Vision-Guided Inspection Equipment Market Size, Share & Industry Analysis, By Offering (Hardware, Software and Services), By Imaging Modality (2D Vision Inspection, 3D Vision Inspection, Spectral Vision Inspection, and Others), By Deployment Type (Inline/In-Process Inspection, At-Line/Near-Line Inspection, and Others) and By End-Use Industry (Electronics & Semiconductors, Automotive, Healthcare, Food & Beverage, Packaging & Printing, General Industrial Manufacturing, Aerospace & Defense, Logistics & Warehousing, and Others), and Regional Forecast, 2026-2034

Vision-Guided Inspection Equipment Market Size and Future Outlook

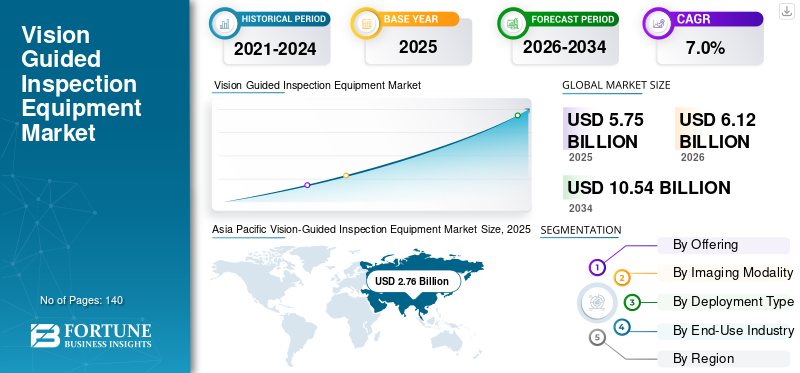

The global vision-guided inspection equipment market size was valued at USD 5.75 billion in 2025. The market is projected to grow from USD 6.12 billion in 2026 to USD 10.54 billion by 2034, exhibiting a CAGR of 7.0% during the forecast period. Asia Pacific dominated the vision guided inspection equipment market with a market share of 48.00% in 2025.

Vision-Guided Inspection Equipment (VGIE) comprises advanced automated inspection and quality assurance systems that leverage machine vision, intelligent imaging, AI-enabled analytics, and 2D and 3D vision to identify defects, verify assembly accuracy, monitor dimensional consistency, and ensure real-time production quality in industrial manufacturing environments. These systems combine specialized hardware components such as industrial cameras, optical sensors, lighting modules, frame grabbers, embedded processors, robotic inspection cells, and vision-guided robotics with software-driven image processing, deep learning algorithms, edge analytics, and remote monitoring platforms to deliver high-speed, repeatable, and precision-based inspection capabilities.

VGIE solutions are increasingly becoming a critical component of smart manufacturing ecosystems, enabling manufacturers to reduce production errors, improve traceability, minimize operational downtime, and support the growing adoption of Industry 4.0 across high-volume industrial operations. As manufacturers accelerate investments in factory automation, automotive electronics, advanced driver assistance systems ADAS, and intelligent production systems, the vision-guided inspection equipment market is witnessing sustained growth driven by rising demand for automated quality control, labor optimization, and higher production throughput.

- For instance, in January 2025, Cognex Corporation announced the launch of the In-Sight SnAPP Vision Sensor 2800, featuring enhanced AI-powered edge learning capabilities for automated defect detection and assembly verification in manufacturing environments, according to the company’s official product announcement.

Cognex Corporation, Keyence Corporation, Omron Corporation, Teledyne Technologies, Basler AG, Zebra Technologies, ISRA Vision, and National Instruments are among the major players with significant market share. Their competitive positioning is supported by strong expertise in industrial machine vision systems, advanced imaging technologies, AI-enabled inspection software, integrated automation platforms, and continuous investments in high-speed inspection capabilities, 3D imaging technologies, edge computing, and smart factory integration solutions to address the evolving requirements of precision manufacturing and industrial quality assurance.

