Vehicle Scanner Market Size, Share & Industry Analysis, By Product Type (OBD Diagnostic Scanners, Multi-System Diagnostic Scanners, OEM Branded Diagnostic Tools, and Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles), By End-User (Dealerships, Independent Workshops, DIY Consumers, and Others), By Propulsion (Internal Combustion Engine and Electric), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

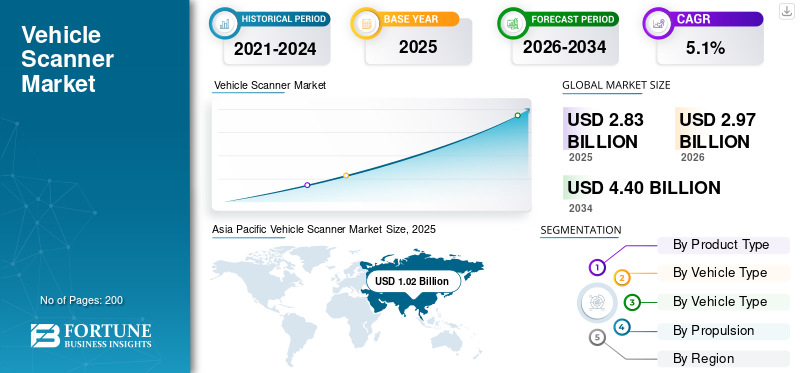

The global vehicle scanner market size was valued at USD 2.83 billion in 2025. The market is projected to grow from USD 2.97 billion in 2026 to USD 4.40 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period. Asia Pacific dominated the global vehicle scanner market with a market share of 36.04% in 2025.

A vehicle scanner is a diagnostic and inspection device designed to read, analyze, and interpret data generated by a vehicle’s electronic systems. Within the vehicle scanner industry, these tools range from diagnostic scanners used in repair environments to advanced vehicle scan systems applied in drive-through and under-vehicle inspections for security, maintenance, and compliance purposes. At their core, vehicle scanners enable fault detection, system monitoring, and operational validation across different vehicle platforms.

The relevance of vehicle scanners has increased significantly as vehicles have become more software-driven and electronically complex. Modern vehicles rely on multiple electronic control units, sensors, and communication networks, making traditional mechanical inspection insufficient. As a result, vehicle scanning technology has become essential not only for repair and maintenance but also for safety assurance, emissions compliance, fleet monitoring, and infrastructure-linked inspection systems. Governments, transport authorities, workshops, and fleet operators increasingly depend on global vehicle scanner solutions to maintain operational efficiency and regulatory alignment.

Currently, the demand for vehicle scanners is rising due to multiple converging factors. Growth in vehicle ownership, expanding infrastructure development such as smart transport hubs and inspection facilities, and increasing vehicle electrification are reshaping the key market dynamics. Additionally, advancements in artificial intelligence and machine learning are enabling scanners to deliver predictive diagnostics, automated fault recognition, and faster inspection cycles. These developments are expected to support sustained market growth during the market during the forecast period, particularly in high-volume and emerging regions.

Manufacturers are actively innovating to strengthen their competitive edge in the market. Key players such as Thinkcar, Denso, and ZF are focusing on software-driven platforms, secure data access, cloud-enabled diagnostics, and modular scanner architectures. Integration of AI-based analytics, enhanced imaging capabilities, and compatibility across multiple vehicle structure type configurations are becoming central to product development strategies, positioning vehicle scanners as critical tools in the evolving automotive ecosystem.

Download Free sample to learn more about this report.

Vehicle Scanner Market KEY TAKEAWAYS

- 2025 Market Size: USD 2.83 billion

- 2026 Market Size: USD 2.97 billion

- 2034 Forecast Market Size: USD 4.40 billion

- CAGR: 5.1% from 2026–2034

- Asia Pacific dominated the market with a 36.04% share in 2025.

- OEM branded diagnostic tools segment is projected to grow at a CAGR of 7.7%.

- Heavy commercial vehicles segment is projected to grow at a CAGR of 7.2%.

