Upstream Services Market Size, Share & Industry Analysis, By Services (Exploration Services, Drilling Services, Completion Services, Production Services, and Well Intervention & Maintenance Services), By Application (Exploration Stage Services, Field Development Services, and Production & Maintenance Services), By Location (Onshore and Offshore), and Regional Forecast, 2026-2034

Upstream Services Market Size and Future Outlook

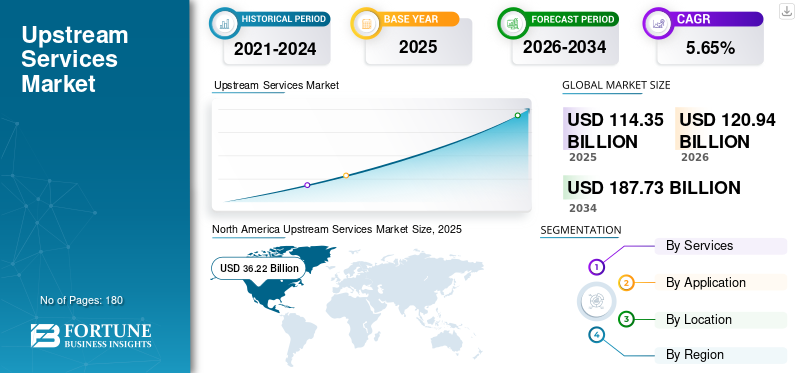

The upstream services market size was valued at USD 114.35 billion in 2025 and is expected to reach USD 120.94 billion by 2026. The market is projected to reach USD 187.73 billion by 2034, recording a CAGR of 5.65% during the forecast period. North America dominated the upstream services market with a market share of 31.67% in 2025. Moreover, the North America market is experiencing rapid growth, and the region features robust exploration, efficiency-focused operations, and sustainability efforts amid favorable regulations and major investments by leading firms.

- According to the International Energy Agency, global oil demand growth is slowing, expected to rise by 830 kb/d in 2025, while oil and gas demand is projected to peak before 2030. Despite this, upstream investment remains focused on offsetting a 5%-plus annual decline in existing fields, with new exploration facing pressure from net-zero goals.

Upstream services in the energy sector, often termed Exploration & Production (E&P), involve searching for, developing, and extracting underground or underwater raw materials, primarily crude oil and natural gas. Key activities include geological surveys, seismic data analysis, exploratory drilling, and operating wells.

SLB maintains its position as the world’s largest oilfield services provider, with a dominant, technology-driven presence in the global upstream oil and gas sector. As of late 2025/early 2026, SLB's prominence is driven by its strong international and offshore activity, a rapidly growing digital business, and the integration of ChampionX to bolster its production systems. SLB’s primary competitors are. Halliburton, Weatherford International, and others have a strong presence in North American land and completion services, while Baker Hughes is a major competitor in oilfield equipment and digital solutions.

Download Free sample to learn more about this report.

UPSTREAM SERVICES MARKET TRENDS

Shift Toward Unconventional Resources is Shaping the Market Trends

The market is increasingly oriented toward unconventional resources as operators seek to secure future supply amid maturing conventional fields. Companies are ramping up activity in shale oil, tight gas, coalbed methane, and other unconventional plays, supported by advances in horizontal drilling, hydraulic fracturing, and high-pressure pumping systems. This shift is driving demand for specialized drilling, completion, stimulation, and reservoir characterization services tailored to complex geologies and higher well counts. As more countries prioritize energy security and domestic production, upstream service providers are retooling portfolios and capabilities to capitalize on sustained unconventional development.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Upstream Capital Expenditure is Driving the Market Expansion

Increasing upstream capital expenditures (capex) is a primary driver propelling the upstream services market growth. Oil and gas industry operators are ramping up investments to explore and develop new reserves, particularly in deep water, shale, and unconventional plays, amid rising global energy demand and geopolitical tensions.

- According to the International Energy Forum, to sustain sufficient energy supplies, annual upstream investments must rise by USD 135 billion to reach USD 738 billion by 2030. This 2030 projection marks a 15% increase from last year's estimate and 41% from two years prior, mainly due to escalating costs and robust demand. Cumulatively, USD 4.3 trillion in spending will be required from 2025–2030, despite decelerating demand growth nearing a peak.

Service providers benefit from higher contract values, longer project durations, and technological upgrades like AI-driven optimization. National oil companies and independents alike prioritize capex to offset production declines and secure supply, ensuring robust market growth through the decade.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Rising Oil Price Volatility and Hampering Investment Decisions to Restrain Market Growth

Oil price volatility remains a significant restraint on the market, creating uncertainty that hampers investment decisions and project sanctioning. Sharp fluctuations driven by geopolitical tensions, OPEC+ policies, supply disruptions, and demand shifts from economic slowdowns or energy transitions erode operator confidence, leading to deferred drilling programs, reduced rig counts, and scaled-back service contracts. When oil prices dip below breakeven thresholds, marginal projects become uneconomic, slashing demand for high-cost services like hydraulic fracturing and seismic imaging. Service firms face margin compression, layoffs, and equipment idling, while volatile forecasts complicate long-term planning and capex allocation in an already cyclical industry.

