energy, and general industrial applications that require robust, wear-resistant, and high-toughness materials. In railways, UHSS supports crash structures, couplers, and underframe components. Shipbuilding uses UHSS for lightweight structural panels, hull reinforcements, and high-strength decks. These diverse applications reflect UHSS’s growing role in heavy-duty, high-durability environments where strength, safety, and long service life are critical requirements.

Ultra High Strength Steel Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

North America Ultra High Strength Steel Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held the largest ultra high strength steel market share in 2024, valued at USD 4.48 billion, and is expected to lead the regional share in 2025. The region is the world’s fastest-growing UHSS market, fueled by its massive automotive sector, rapid electrification, and extensive expansion of hot-stamping facilities. Countries such as China, Japan, and South Korea are global leaders in PHS technology adoption, supported by deep collaboration between OEMs and regional steelmakers such as Baowu, POSCO, Nippon Steel, JFE Steel, and Hyundai Steel. The region’s construction, mining machinery, and infrastructure sectors further drive UHSS usage through demand for Q&T and ferrite-bainite grades.

In 2025, the China market is estimated to reach USD 2.76 billion. China is the largest UHSS-consuming country globally, driven by its dominant automotive production, which exceeds 30 million vehicles annually, and the rapid expansion of EV platforms. Chinese OEMs, including BYD, Geely, Changan, SAIC, and NIO, are integrating UHSS and giga-pascal-class steels across BIW structures, battery enclosures, and safety reinforcements.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe contributes a notable share of the global UHSS market. The region has the highest UHSS penetration per vehicle globally, supported by strict Euro NCAP safety standards, high adoption of hot-stamping, and leadership from OEMs such as Volkswagen, BMW, Stellantis, Volvo, and Renault. The region is a technological hub for press-hardened steel components, with extensive use of PHS in the range of 1500–2000 MPa in safety cage structures. Strong environmental commitments and lightweighting initiatives drive Europe’s shift toward multi-material BIW architectures, where UHSS remains essential for strength-critical areas. Major steelmakers, including ArcelorMittal, SSAB, ThyssenKrupp, and Voestalpine, continue to invest in green steel and hydrogen-based production routes, further shaping market growth.

North America

North America represents one of the most mature UHSS markets, driven primarily by the region’s robust automotive, heavy-duty truck, and machinery manufacturing sectors. The U.S. and Canada remain early adopters of martensitic and press-hardened steels due to stringent crash standards and the dominance of SUVs, pickups, and commercial vehicles, all of which require high-strength structural components. Rising EV production led by Tesla, GM, and Ford is further boosting UHSS demand for battery protection trays and crash structures. Additionally, adoption across construction, mining equipment, and defense programs in the U.S. further strengthens UHSS consumption.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions would witness a moderate growth in this market. The regions exhibit growing demand for UHSS, primarily driven by automotive production in Brazil and Mexico. Mexico, a major hub for export manufacturing, has rapidly increased UHSS penetration in globally aligned vehicle platforms from GM, VW, Nissan, and Stellantis. Brazil’s strong machinery, mining, and agricultural equipment industries drive demand for martensitic and quenched and tempered (Q&T) steels in structural and wear-resistant applications. Infrastructure modernization across LATAM continues to create opportunities for UHSS in bridges, cranes, and high-load construction structures.

The Middle East & Africa market for UHSS is expanding gradually, driven by large-scale construction megaprojects in the GCC, the modernization of heavy machinery fleets in mining-intensive countries, and increased defense procurement. GCC nations require UHSS for cranes, lifting structures, industrial frameworks, and armored defense platforms.

COMPETITIVE LANDSCAPE

Key Industry Players:

Companies Focus on Scaling Production to Strengthen Their Market Position

The global UHSS landscape is moderately consolidated, with competitiveness driven by hot-stamping infrastructure, metallurgical innovation, coating technologies, and regional supply integration. Major steel producers, including ArcelorMittal, SSAB, POSCO, Nippon Steel, JFE Steel, Baowu Group, Hyundai Steel, and U.S. Steel, continue to strengthen their positions by expanding advanced UHSS production lines, upgrading continuous annealing facilities, and integrating upstream ironmaking capabilities. Asian producers, particularly in China, Japan, and South Korea, are aggressively scaling press-hardened steel (PHS) and martensitic UHSS output to meet surging automotive and EV demand. Investments in PHS 1500–2000 MPa lines, Al-Si-coated UHSS, and hydrogen-ready steelmaking are emerging as key competitive differentiators. Meanwhile, European and North American steelmakers are prioritizing green-steel pathways, advanced coatings, and partnerships with automotive OEMs to secure long-term offtake agreements.

LIST OF KEY ULTRA HIGH STRENGTH STEEL COMPANIES PROFILED:

- Ansteel Group (China)

- ArcelorMittal (Luxembourg)

- China Baowu Steel Group Corporation Limited (China)

- Hyundai Steel (South Korea)

- JFE Steel (Japan)

- Nippon Steel (Japan)

- Nucor (USA)

- POSCO (South Korea)

- SSAB (Sweden)

- Tata Steel Europe (Netherlands)

KEY INDUSTRY DEVELOPMENTS:

- June 2025: As per the definitive Equity Purchase Agreement signed between ArcelorMittal and Nippon Steel Corporation (“NSC”) on October 11, 2024, ArcelorMittal completed the acquisition of the remaining stake in AM/NS Calvert, thereby solidifying full ownership. This consolidation may streamline UHSS production output and supply-chain control in North America.

- April 2025: SSAB announced a major expansion at its Alabama plant, including a new tempering furnace, to boost production of high-strength steels such as Hardox & Strenx. This strengthens their capacity to serve U.S. and global markets with premium UHSS steels.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 6.6% from 2025-2032 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Type, End Use, and Region |

| By Type |

|

| By End Use |

|

| By Geography |

· North America (By Type, End Use, and Country)

· Europe (By Type, End Use, and Country/Sub-region)

· Asia Pacific (By Type, End Use, and Country/Sub-region)

· Latin America (By Type, End Use, and Country/Sub-region)

· Middle East & Africa (By Type, End Use, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.13 billion in 2024 and is projected to reach USD 15.08 billion by 2032.

In 2024, the market value stood at USD 4.18 billion.

The market is expected to exhibit a CAGR of 6.6% during the forecast period (2025-2032).

The press hardened steel type segment led the market by type.

The key factors driving the market are the increasing use of UHSS in construction, mining, and heavy machinery for performance-driven applications.

ArcelorMittal, SSAB, POSCO, Nippon Steel, JFE Steel, Baowu Group, Hyundai Steel, and U.S. Steel are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

The trend of lightweighting and electric vehicles will favor the adoption of the product.

- 2019-2032

- 2024

- 2019-2023

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us