Asia Pacific

Asia Pacific Large vehicle parc and fast EV adoption driving scanner demand.

North America

North America Mature market driven by ADAS, secure access, and software updates.

Europe

Europe Strong workshop network and advanced diagnostics adoption supporting growth.

U.S.

U.S. Large vehicle base and high repair activity driving steady demand for diagnostic tools.

Japan

Japan Advanced automotive ecosystem and high service standards supporting premium scanner adoption.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Vehicle Electronics and ADAS Complexity are Pushing Workshops Toward Higher-End Diagnostics

Modern vehicles integrate more ECUs, networks, and safety systems, increasing diagnostic steps and the need for multi-system tools that can run deeper tests and calibrations. As software-driven faults rise, repairers invest in capable scanners and updated coverage to maintain throughput and first-time-fix performance. This is expected to boost the vehicle scanner market growth in the coming years.

- For instance, Bosch’s ADS X software updates emphasize expanding model-year coverage and additional ADAS calibrations, evidence that growing complexity is driving ongoing diagnostic tool upgrades.

MARKET RESTRAINTS

Secure Gateways and Restricted Vehicle Data Access Increase Friction and Cost for Non-OEM Repairers

As OEMs protect certain functions behind authentication, independent workshops may face added registration steps, subscriptions, and tool compatibility limits. This can slow adoption for smaller garages and shift some advanced repair work back to dealerships, constraining broader market penetration.

- For example, the Auto Care Association warns that direct repair data access is increasingly threatened as data moves wirelessly to OEMs, complicating independent diagnostics and repair.

MARKET OPPORTUNITIES

Standardized Programming and Pass-thru Workflows Expand Demand Beyond Diagnostics into Reprogramming

As module updates and replacements grow, scanners paired with J2534-compatible interfaces and guided procedures can unlock new revenue streams in programming, coding, and setup. Vendors that package hardware with practical software guidance and support can win share among general repair and collision shops.

- For example, SAE J2534 is designed so OEM reprogramming applications can work with multiple interface tools supporting broader adoption of pass-thru programming hardware across brands.

MARKET CHALLENGES

Keeping Coverage Current Across Fast-changing Model Years Strains Smaller Tool Brands and Workshops

Vehicle scanner value increasingly depends on frequent updates, validated functions, and accurate procedures. Maintaining broad coverage across regions and powertrains requires high engineering effort, data licensing, testing, and customer support, raising subscription expectations and creating dissatisfaction when gaps appear.

- For example, Bosch release notes highlight thousands of new special tests and expanding 2024–2025 coverage, illustrating the scale and pace required to keep diagnostic platforms current.

VEHICLE SCANNER MARKET TRENDS

Diagnostic Platforms are Converging with Security Validation and Authenticated Access

To balance repair access with theft prevention and cybersecurity, the market is moving toward verified users, validated tools, and logged security transactions. This trend favors vendors that can integrate secure gateway access and identity workflows without disrupting workshop productivity.

- For instance, NASTF notes that aftermarket tool companies began using its security validation process in 2024 to reduce theft and discourage illicit use of diagnostic tools.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Multi-system Diagnostic Scanners Lead Market as They Comprise a Wide Range of Vehicle Functions

On the basis of product type, the market is segmented into OBD diagnostic scanners, multi-system diagnostic scanners, OEM branded diagnostic tools, and others.

Multi-system diagnostic scanners lead by value as they cover the widest set of vehicle functions beyond generic OBD codes, enabling live data, bi-directional tests, resets, and deeper troubleshooting across multiple ECUs. Workshops prioritize these tools to handle diverse makes and model years efficiently, especially as ADAS and network protocols expand. OBD-only tools remain lower priced and DIY-skewed.

- For instance, LAUNCH’s X-431 EURO is positioned as a modular, high-end diagnostics tool for workshop needs, reflecting strong demand for multi-system capability.

The OEM branded diagnostic tools segment is expected to grow at a CAGR of 7.7% over the forecast period.

By Vehicle Type

High Electronic Complexity Sustains Passenger Vehicle Scanner Dominance

On the basis of vehicle type, the market is segmented into passenger cars, light commercial vehicles, and heavy commercial vehicles.