Download Free sample to learn more about this report.

Vision Guided Inspection Equipment Market Key Takeaways

- 2025 Market Size: USD 5.75 billion

- 2026 Market Size: USD 6.12 billion

- 2034 Forecast Market Size: USD 10.54 billion

- CAGR: 7.0% from 2026–2034

- Asia Pacific dominated the market with a 48.00% share in 2025.

- Hardware held the largest market share by offering in 2025.

- 2D Vision Inspection accounted for the largest market share by imaging modality in 2025.

North America

The market reached USD 1.29 billion in 2025, supported by advanced industrial automation and semiconductor manufacturing.

Asia Pacific

The market reached USD 2.76 billion in 2025, driven by strong manufacturing and automation adoption.

Europe

The market is driven by precision manufacturing, industrial automation, and stringent quality standards across key industries.

U.S.

The market is projected to reach USD 1.09 billion in 2026.

Japan

The market is projected to reach USD 0.39 billion in 2026.

Read More

VISION-GUIDED INSPECTION EQUIPMENT MARKET TRENDS

Rising Adoption of AI-Enabled Inline Inspection Systems is Transforming Industrial Quality Control

The rapid adoption of AI-enabled inline inspection systems in high-speed manufacturing environments is driving demand for vision-guided inspection equipment. As manufacturers continue shifting toward smart factory operations and digitally connected production ecosystems, there is a growing emphasis on real-time defect detection, predictive quality control, and automated process optimization to improve production efficiency and minimize quality-related losses. Traditional manual inspection methods are gradually being replaced by intelligent vision inspection systems that continuously monitor production lines, identify microscopic defects, verify assembly accuracy, and perform traceability verification at significantly higher speed and consistency. This transition is encouraging manufacturers to integrate machine vision systems directly into automated production lines, enabling continuous inspection without interrupting throughput or increasing labor dependency.

The market is also witnessing increased deployment of AI-driven vision software, edge-based analytics, and deep learning algorithms that can adapt to changing product designs, complex surface variations, and highly dynamic manufacturing conditions. Next-generation AI-powered inspection platforms can continuously learn from production data, improve defect classification accuracy, reduce false rejection rates, and optimize inspection performance across multi-product manufacturing environments.

- For instance, in February 2025, Zebra Technologies announced the launch of Aurora Velocity, a suite of vision software enhancements designed to improve AI-powered machine vision inspection and industrial automation workflows, according to the company’s official newsroom announcement.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Smart Manufacturing and Automated Quality Control Boosts Market Growth

The vision-guided inspection equipment market growth is increasingly being driven by the rapid expansion of smart manufacturing infrastructure and the growing need for automated quality assurance across industrial production environments. As manufacturers continue transitioning toward Industry 4.0 and digitally connected factory ecosystems, there is growing demand for intelligent inspection systems that improve production accuracy, minimize defects, reduce operational downtime, and ensure real-time process visibility. Vision-guided inspection systems enable continuous, high-speed, and highly repeatable quality verification across complex manufacturing operations, making them critical for industries operating under stringent quality and traceability requirements.

- For instance, in March 2025, Omron Corporation announced the expansion of its AI-powered automation and machine vision solutions portfolio to support advanced manufacturing inspection and smart factory applications, according to the company’s official newsroom announcement.

MARKET RESTRAINTS

High System Integration Costs and Complex Industrial Deployment Limiting Broader Adoption

Market growth is constrained by the high initial investment required for advanced inspection systems, integration complexity within existing production environments, and the technical challenges of maintaining inspection accuracy across diverse manufacturing conditions. Vision-guided inspection systems require specialized cameras, optics, lighting systems, AI-enabled software, embedded processors, robotic integration capabilities, and real-time data infrastructure, resulting in significantly higher deployment and operational costs for manufacturers. Small and medium-sized enterprises often face challenges in adopting these systems due to capital limitations, integration expenses, and the need for skilled technical personnel to configure, operate, and maintain inspection platforms.

