Veterinary Eye Care Market Size, Share & Industry Analysis By Product Type (Instruments [Diagnostic Equipment {Tonometers, Ophthalmic Test Kits, Electroretinogram (ERG), and Others} and Treatment & Surgical Devices {Laser Devices, Surgical Equipment, and Others}] and Consumables), By Animal Type (Companion Animals [Dogs, Cats, and Others] and Livestock Animals [Cattle, Sheep & Goats, and Others), By Disease Indication (External Eye Disorders, Corneal Disorders, Internal Eye Disorders, and Others), By End User (Veterinary Hospitals & Clinics, & Others), and Regional Forecast, 2026-2034

Veterinary Eye Care Market Size and Future Outlook

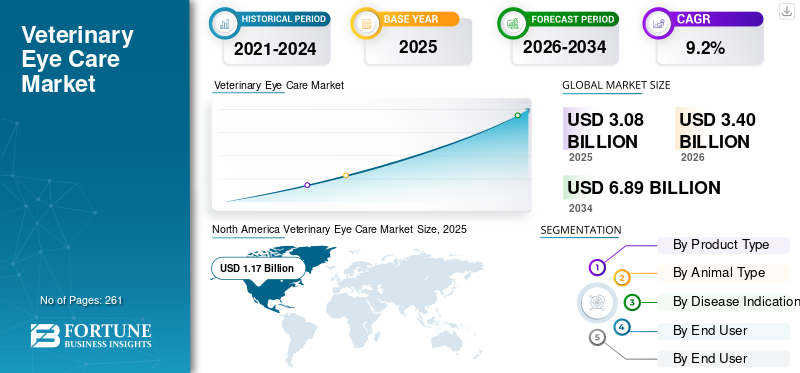

The global veterinary eye care market size was valued at USD 3.08 billion in 2025 and is projected to grow from USD 3.40 billion in 2026 to USD 6.89 billion by 2034, exhibiting a CAGR of 9.2% during the forecast period. North America dominated the veterinary eye care market with a market share of 37.99% in 2025.

Veterinary eye care is a diagnostic, surgical, and therapeutic medical device designed to evaluate, treat, and monitor ocular conditions in animals. The growing prevalence of ocular disorders among animals and rising pet ownership are further resulting in an increasing adoption of these instruments in the market. The growing veterinary healthcare expenditure is further fueling the product adoption in the market.

- For instance, according to the 2021 data published by the Veterinary Business Development Ltd, about 1,456 dogs among the total 363,898 dogs were affected by keratoconjunctivitis sicca (KCS) globally.

The rising incorporation of technological advancements in these devices among the major players, such as Bausch + Lomb, and Zoetis Services LLC, is further contributing to the demand for these products in the market.

Download Free sample to learn more about this report.

Veterinary Eye Care Market Key Takeaways

- 2025 Market Size: USD 3.08 billion

- 2026 Market Size: USD 3.40 billion

- 2034 Forecast Market Size: USD 6.89 billion

- CAGR: 9.2% from 2026–2034

- North America dominated the veterinary eye care market with a 37.99% share in 2025.

- The internal eye disorders segment is projected to grow at the fastest CAGR of 9.8% during the forecast period.

- Veterinary diagnostic laboratories are expected to expand at a CAGR of 10.7% over the study period.

North America

North America led the global market in 2025, driven by high veterinary healthcare spending, advanced veterinary infrastructure, and increasing adoption of specialized ophthalmic devices for animals.

Europe

Europe secured the second-largest market position, supported by strong adoption of animal diagnostics and stringent veterinary healthcare standards.

Asia Pacific

Asia Pacific ranked as the third-largest market, fueled by rising pet adoption rates and growing investments in livestock healthcare across emerging economies.

U.S.

The U.S. veterinary eye care market is estimated to reach approximately USD 1.16 billion by 2026, supported by increasing pet ownership and rising demand for advanced veterinary ophthalmology services.

Japan

Japan’s market is estimated at around USD 0.10 billion in 2026, driven by the increasing prevalence of ocular diseases among animals and high pet adoption rates.

Read More

Veterinary Eye Care Market Trends

Increasing Adoption of Advanced Diagnostic and Treatment Tools to Fuel Product Demand

The increasing adoption of advanced diagnostic and treatment tools that enhance accuracy, speed, and clinical outcomes is driving technological innovation in the market. The market is shifting toward portable pressure measurement, high-resolution imaging, and more advanced microsurgical devices for the management of eye disorders.