Passenger cars dominate market value as they account for the largest repair population across dealerships, independent workshops, and DIY users. They also carry high electronics content body modules, infotainment, ADAS, and (increasingly) electrified systems, driving demand for multi-system diagnostics and frequent software updates. Commercial fleets often centralize tools, reducing unit purchases per vehicle.

- For instance, EPA’s OBD requirements for light-duty vehicles drove widespread diagnostic accessibility, supporting long-term scanner adoption in the passenger vehicle service ecosystem.

The heavy commercial vehicles segment is expected to grow at a CAGR of 7.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End-User

Independent Workshops Lead Demand Through Multi-Brand Servicing

On the basis of end-user, the market is segmented into dealerships, independent workshops, DIY consumers, and others.

Independent workshops dominate scanner demand as they service a broad, multi-brand vehicle base and must diagnose efficiently without OEM-exclusive infrastructure. They also face daily pressure to deliver quick, accurate repairs, making scanners a core productivity tool. As secure gateways and ADAS expand, independents increasingly upgrade equipment to maintain service coverage and avoid losing work to dealerships.

- For example, Snap-on’s Secure Vehicle Gateway offering targets aftermarket scan tools needing authenticated access, supporting independent workshop capability on gateway-protected vehicles.

The others segment is set to rise at a CAGR of 9.6% over the forecast period.

By Propulsion

Large Installed Internal Combustion Engine Fleet Maintains Its Scanner Market Leadership

On the basis of propulsion, the market is segmented into internal combustion engine and electric.

The internal combustion engine segment dominates scanner value today as the global fleet is still primarily ICE, creating the largest installed base requiring maintenance, emissions diagnostics, and drivability troubleshooting. EV growth increases diagnostic intensity per vehicle, but fleet composition changes gradually. Over time, the EV share will lift demand for high-voltage diagnostics and software-led workflows, but ICE remains the core volume driver in most regions.

- For instance, EPA’s light-duty OBD framework underpins widespread diagnostics for gasoline operation in the U.S., reinforcing the long-standing dominance of ICE-related diagnostic needs.

The electric segment is expected to grow at the highest CAGR of 10.9% over the forecast period.

Vehicle Scanner Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Vehicle Scanner Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific leads the vehicle scanner market share due to sheer vehicle parc scale, a dense independent repair ecosystem, and rapid adoption of affordable professional scanners across emerging markets. China’s high new-vehicle output and fast electrification increase diagnostic intensity and the need for updated software coverage. India and Southeast Asia add volume through expanding workshop networks and growing car parc, while Japan and Korea maintain sophisticated service standards that support premium diagnostic tool usage.

- For instance, IEA highlights accelerating EV trends, which are particularly influential in Asia’s largest markets and raise demand for advanced diagnostics and battery-related troubleshooting.

North America

North America is a mature but expanding market driven by secure gateway access needs, ADAS-related diagnostic demand, and frequent software update cycles for new model-year coverage. The U.S. remains the anchor due to a large installed vehicle base, strong independent workshop presence, and high penetration of professional tools in both general repair and collision environments, supporting steady replacement and upgrade demand.

Europe

Europe’s growth is supported by high diagnostic sophistication, strong independent workshop networks, and increasing secure access requirements that push upgrades to validated, updatable platforms. ADAS calibration readiness and multi-brand coverage remain central purchase drivers, while electrification increases the need for advanced workflows and high-voltage service support.

Rest of the World

The rest of the World grows through workshop digitization and the rising adoption of cost-effective professional scanners as vehicle fleets modernize. The strongest momentum is typically in urban repair hubs, where mixed vehicle brands and imported models increase multi-system diagnostic demand. Over time, training and authenticated access will shape upgrade cycles in key markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Software-Centric Innovation Shapes Competition in Market

The global vehicle scanner market is moderately consolidated, comprising established diagnostic equipment manufacturers, vehicle inspection technology providers, and regional solution developers competing through advancements in software intelligence, system accuracy, and multi-vehicle compatibility. Companies are increasingly focusing on integrated vehicle scan systems, enhanced imaging precision, and AI-enabled analytics to support both diagnostic and inspection-based applications.