MARKET OPPORTUNITIES

Growing Adoption of AI-Driven Smart Factories and Advanced Semiconductor Manufacturing Creating New Growth Opportunities

An emerging opportunity in the market lies in the accelerating deployment of AI-driven smart factories and the rapid expansion of advanced semiconductor and electronics manufacturing capacity worldwide. As manufacturers continue modernizing production facilities with connected automation systems, industrial robotics, and data-driven manufacturing platforms, demand is growing for intelligent inspection technologies that deliver real-time quality control, adaptive defect detection, and automated production monitoring. The transition toward high-density semiconductor packaging, electric vehicle electronics, advanced battery systems, and miniaturized electronic components is further increasing the need for high-precision vision inspection systems capable of identifying microscopic defects while maintaining production consistency at high throughput.

- For instance, in April 2025, Teledyne Technologies announced expanded industrial vision capabilities through new AI-enabled imaging solutions designed to support semiconductor inspection, electronics manufacturing, and automated industrial quality control applications, according to the company’s official newsroom announcement.

MARKET CHALLENGES

High Data Processing Requirements and Complex Integration across Diverse Manufacturing Environments are Key Market Challenges

A key challenge in the market is the growing complexity of integrating advanced inspection systems into highly diverse, rapidly evolving manufacturing environments. Modern vision-guided inspection platforms generate large volumes of high-resolution imaging data that require real-time processing, AI-based analysis, and continuous system optimization to maintain inspection accuracy and production efficiency. Managing these data-intensive operations while ensuring low-latency inspection performance, especially in high-speed production environments, increases infrastructure requirements and system complexity for manufacturers.

Another major challenge is maintaining stable inspection performance across varying production conditions, product configurations, and manufacturing environments. Factors such as reflective materials, lighting variability, vibration, changes in product orientation, and inconsistent surface textures can affect imaging quality and the reliability of defect detection, requiring continuous calibration and software tuning.

Segmentation Analysis

By Offering

Hardware Segment Led Market Owing to High Deployment of Industrial Vision Components across Automated Inspection Environments

By offering, the market is segmented into hardware, software, and services.

Hardware held the largest vision-guided inspection equipment market share in 2025, as it represents the core physical infrastructure required for deploying vision-guided inspection systems across industrial manufacturing environments. This segment includes industrial cameras, optical sensors, lighting systems, frame grabbers, embedded processors, smart cameras, robotic inspection cells, and inline inspection stations that form the foundation of automated inspection operations. The increasing deployment of factory automation systems, robotic production lines, semiconductor inspection platforms, and high-speed packaging systems has significantly strengthened demand for advanced machine vision hardware capable of delivering precision inspection, real-time monitoring, and high-throughput quality control.

- For instance, in April 2025, Basler AG announced the expansion of its industrial camera portfolio with new high-performance machine vision cameras designed for factory automation, semiconductor inspection, and high-speed industrial quality control applications, according to the company’s official newsroom announcement.

Software is expected to witness the highest growth rate, with a CAGR of 8.6% over the forecast period, driven by increasing adoption of AI-powered defect detection, deep learning-based image analysis, edge analytics, predictive quality control, and cloud-connected inspection management platforms. Modern software-driven inspection solutions enable adaptive learning, real-time process optimization, advanced traceability, and automated defect classification across dynamic production environments.

To know how our report can help streamline your business, Speak to Analyst

By Imaging Modality

2D Vision Inspection Segment Led Market Owing to Its Broad Industrial Adoption across Manufacturing Operations

By imaging modality, the market is segmented into 2D vision inspection, 3D vision inspection, spectral vision inspection, and infrared vision inspection.