MARKET OPPORTUNITIES

Carbon Capture and Low-Carbon Services are Expected to Create Lucrative Opportunities

Carbon capture and low-carbon services are poised to unlock lucrative opportunities in the upstream services market as operators navigate stringent emissions regulations and net-zero mandates. With global policies like the Europe's Carbon Border Adjustment Mechanism and the U.S. Inflation Reduction Act incentives, oil and gas companies are integrating carbon capture, utilization, and storage (CCUS) into upstream operations to decarbonize flaring, venting, and enhanced oil recovery. Service providers are capitalizing on demand for specialized engineering, injection well design, monitoring technologies, and CO2 handling infrastructure. Low-carbon hydrogen production from associated gas and methane abatement solutions further expands the addressable market, projected to surpass USD 10 billion by 2030, blending traditional expertise with green innovation.

MARKET CHALLENGES

Increasing Geopolitical Risks May Create Challenges for Market Growth

Geopolitical risks pose formidable challenges faced by the industry, disrupting supply chains, inflating costs, and delaying critical projects worldwide. Ongoing conflicts in the Middle East, Russia-Ukraine tensions, and U.S.-China trade frictions threaten access to key reserves, impose sanctions on equipment and technology transfers, and spike insurance premiums for high-risk regions like the South China Sea or Arctic frontiers. Operators face permit delays, force majeure declarations, and expatriate safety issues, while service providers grapple with logistics bottlenecks, tariff hikes, and volatile regional demand. These uncertainties deter long-term investments, fragment global operations, and heighten exposure to sudden policy shifts, undermining project economics in an already capital-intensive sector.

Segmentation Analysis

By Services

Drilling Services Led the Dominant Share Due to Sustained Rig Demand for Exploration in Shale

Based on services, the market is classified into exploration services, drilling services, completion services, production services, and well intervention & maintenance services.

In 2025, the drilling services segment dominated with the largest revenue share of 34.66%, driven by sustained rig demand for exploration and production in shale, deep water, and unconventional plays.

- In March 2026, the Government of India launches a historic oil and gas drilling campaign with ONGC and OIL, investing USD 385M starting early 2026. Four deep-sea wells target Andaman, Mahanadi, Saurashtra, and Bengal basins with BP's expertise to discover reserves and cut import reliance.

Meanwhile, completion services emerged as the fastest-growing segment with a CAGR of 6.71% during the forecast period, fueled by complex well designs, hydraulic fracturing innovations, and multilateral completions that boost recovery rates amid rising capex. This dynamic underscores operators' focus on efficiency and output maximization.

By Application

Field Development Services Segment Dominated Due to High Demand, Optimized Oil and Gas Production

Based on application, the market is classified into exploration stage services, field development services, and production & maintenance services.

In 2025, field development services dominated the upstream services market share with a 52.76% revenue, due to their critical role in optimizing production and reservoir management.

Meanwhile, exploration stage services are poised for significant growth with a CAGR of 5.21% during the forecast period, driven by rising global demand for new energy reserves, technological advancements in seismic imaging and drilling, and increasing investments in frontier basins. This dual dynamic underscores the sector's evolution toward efficient development alongside aggressive exploration efforts.

By Location

To know how our report can help streamline your business, Speak to Analyst

Onshore Segment Held the Largest Market Share Owing to Cost-Effective Operations and Rapid Scalability

Based on location, the market is bifurcated into onshore and offshore.

In 2025, the onshore segment dominated with the largest market share of 53.67%, propelled by cost-effective operations, vast shale reserves, and rapid scalability in regions like North America and the Middle East.

Meanwhile, the offshore segment is expected to witness significant growth with a CAGR of 5.18%, driven by deep water discoveries, floating production innovations, and investments in high-margin frontiers like Guyana and the Arctic, despite higher complexities and costs.

Upstream Services Market Regional Outlook

By region, the Market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

North America Upstream Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the third largest share in 2025, valued at USD 17.82 billion, and in 2026, the region is expected to hit USD 19.10 billion. Asia Pacific leads global market growth, driven by surging energy demand in China, India, and Australia. Key growth stems from deep water exploration in Indonesia, Malaysia, and offshore Australia, alongside onshore shale and gas projects.

China Upstream Services Market

The China market in 2025 valued at USD 6.95 billion, accounting for roughly 6.08% of the global revenues. The regional market is a cornerstone of its energy security strategy, dominated by state giants like CNPC, Sinopec, and CNOOC. It focuses on onshore mature fields, unconventional shale gas, tight oil, and emerging offshore deep water plays. Technological advances in fracking, enhanced recovery, and digital solutions drive efficiency amid import reduction efforts. Government policies prioritize domestic exploration to fuel economic growth and transition goals.

India Upstream Services Market

India's market is projected to be one of the largest worldwide, with 2025 revenues valued at around USD 2.51 billion, representing approximately 2.20% of the global revenue.

Japan Upstream Services Market

The Japanese market in 2025 valued at USD 0.80 billion, accounting for approximately 0.70% of global revenues.