Additionally, the technologies, including optical coherence tomography (OCT), are allowing near-histologic visualization of the cornea, retina, and optic nerve, which is further supporting the adoption rate for these products in the market. Moreover, phacoemulsification with intraocular lens implantation has become the standard surgical approach for canine cataracts, contributing to the wider penetration rate for advanced veterinary eye care devices and boosting demand for specialized instruments and consumables.

- For instance, in November 2024, Photon Therapeutics LTD launched the PhotonUVC, a revolutionary new veterinary non-contact device, which treats corneal infections at the London Vet Show.

Other Prominent Trends

- Rising pet humanization

- Increasing demand for minimally invasive surgeries

- Expansion of veterinary specialty clinics

- Adoption of tele-ophthalmology

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Increasing Prevalence of Ocular Diseases to Boost Market Growth

The increasing prevalence of ocular conditions, including cataracts, glaucoma, and others, is resulting in the growing demand for routine ophthalmic screening and diagnostic devices, consequently fueling the demand for the product in the market.

- For instance, according to 2019 data published by the Royal Veterinary College, University of London, about 3,029 dogs were diagnosed with conformational eyelid disorder cases in primary veterinary care practices amongst 2,250,417 dogs in the U.K.

This, along with growth in the increasing pet population, veterinary healthcare infrastructure, and increasing spending on pet healthcare, is also contributing to the rising adoption rate of these products in the market. Therefore, the above-mentioned factors, along with increasing awareness regarding routine check-ups and preventive screening, are further contributing to the global veterinary eye care market growth.

Market Restraints

High Cost Associated with Treatment Procedures to Hamper Market Growth

The high cost of veterinary ophthalmic treatment is a major restraint limiting the adoption of advanced eye care, especially in emerging markets. Chronic ophthalmic diseases often require repeated diagnostic workups, specialist consultation, long-term medication, or surgery using highly advanced devices, including phacoemulsification systems, operating microscopes, lasers, and microsurgical instruments.

Along with this, the management and treatment of ocular disorders, including cataracts, glaucoma, and severe corneal disease, can become financially burdensome for pet owners. This often results in delayed specialist referral or reduced adherence to recommended treatment plans, thereby hampering the growth of the market.

- For instance, according to the 2025 statistics published by the American Veterinary Medical Association (AVMA), it was reported that about 4.6% decrease was observed in visits among small animal veterinary clinics in the U.S.

Market Opportunities

Expansion of Veterinary Healthcare Infrastructure to Amplify Product Demand

There is an expansion of veterinary healthcare facilities in emerging countries, such as South Africa, Mexico, and others. The growing prevalence of ocular disorders, expansion of veterinary healthcare infrastructure, and the increasing number of veterinary healthcare facilities are resulting in the adoption of veterinary eye care devices across healthcare facilities.

This, along with the growing demand for technologically advanced ophthalmic devices, including tonometers, imaging systems, surgical instruments, intraocular lenses, and others, is resulting in increasing efforts among key manufacturers to introduce novel devices, thereby creating a lucrative opportunity in the market.

- According to 2026 data published by the American Animal Hospital Association, there are more than 4,500 veterinary practices in the U.S.

Market Challenges

Limited Awareness in Developing Regions to Limit Market Growth

There is a growing demand for innovative veterinary eye care devices among the patient population. However, limited awareness and availability of technologically advanced devices, limited veterinary healthcare expenditure, regulatory constraints, and an inadequate reimbursement framework, especially in emerging nations, are resulting in limited access to advanced veterinary ophthalmic devices.

Furthermore, the limited number of veterinary healthcare facilities and the shortage of trained veterinarians are crucial factors contributing to delays in diagnostic and surgical procedures for animals, especially in emerging countries, such as Mexico and Brazil.

- For instance, according to 2024 data published by Medscape, only 21.25% of respondents demonstrated good knowledge based on the study’s assessment metrics, indicating a substantial gap in pet owner awareness in emerging-market settings.

SEGMENTATION ANALYSIS

By Product Type

Increasing Launches of Novel Instruments by Key Players Led to the Instruments Segment Dominance

Based on product type, the market is classified into instruments and consumables. Additionally, instruments are further subdivided into diagnostic equipment and treatment & surgical devices. Furthermore, diagnostic equipment is divided into tonometers, ophthalmic test kits, electroretinogram (ERG), and others. The treatment & surgical devices are segmented into laser devices, surgical equipment, and others.

