Utility Drones Market Size, Share & Industry Analysis, By End-Use Industry (Energy & Power, Oil & Gas, Telecommunications and Utilities), By Payload Capacity (Lightweight Drones, Medium Weight Drones and Heavy-Duty Drones), By Drone Type (Fixed-Wing Drones, Rotary-Wing Drones and Hybrid Drones), By Application (Power Line Inspection, Substation Inspection, Vegetation Management, Emergency Response, Monitoring & Surveillance and Mapping & Modeling), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

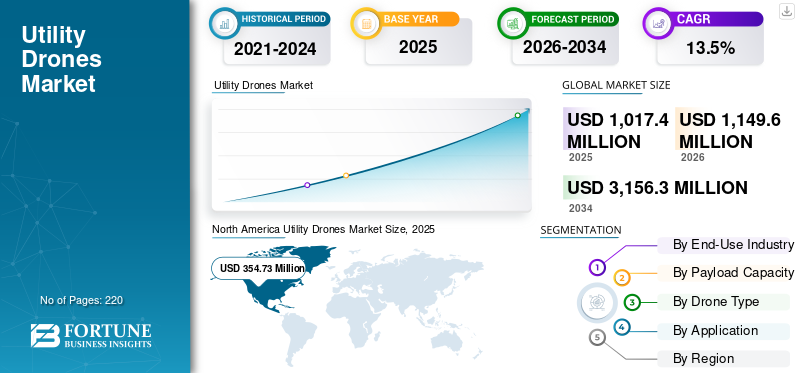

The global Utility Drones market size was valued at USD 1,017.4 million in 2025. The market is projected to grow from USD 1,149.6 million in 2026 to USD 3,156.3 million by 2034, exhibiting a CAGR of 13.5% during the forecast period. North America dominated the global market with a market share of 34.87% in 2025.

The market has evolved into a strategic pillar of the global aviation aftermarket, rather than a tactical cost-cutting tool. Airlines, MROs, lessors and OEM-affiliated providers are increasingly using recycled serviceable material to manage escalating maintenance costs, offset long lead times for new spares and allows aging fleets fly longer. Most of its value is concentrated in engine and high-value unmanned systems tied to narrow body workhorses, with widebody and regional fleets, contributing to a smaller, but growing share. North America and Europe remain the core hubs for teardown, repair and distribution, while Asia Pacific and the Middle East are rapidly expanding their role as fleets and local MRO capacity scale up. Competition is intensifying between independent traders, airline maintenance repair and overhaul units and OEM-branded USM programs, with digital platforms slowly improving transparency around availability, traceability and pricing, and pushing the market toward more professional, programmatic, and data-driven material strategies.

Key players in the utility drones landscape includes independents, airline MROs, and OEM-linked providers. A J Walter Aviation Limited and AJ Walter Aviation Limited lead in global component pooling and availability solutions. AAR Corp., AerSale Inc., GA Telesis, LLC, and Delta TechOps drive much of the teardown and trading volume, feeding USM into engine and component maintenance. Boeing Company and General Electric increasingly integrate USM into OEM support contracts, while HEICO Corporation and Liebherr Group add depth in specialized components, systems and lifecycle support.

Download Free sample to learn more about this report.

Utility Drones Market KEY TAKEAWAYS

- 2025 Market Size: USD 1,017.4 million

- 2026 Market Size: USD 1,149.6 million

- 2034 Forecast Market Size: USD 3,156.3 million

- CAGR: 13.5% from 2026–2034

- North America dominated the market with a 34.87% share in 2025.

- The energy & power segment accounted for the largest market share in 2026.

- The lightweight drones segment is projected to hold a 52.23% share in 2026.

North America

USD 354.7 million in 2025. Driven by aging infrastructure, wildfire risk, storm damage response, and utility inspection automation.

Europe

USD 298.4 million in 2026. Growth supported by decarbonization goals, strict regulations, and renewable energy asset monitoring.

Asia Pacific

USD 341.8 million in 2026. Growth driven by rapid grid expansion, urbanization, and large-scale renewable energy projects.

U.S.

USD 293.3 million in 2026. Demand driven by grid modernization, wildfire risk, and large-scale utility inspection needs.

Rest of the World

USD 109.7 million in 2026. Growth driven by increasing adoption for remote monitoring of pipelines, power lines, and infrastructure in challenging terrains across Latin America, Middle East & Africa.