Leading participants such as Snap-on, Bosch Diagnostics, Autel, LAUNCH, and TEXA play a significant role in shaping the vehicle scanner industry. Snap-on continues to strengthen its position by investing in software-led diagnostic ecosystems that emphasize workflow efficiency and secure access. Bosch Diagnostics focuses on scalable diagnostic platforms with frequent software updates and expanded system coverage. Autel and LAUNCH emphasize feature-rich, multi-system scanners that balance affordability with professional-grade capabilities, particularly for independent workshops and fleet operators.

Additional players, including Hella Gutmann, Opus IVS, ZF Aftermarket, and TOPDON, are expanding their portfolios with advanced scanning platforms that integrate ADAS support, remote diagnostics, and AI-driven inspection logic. Many manufacturers are also incorporating artificial intelligence and machine learning to automate fault identification and enhance inspection accuracy in drive-through and under-vehicle scanning environments. Investments in cloud connectivity, cybersecurity, and modular upgrades are increasingly used to maintain a long-term competitive edge in the market, especially as regulatory and technological requirements continue to evolve.

- For instance, Snap-on’s spring 2024 diagnostic software release added new coverage plus guided tests and workflows, reinforcing its strategy of frequent updates to sustain professional tool differentiation.

LIST OF KEY VEHICLE SCANNER COMPANIES PROFILED

- Launch Tech (China)

- Topdon (China)

- Autel (China)

- Actia Group (France)

- ZF Aftermarket (Germany)

- Innova Electronics (U.S.)

- Softing Automotive (Germany)

- Opus IVS (U.S.)

- Thinkcar (China)

- Denso (Japan)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Launch Tech UK unveiled the X-431 EURO modular diagnostics platform, aimed at workshop flexibility, an example of product strategy focused on scalable configurations.

- March 2025: Bosch posted ADS X Version 6.6 update notes with additional 2024/2025 coverage and ADAS calibrations, reinforcing continual expansion of special tests and applications.

- October 2024: Snap-on announced its fall diagnostic software release, adding systems, tests, and guided workflows to keep technicians current with changing technology.

- September 2024: Hella Gutmann introduced mega macs S 20 as a more accessible multi-brand diagnostics option while retaining modern features such as DoIP and EV battery state-of-health functions.

- August 2024: Autel launched the MaxiSYS IA700 modular ADAS calibration frame system, aligning diagnostics ecosystems with calibration workflows for modern safety features.

REPORT COVERAGE

- The global vehicle scanner market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.1% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Vehicle Type, End-User, Propulsion, and Region |

|

By Product Type |

· OBD Diagnostic Scanners · Multi-System Diagnostic Scanners · OEM Branded Diagnostic Tools · Others |

|

By Vehicle Type |

· Passenger Cars · Light Commercial Vehicles · Heavy Commercial Vehicles |

|

By End-User |

· Dealerships · Independent Workshops · DIY Consumers · Others |

|

By Propulsion |

· Internal Combustion Engine · Electric |

|

By Region |

· North America (By Product Type, Vehicle Type, End-User, Propulsion, and Country) o U.S. o Canada o Mexico · Europe (By Product Type, Vehicle Type, End-User, Propulsion, and Country) o U.K. o Germany o France o Italy o Rest of Europe · Asia Pacific (By Product Type, Vehicle Type, End-User, Propulsion, and Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World (By Product Type, Vehicle Type, End-User, Propulsion, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.83 billion in 2025 and is projected to reach USD 4.40 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 1.02 billion.

The market is expected to exhibit a CAGR of 5.1% during the forecast period of 2026-2034.

The passenger cars segment leads the market by vehicle type.

Rising vehicle electronics and ADAS complexity are pushing workshops toward higher-end diagnostics, which is driving the market.

Launch Tech, Thinkcar, Opus IVS, and Autel are some of the prominent players in the market.

Asia Pacific dominates the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us