The instruments segment held the largest market share in 2025. The growth is owing to the growing prevalence of ocular conditions among animals, which has increased the adoption of advanced diagnostic and surgical instruments. This, along with the growing focus of key companies on launching novel instruments, is further anticipated to contribute to the segment’s growth.

To know how our report can help streamline your business, Speak to Analyst

- For instance, in September 2025, Zoetis Services LLC is expanding the availability of its advanced, point-of-care veterinary hematology analyzer into Europe. The Vetscan OptiCell is the cartridge-based diagnostic tool powered by artificial intelligence.

The consumables segment is expected to grow at a CAGR of 8.6% over the forecast period.

By Animal Type

Increasing Prevalence of Ocular Disorders Led to the Dominance of the Companion Animals Segment

Based on animal type, the market is segmented into companion animals and livestock animals. Additionally, companion animals are segmented into dogs, cats, and others. Moreover, livestock animals are divided into cattle, sheep & goats, and others.

The companion animals segment dominated the global market, accounting for 83.1% share in 2025. The growth is due to the increasing prevalence of ocular conditions among companion animals, which has led key companies to focus on launching innovative devices, thereby supporting higher adoption rates.

- For instance, according to 2025 data published by the Indian Journal of Animal Research (IJAR), about 300 dogs suffered from various ocular affections in a total of 6,863 dogs in India.

The livestock animals segment is set to flourish with a growth rate of 8.5% across the forecast period.

By Disease Indication

Increasing Prevalence of External Disorders Led to the Dominance of the Segment

Based on disease indication, the market is segmented into external eye disorders, corneal disorders, internal eye disorders, and others.

The external eye disorders segment dominated the global market, accounting for 31.9% in 2025. The growth is due to the increasing prevalence of external eye disorders, including eyelid abnormalities, conjunctivitis, and others. The growing adoption of pets is resulting in an increasing adoption of devices, thereby contributing to the adoption rate of these devices in the market.

- For instance, according to the 2025 statistics published by the National Center for Biotechnology Information (NCBI), about 14.5% pugs suffered from eyelid abnormalities in Australia.

The internal eye disorders segment is set to flourish with a growth rate of 9.8% throughout the forecast period.

By End-user

Increasing Number of Veterinary Hospitals & Clinics Led to the Segmental Dominance

Based on end user, the market is fragmented into veterinary hospitals & clinics, veterinary diagnostic laboratories, and others.

The veterinary hospitals & clinics segment dominated the market in 2025. The increasing prevalence of ocular conditions, the growing number of veterinary hospitals & clinics, among others, are some of the vital factors supporting the segment's growth in the market. Furthermore, the segment is set to hold a 82.6% share by 2026.

- For instance, according to 2022 statistics published by the Animal Husbandry Department, it was reported that there were about 12,452 hospitals in India.

Veterinary diagnostic laboratories are projected to grow at a 10.7% CAGR during the forecast period.

Veterinary Eye Care Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Veterinary Eye Care Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market held the dominant share in 2024, valued at USD 1.06 billion, and also maintained its leading share in 2025 with USD 1.17 billion. The high veterinary healthcare spending, adoption of pets, advanced veterinary hospital infrastructure, growing number of veterinary ophthalmologists, and strong demand for specialized veterinary devices are some of the factors contributing to the growth of the market.

- For instance, according to the 2025 data published by the American Pet Products Association (APPA), 49 million U.S. households own pet cats.

U.S. Veterinary Eye Care Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.16 billion by 2026, accounting for roughly 34.1% of sales.

Europe

Europe is projected to record a growth rate of 8.1% in the coming years, which is the second-highest among all regions, and reach a valuation of USD 1.01 billion by 2026. The strong adoption of animal diagnostics and regulatory standards is likely to support market growth.

U.K. Veterinary Eye Care Market

The U.K. market is estimated at around USD 0.14 billion by 2026, representing roughly 4.1% of global revenues.

Germany Veterinary Eye Care Market

Germany’s market is projected to reach approximately USD 0.21 billion by 2026, equivalent to around 6.0% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.76 billion by 2026 and secure the position of the third-largest region in the market. The rapid growth in pet adoption and livestock healthcare investments is likely to contribute to the growth of the market. In the region, India and China are both estimated to reach USD 0.07 billion and USD 0.24 billion, respectively, by 2026.