2D vision inspection held the largest market share in 2025, as it represents the most widely deployed and commercially established inspection across industrial manufacturing environments. The segment is extensively used for applications such as surface defect detection, label verification, barcode and code reading, assembly validation, dimensional measurement, and packaging inspection across industries including electronics, automotive, food & beverage, healthcare, and packaging & printing. Compared with more advanced imaging technologies, 2D vision systems offer lower implementation costs, faster integration into production lines, and high inspection speed, making them highly suitable for high-volume manufacturing operations. The widespread adoption of smart cameras, inline inspection systems, and AI-enabled 2D imaging platforms across factory automation environments continues to strengthen the segment’s market leadership.

Spectral vision inspection is expected to witness the highest growth rate, with a CAGR of 8.5% over the forecast period, driven by increasing demand for advanced material analysis, contamination detection, chemical composition verification, and precision inspection capabilities that extend beyond visible-light imaging. Spectral imaging technologies enable manufacturers to capture and analyze wavelength-specific information, making them highly valuable for pharmaceutical inspection, food quality analysis, semiconductor manufacturing, agricultural processing, and advanced material inspection applications.

By Deployment Type

Inline/In-Process Inspection Led Market Owing to Rising Demand for Real-Time Automated Quality Control

By deployment type, the market is segmented into inline/in-process inspection, at-line/near-line inspection, and offline/laboratory inspection.

Inline/In-Process inspection held the largest market share in 2025, as it represents the most widely adopted deployment approach for automated quality assurance across modern industrial manufacturing environments. These systems are directly integrated into production lines, enabling continuous real-time inspection, defect detection, dimensional verification, and assembly validation without interrupting manufacturing throughput. The growing adoption of smart factories, robotic production systems, semiconductor fabrication lines, automotive assembly operations, and high-speed packaging environments has significantly increased demand for inline inspection systems capable of delivering high-speed, repeatable, and precision-based quality control. In addition, manufacturers are increasingly deploying AI-enabled inline vision systems to minimize production errors, improve traceability, reduce waste, and optimize operational efficiency across large-scale manufacturing facilities.

Offline/Laboratory inspection is expected to grow at a CAGR of 5.8% over the forecast period, driven by increasing demand for high-precision inspection, detailed defect analysis, material characterization, and validation testing across industries that require advanced quality assurance capabilities.

By End-Use Industry

Electronics & Semiconductors Segment Led Market Owing to High Precision Inspection Requirements

By end-use industry, the market is segmented into electronics & semiconductors, automotive, healthcare, food & beverage, packaging & printing, general industrial manufacturing, aerospace & defense, logistics & warehousing, and others (textile & apparel, agriculture).

Electronics & semiconductors held the largest market share in 2025, as the industry requires highly precise, high-speed, and continuously automated inspection systems to support increasingly complex manufacturing processes and miniaturized component architectures. Vision-guided inspection systems are extensively deployed across semiconductor fabrication, printed circuit board (PCB) assembly, chip packaging, display manufacturing, and electronic component inspection applications to identify microscopic defects, validate assembly accuracy, and ensure production consistency. The growing demand for advanced semiconductors, consumer electronics, artificial intelligence hardware, data center infrastructure, and electric vehicle electronics is further accelerating the adoption of high-resolution 2D and 3D vision inspection technologies across electronics manufacturing facilities.

Automotive is expected to witness significant growth, with a CAGR of 7.7% over the forecast period, driven by the increasing adoption of electric vehicle manufacturing, battery production automation, robotic assembly systems, and advanced driver-assistance system (ADAS) component manufacturing.

Vision-Guided Inspection Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Vision-Guided Inspection Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific was valued at USD 2.76 billion in 2025 and is expected to remain the dominating market during the forecast period. The region’s growth is driven by rising demand for automated quality control, high-speed production inspection, and AI-enabled defect detection across industries such as automotive, electronics, healthcare, food & beverage, and packaging. Asia Pacific is emerging as a major hub for the deployment of vision-guided inspection systems due to its strong manufacturing base, growing adoption of industrial robotics, and ongoing investments in advanced production technologies.