Read More

MARKET DYNAMICS

Market Drivers

Reliability Requirements, Climate Risk and Cost Pressure on Utilities Are Boosting Market Growth

Utility drones market growth is driven by rising reliability expectations, climate-related risk, and economic constraints. Aging infrastructure and increasing load demand require more frequent inspections to prevent outages and failures. At the same time, extreme weather events and wildfire risk have also intensified scrutiny on vegetation management and asset condition. Regulators and insurers are demanding clearer evidence of proactive risk mitigation. Drones provide a cost-effective way to increase inspection frequency and documentation without proportionally increasing field crews or helicopter hours. Additionally, drone inspections reduce exposure to live conductors, elevated structures, and hazardous terrain, thus lowering operational risk. Labor availability also plays a significant role, as utilities face shortage of skilled technicians and longer training cycles. Drones also aid in extending workforce productivity by enabling remote assessment and targeted field interventions. Progress in BVLOS permissions and traffic management frameworks further reinforces these drivers by making long-distance inspections operationally viable.

Market Restraints

Regulatory Uncertainty and Enterprise Integration Gaps to Hamper Market Growth

Regulatory limitations remain the most significant restraint. BVLOS approvals are still inconsistent across regions and often require case-by-case justification, slowing large-scale deployment. This uncertainty discourages utilities from committing to full network-level drone programs. Internally, utilities operate within conservative governance structures, where safety, labor agreements, and cybersecurity reviews can delay product adoption. Technical constraints such as limited endurance, payload capacity and sensitivity to weather conditions also restrict operations in certain environments. Integration challenges further reduce the comprehended value. Drone data is often soloed in standalone platforms rather than embedding into GIS, asset management and outage systems. Without seamless integration, drone insights do not consistently translate into maintenance actions. Additionally, the fragmented supplier landscape raises concern about long-term vendor stability, interoperability, and support, particularly for utilities seeking multi-decade asset strategies.

UTILITY DRONES MARKET TRENDS

Transition from Standalone Drone Flights to Integrated Utility Inspection Systems Driving Market Expansion

The market is moving from isolated, pilot-level deployments to integrated inspection systems embedded in daily utility operations. Utilities are standardizing drone missions for corridor patrols, substation checks, vegetation assessment and post-event damage surveys. This shift is driven by the need for repeatability, auditability and scalability rather than one-off visual inspections. Progress in BVLOS frameworks and managed airspace concepts is enabling longer and linear inspections that aligns with utility asset layouts. At the same time, value is increasingly concentrated in software and data workflows rather than airframes. Utilities are adopting standard payload stacks such as RGB, thermal and LiDAR, combined with AI-based defect detection and automated reporting. Docked and “drone-in-a-box” systems are gaining traction at substations and depots, enabling scheduled or event-triggered flights without on-site crews. Overall, the market trend points toward drones becoming a permanent sensing layer within the utility digital ecosystem, feeding GIS, asset management and predictive maintenance systems with consistent as well as structured data.

Download Free sample to learn more about this report.

MARKET OPPORTUNITIES

Large-Scale Linear Infrastructure and Recurring Data-Driven Services to Accentuate Market Growth

The primary opportunity lies in under-penetration of drones across global utility infrastructure. Most transmission lines, distribution networks, pipelines and towers are still using trucks, climbers, or helicopters, which limits inspection frequency and data quality. Drones enable higher inspection coverage at lower marginal cost, creating a strong case for systematic adoption. As utilities increase inspection frequency, they generate longitudinal datasets that support condition-based maintenance, vegetation optimization and asset life-extension decisions. This creates downstream opportunities in analytics, digital twins and compliance reporting. Emerging markets represent additional upside, as new grid and telecom deployments can integrate drone inspection from the outset rather than retrofitting legacy processes. Commercial opportunity extends beyond hardware sales into multi-year inspection-as-a-service contracts, AI analytics subscriptions, emergency-response readiness programs, and long-term framework agreements. As airspace frameworks mature, utilities are expected to expand drone use from high-risk corridors to network-wide coverage, significantly enlarging the market.

MARKET CHALLENGES

Scaling Operations and Converting Data into Actionable Outcomes are Major Challenges in the Market

The central market challenge is scaling drone programs from pilot projects to enterprise-wide operations. Utilities must establish standard operating procedures, fleet governance, training frameworks and safety management systems suitable for continuous use. Airspace coordination becomes increasingly complex as the number of simultaneous drone operations grows, especially during storm response or emergency situations. On the data side, utilities face challenge in managing and analyzing large volumes of imagery and LiDAR. AI tools must deliver consistent, explainable and auditable outputs to gain trust from engineers, regulators and insurers. Without this trust, decision-makers default to manual validation, reducing efficiency gains. Procurement and standardization also pose challenges, as utilities must balance security requirements, hardware restrictions and long-term vendor viability. Ultimately, success depends on treating drones as a core operational capability, governed and integrated similar any other critical utility system.

SEGMENTATION ANALYSIS

By End-Use Industry

Grid Reliability and Safety Pressures Drive Energy & Power Segment Growth

By end-use industry, the market is segmented into energy & power, oil & gas, telecommunications, and utilities.