Japan Veterinary Eye Care Market

The Japanese market in 2026 is estimated at around USD 0.10 billion, accounting for roughly 2.9% of global revenues. Japan has historically reported a relatively increasing prevalence of ocular diseases among animals, with a large adoption rate for pet animals.

China Veterinary Eye Care Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.24 billion, representing roughly 7.1% of global sales.

India Veterinary Eye Care Market

The Indian market is estimated at around USD 0.07 billion by 2026, accounting for roughly 2.1% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market is set to reach a valuation of USD 0.19 billion by 2026, driven by the growing opportunities for veterinary eye care services and rising awareness of preventive animal healthcare across the region.

The Middle East & Africa region is also expected to grow with a considerable growth rate during the forecast period. The growth is due to the rising prevalence of eye diseases such as dry eye disease, and others, along with healthcare investments in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.05 billion by 2026.

South Africa Veterinary Eye Care Market

The South African market is projected to reach around USD 0.03 billion by 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Increasing Number of Product Launches to Support Their Dominance

A strong product portfolio, along with a significant emphasis on strategic initiatives, is one of the crucial factors contributing to the dominance of key market players. Bausch + Lomb and Zoetis Services LLC are among the leading participants in the market in 2025. Moreover, the growing emphasis on strategic initiatives by key companies is strengthening their presence and is anticipated to boost the global veterinary eye care market share.

- For instance, in May 2024, Bausch + Lomb provided a USD 25,000 grant to The Seeing Eye, the non-profit organization that provides specially bred and trained dogs to guide people with blindness and low vision, with an aim to strengthen its presence in the market.

Other key players, including Reichert, Inc., and others, are also growing in the market, primarily owing to their growing focus on R&D activities to launch innovative products to strengthen their brand presence in the market.

List of Key Veterinary Eye Care Companies Profiled

- Bausch + Lomb (U.S.)

- Zoetis Services LLC (U.S.)

- Reichert, Inc. (U.S.)

- Revenio Group Oyj (Finland)

- Keeler (U.K.)

- AMETEK, Inc. (U.S.)

- an-vision (U.S.)

- Iridex Corporation (U.S.)

- Optomed (Finland)

- Norlase (Denmark)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Zoetis Inc., the world’s animal health company, acquired Neogen Corporation's animal genomics business for USD 160 million to strengthen its presence.

- March 2026: Zoetis Services LLC announced that Vetscan OptiCell has been named a Best New Companion Animal Product winner of the 2025 S&P Global Animal Health Awards, recognizing innovations that are advancing veterinary medicine and supporting the evolving needs of today’s practices.

- February 2026: AMETEK, Inc., acquired LKC Technologies, a player in functional retinal testing using electroretinography (ERG), with an aim to strengthen its market presence.

- November 2025: Zoetis Inc. acquired the Veterinary Pathology Group (VPG), a veterinary diagnostic laboratory group with multiple locations across the U.K. and Ireland. The acquisition further expands Zoetis’ comprehensive diagnostics portfolio and reinforces its commitment to advancing animal health through innovative, high-quality diagnostic solutions.

- September 2024: Reichert, Inc., a business unit of AMETEK Inc. and a player in designing, engineering, and manufacturing high-quality diagnostic instruments and equipment for ophthalmologists, optometrists, and eye care professionals, launched the Tono-Vera Vet Tonometer with ActiView Positioning System.

- May 2024: Reichert Inc., a business of AMETEK, Inc., and a global player in designing, engineering, and manufacturing diagnostic devices for eye care, announced the availability of the Tono-Vera Tonometer with ActiView Positioning System in the U.S.

- September 2023: Reichert, Inc., a business of AMETEK, Inc., showcased the all-new Tono-Vera Tonometer with ActiView Positioning System at the 41st Congress of the European Society of Cataract and Refractive Surgeons (ESCRS) in Europe and Canada.

REPORT COVERAGE

The report provides a detailed global veterinary eye care market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, animal type, disease indication, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.2% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Animal Type, Disease Indication, End User, and Region |

| By Product Type |

|

| By Animal Type |

|

| By Disease Indication |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.08 billion in 2025 and is projected to reach USD 6.89 billion by 2034.

In 2025, the North America regional market value stood at USD 1.17 billion.

Growing at a CAGR of 9.2%, the market will exhibit steady growth over the forecast period (2026-2034).

By product type, the instruments segment led the market.

The prevalence of ocular conditions is one of the key factors driving the market.

Bausch + Lomb and Zoetis Services LLC are the major players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us