China Vision-Guided Inspection Equipment Market

China’s market is projected to remain the dominant one in the Asia Pacific region, with 2026 revenues estimated at around USD 1.25 billion, representing roughly 20.4% of global sales.

Japan Vision-Guided Inspection Equipment Market

The Japanese market in 2026 is estimated at around USD 0.39 billion, accounting for roughly 6.3% of global sales.

India Vision-Guided Inspection Equipment Market

The Indian market in 2026 is estimated at around USD 0.40 billion, accounting for roughly 6.6% of global sales.

North America

North America accounted for USD 1.29 billion in 2025, supported by strong industrial automation adoption, expanding semiconductor and electronics manufacturing activity, and increasing investments in smart factory infrastructure across the U.S., Canada, and Mexico. Regional demand is closely linked to the growing deployment of AI-enabled quality control systems, robotic inspection platforms, and high-speed inline inspection technologies across industries such as automotive, healthcare, food & beverage, aerospace, and logistics. The region benefits from a mature industrial automation ecosystem, strong adoption of Industry 4.0 technologies, and the presence of major machine vision companies that continue to invest in intelligent inspection software, 3D imaging systems, and edge-based analytics platforms.

U.S. Vision-Guided Inspection Equipment Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 1.09 billion in 2026, driven by its advanced manufacturing infrastructure, strong presence of industrial automation providers, and increasing investments in semiconductor manufacturing, electric vehicle production, medical device manufacturing, and logistics automation. Unlike many regions, the U.S. has rapidly accelerated the adoption of AI-powered inspection systems integrated with robotic production lines, predictive quality analytics, and cloud-connected manufacturing platforms. Demand for vision-guided inspection systems is particularly strong across semiconductor fabrication, automotive assembly, pharmaceutical packaging, warehouse automation, and aerospace manufacturing applications, where high-speed, high-precision inspection and traceability capabilities are critical to maintaining production quality and regulatory compliance.

Europe

The European market is driven by strong demand for precision manufacturing, industrial automation, and advanced quality control systems across major economies, including Germany, the U.K., France, Italy, Spain, and the Netherlands. Regional demand is closely tied to the automotive, industrial machinery, pharmaceutical, packaging, and food processing sectors, where manufacturers increasingly deploy automated inspection systems to improve production efficiency, reduce defects, and comply with stringent quality and safety regulations. Europe also benefits from a well-established industrial engineering ecosystem, high adoption of robotics and smart manufacturing technologies, and ongoing investments in sustainable and digitally connected production facilities.

U.K. Vision-Guided Inspection Equipment Market

The U.K. market in 2026 is estimated at around USD 0.13 billion, representing roughly 2.1% of global sales.

Germany Vision-Guided Inspection Equipment Market

Germany’s market is projected to reach approximately USD 0.31 billion in 2026, equivalent to around 5.0% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing industrial automation investments, expanding manufacturing diversification initiatives, and the gradual adoption of smart factory technologies across GCC countries, Israel, South Africa, and North Africa. Demand for vision-guided inspection equipment in the region is closely linked to growing deployment of automated quality control systems across industries such as food & beverage, packaging, healthcare, logistics, and industrial manufacturing. GCC countries, particularly the UAE and Saudi Arabia, are actively investing in advanced manufacturing, warehouse automation, and industrial digitalization initiatives aimed at reducing dependence on traditional energy sectors and strengthening high-Deployment Type industrial capabilities.

GCC Vision-Guided Inspection Equipment Market

The GCC market is projected to reach around USD 0.13 billion in 2026, representing roughly 2.1% of the global sales.

South America

The South America market is driven by increasing industrial modernization, growing automation adoption, and expanding investments in manufacturing efficiency across key economies such as Brazil, Argentina, and Chile. Demand for vision-guided inspection equipment in the region is primarily driven by automotive manufacturing, food & beverage processing, packaging, agriculture-related industries, and general industrial production, rather than by highly advanced semiconductor or electronics manufacturing activities. Brazil and Argentina are the leading contributors in the region, supported by their relatively established manufacturing bases, the increasing deployment of automated production systems, and the gradual adoption of machine vision technologies across quality control and industrial inspection applications.