The energy & power segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 41.77% share. Demand in the energy & power segment is rising as utilities confront stricter reliability standards, wildfire risk and more frequent extreme weather. Drones enable faster, safer inspection of high-voltage lines, towers, substations and renewables assets, replacing many helicopter flights and manual climbs while generating detailed data for predictive maintenance and grid planning.

The telecommunications segment is expected to grow at a CAGR of 14.4% over the forecast period.

By Payload Capacity

Low Cost and Easy Deployment Boosts Lightweight Drone Segment Growth

By payload capacity the market is classified into lightweight drones, medium weight drones and heavy-duty drones.

The lightweight drones segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 52.23% share. Lightweight drones are in demand as they are cheap, easy to deploy from any service vehicle, and generally easier to certify and operate under existing rules. Utilities and contractors use them for visual and thermal spot checks, tower tops, rooftop solar and quick fault-locating, without needing complex logistics or specialist pilots.

The medium weight drones segment is expected to grow at a CAGR of 14.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Drone Type

Operational Flexibility Makes Rotary-Wing Drones the Workhorse

By drone type segment, the market is classified into fixed-wing drones, rotary-wing drones, and hybrid drones.

The rotary-wing drones segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 67.31% share. Rotary-wing drones are high in demand as they can hover and maneuver in tight substation spaces, and inspect towers or fittings from any angle. Their vertical take-off and landing as well as short launch requirements fit field crews’ workflows, allowing rapid deployment from rough terrain, access tracks or rooftops without runways or elaborate ground infrastructure.

The hybrid drones segment is expected to grow at a CAGR of 14.4% over the forecast period.

By Application

Linear Asset Complexity Accelerates Power Line Inspection Segment Expansion

By application segment, the market is classified into power line inspection, substation inspection, vegetation management, emergency response, monitoring & surveillance, and mapping & modeling.

The power line inspection segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with 37.07% share. Demand for power line inspection is growing as operators manage thousands of kilometers of overhead lines exposed to weather, vegetation and theft. Drones provide detailed visual, thermal and sometimes LiDAR data on insulators, conductors and hardware, supporting condition-based maintenance, wildfire prevention programs, outage reduction and documented evidence for regulators and insurers.

The vegetation management segment is expected to grow at a CAGR of 15.8% over the forecast period.

UTILITY DRONES MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and Rest of the World.

North America

North America Utility Drones Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

The North America held the dominant utility drones market share in 2024 valuing at USD 314.8 million and also took the leading share in 2025 with USD 354.7 million value. Demand in North America is powered by aging grid and pipeline assets, wildfire and storm risk, and strong pressure to cut inspection costs. Utilities and energy companies are moving from helicopter and ground patrols to drones for safer, more frequent inspections, vegetation management, and rapid post-storm assessment across large territories.

In 2026, U.S. market is estimated to reach USD 293.3 million. In the U.S., demand is driven by wildfire liability, storm outages, regulatory scrutiny and massive grid-modernization programs. Investor-owned utilities, co-ops and pipeline operators are scaling drone fleets for vegetation patrols, thermal hotspot detection and rapid damage surveys, aiming to cut truck rolls, limit helicopter use, and document compliance more rigorously.

Europe

During the forecast period, European region is projected to record the growth rate of 12.7% and touch the valuation of USD 298.4 million in 2026. In Europe, demand is driven by aggressive decarbonisation targets, cross-border transmission projects, and strict safety and environmental rules. TSOs, DSOs and large utilities use drones for line inspection, wind and solar asset checks, and corridor mapping, helping meet regulatory reporting needs while coping with skilled-labour shortages and high operational costs.

Asia Pacific

The market in Asia Pacific is estimated to reach USD 341.8 million in 2026. Asia Pacific market growth is fueled by rapid grid expansion, heavy urbanization and large-scale renewables build-out in China, India and Southeast Asia. Governments are more open to drone-friendly regulations and utilities use drones to monitor long new corridors, hilly terrain and offshore assets, skipping straight from manual methods to digital inspection workflows.

Rest of the World

Rest of the World market in 2026 is set to record USD 109.7 million as its valuation. In the Middle East & Africa and Latin America, demand is emerging as utilities and energy firms seek low-cost ways to monitor remote lines, pipelines and desert or jungle corridors. Drones reduce the need for dangerous field travel, support new megaprojects, and give operators modern asset data without massive legacy systems.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Rapidly Scaling Capabilities to Sustain the Market Competition

Key players in the market combine airframe manufacturing, payload integration and data services. AeroVironment leads in small tactical and long-endurance platforms increasingly adapted for power and pipeline inspection. Autel Robotics, Parrot, and Yuneec provide versatile multirotor systems widely used by utilities and contractors for tower, line, and substation surveys. PrecisionHawk, Sky-Futures, Terra Drone, Measure, HEMAV and Delair focus more on turnkey inspection programs, analytics and regulatory-compliant operations, translating raw imagery and LiDAR into actionable asset intelligence. Many bundle flight services, cloud platforms, and AI defect detection into multi-year contracts with grid, oil and gas, and telecom operators. Together, this group is pushing standards for BVLOS operations, safety cases, and data quality, while driving down per-mile inspection costs and accelerating the shift from ad-hoc pilot projects to scaled, enterprise-wide drone programs. Their strategies emphasize recurring revenue, interoperability with utility asset systems, and regional partnerships to win regulated tenders.