North America

The North America market held USD 36.22 billion in 2025. North America's market dominates globally, driven by shale innovations in key basins and advanced drilling technologies. It features robust exploration, efficiency-focused operations, and sustainability efforts amid favorable regulations and major investments by leading firms.

U.S. Upstream Services Market

With North America's strong contribution and the U.S. dominance in the region, the U.S. market was valued at USD 32.08 billion in 2025, accounting for roughly 28.05% of the global revenue.

The regional market thrives on shale innovation, advanced technologies, and efficiency gains in key basins, led by majors amid strong energy demand.

Europe

Europe is projected to grow at 4.50% over the coming years and to reach a valuation of USD 11.47 billion by 2026. Europe's market shifts toward sustainable practices amid strict regulations, with a North Sea focus, cleaner tech investments, and energy transition led by Norway and U.K firms.

Germany Upstream Services Market

The German market in 2025 valued at USD 0.75 billion. It is projected to reach USD 0.79 billion by 2026, representing approximately 0.65% of the global industry revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 16.12 billion in 2026. Latin America's market thrives on offshore Brazil pre-salt, Argentina shale, and Mexico reforms, blending deep water tech, NOCs, and frontier exploration.

Brazil Upstream Services Market

Brazil's market valued at USD 7.24 billion in 2025, accounting for a very minor share of the global market revenue.

Middle East & Africa

The Middle East & Africa accounted for the second largest market share of 29.68% in 2025 and is expected to witness significant growth in this market space during the forecast period. The region is set to reach a valuation of USD 36.15 billion in 2026. The regional market leverages vast reserves, operational costs, production, and mega-projects led by NOCs in Saudi Arabia, the UAE, and Nigeria.

GCC Upstream Services Market

The GCC market was valued at USD 20.01 billion in 2025, accounting for around 17.50% of the global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Business Expansion and Technological Advancements Among the Players to Gain a Competitive Edge

The global industry is considered consolidated, featuring a mix of major global players and numerous regional market players, including SLB, Halliburton Company, Baker Hughes Company, Weatherford International plc, NOV Inc. (National Oilwell Varco), and others. For instance, in March 2025, TGS launched advanced imaging centers in Rio de Janeiro for Petrobras, focusing on OBN and 4D imaging in Brazil's Campos and Santos basins. These facilities use 4D FWI technology and hybrid solutions to boost offshore exploration, production, and resource recovery. Such developments are expected to fuel market growth during the forecast period.

LIST OF KEY UPSTREAM SERVICES COMPANIES PROFILED

- SLB (U.S.)

- Halliburton Company (U.S.)

- Baker Hughes Company (U.S.)

- Weatherford International plc (U.S.)

- NOV Inc. (National Oilwell Varco) (U.S.)

- TechnipFMC plc (U.S.)

- Saipem S.p.A. (Italy)

- Transocean Ltd. (Switzerland)

- COSL (China Oilfield Services Limited) (China)

- Petrofac Limited (U.K)

- Aker Solutions ASA (Norway)

- Oceaneering International Inc. (U.S.)

- Helmerich & Payne, Inc. (U.S.)

- Patterson-UTI Energy, Inc. (U.S.)

- Nabors Industries Ltd. (U.K)

KEY INDUSTRY DEVELOPMENTS

- March 2026: ExxonMobil and Halliburton achieved the world's first fully closed-loop automated geological well placement in offshore Guyana, integrating rig automation, subsurface interpretation, and real-time hydraulics for superior efficiency and reservoir contact.

- March 2026: BP confirmed the start-up of gas production from Angola's Quiluma field in the New Gas Consortium project, operated by Azule Energy. This milestone non-associated gas development feeds the Angola LNG plant, enhancing regional energy security through strategic partnerships.

- January 2026: ONGC launched Pragya-AIX, a unified AI platform integrating over 26 intelligent apps for upstream operations, advancing from pilots to practical use. It enhances seismic analytics, production optimization, and smart field monitoring to boost efficiency and India's energy security.

- November 2025: Eni and Petronas formed a 50:50 joint venture, NewCo, to launch eight upstream gas projects, four each in Indonesia and Malaysia, over three years, investing heavily in reserves development and exploration for sustainable regional energy growth.

- October 2025: BP started production at its sixth major upstream project of 2025, the Murlach field in the U.K North Sea. This subsea tieback adds peak capacity to the ETAP hub, advancing plans for ten projects by 2027 amid efficient delivery.

REPORT COVERAGE

The global upstream services market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the Market dynamics and industry trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market report also encompasses a detailed competitive landscape, including market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.65% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Services, Application, Location, and Region |

| By Services |

|

| By Application |

|

| By Location |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 114.35 billion in 2025 and is projected to reach USD 187.73 billion by 2034.

In 2025, the North American market value stood at USD 36.22 billion.

The market is expected to exhibit a CAGR of 5.65% during the forecast period.

The onshore sector led the location segment.

Increasing upstream capital expenditures (capex) is a primary driver propelling the market forward.

SLB, Halliburton Company, Baker Hughes Company, Weatherford International plc, and NOV Inc. (National Oilwell Varco) are some of the prominent players in the Market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us