Brazil Vision-Guided Inspection Equipment Market

The market in Brazil is projected to reach around USD 0.16 billion in 2026, representing roughly 2.7% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage Driven by AI-Enabled Inspection Technologies, Industrial Automation Expertise, and Integrated Machine Vision Capabilities

The vision-guided inspection equipment market is moderately consolidated and highly Deployment Type-driven, with competitive positioning shaped by expertise in industrial machine vision systems, AI-powered inspection software, advanced imaging technologies, and integrated automation capabilities. Leading players such as Cognex Corporation, Keyence Corporation, Omron Corporation, Teledyne Technologies, Basler AG, and Zebra Technologies maintain strong market positions through broad product portfolios that combine industrial cameras, smart sensors, embedded vision systems, AI-driven analytics, and real-time inspection software to support high-speed automated manufacturing environments.

Competitive differentiation is increasingly influenced by the ability to deliver intelligent inspection platforms that support complex production environments, high-speed inline inspection, predictive quality control, and seamless integration with robotics and smart factory systems. Companies are investing heavily in deep learning-based defect detection, 3D imaging technologies, edge computing, and modular inspection architectures to improve inspection accuracy, reduce false rejection rates, and support flexible manufacturing operations across industries such as electronics, automotive, healthcare, food processing, and packaging.

- For instance, in February 2025, Zebra Technologies announced enhancements to its Aurora machine vision software platform to support AI-powered industrial inspection and advanced automation workflows, according to the company’s official newsroom announcement.

LIST OF KEY VISION-GUIDED INSPECTION EQUIPMENT COMPANIES PROFILED

- Cognex Corporation (U.S.)

- Keyence Corporation (Japan)

- Omron Corporation (Japan)

- Teledyne Technologies Incorporated (U.S.)

- Basler AG (Germany)

- Zebra Technologies Corporation (U.S.)

- ISRA Vision GmbH (Germany)

- National Instruments Corporation / Emerson (U.S.)

- Sick AG (Germany)

- Sony Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Cognex Corporation announced the launch of the In-Sight® 6900 Vision Controller powered by NVIDIA Deployment Type to support modular industrial machine vision and AI-enabled inspection applications.

- October 2025: Cognex Corporation introduced its Solutions Experience (SLX™) Logistics Portfolio, including AI-powered machine vision devices developed for logistics automation and barcode reading applications.

- April 2025: Teledyne DALSA introduced the Linea™ HS2 16k Multispectral line-scan camera, designed for high-speed machine vision inspection applications requiring advanced spectral imaging capabilities.

- March 2025: Basler AG announced the expansion of its ace 2 camera series with new high-resolution machine vision cameras developed for factory automation, semiconductor inspection, and robotics applications.

- January 2025: Cognex Corporation launched the DataMan® 290 and 390 barcode readers featuring an AI-powered Deployment Type designed to improve industrial barcode reading performance in manufacturing and logistics applications.

REPORT COVERAGE

The global vision-guided inspection equipment market analysis includes a comprehensive study of the market size & forecast across all market segments covered in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Imaging Modality, Deployment Type, End-Use Industry, and Region |

| By Offering |

|

| By Imaging Modality |

|

| By Deployment Type |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 5.75 billion in 2025 and is projected to reach USD 10.54 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 2.76 billion.

The market is expected to exhibit a CAGR of 7.0% during the forecast period (2026-2034).

By end-use industry, the electronics & semiconductors segment led the market.

Rising adoption of smart manufacturing and automated quality control is fueling market growth.

Cognex Corporation, Keyence Corporation, Omron Corporation, Teledyne Technologies, Basler AG, and Zebra Technologies are the top players in the market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us