LIST OF KEY UTILITY DRONES COMPANIES PROFILED

- AeroVironment, Inc. (U.S.)

- Autel Robotics (U.S.)

- Parrot Drone S.A.S. (Switzerland)

- Yuneec (China)

- PrecisionHawk (U.S.)

- Sky-Futures (U.K.)

- Terra Drone (Japan)

- Measure (U.S.)

- HEMAV (Spain)

- Delair (France)

KEY INDUSTRY DEVELOPMENTS

- November 2025 - Larsen & Toubro (L&T) has entered a strategic partnership with U.S.-based General Atomics Aeronautical Systems, Inc. (GA-ASI) to build Medium Altitude Long Endurance (MALE) remotely piloted aircraft systems within India, marking a notable boost for the country’s defence and manufacturing ecosystem.

- September 2025 - Volatus Aerospace Inc. has signed a multi-year contract with one of North America’s largest power utilities. Under this deal, Volatus will deliver RPAS-based inspection, mapping, and data services across roughly 100,000 miles of transmission and distribution lines.

- August 2025 - The NATO Support and Procurement Agency (NSPA) has chosen U.S. autonomous drone maker Skydio, together with its European partner COBBS BELUX BV, under a new framework to provide and support small ISR drones for NATO member countries within the Uncrewed Aerial Systems Support Partnership.

- July 2025 - Virginia Tech’s Mid-Atlantic Aviation Partnership (MAAP) has helped bring into operation the first uncrewed aircraft traffic management (UTM) system in the U.S.. Designed to cut down drone-on-drone collision risks, this system is now available to any public or private organization seeking to improve the safety of its drone operations.

- May 2025 - Paras Defence and Space Technologies Limited has signed an MoU with Israel-based Heven Drones Ltd. to form a joint venture in India focused on manufacturing logistics and cargo drones.

REPORT COVERAGE

This report delivers a tight, deep dive into the Utility Drones ecosystem, profiling leading platform OEMs, payload and sensor providers, flight-service operators, data/analytics specialists, and long-term fleet and maintenance partners. It maps the core solution stack airframes, navigation and control systems, payloads (EO/IR, LiDAR, corona, gas detection), software, and data platforms and the main use cases across power grids, oil & gas networks, telecom towers, and municipal utilities. It charts regulatory milestones, BVLOS and corridor-permission progress, grid and pipeline inspection programs, vegetation-management campaigns, and emergency-response deployments already in motion, and pinpoints the shifts setting up the next wave of drone-enabled inspection and monitoring. Taken together, these threads explain the recent upswing in utility drone adoption and what will propel the market’s next stage of growth.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 13.5% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By End-Use Industry · Energy & Power · Oil & Gas · Telecommunications · Utilities |

|

By Payload Capacity · Lightweight Drones · Medium Weight Drones · Heavy-Duty Drones |

|

|

By Drone Type · Fixed-Wing Drones · Rotary-Wing Drones · Hybrid Drones |

|

|

By Application · Power Line Inspection · Substation Inspection · Vegetation Management · Emergency Response · Monitoring & Surveillance · Mapping & Modeling |

|

|

By Geography · North America (By End-Use Industry, Payload Capacity, Drone Type, and Application) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By End-Use Industry, Payload Capacity, Drone Type, and Application) o U.K. (By End-Use Industry) o Germany (By End-Use Industry) o France (By End-Use Industry) o Russia (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By End-Use Industry, Payload Capacity, Drone Type, and Application) o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Rest of the World (By End-Use Industry, Payload Capacity, Drone Type, and Application) o Middle East and Africa (By End-Use Industry) o Latin America (By End-Use Industry) |

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 1,017.4 million in 2025 and is estimated to reach USD 3,156.3 million by 2034.

The market is growing at a CAGR of 13.5% during the projection period (2026-2034).

The Energy & Power segment is estimated to be the leading segment in this market during the forecast period.

The Lightweight Drones segment is estimated to be the leading segment in this market during the forecast period.

AeroVironment, Inc. (U.S.), Autel Robotics (U.S.), Parrot Drone S.A.S. (Switzerland), Yuneec (China), PrecisionHawk (U.S.), Sky-Futures (U.K.) some of the leading players in the market.

North America is projected to be the largest shareholder in the market.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us